|

市場調查報告書

商品編碼

1685053

精準農業市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Precision Farming Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

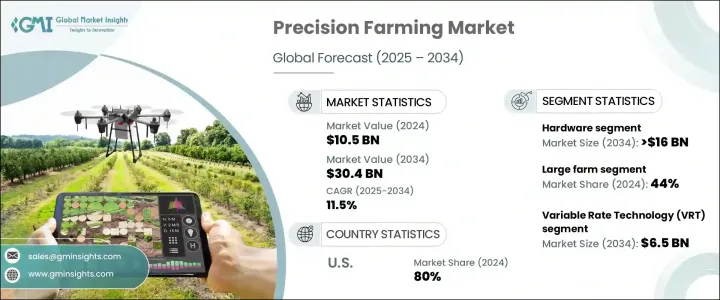

2024 年全球精準農業市場價值為 105 億美元,預估 2025 年至 2034 年期間複合年成長率為 11.5%。人口快速成長和糧食需求不斷增加是推動這一擴張的主要驅動力。隨著全球人口每年增加約 8,300 萬,對永續農業實踐的需求變得更加迫切。精準農業利用先進技術來最佳化作物產量,已成為解決這項挑戰的關鍵解決方案。

世界各國政府在推動精準農業的應用方面發揮著至關重要的作用。透過提供補貼、補助和政策激勵,他們旨在提高農業生產力,同時最大限度地減少對環境的影響。精準農業融合了物聯網、人工智慧、無人機和資料分析等技術,以提高效率並減少資源消耗。這些創新幫助農民提高生產力,降低營運成本,實施生態友善實踐,確保長期永續的糧食生產。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 105億美元 |

| 預測值 | 304億美元 |

| 複合年成長率 | 11.5% |

市場根據組件進行細分,硬體在 2024 年處於領先地位,佔有超過 55% 的市場佔有率。到 2034 年,該部分的規模預計將超過 160 億美元。農業經營中 GPS、感測器和自動化設備的日益廣泛應用推動了這一成長。土壤感測器、氣象站和 GPS 接收器等硬體工具使農民能夠監測條件、最佳化灌溉並自動執行種植和收穫等關鍵任務。自動化進一步提高了效率,機器人系統可以執行傳統上手動處理的任務。

以農場規模計算,大型農場在 2024 年佔據了約 44% 的市場。他們投資先進技術以提高生產力和效率的能力促成了這種主導地位。 GPS 導航曳引機、無人機和智慧灌溉系統可以實現精確的作物監測和資源管理。隨著大型農場尋求最佳化營運,對精準農業解決方案的需求持續上升。

從技術角度來看,變數速率技術 (VRT) 是一個主導領域,預計到 2034 年將創造 65 億美元的產值。該技術允許農民根據具體的田間條件客製化肥料、種子和農藥的使用。透過利用感測器、GPS 和先進軟體的資料,VRT 可確保最佳輸入分配,減少浪費並最大限度地提高產量。對成本效益和永續農業的日益重視正在加速其應用,農業機構的支持不斷增加使得這些系統更容易獲得。

在應用方面,產量監測將在 2024 年以 25% 的佔有率引領市場。該系統幫助農民即時追蹤作物生長情況,從而根據數據做出決策,提高生產力。感測器技術和資料分析的進步提供了對產量模式和土壤條件的精確洞察,從而改善了長期農場管理。隨著糧食需求的增加,精準農業解決方案對於最佳化農業產量變得至關重要。

北美引領全球市場,美國在 2024 年佔據 80% 的佔有率。先進農業技術的廣泛採用、政府補貼和強大的基礎設施支持精準農業的擴張。對無人機、感測器和資料分析的日益依賴不斷改變農業經營方式,使農業更有效率、更有利可圖。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 硬體提供者

- 軟體供應商

- 服務提供者

- 技術提供者

- 最終客戶

- 供應商概況

- 利潤率分析

- 技術與創新格局

- 專利分析

- 重要新聞及舉措

- 監管格局

- 精準農業的演變

- 使用案例

- 衝擊力

- 成長動力

- 對永續農業實踐的需求日益成長

- 全球人口不斷成長,對糧食產量的需求也隨之增加

- 增加對農業技術的投資

- 政府支持數位農業技術的措施和補貼

- 產業陷阱與挑戰

- 缺乏操作先進精準農業設備的熟練勞動力

- 農村地區高速網路存取有限

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 硬體

- 感應器

- 自動轉向系統

- 無人機、無人駕駛飛機和攝影機

- 行動裝置

- GPS 和 GNSS

- 其他

- 軟體

- 農場管理軟體(FMS)

- 數據分析與巨量資料解決方案

- 地理資訊系統 (GIS) 軟體

- 基於雲端的軟體解決方案

- 人工智慧和機器學習軟體

- 服務

- 專業服務

- 託管服務

第6章:市場估計與預測:依技術,2021 - 2034 年

- 主要趨勢

- 高精度定位系統

- 地理測繪

- 遙感

- 綜合電子通訊

- 可變速率技術 (VRT)

第 7 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 天氣監測

- 產量監測

- 字段映射

- 灌溉管理

- 廢棄物管理

- 財務管理

- 其他

第 8 章:市場估計與預測:按農場規模,2021 - 2034 年

- 主要趨勢

- 小農場

- 中型農場

- 大型農場

第 9 章:市場估計與預測:按地區,2021 - 2034 年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- AG Leader

- AGCO

- Agribotix

- AgSense

- AgSmarts

- Boumatic

- CNH

- CropMetrics

- CropX

- Delaval

- Dickey-John

- Farmers Edge

- GEA Group

- John Deere

- Monsanto

- Precision Planting

- Raven

- Topcon

- Trimble

- Yara

The Global Precision Farming Market was valued at USD 10.5 billion in 2024 and is projected to grow at an 11.5% CAGR from 2025 to 2034. Rapid population growth and the increasing demand for food are key drivers behind this expansion. With the global population rising by approximately 83 million annually, the need for sustainable agricultural practices has become more urgent. Precision farming, which leverages advanced technologies to optimize crop yields, has emerged as a critical solution to this challenge.

Governments worldwide are playing a crucial role in promoting the adoption of precision agriculture. By offering subsidies, grants, and policy incentives, they aim to boost agricultural productivity while minimizing environmental impact. Precision farming integrates technologies such as IoT, AI, drones, and data analytics to improve efficiency and reduce resource consumption. These innovations help farmers enhance productivity, cut operational costs, and implement eco-friendly practices, ensuring sustainable food production in the long run.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.5 billion |

| Forecast Value | $30.4 billion |

| CAGR | 11.5% |

The market is segmented based on components, with hardware leading in 2024, holding over 55% market share. By 2034, the segment is anticipated to surpass USD 16 billion. The increasing adoption of GPS, sensors, and automated equipment in farming operations is driving this growth. Hardware tools such as soil sensors, weather stations, and GPS receivers enable farmers to monitor conditions, optimize irrigation, and automate critical tasks like planting and harvesting. Automation further enhances efficiency, with robotic systems performing tasks traditionally handled manually.

By farm size, large farms accounted for approximately 44% of the market share in 2024. Their ability to invest in advanced technology for improved productivity and efficiency contributes to this dominance. GPS-guided tractors, drones, and smart irrigation systems allow for precise crop monitoring and resource management. As large-scale farms seek to optimize operations, demand for precision farming solutions continues to rise.

Technology-wise, variable rate technology (VRT) is a dominant segment, expected to generate USD 6.5 billion by 2034. This technology allows farmers to tailor the application of fertilizers, seeds, and pesticides based on specific field conditions. By leveraging data from sensors, GPS, and advanced software, VRT ensures optimal input distribution, reducing waste while maximizing yield. The growing emphasis on cost efficiency and sustainable farming is accelerating adoption, with increased support from agricultural institutions making these systems more accessible.

In terms of applications, yield monitoring led the market in 2024 with a 25% share. This system helps farmers track crop performance in real time, enabling data-driven decisions to enhance productivity. Advancements in sensor technology and data analytics provide precise insights into yield patterns and soil conditions, improving long-term farm management. With increasing food demand, precision farming solutions are becoming essential for optimizing agricultural output.

North America leads the global market, with the US holding an 80% share in 2024. The widespread adoption of advanced agricultural technologies, government subsidies, and strong infrastructure support precision farming expansion. Increased reliance on drones, sensors, and data analytics continues to transform farming operations, making agriculture more efficient and profitable.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Hardware providers

- 3.1.2 Software providers

- 3.1.3 Service providers

- 3.1.4 Technology providers

- 3.1.5 End customers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Evolution of precision farming

- 3.9 Use cases

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 The growing need for sustainable farming practices

- 3.10.1.2 The rising global population and the corresponding demand for higher food production

- 3.10.1.3 Increased investment in agricultural technologies

- 3.10.1.4 Government initiatives and subsidies supporting digital farming technologies

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 The lack of skilled labor to operate advanced precision farming equipment

- 3.10.2.2 Limited access to high-speed internet in rural areas

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensor

- 5.2.2 Automated steering system

- 5.2.3 Drone, UAV, and camera

- 5.2.4 Mobile device

- 5.2.5 GPS and GNSS

- 5.2.6 Others

- 5.3 Software

- 5.3.1 Farm Management Software (FMS)

- 5.3.2 Data analytics and big data solution

- 5.3.3 Geographic information system (GIS) software

- 5.3.4 Cloud-based software solution

- 5.3.5 Artificial intelligence and machine learning software

- 5.4 Services

- 5.4.1 Professional services

- 5.4.2 Managed services

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 High precision positioning system

- 6.3 Geo mapping

- 6.4 Remote sensing

- 6.5 Integrated electronic communication

- 6.6 Variable Rate Technology (VRT)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Weather monitoring

- 7.3 Yield monitoring

- 7.4 Field mapping

- 7.5 Irrigation management

- 7.6 Waste management

- 7.7 Financial management

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Farm Size, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Small farm

- 8.3 Medium farm

- 8.4 Large farm

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 North America

- 9.1.1 U.S.

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Russia

- 9.2.7 Nordics

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 South Korea

- 9.3.6 Southeast Asia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 UAE

- 9.5.2 South Africa

- 9.5.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 AG Leader

- 10.2 AGCO

- 10.3 Agribotix

- 10.4 AgSense

- 10.5 AgSmarts

- 10.6 Boumatic

- 10.7 CNH

- 10.8 CropMetrics

- 10.9 CropX

- 10.10 Delaval

- 10.11 Dickey-John

- 10.12 Farmers Edge

- 10.13 GEA Group

- 10.14 John Deere

- 10.15 Monsanto

- 10.16 Precision Planting

- 10.17 Raven

- 10.18 Topcon

- 10.19 Trimble

- 10.20 Yara

2025年全球精密農業人工智慧市場報告

2025年全球精密農業人工智慧市場報告 精準葡萄栽培市場規模、佔有率和成長分析(按組件、技術、應用和地區)- 2025-2032 年行業預測

精準葡萄栽培市場規模、佔有率和成長分析(按組件、技術、應用和地區)- 2025-2032 年行業預測 2025 年精密農業全球市場報告

2025 年精密農業全球市場報告 精準採收市場規模、佔有率、趨勢分析報告:按應用、產品、供應、地區、細分市場預測,2025-2030 年

精準採收市場規模、佔有率、趨勢分析報告:按應用、產品、供應、地區、細分市場預測,2025-2030 年 精密農業-市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

精密農業-市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 精密農業的全球市場:市場規模·佔有率·趨勢,產業分析 (提供內容·各技術·各用途·各地區),未來預測 (2025年~2034年)

精密農業的全球市場:市場規模·佔有率·趨勢,產業分析 (提供內容·各技術·各用途·各地區),未來預測 (2025年~2034年) 精密農業市場規模、佔有率、成長分析,按產品、按技術、按應用、按地區 - 按行業預測,2024-2031 年

精密農業市場規模、佔有率、成長分析,按產品、按技術、按應用、按地區 - 按行業預測,2024-2031 年 到 2030 年地膜材料市場預測:按產品、銷售管道、功能、應用和地區進行全球分析

到 2030 年地膜材料市場預測:按產品、銷售管道、功能、應用和地區進行全球分析 精密農業軟體市場:依軟體、交付模式、應用、最終用途分類 - 2025-2030 年全球預測

精密農業軟體市場:依軟體、交付模式、應用、最終用途分類 - 2025-2030 年全球預測 精密農業市場:按組件、技術和應用分類 - 2025-2030 年全球預測

精密農業市場:按組件、技術和應用分類 - 2025-2030 年全球預測