|

市場調查報告書

商品編碼

1684194

實驗室真空幫浦市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Laboratory Vacuum Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

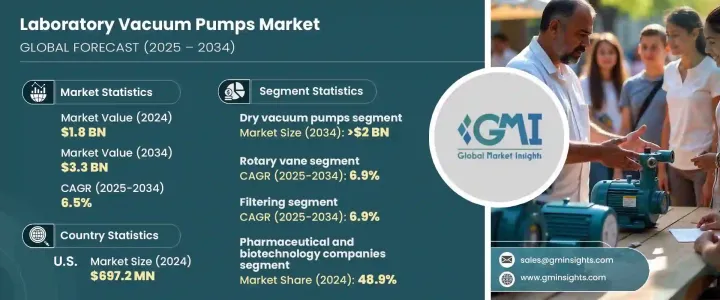

2024 年全球實驗室真空幫浦市場價值為 18 億美元,預計 2025 年至 2034 年期間的複合年成長率為 6.5%。這些產業的實驗室依靠真空幫浦來進行藥物開發、滅菌和乾燥等關鍵應用。隨著全球慢性病盛行率不斷上升,對診斷工具和實驗室設備的需求也不斷增加,進一步推動了真空幫浦市場的擴張。此外,隨著醫療保健計劃推動更準確的診斷和更有效率的藥物開發過程,實驗室真空幫浦在確保實現這些進步方面發揮著至關重要的作用。

技術創新,特別是無油和節能真空幫浦的技術創新也推動了市場的成長。隨著人們對永續性的認知不斷提高以及對實驗室設備的嚴格規定,製造商現在專注於創造高性能、環保的解決方案。這種向綠色技術的轉變不僅滿足了監管要求,而且擴大了真空幫浦在不同實驗室環境中的應用範圍。因此,真空幫浦在實驗室環境中變得越來越重要,可以提高效率、永續性和性能。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 18億美元 |

| 預測值 | 33億美元 |

| 複合年成長率 | 6.5% |

市場按產品類型細分,包括濕式真空幫浦、真空幫浦和乾式真空幫浦。乾式真空幫浦領域預計將實現最高成長,預計複合年成長率為 6.8%,到 2034 年將達到 20 億美元。它們的無油設計在純度至關重要的環境中至關重要,使其非常適合乾燥和過濾等應用。

就技術而言,實驗室真空幫浦市場分為旋片式、旋轉式螺桿式、旋轉爪式和其他技術。旋片真空幫浦市場將佔據主導地位,預計複合年成長率為 6.9%,到 2034 年達到 15 億美元。 這些幫浦以其在過濾、乾燥和蒸餾等應用中的可靠性和多功能性而聞名。其耐用的設計確保了穩定的真空水平,使其成為製藥和工業實驗室必不可少的工具。

在美國,實驗室真空幫浦市場規模在 2024 年達到 6.972 億美元,預計將繼續推動市場成長,預計 2025 年至 2034 年的複合年成長率為 5.9%。 這一成長得益於美國在製藥和生物技術領域的領導地位,對先進實驗室的需求不斷增加,以支持新的醫療保健計劃和創新。

目錄

第 1 章:方法論與範圍

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 醫療保健領域對診斷實驗室的需求不斷增加

- 製藥和生物技術研究活動的成長

- 需要真空技術的先進醫療設備日益普及

- 擴大生物製藥產業和疫苗生產

- 產業陷阱與挑戰

- 某些真空幫浦的維護挑戰和營運成本

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 差距分析

- 波特的分析

- PESTEL 分析

- 未來市場趨勢

- 價值鏈分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第 5 章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 乾式真空幫浦

- 濕式真空幫浦

- 組合真空幫浦

第6章:市場估計與預測:按技術,2021 - 2034 年

- 主要趨勢

- 旋片式

- 旋轉螺桿

- 旋爪

- 其他技術

第 7 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 濾

- 烘乾

- 蒸餾

- 其他應用

第 8 章:市場估計與預測:按最終用途,2021 - 2034 年

- 主要趨勢

- 製藥和生物技術公司

- 醫院和診斷實驗室

- 學術和研究機構

- 其他最終用戶

第 9 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Agilent

- Atlas Copco

- BUSCH

- DEKKER

- Ebara Technologies

- EDWARDS

- gast

- Graham

- KNF

- Leybold

- PFEIFFER

- SHIMADZU

- ULVAC

- VACUUBRAND

- WELCH

The Global Laboratory Vacuum Pumps Market was valued at USD 1.8 billion in 2024 and is projected to experience a CAGR of 6.5% from 2025 to 2034. This growth is primarily attributed to the booming pharmaceutical and biotechnology sectors, increasing investment in research and development (R&D), and the escalating need for advanced diagnostic solutions. Laboratories in these industries depend on vacuum pumps for critical applications such as drug development, sterilization, and drying. As the global prevalence of chronic diseases continues to rise, so does the demand for diagnostic tools and laboratory equipment, further driving the vacuum pump market expansion. Additionally, as healthcare initiatives push for more accurate diagnostics and efficient drug development processes, laboratory vacuum pumps play an essential role in ensuring these advancements can be achieved.

Technological innovations, particularly in oil-free and energy-efficient vacuum pumps, are also fueling market growth. With heightened awareness around sustainability and stringent regulations on laboratory equipment, manufacturers are now focusing on creating high-performance, eco-friendly solutions. This shift toward green technologies not only meets regulatory demands but also expands the range of applications for vacuum pumps in diverse laboratory environments. As such, vacuum pumps are becoming increasingly integral to laboratory settings, enhancing efficiency, sustainability, and performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 6.5% |

The market is segmented by product type, including wet vacuum pumps, vacuum pumps, and dry vacuum pumps. The dry vacuum pumps segment is expected to see the highest growth, projected to grow at a CAGR of 6.8%, reaching USD 2 billion by 2034. These pumps are especially favored in industries like pharmaceuticals and biotechnology for their contamination-free operation and low maintenance needs. Their oil-free design is critical in environments where purity is paramount, making them highly suitable for applications such as drying and filtration.

Regarding technology, the laboratory vacuum pumps market is divided into rotary vane, rotary screw, rotary claw, and other technologies. The rotary vane vacuum pump segment is set to dominate, expected to grow at a CAGR of 6.9%, reaching USD 1.5 billion by 2034. These pumps are renowned for their reliability and versatility in applications such as filtration, drying, and distillation. Their durable design ensures stable vacuum levels, making them an essential tool in both pharmaceutical and industrial laboratories.

In the U.S., the laboratory vacuum pumps market reached USD 697.2 million in 2024 and is projected to continue driving market growth, with an expected CAGR of 5.9% from 2025 to 2034. This growth is fueled by the nation's leadership in the pharmaceutical and biotechnology sectors, with increasing demand for advanced laboratory equipment to support new healthcare initiatives and innovative drug development.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for diagnostic laboratories in the healthcare sector

- 3.2.1.2 Growth in pharmaceutical and biotechnology research activities

- 3.2.1.3 Rising adoption of advanced medical devices requiring vacuum technology

- 3.2.1.4 Expanding biopharmaceutical industry and vaccine production

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Maintenance challenges and operational costs of certain vacuum pumps

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dry vacuum pumps

- 5.3 Wet vacuum pumps

- 5.4 Combination vacuum pumps

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Rotary vane

- 6.3 Rotary screw

- 6.4 Rotary claw

- 6.5 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Filtering

- 7.3 Drying

- 7.4 Distillation

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical and biotechnology companies

- 8.3 Hospitals and diagnostic labs

- 8.4 Academic and research institutes

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Agilent

- 10.2 Atlas Copco

- 10.3 BUSCH

- 10.4 DEKKER

- 10.5 Ebara Technologies

- 10.6 EDWARDS

- 10.7 gast

- 10.8 Graham

- 10.9 KNF

- 10.10 Leybold

- 10.11 PFEIFFER

- 10.12 SHIMADZU

- 10.13 ULVAC

- 10.14 VACUUBRAND

- 10.15 WELCH

渦輪分子幫浦市場規模、佔有率和成長分析(按類型、最大抽速、應用和地區)- 產業預測 2025-2032實驗室真空幫浦市場規模、佔有率和成長分析(按產品、技術、應用、最終用途和地區)- 產業預測 2025-2032液環真空幫浦市場按類型、材料、應用和地區分類

渦輪分子幫浦市場規模、佔有率和成長分析(按類型、最大抽速、應用和地區)- 產業預測 2025-2032實驗室真空幫浦市場規模、佔有率和成長分析(按產品、技術、應用、最終用途和地區)- 產業預測 2025-2032液環真空幫浦市場按類型、材料、應用和地區分類 2025 年全球液環真空幫浦市場報告

2025 年全球液環真空幫浦市場報告 實驗室真空幫浦市場,按技術、按產品、按應用、按最終用途、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

實驗室真空幫浦市場,按技術、按產品、按應用、按最終用途、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 全球流量控制 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)真空幫浦:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)轉葉真空幫浦:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

全球流量控制 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)真空幫浦:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)轉葉真空幫浦:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 流量控制市場:按設備類型、應用分類 - 2025-2030 年全球預測真空幫浦市場:按產品類型、技術、操作方法和最終用戶分類 - 2025-2030 年全球預測

流量控制市場:按設備類型、應用分類 - 2025-2030 年全球預測真空幫浦市場:按產品類型、技術、操作方法和最終用戶分類 - 2025-2030 年全球預測