|

市場調查報告書

商品編碼

1684766

電動二輪車市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Electric Two-wheeler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

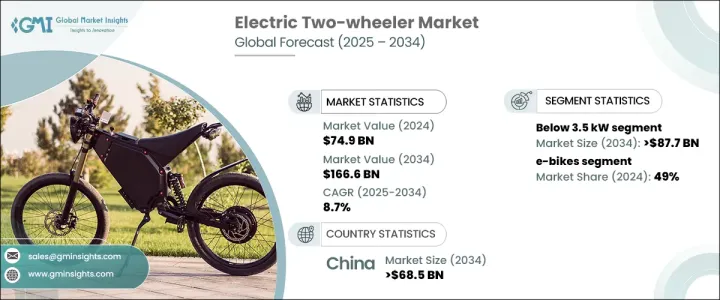

2024 年全球電動二輪車市場價值為 749 億美元,預計 2025 年至 2034 年期間將以 8.7% 的強勁複合年成長率擴張。需求激增受到多種因素的推動,包括對環保交通解決方案的日益關注、政府激勵措施以及解決城市堵塞的需要。隨著世界各國尋求減少碳排放和對化石燃料的依賴,電動二輪車已成為關鍵的解決方案,為消費者提供了一種經濟實惠、高效且環保的交通方式。隨著許多國家推出補貼、退稅和優惠政策,這些電動替代品正變得越來越可以被更廣泛的消費者群體所接受。

城市化在推動市場成長方面發揮關鍵作用,因為交通堵塞加劇了對緊湊、高效、便利的交通解決方案的需求。電動二輪車以其體積小、運行平穩、易於在擁擠的城市環境中行駛而聞名,正迅速成為人們的首選。此外,隨著越來越多的人選擇使用車輛來連接家庭、工作場所和公共交通站之間的距離,對這些車輛進行最後一英里連接的日益依賴也推動了市場擴張。電動滑板車和租賃自行車等共享旅遊服務的成長進一步促進了電動二輪車的廣泛採用,有助於提升其作為主流交通方式的地位。隨著電動車型價格越來越便宜,以及消費者對環保出行益處的認知不斷增強,電動車市場預計將繼續成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 749億美元 |

| 預測值 | 1666億美元 |

| 複合年成長率 | 8.7% |

依馬達功率分類,市場分為3.5kW以下、3.5kW-6.5kW、6.5kW以上三類。 2024 年,馬達功率低於 3.5 kW 的市場將佔據主導地位,佔有 54% 的佔有率。預計到 2034 年,這一類別將創造 877 億美元的收入,因為這些車輛因其經濟實惠、實用性以及適合短途城市旅行而被廣泛選為日常通勤車輛。它們主要設計用於城市和郊區,在性能和成本之間實現了完美平衡,因此對於注重預算的消費者特別有吸引力。

就車輛類型而言,市場包括電動摩托車、電動踏板車、電動自行車和電動滑板車。 2024 年,電動自行車佔據了 49% 的市場佔有率,其吸引力還在持續成長。電動自行車兼具經濟實惠、多功能性和永續性,吸引了從城市通勤者到休閒騎行者的廣泛消費者。電動自行車具有輕巧的設計、踏板輔助功能和長壽命的電池,已成為尋求實用且環保的交通解決方案的人的熱門選擇。

中國繼續引領電動二輪車市場,到 2024 年將佔 48% 的佔有率。在強勁的國內生產、不斷成長的消費需求和政府支持政策的共同推動下,預計到 2034 年,中國市場將創造 685 億美元。憑藉成熟的製造生態系統和對電動車基礎設施的持續投資,中國在該領域的主導地位預計將保持強勁。該國的優惠法規、免稅和激勵措施正在推動電動二輪車的廣泛普及,使其成為全球市場上最大的參與者。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估計和計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究與驗證

- 主要來源

- 資料探勘來源

- 市場定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 技術提供者

- 零件供應商

- 原始設備製造商

- 最終用戶

- 供應商概況

- 利潤率分析

- 技術與創新格局

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 燃料價格上漲和成本效益

- 政府激勵措施和政策

- 都市化與最後一哩旅行需求

- 提高環保意識與永續發展目標

- 產業陷阱與挑戰

- 先進模型的初始成本較高

- 充電基礎設施有限

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 電動摩托車

- 電動滑板車

- 電動自行車

- 電動滑板車

第6章:市場估計與預測:按電池,2021 - 2034 年

- 主要趨勢

- 服務等級協定

- 鋰離子

第 7 章:市場估計與預測:按馬達功率,2021 - 2034 年

- 主要趨勢

- 3.5千瓦以下

- 3.5 千瓦 – 6.5 千瓦

- 6.5千瓦以上

第 8 章:市場估計與預測:按電壓,2021 - 2034 年

- 主要趨勢

- 48伏

- 60 伏

- 72伏

- 其他

第 9 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Ampere Vehicles

- Ather Energy Pvt. Ltd.

- Bajaj Auto Ltd.

- Emflux Motors

- Giant Bicycles

- Gogoro Inc.

- Hero Electric Vehicles Pvt. Ltd.

- Jiangsu Xinri E-Vehicle Co. Ltd.

- Niu Technologies

- Ola Electric Mobility Pvt. Ltd.

- PURE EV

- Revolt Motors

- Super Soco

- Tork Motors

- TVS Motor Company

- Ultraviolette Automotive Pvt. Ltd.

- VMOTO SOCO Italy SRL

- Yadea Group Holdings Ltd.

- Yamaha Motor Company

- Zero Motorcycles Inc.

The Global Electric Two-Wheeler Market, valued at USD 74.9 billion in 2024, is expected to expand at a robust CAGR of 8.7% from 2025 to 2034. The surge in demand is being fueled by various factors, including the increasing focus on eco-friendly transportation solutions, governmental incentives, and the need to address urban congestion. As the world seeks to cut carbon emissions and reduce dependency on fossil fuels, electric two-wheelers have become a key solution, offering consumers an affordable, efficient, and environmentally conscious mode of transport. With many countries rolling out subsidies, tax rebates, and favorable policies, these electric alternatives are becoming more accessible to a broader consumer base.

Urbanization is playing a pivotal role in driving market growth, as rising traffic congestion intensifies the demand for compact, efficient, and convenient transportation solutions. Electric two-wheelers, known for their small size, smooth operation, and ease of maneuvering through crowded urban environments, are rapidly becoming the go-to choice. Moreover, the increasing reliance on these vehicles for last-mile connectivity is fueling market expansion as more people opt for them to bridge the gap between homes, workplaces, and public transportation stations. The growth of shared mobility services, including electric scooters and bikes for rentals, further contributes to the widespread adoption of electric two-wheelers, helping to elevate their role as a mainstream mode of transport. As electric models become more affordable and consumer awareness about the benefits of eco-friendly mobility grows, the market is poised for continued growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $74.9 Billion |

| Forecast Value | $166.6 Billion |

| CAGR | 8.7% |

In terms of motor power, the market is divided into three categories: below 3.5 kW, 3.5 kW-6.5 kW, and above 6.5 kW. The segment with motor power below 3.5 kW dominated the market in 2024, holding a 54% share. This category is expected to generate USD 87.7 billion by 2034, as these vehicles are widely chosen for daily commutes due to their affordability, practicality, and suitability for short urban trips. Designed primarily for city and suburban use, they strike a perfect balance between performance and cost, making them especially attractive to budget-conscious consumers.

Regarding vehicle types, the market includes electric motorcycles, electric scooters, e-bikes, and electric kick scooters. E-bikes represented 49% of the market share in 2024, with their appeal continuing to grow. Offering a blend of affordability, versatility, and sustainability, e-bikes attract a wide range of consumers-from urban commuters to recreational riders. With lightweight designs, pedal-assist capabilities, and long-lasting batteries, e-bikes have become a popular choice for those seeking a practical yet eco-friendly transportation solution.

China continues to lead the electric two-wheeler market, holding a 48% share in 2024. The country's market is expected to generate USD 68.5 billion by 2034, driven by a combination of strong domestic production, increasing consumer demand, and supportive government policies. With an established manufacturing ecosystem and ongoing investments in electric mobility infrastructure, China's dominance in the sector is expected to remain strong. The country's favorable regulations, tax exemptions, and incentives are encouraging the widespread adoption of electric two-wheelers, making it the largest player in the market globally.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Technology providers

- 3.1.2 Component suppliers

- 3.1.3 OEMs

- 3.1.4 End user

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising fuel prices and cost-effectiveness

- 3.7.1.2 Government incentives and policies

- 3.7.1.3 Urbanization and demand for last-mile mobility

- 3.7.1.4 Rising environmental awareness and sustainability goals

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High initial costs for advanced models

- 3.7.2.2 Limited charging infrastructure

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Electric motorcycle

- 5.3 Electric scooter

- 5.4 E-bikes

- 5.5 Electric kick scooter

Chapter 6 Market Estimates & Forecast, By Battery, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 SLA

- 6.3 Li-ion

Chapter 7 Market Estimates & Forecast, By Motor Power, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Below 3.5 kW

- 7.3 3.5 kW – 6.5 kW

- 7.4 Above 6.5 kW

Chapter 8 Market Estimates & Forecast, By Voltage, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 48V

- 8.3 60 V

- 8.4 72V

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Ampere Vehicles

- 10.2 Ather Energy Pvt. Ltd.

- 10.3 Bajaj Auto Ltd.

- 10.4 Emflux Motors

- 10.5 Giant Bicycles

- 10.6 Gogoro Inc.

- 10.7 Hero Electric Vehicles Pvt. Ltd.

- 10.8 Jiangsu Xinri E-Vehicle Co. Ltd.

- 10.9 Niu Technologies

- 10.10 Ola Electric Mobility Pvt. Ltd.

- 10.11 PURE EV

- 10.12 Revolt Motors

- 10.13 Super Soco

- 10.14 Tork Motors

- 10.15 TVS Motor Company

- 10.16 Ultraviolette Automotive Pvt. Ltd.

- 10.17 VMOTO SOCO Italy SRL

- 10.18 Yadea Group Holdings Ltd.

- 10.19 Yamaha Motor Company

- 10.20 Zero Motorcycles Inc.

電動二輪車充電站市場按充電器類型、充電等級、功率容量、站類型、連接器類型、應用和最終用戶分類 - 2025-2030 年全球預測

電動二輪車充電站市場按充電器類型、充電等級、功率容量、站類型、連接器類型、應用和最終用戶分類 - 2025-2030 年全球預測 全球電動二輪車市場:成長、未來展望與競爭分析(2025-2033 年)

全球電動二輪車市場:成長、未來展望與競爭分析(2025-2033 年) 印度的電動二輪車市場評估:各車輛類型,各電池類型,各電池技術,各流通管道,各地區,機會及預測,2018~2032年

印度的電動二輪車市場評估:各車輛類型,各電池類型,各電池技術,各流通管道,各地區,機會及預測,2018~2032年 消費者之聲:印度電動二輪車購買者概況2025-2033 年電動二輪車市場報告(按車輛類型、電池類型(鋰離子、密封鉛酸)、電壓類型、峰值功率、電池技術、馬達佈置和地區分類)

消費者之聲:印度電動二輪車購買者概況2025-2033 年電動二輪車市場報告(按車輛類型、電池類型(鋰離子、密封鉛酸)、電壓類型、峰值功率、電池技術、馬達佈置和地區分類) 電動摩托車市場分析及預測(截至 2033 年),按類型、產品、技術、組件、應用、最終用戶、功能、安裝類型、設備和解決方案分類電動摩托車電池:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)電動二輪車市場:按產品類型、技術、電壓、覆蓋距離、銷售管道、應用分類 - 2025-2030 年全球預測

電動摩托車市場分析及預測(截至 2033 年),按類型、產品、技術、組件、應用、最終用戶、功能、安裝類型、設備和解決方案分類電動摩托車電池:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)電動二輪車市場:按產品類型、技術、電壓、覆蓋距離、銷售管道、應用分類 - 2025-2030 年全球預測 電動二輪車的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)二輪車零件的印度市場評估:各車輛類型,各推動器類型,各產品類型,各銷售管道,各地區,機會,預測(2018年度~2032年度)

電動二輪車的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)二輪車零件的印度市場評估:各車輛類型,各推動器類型,各產品類型,各銷售管道,各地區,機會,預測(2018年度~2032年度)