|

市場調查報告書

商品編碼

1666683

數位取證市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Digital Forensics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

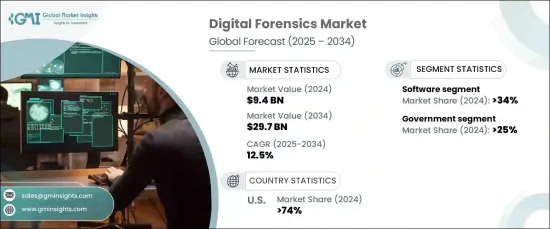

2024 年全球數位鑑識市場價值為 94 億美元,預計將經歷強勁成長,2025 年至 2034 年的複合年成長率為 12.5%。隨著企業接受數位轉型,它們面臨網路威脅的激增,包括資料外洩、勒索軟體攻擊和內部風險。這些挑戰凸顯了對先進的數位鑑識解決方案的迫切需求,以便有效地調查、緩解和預防安全事件。

雲端運算和物聯網設備的日益普及進一步加速了市場的成長。由於企業和個人嚴重依賴雲端平台和互聯系統,面臨風險的數位資料量急劇增加。數位取證工具對於分析複雜的資料環境和解決雲端和物聯網生態系統特有的安全挑戰至關重要。與物聯網設備相關的漏洞越來越多,這也增加了對保障資料完整性和重要基礎設施的取證解決方案的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 94億美元 |

| 預測值 | 297億美元 |

| 複合年成長率 | 12.5% |

數位鑑識市場分為硬體、軟體和服務。 2024 年,軟體領域佔據了 34% 的市場佔有率,預計到 2034 年將創造 100 億美元的市場價值。這些先進的工具使調查人員能夠分析海量資料集,恢復已刪除的資訊,並追蹤各種網路和設備上的惡意活動。

該市場涵蓋多個關鍵垂直行業,包括政府、BFSI(銀行、金融服務和保險)、IT 和電信、零售和醫療保健。 2024 年,政府部門佔據了 25% 的佔有率,反映了其在國家安全和監管合規方面的關鍵作用。政府機構正在增加對取證技術的投資,以打擊網路犯罪、恐怖主義和數位詐欺。用於情報和防禦目的的恢復證據和安全調查的複雜工具的需求日益成長,進一步推動了這一領域的發展。

美國數位取證市場在 2024 年佔據了 74% 的佔有率,預計到 2034 年將達到 60 億美元。大力投資研發,加上政府的舉措,推動了其主導。這些因素使美國成為數位鑑識創新和應用領域的全球領導者。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估計和計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究與驗證

- 主要來源

- 資料探勘來源

- 市場定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 供應商概況

- 數位取證硬體供應商

- 軟體供應商

- 經銷商

- 最終用途

- 利潤率分析

- 定價分析

- 專利格局

- 技術與創新格局

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 網路犯罪不斷增加

- 智慧型手機的廣泛使用

- 金融詐欺調查需求不斷成長

- 嚴格的法規和合規要求

- 產業陷阱與挑戰

- 缺乏熟練的數位鑑識專業人員

- 加密技術的使用日益廣泛

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 電腦取證

- 網路取證

- 行動裝置取證

- 雲取證

- 其他

第 6 章:市場估計與預測:按工具,2021 - 2034 年

- 主要趨勢

- 數據採集與保存

- 法醫資料分析

6.4 審查和報告

- 法醫解密

- 其他

第7章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 硬體

- 軟體

- 服務

第 8 章:市場估計與預測:按垂直產業,2021 - 2034 年

- 主要趨勢

- 金融保險業協會

- 衛生保健

- 政府

- 資訊科技和電信

- 零售

- 其他

第 9 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Autopsy

- Cellebrite

- Cisco

- Check Point Software

- Cyrebro

- ExtraHop

- Exterro

- Global Digital Forensics

- IBM Corporation

- Imperva

- KLDiscovery

- LogRythm

- Magnet Forensics

- Microsoft

- MSAB

- Nuix

- OpenText

- Oxygen Forensics

- Paraben

- Parrot Security

- Sanyo Special Steel Co.,

- Shriram Pistons & Rings

- Thyssenkrupp

- Tupy SA

- Wiseco Piston Company

- Yasunaga

The Global Digital Forensics Market, valued at USD 9.4 billion in 2024, is projected to experience robust growth, with a CAGR of 12.5% from 2025 to 2034. This expansion is fueled by the increasing complexity and prevalence of cybercrimes. As businesses embrace digital transformation, they face a surge in cyber threats, including data breaches, ransomware attacks, and insider risks. These challenges highlight the critical need for advanced digital forensics solutions to investigate, mitigate, and prevent security incidents effectively.

The rising adoption of cloud computing and IoT devices further accelerates market growth. With businesses and individuals heavily relying on cloud platforms and interconnected systems, the volume of digital data at risk has surged dramatically. Digital forensics tools are indispensable in analyzing intricate data environments and addressing security challenges unique to cloud and IoT ecosystems. The growing vulnerabilities linked to IoT devices have amplified the demand for forensic solutions that safeguard data integrity and protect vital infrastructures.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.4 Billion |

| Forecast Value | $29.7 Billion |

| CAGR | 12.5% |

The digital forensics market is segmented into hardware, software, and services. In 2024, the software segment accounted for 34% of the market share and is on track to generate USD 10 billion by 2034. Software solutions lead the market due to their ability to streamline and automate investigative processes, delivering enhanced accuracy and efficiency. These advanced tools empower investigators to analyze massive datasets, recover deleted information, and trace malicious activities across various networks and devices.

The market spans several key industry verticals, including government, BFSI (banking, financial services, and insurance), IT and telecom, retail, and healthcare. In 2024, the government sector claimed a 25% share, reflecting its pivotal role in national security and regulatory compliance. Government agencies are increasingly investing in forensic technologies to combat cybercrime, terrorism, and digital fraud. The growing demand for sophisticated tools to recover evidence and secure investigations for intelligence and defense purposes is further propelling this segment.

The U.S. digital forensics market accounted for a commanding 74% share in 2024 and is projected to reach USD 6 billion by 2034. The country's advanced technological infrastructure and high cybercrime rates have created a significant demand for cutting-edge digital forensics solutions. Strong investments in research and development, coupled with government initiatives, drive its dominance. These factors position the U.S. as a global leader in digital forensics innovation and adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Digital forensics hardware providers

- 3.2.2 Software providers

- 3.2.3 Distributors

- 3.2.4 End use

- 3.3 Profit margin analysis

- 3.4 Pricing analysis

- 3.5 Patent Landscape

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising cybercrimes

- 3.9.1.2 The wide use of smartphones

- 3.9.1.3 Rising demand in financial fraud investigation

- 3.9.1.4 Stringent regulations and compliance requirements

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Shortage of skilled digital forensic professionals

- 3.9.2.2 Increasing use of encryption technologies

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Computer forensics

- 5.3 Network forensics

- 5.4 Mobile device forensics

- 5.5 Cloud forensics

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Tools, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Data acquisition & preservation

- 6.3 Forensic data analysis

6.4 Review and reporting

- 6.5 Forensic decryption

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Hardware

- 7.3 Software

- 7.4 Service

Chapter 8 Market Estimates & Forecast, By Industry Vertical, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 Healthcare

- 8.4 Government

- 8.5 IT & telecom

- 8.6 Retail

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Autopsy

- 10.2 Cellebrite

- 10.3 Cisco

- 10.4 Check Point Software

- 10.5 Cyrebro

- 10.6 ExtraHop

- 10.7 Exterro

- 10.8 Global Digital Forensics

- 10.9 IBM Corporation

- 10.10 Imperva

- 10.11 KLDiscovery

- 10.12 LogRythm

- 10.13 Magnet Forensics

- 10.14 Microsoft

- 10.15 MSAB

- 10.16 Nuix

- 10.17 OpenText

- 10.18 Oxygen Forensics

- 10.19 Paraben

- 10.20 Parrot Security

- 10.21 Sanyo Special Steel Co.,

- 10.22 Shriram Pistons & Rings

- 10.23 Thyssenkrupp

- 10.24 Tupy S.A.

- 10.25 Wiseco Piston Company

- 10.26 Yasunaga

亞太地區數位鑑識 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030 年)

亞太地區數位鑑識 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030 年) 北美數位鑑識:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

北美數位鑑識:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 歐洲數位鑑識:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

歐洲數位鑑識:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 數位取證市場規模、佔有率、成長分析,按組件、按類型、按部署模式、按行業、按地區 - 行業預測,2024-2031 年

數位取證市場規模、佔有率、成長分析,按組件、按類型、按部署模式、按行業、按地區 - 行業預測,2024-2031 年 數位取證市場:按類型、按組件、按部署、按應用、按行業 - 2025-2030 年全球預測

數位取證市場:按類型、按組件、按部署、按應用、按行業 - 2025-2030 年全球預測 全球AI驅動數位鑑識市場:市場規模、佔有率、趨勢分析報告 - 按部署模型、按組件、按應用程式、按組織規模、按最終用途、按地區、展望和預測,2024-2031年

全球AI驅動數位鑑識市場:市場規模、佔有率、趨勢分析報告 - 按部署模型、按組件、按應用程式、按組織規模、按最終用途、按地區、展望和預測,2024-2031年 按組件、類型、工具、最終用戶、地區、範圍和預測劃分的全球數位取證市場規模

按組件、類型、工具、最終用戶、地區、範圍和預測劃分的全球數位取證市場規模 數位取證市場,按組件、類型、部署、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

數位取證市場,按組件、類型、部署、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 全球數位取證市場規模、佔有率和趨勢分析報告(依組件、部署模式(雲端和本地)、類型、產業、區域展望和預測,2024 - 2031 年)

全球數位取證市場規模、佔有率和趨勢分析報告(依組件、部署模式(雲端和本地)、類型、產業、區域展望和預測,2024 - 2031 年) 數位鑑識的全球市場的分析與預測(~2033年):類型,產品,服務,技術,零組件,用途,設備,流程,展開,終端用戶

數位鑑識的全球市場的分析與預測(~2033年):類型,產品,服務,技術,零組件,用途,設備,流程,展開,終端用戶