|

市場調查報告書

商品編碼

1684853

教育智慧顯示器市場機會、成長動力、產業趨勢分析與預測 2025-2034Education Smart Display Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

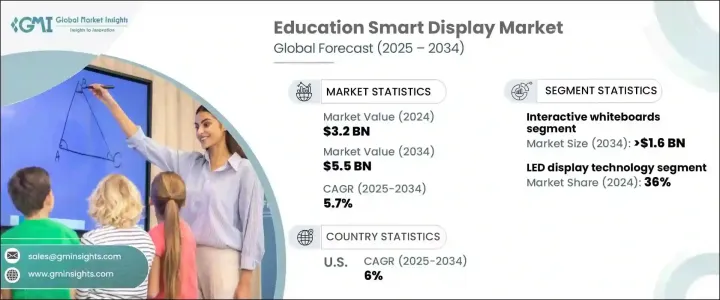

2024 年全球教育智慧顯示器市場價值為 32 億美元,預計 2025 年至 2034 年的複合年成長率為 5.7%。隨著世界各地的教育機構採用可增強參與度、協作性和整體學習成果的數位工具,對創新和互動學習解決方案的需求日益成長,推動了該市場的發展。先進科技與課堂的融合正在改變傳統的教學方法,為教育工作者提供更具活力和靈活性的教學環境。對個人化學習和提高學生參與度的日益關注繼續推動對智慧顯示解決方案的需求。隨著教育機構致力於讓學生為日益數位化的世界做好準備,智慧顯示器對於營造支持多種教學風格的互動學習氛圍至關重要。

教育智慧顯示市場依產品類型分為視訊牆、互動式白板、互動式平板、互動式投影機等。其中,互動式白板市場預計將引領市場,到 2034 年將達到 16 億美元。這些互動式白板透過提供動態、協作的環境,讓學生和教師可以即時與數位內容進行交互,從而徹底改變課堂。由於互動式和個人化學習解決方案的日益普及,這一領域的受歡迎程度正在迅速成長。它們提供的靈活性使機構能夠適應各種教學方法,同時提高學生的參與度和學習成果。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 32億美元 |

| 預測值 | 55億美元 |

| 複合年成長率 | 5.7% |

從顯示器技術來看,市場分為 LCD、LED 和 OLED 技術。 LED 顯示器預計將佔據主導地位,到 2024 年將佔據 36% 的市場佔有率。 LED 顯示器因其卓越的亮度、能源效率和長壽命而成為教育環境的首選。它們能夠製作高品質的視覺效果並與互動式工具無縫整合,這使得它們成為教室和演講廳中必不可少的器材。出於永續發展的考慮,教育機構青睞 LED 顯示螢幕,因為它具有成本效益和環境效益,這使得 LED 顯示器成為全球學校越來越受歡迎的選擇。

北美教育智慧顯示器市場預計將穩定成長,2024 年的複合年成長率為 6%。在美國,完善的數位基礎設施和對教育科技的大量投資推動了該市場的發展。美國教育部門正在教室和演講廳迅速採用智慧顯示器來增強學習體驗。政府措施和私營部門對數位教育的投資進一步支持了這些技術的採用,使該地區成為全球市場成長的主要驅動力之一。隨著教育機構專注於推動數位化學習工具,對創新有效的智慧顯示解決方案的需求將持續上升。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 產品類型、顯示尺寸、顯示技術、應用程式、最終用戶

- 數位化學習解決方案的採用率提高

- 政府措施和資金不斷增加

- 協作學習需求激增

- 全球轉向混合式和遠距學習轉變

- 專注於STEM教育與沉浸式學習

- 產業陷阱與挑戰

- 成本和預算限制

- 資料隱私和安全問題

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按產品類型,2021-2034 年

- 主要趨勢

- 視訊牆

- 互動式白板

- 互動式平板

- 互動式投影儀

- 其他

第 6 章:市場估計與預測:依顯示器尺寸,2021 年至 2034 年

- 主要趨勢

- 小號(50吋以下)

- 中號(50-70 英吋)

- 大號(70吋以上)

第 7 章:市場估計與預測:按顯示技術,2021 年至 2034 年

- 主要趨勢

- 液晶顯示器

- 引領

- OLED

第 8 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 課堂教學

- 互動式演示

- 遠距教學

- 協作學習

- 其他

第 9 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- K-12 學校

- 高等教育機構

- 輔導中心

- 企業培訓中心

- 其他

第 10 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地區

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- MEA 其他地區

第 11 章:公司簡介

- Apple Inc

- Aser

- Asus

- Barco

- BenQ

- Christie Digital Systems USA, Inc.

- Epson

- Fujitsu

- Globus Infocom Limited

- HP Inc.

- Lenovo

- LG Electronics

- Newline Interactive Inc.

- Optoma Corporation

- Panasonic Holdings Corporation

- PPDS (PHILIPS)

- Promethean World Ltd.

- SAMSUNG

- Sharp NEC Display Solutions

- SMART Technologies ULC

- Sony Group Corporation

- Toshiba Corporation

- ViewSonic Corporation

The Global Education Smart Display Market was valued at USD 3.2 billion in 2024 and is expected to experience a CAGR of 5.7% from 2025 to 2034. This market is being driven by the increasing need for innovative and interactive learning solutions as educational institutions worldwide embrace digital tools that enhance engagement, collaboration, and overall learning outcomes. The integration of advanced technology in classrooms is transforming traditional teaching methods, providing educators with more dynamic and flexible teaching environments. The growing focus on personalized learning and improving student engagement continues to push the demand for smart display solutions. As educational institutions aim to prepare students for an increasingly digital world, smart displays have become crucial in fostering an interactive learning atmosphere that supports a variety of teaching styles.

The education smart display market is divided by product type into video walls, interactive whiteboards, interactive flat panels, interactive projectors, and others. Among these, the interactive whiteboards segment is expected to lead the market, reaching USD 1.6 billion by 2034. These interactive whiteboards are revolutionizing classrooms by offering dynamic, collaborative environments where students and teachers can interact with digital content in real time. This segment's popularity is growing rapidly due to the increasing adoption of interactive and personalized learning solutions. The flexibility they provide allows institutions to adapt to various teaching methods while improving student engagement and learning outcomes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $5.5 Billion |

| CAGR | 5.7% |

When looking at display technology, the market is divided into LCD, LED, and OLED technologies. LED displays are expected to dominate, accounting for a 36% market share in 2024. Recognized for their superior brightness, energy efficiency, and long lifespan, LED displays are the preferred choice for educational environments. Their ability to produce high-quality visuals and integrate seamlessly with interactive tools has made them essential in classrooms and lecture halls. With sustainability in mind, educational institutions favor LED displays for their cost-effectiveness and environmental benefits, making them an increasingly popular choice in schools worldwide.

The North American education smart display market is expected to grow at a steady pace, with a CAGR of 6% during 2024. In the United States, the market is fueled by a well-established digital infrastructure and significant investments in educational technology. The U.S. education sector is rapidly adopting smart displays in classrooms and lecture halls to enhance learning experiences. Government initiatives and private sector investments in digital education further support the adoption of these technologies, making the region one of the key drivers of growth in the global market. As educational institutions focus on advancing digital learning tools, the demand for innovative and effective smart display solutions will continue to rise.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.7 Growth drivers

- 3.7.1 Product Type, display size, display technology, application, end user

- 3.7.2 Increased adoption of digital learning solutions

- 3.7.3 Rising government initiatives and funding

- 3.7.4 Surge in demand for collaborative learning

- 3.7.5 Global shift towards hybrid and remote learning

- 3.7.6 Focus on STEM education and immersive learning

- 3.8 Industry pitfalls & challenges

- 3.8.1 Cost and budget constraints

- 3.8.2 Data privacy and security concerns

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD billion)

- 5.1 Key trends

- 5.2 Video wall

- 5.3 Interactive whiteboards

- 5.4 Interactive flat panels

- 5.5 Interactive projectors

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Display Size, 2021-2034 (USD billion)

- 6.1 Key trends

- 6.2 Small (Below 50 inches)

- 6.3 Medium (50-70 inches)

- 6.4 Large (Above 70 inches)

Chapter 7 Market Estimates & Forecast, By Display Technology, 2021-2034 (USD billion)

- 7.1 Key trends

- 7.2 LCD

- 7.3 LED

- 7.4 OLED

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD billion)

- 8.1 Key trends

- 8.2 Classroom teaching

- 8.3 Interactive presentations

- 8.4 Distance learning

- 8.5 Collaborative learning

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2034 (USD billion)

- 9.1 Key trends

- 9.2 K-12 Schools

- 9.3 Higher education institutions

- 9.4 Coaching centers

- 9.5 Corporate training centers

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD billion)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Rest of Latin America

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Rest of MEA

Chapter 11 Company Profiles

- 11.1 Apple Inc

- 11.2 Aser

- 11.3 Asus

- 11.4 Barco

- 11.5 BenQ

- 11.6 Christie Digital Systems USA, Inc.

- 11.7 Epson

- 11.8 Fujitsu

- 11.9 Globus Infocom Limited

- 11.10 HP Inc.

- 11.11 Lenovo

- 11.12 LG Electronics

- 11.13 Newline Interactive Inc.

- 11.14 Optoma Corporation

- 11.15 Panasonic Holdings Corporation

- 11.16 PPDS (PHILIPS)

- 11.17 Promethean World Ltd.

- 11.18 SAMSUNG

- 11.19 Sharp NEC Display Solutions

- 11.20 SMART Technologies ULC

- 11.21 Sony Group Corporation

- 11.22 Toshiba Corporation

- 11.23 ViewSonic Corporation

2025 年全球智慧顯示器市場報告2025 年全球汽車智慧顯示器市場報告汽車智慧顯示市場 - 全球產業規模、佔有率、趨勢、機會和預測,按顯示技術、車輛類型、顯示尺寸、地區和競爭細分,2020-2030F

2025 年全球智慧顯示器市場報告2025 年全球汽車智慧顯示器市場報告汽車智慧顯示市場 - 全球產業規模、佔有率、趨勢、機會和預測,按顯示技術、車輛類型、顯示尺寸、地區和競爭細分,2020-2030F 智慧顯示器 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

智慧顯示器 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 教育智慧顯示市場:按產品、顯示技術、顯示尺寸、應用分類 - 2025-2030 年全球預測

教育智慧顯示市場:按產品、顯示技術、顯示尺寸、應用分類 - 2025-2030 年全球預測 汽車智慧顯示市場規模、佔有率、成長分析、按車型、按車輛類別、按電動車、按自動駕駛、按顯示技術、按顯示尺寸、按應用、按地區 - 行業預測,2024-2031 年智慧顯示器市場:按類型、解析度、顯示器尺寸和最終用戶分類 - 2025-2030 年全球預測汽車智慧顯示市場:按顯示技術、自動駕駛、顯示尺寸、車輛類別、應用、車輛類型分類 - 2025-2030 年全球預測智慧顯示市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、技術(LCD、OLED、QLED)、最終用戶、地區和競爭細分,2019-2029F2024-2032 年智慧顯示器市場報告(按類型、顯示器尺寸、解析度、最終用戶和地區分類)

汽車智慧顯示市場規模、佔有率、成長分析、按車型、按車輛類別、按電動車、按自動駕駛、按顯示技術、按顯示尺寸、按應用、按地區 - 行業預測,2024-2031 年智慧顯示器市場:按類型、解析度、顯示器尺寸和最終用戶分類 - 2025-2030 年全球預測汽車智慧顯示市場:按顯示技術、自動駕駛、顯示尺寸、車輛類別、應用、車輛類型分類 - 2025-2030 年全球預測智慧顯示市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、技術(LCD、OLED、QLED)、最終用戶、地區和競爭細分,2019-2029F2024-2032 年智慧顯示器市場報告(按類型、顯示器尺寸、解析度、最終用戶和地區分類)