|

市場調查報告書

商品編碼

1666698

家用冰箱和冰櫃市場機會、成長動力、產業趨勢分析和 2024 - 2032 年預測Household Refrigerators and Freezers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 - 2032 |

||||||

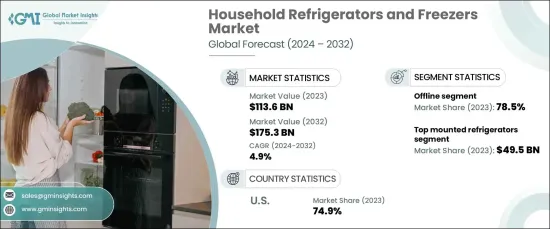

2023 年全球家用冰箱和冰櫃市場價值為 1,136 億美元,預計 2024 年至 2032 年期間的複合年成長率為 4.9%。

製造商正透過引入自動除霜和精確溫度控制等先進技術來提高能源效率。政府支持環保家電的政策和激勵措施進一步放大了這一趨勢,使永續選擇對消費者更具吸引力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2023 |

| 預測年份 | 2024-2032 |

| 起始值 | 1136億美元 |

| 預測值 | 1753億美元 |

| 複合年成長率 | 4.9% |

智慧技術的融合正在重塑家電市場。現代冰箱和冷凍機現在具有 Wi-Fi 連接、互動式觸控螢幕和虛擬助理相容性,提供更大的便利性和個人化。這些進步使用戶能夠遠端控制電器、接收警報和最佳化食物儲存,從而增強整體用戶體驗。

都市化,特別是發展中地區的都市化,有助於提高可支配收入和擴大中產階級。這種轉變推動了對先進家用電器的需求,這些電器透過提供高效、便利和創新的功能來滿足現代生活方式。

就產品類型而言,市場包括頂置式、底置式、對開門式和法式門冰箱等類別。其中,頂置式冰箱佔據市場主導地位,銷售額可觀,成長軌跡穩健。它們之所以受歡迎,是因為其成本效益和高效的冷卻動力,吸引了廣泛的消費者群體。

就分銷管道而言,市場分為線上和線下部分。線下通路佔據最大的市場佔有率,因為消費者通常更喜歡在購買之前親自評估電器。實體店提供了親身體驗產品、獲得個人化幫助以及享受促銷或延長保固的機會,從而增強了消費者的信任和滿意度。

從地區來看,美國引領北美家用冰箱和冰櫃市場,佔有相當大的佔有率。高可支配收入和智慧家庭技術的廣泛採用等因素推動了對先進和優質家電的需求。人們對智慧冰箱的日益青睞,符合將技術融入日常生活以實現便利和高效的日益成長的趨勢。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 節能電器需求不斷成長

- 技術進步和智慧功能

- 都市化和可支配所得不斷提高

- 產業陷阱與挑戰

- 延長更換週期

- 消費者的價格敏感性

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按產品,2021-2032 年

- 主要趨勢

- 頂置式冰箱

- 底部安裝冰箱

- 並排冰箱

- 法式對開門冰箱

第6章:市場估計與預測:依產能,2021-2032 年

- 主要趨勢

- 小於 15 立方英尺。英尺。

- 16 立方英尺英尺到 30 立方英尺。英尺。

- 超過30立方英尺。英尺。

第7章:市場估計與預測:依結構,2021-2032 年

- 主要趨勢

- 內建

- 獨立式

第 8 章:市場估計與預測:按價格範圍,2021 年至 2032 年

- 主要趨勢

- 低的

- 中等的

- 高的

第 9 章:市場估計與預測:依最終用途,2021-2032 年

- 主要趨勢

- 住宅

- 商業的

第 10 章:市場估計與預測:按配銷通路,2021-2032 年

- 主要趨勢

- 線上

- 電子商務

- 公司網站

- 離線

- 百貨公司

- 大賣場/超市

- 專業零售商

- 其他

第 11 章:市場估計與預測:按地區,2021-2032 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 12 章:公司簡介

- BSH

- Electrolux

- GE Appliances

- Godrej

- Haier

- Hisense

- Hitachi

- LG

- Liebherr

- Midea

- Panasonic

- Samsung

- Sub-Zero

- Toshiba

- Whirlpool

The Global Household Refrigerators And Freezers Market was valued at USD 113.6 billion in 2023 and is projected to grow at a 4.9% CAGR from 2024 to 2032. Rising environmental awareness among consumers drives demand for energy-efficient appliances that reduce electricity consumption and have minimal environmental impact.

Manufacturers are responding by introducing advanced technologies like automatic defrost and precise temperature control to enhance energy efficiency. Government policies and incentives supporting eco-friendly appliances further amplify this trend, making sustainable options more attractive to consumers.

| Market Scope | |

|---|---|

| Start Year | 2023 |

| Forecast Year | 2024-2032 |

| Start Value | $113.6 Billion |

| Forecast Value | $175.3 Billion |

| CAGR | 4.9% |

The integration of smart technologies is reshaping the household appliances market. Modern refrigerators and freezers now feature Wi-Fi connectivity, interactive touch screens, and virtual assistant compatibility, offering greater convenience and personalization. These advancements enable users to control appliances remotely, receive alerts, and optimize food storage, enhancing the overall user experience.

Urbanization, particularly in developing regions, contributes to higher disposable incomes and the expansion of the middle class. This shift is fueling demand for advanced household appliances that cater to modern lifestyles by providing efficiency, convenience, and innovative features.

In terms of product types, the market includes categories such as top-mounted, bottom-mounted, side-by-side, and French door refrigerators. Among these, top-mounted refrigerators dominate the market with significant revenue and a steady growth trajectory. Their popularity is attributed to cost-effectiveness and efficient cooling dynamics, appealing to a broad consumer base.

Regarding distribution channels, the market is divided into online and offline segments. Offline channels account for the largest market share, as consumers often prefer to assess appliances in person before making purchases. Physical stores provide the opportunity to experience products firsthand, receive personalized assistance, and benefit from promotions or extended warranties, enhancing consumer trust and satisfaction.

Regionally, the U.S. leads the North American household refrigerators and freezers market, holding a significant share. Factors such as high disposable incomes and the widespread adoption of smart home technologies drive demand for advanced and premium appliances. The increasing preference for smart refrigerators aligns with the growing trend of integrating technology into daily living for convenience and efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021-2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for energy-efficient appliances

- 3.6.1.2 Technological advancements and smart features

- 3.6.1.3 Increasing urbanization and disposable income

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Extended replacement cycles

- 3.6.2.2 Price sensitivity among consumers

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021-2032 (USD Billion)

- 5.1 Key trends

- 5.2 Top mounted refrigerators

- 5.3 Bottom mounted refrigerators

- 5.4 Side-by-side refrigerators

- 5.5 French door refrigerators

Chapter 6 Market Estimates & Forecast, By Capacity, 2021-2032 (USD Billion)

- 6.1 Key trends

- 6.2 Less than 15 cu. Ft.

- 6.3 16 cu. Ft to 30 cu. Ft.

- 6.4 More than 30 cu. Ft.

Chapter 7 Market Estimates & Forecast, By Structure, 2021-2032 (USD Billion)

- 7.1 Key trends

- 7.2 Built-in

- 7.3 Freestanding

Chapter 8 Market Estimates & Forecast, By Price Range, 2021-2032 (USD Billion)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates & Forecast, By End use, 2021-2032 (USD Billion)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021-2032 (USD Billion)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce

- 10.2.2 Company websites

- 10.3 Offline

- 10.3.1 Departmental stores

- 10.3.2 Hypermarkets/supermarkets

- 10.3.3 Specialty retailers

- 10.3.4 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021-2032 (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 BSH

- 12.2 Electrolux

- 12.3 GE Appliances

- 12.4 Godrej

- 12.5 Haier

- 12.6 Hisense

- 12.7 Hitachi

- 12.8 LG

- 12.9 Liebherr

- 12.10 Midea

- 12.11 Panasonic

- 12.12 Samsung

- 12.13 Sub-Zero

- 12.14 Toshiba

- 12.15 Whirlpool

日本冰箱市場:依產品類型、類型、部署類型、容量、最終用途、技術、價格、通路、地區、機會、預測,2018 -2032年印度冰箱市場:依產品類型、類型、部署類型、容量、最終用途、技術、價格、通路、地區、機會、預測,2018 -2032年

日本冰箱市場:依產品類型、類型、部署類型、容量、最終用途、技術、價格、通路、地區、機會、預測,2018 -2032年印度冰箱市場:依產品類型、類型、部署類型、容量、最終用途、技術、價格、通路、地區、機會、預測,2018 -2032年 冰箱市場機會、成長動力、產業趨勢分析及2025-2034年預測家用對開式冰箱:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)印度冰箱:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲家用對開式冰箱:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)法國國內對開式冰箱:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

冰箱市場機會、成長動力、產業趨勢分析及2025-2034年預測家用對開式冰箱:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)印度冰箱:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲家用對開式冰箱:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)法國國內對開式冰箱:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 房車冰箱市場:按類型、尺寸、電源、門類型、分銷管道分類 - 2025-2030 年全球預測

房車冰箱市場:按類型、尺寸、電源、門類型、分銷管道分類 - 2025-2030 年全球預測 冰箱市場規模、佔有率、成長分析、按技術、按產品類型、按冷凍庫、按分銷管道、按地區 - 行業預測,2024-2031 年北美家用冰箱和冷凍庫市場規模、佔有率和趨勢分析報告:2025-2030 年按設備、結構、容量、價格分佈範圍、地區和細分市場進行的預測

冰箱市場規模、佔有率、成長分析、按技術、按產品類型、按冷凍庫、按分銷管道、按地區 - 行業預測,2024-2031 年北美家用冰箱和冷凍庫市場規模、佔有率和趨勢分析報告:2025-2030 年按設備、結構、容量、價格分佈範圍、地區和細分市場進行的預測