|

市場調查報告書

商品編碼

1637870

精密農業-市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)Precision Farming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

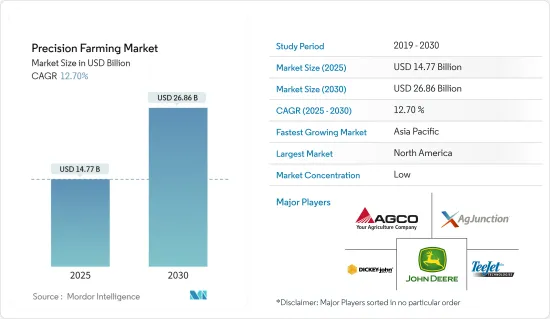

精密農業市場規模預計到2025年為147.7億美元,預計2030年將達到268.6億美元,預測期內(2025-2030年)複合年成長率為12.7%。

採用精密農業的主要促進因素包括氣候變遷、糧食需求增加、全球農業部門技術採用的增加以及政府利用新技術來提高農民效率的努力。

主要亮點

- 精密農業是一種農業管理概念,重點是觀察、測量和應對田間作物變化。植物生產集中在由財產線、特定田地的預期作物產量、地理和環境因素所界定的區域。

- 預計到 2030年終,精密農業將成為重要趨勢,超越農業領域的其他進步。透過行動應用程式,您可以透過遙感探測和地面通訊獲取設備的即時資訊。 (VRT) 使農民能夠根據天氣變化做出更具體的土地管理決策,並更有效地使用種子、化肥和農藥等投入品。

- 大多數廣泛的市場供應商提供導引系統、氣候/天氣預報和輸入分配設備。這家小型供應商主要針對智慧灌溉和田間監測技術,並專注於物聯網解決方案。北美是技術的早期採用者,對精密農業中使用的許多創新技術的採用率很高。該地區在農業中大量採用了物聯網、巨量資料、無人機和機器人技術。

- 此外,在研究期間,增加對駕駛人曳引機、導引系統和GPS感測系統等技術的投資也有望有助於擴大精密農業市場規模。

- 高昂的成本使得小農很難採用該工具,並且僅限於大型農場。然而,可變施肥量 (VRA) 和控制交通系統 (CTF) 有助於提高作物養分利用率、改善作物品質並減少重複生產,從而提高生產經濟效益。

- 然而,在 COVID-19 之後,遙感探測和農場管理軟體技術的採用預計將導致更廣泛的採用。公司已經轉向無線平台來支援即時決策,包括作物健康監測、產量監測、灌溉調度、田間測繪和收穫管理。這可能會在預測期內推動所研究的市場需求。

精密農業市場趨勢

土壤監測可望佔有較大佔有率

- 可靠的通訊使土壤感測器能夠測量土壤的基本特性並將其傳輸到顯示單元。土壤感測器通常用於速度應用,並與 GPS 結合使用,根據土壤特性繪製田野地圖。土壤感測器對於監測收穫期間作物的生長至關重要。

- 分析資料後,感測器即時提供資訊並相應地改變施用量。使用地圖方法的傳統模型被認為更有效。下一步,進行問題分析並應用可變利率。就工業研究而言,用於土壤監測目的整合的不同類型的感測器包括電磁、光學、機械、聲學和電化學。

- 此外,隨著世界各地先進農民擴大使用各種土壤監測感測器,地面監測系統預計將成為整個預測期內的主要需求。地面監測具有很高的市場佔有率,因為它不需要大量的專業知識。智慧感測器技術的改進以及與物聯網模組的整合正在推動綜合農業的需求

- 此外,農業技術進步可能會進一步推動所研究市場的成長。據 ETNO 稱,未來幾年歐盟 (EU) 農業中的物聯網活躍連接數量預計將增加。預計2022年連線數將達到4692萬,2025年連線數將達到7026萬。物聯網設備在農業中的應用包括使用無人機進行監控和種子分發。

亞太地區市場將實現顯著成長

- 預計該地區在預測期內將出現顯著成長,特別是開發中國家的政府舉措鼓勵使用旨在最大限度提高生產力的現代精密農業技術。

- IBEF 表示,在Pradhan Mantri Kisan Sampada Yojana 等政府舉措和1 兆美元基礎設施發展計畫的支持下,印度加工食品市場將從上個月的193,128.87 億盧比成長到2025 年,預計將擴大到345,135.25 億盧比。

- 在許多亞洲國家,服務供應商正在迅速採取行動改善應用方法,使亞洲農業成為研究市場供應商的重點。智慧曳引機、無人機、整地服務、農作物噴粉、衛星圖像、灌溉服務、手持式決策診斷等正在幫助該地區改善對小規模農民的決策支持,而無需投資昂貴的基礎設施。

- 亞太地區的主要促進因素包括產量和盈利的提高,這推動農民採用精密農業中的作物監測技術。

- 澳洲在該地區佔有很大佔有率。市場尚未跟上作物日益成長的需求以及可變利率施用 (VRA) 市場的預期成長。該地區的機會包括無人機和無人機在精密農業實踐中的應用以及日益嚴重的環境問題。

精密農業產業概況

精密農業市場高度分散,涉及眾多參與企業。市場主要企業包括AgJunction Inc.、Raven Industries Inc.、DICKEY-john Corporation.、TeeJet Technologies.等。這些公司從事市場擴張活動,並採用有機和無機成長策略,以最大限度地提高不同地區的收益。

- 2023 年 10 月,迪爾公司將與瑞典的 Delaval 合作建立牛奶永續發展中心,並與挪威的 Yara 合作開發數位化精密農業工具以實現永續性。

- 2023年4月,全球農業設備供應商愛科公司與工業技術解決方案供應商海克斯康宣布結成策略聯盟。此次合作的重點是擴大愛科的工廠組裝和售後指導產品。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 買方議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 評估 COVID-19 對產業的影響

第5章市場動態

- 市場促進因素

- 使用人工智慧和物聯網技術的土壤監測正在推動市場

- 新技術的出現

- 政府措施和新興企業的崛起

- 市場問題

- 由於地區意識的差異,實施模式因地區而異。

- 市場機會

- 技術進步正在降低許多先進設備的成本。

- 支援LiDAR的無人機等技術進步、資料分析和該領域雲的出現

第6章 市場細分

- 依技術

- 引導系統

- 全球定位系統 (GPS)/全球衛星導航系統 (GNSS)

- 全球資訊系統(GIS)

- 遙感探測

- 可變利率技術

- 變數肥料

- 變速播種

- 變速農藥

- 無人機和無人機

- 其他

- 引導系統

- 按成分

- 硬體

- 軟體

- 按服務

- 按用途

- 產量監控

- 可變利率應用

- 現場測繪

- 土壤監測

- 作物偵察

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 歐洲其他地區

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 其他亞太地區

- 拉丁美洲

- 中東/非洲

- 北美洲

第7章 競爭格局

- 公司簡介

- AGCO Corporation

- Ag Junction Inc

- John Deere

- DICKEY-john Corporation

- TeeJet Technologies

- Raven Industries Inc.

- Lindsay Corporation

- Topcon Precision Agriculture

- Land O'lakes Inc.

- BASF SE

- Yara International ASA

第8章投資分析

第9章 市場的未來

The Precision Farming Market size is estimated at USD 14.77 billion in 2025, and is expected to reach USD 26.86 billion by 2030, at a CAGR of 12.7% during the forecast period (2025-2030).

Some of the main drivers for adopting precision farming are climate change, growing demand for food, more technology adoption in global agriculture sector and government initiatives to improve farmers' efficiency by means of new technologies.

Key Highlights

- Precision farming is an agricultural management concept which focuses on the observation, measurement and response to crop variability between fields. Production of plants is focused on the areas defined by property lines, expected crop yields in a given field and geographical and environmental factors.

- Moroever, Precision farming, which will overtake other advances in agriculture by the end of 2030, is predicted to be an important trend. Through the mobile app, real time information on equipment is available through remote sensing and ground communication. (VRTs) has allows farmers to make more specific land management decisions, so that inputs like seeds, fertilisers and pesticides can be used more effectively in the context of changing weather conditions.

- Most broad-market vendors offer guidance systems, climate-weather predictions, and input applications equipment. Small vendors mainly target smart irrigation and field monitoring techniques specializing in IoT solutions. North America is the early adopter of technology and has a significant adoption rate of many innovative technologies used in precision farming. The region is a substantial adopter of IoT, big data, drones, and robotics in agriculture.

- Moreover, growing investments in technologies such as driverless tractors, guidance systems, and GPS sensing systems are also anticipated to contribute to the precision agriculture market scope growth during the study period.

- High costs have made it tough for small-scale farmers to deploy the tools, thereby, restricting them to only large farms. However, variable rate application (VRA) and controlled traffic systems (CTF) help in enhanced utilization of crop nutrients, improvement of crop quality, and the reduction of overlap, thus resulting in better production economy.

- However, more significant adoption could result from deploying remote sensing and farm management software technologies after COVID-19. Businesses have already started concentrating more on wireless platforms to support real-time decision-making for crop health monitoring, yield monitoring, irrigation scheduling, field mapping, and harvesting management. This may propel the studied market demand in the forecasted period.

Precision Farming Market Trends

Soil Monitoring is Expected to Hold Significant Share

- By means of reliable communication, soil sensors are capable of measuring the essential properties of soils and transmitting them to a display unit. In order to create field maps based on the soil's characteristics, soils sensors are usually used in combination with velocity applications or GPS. Soil sensors are essential for monitoring the viability of crop growth at harvest time.

- After analysing the data, sensors provide real time information which changes the application rate accordingly. It is considered that traditional models of using the map approach are more efficient. In the following steps, they enable a problem analysis to be carried out and variable rate applications to be adapted.The various type of sensors being integrated for soil monitoring purposes includes electromagnetic, optical, mechanical, acoustic, and electrochemical, as far as industrial research has reached.

- Moreover, in view of the increasing use of different soil monitoring sensors by forward thinking farmers from around the world, ground surveillance systems are expected to be a major demand throughout the forecast period. The market share of ground monitoring is high because it does not require a lot of expertise. Improvements in intelligent sensor technologies and their integration with the Internet of Things modules have led to a growing demand for integrated agriculture.

- Furthermore, technological advancement in farming may further propel the studied market growth. According to ETNO, the number of IoT active connections in agriculture was expected to increase in the European Union through the years. It was recorded at 46.92 million connections in 2022 and is expected to reach 70.26 million by 2025. Some uses for IoT devices in agriculture would be drone usage for surveillance or distributing seeds.

Asia-Pacific to Experience Significant Market Growth

- In particular due to government initiatives in developing countries encouraging the use of modern precision farming technologies, which is aimed at maximising productivity, this region is expected to experience significant growth over the projected period.

- According to IBEF, from INR 1,931,288.7 crore USD 263 billion last month on the back of government initiatives like Pradhan Mantri Kisan Sampada Yojana and plans for a 1 trillion dollar infrastructure, India's processing food market is projected to increase to INR 3,451,352.5 cr USD 470 billion by 2025.

- In many Asian countries, service providers are rapidly moving to improve their application methods and make Asia agriculture the main focus of study market vendors. Smart tractors, UAVs, ground leveling services, pesticide application, satellite imaging, irrigation services, and handheld decision diagnostics along with In this region, without investment in costly infrastructure, decision support is becoming more easily available for small farmers.

- The market growth is being driven by some of the main factors in Asia-Pacific are augmented yield and profitability, which are pushing farmers toward crop monitoring technology in precision farming.

- Australia holds the major share of market in this region. The market is yet to catch up with its growing demand for food crops and the anticipated growth in the variable rate applications (VRA) market. Some of the opportunities in the region are application of drones and unmanned aerial vehicles (UAVs) in precision farming practices and the growing environmental issues.

Precision Farming Industry Overview

The precision farming market is highly fragmented, with numerous participants involved. Key players in the market include AgJunction Inc., Raven Industries Inc., DICKEY-john Corporation., TeeJet Technologies., and others. These companies are engaged in market expansion activities and adopting organic and inorganic growth strategies to maximize their revenue across different regions.

- In October 2023, Deere & Co teams with 2 Sweden-based Delaval on the Milk Sustainability Center and Norway-based Yara on digital precision agriculture tools for sustainability, where the partnerships aim to help farmers track livestock and fertilizer data so they can make smarter business decisions that are better for the environment.

- In April 2023 AGCO Corporation, a one of global agriculture equipment provider, and Hexagon, an industrial technology solution provider declared their strategic collaboration. The collaboration is focused on the expansion of AGCO's factory-fit and aftermarket guidance offerings.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness- Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment Of COVID-19 Impact On The Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Soil Monitoring using AI and IOT technologies to drive the market

- 5.1.2 Emergence of New Technologies

- 5.1.3 Government Initiative and Increasing Number of Startups

- 5.2 Market Challenges

- 5.2.1 Difference in Awareness in Different Regions is also Resulting in Varying Adoption Patterns in These Regions

- 5.3 Market Opportunities

- 5.3.1 Technological Advancement is Reducing the Cost of Many Advance Equipment

- 5.3.2 Advancement in Technologies, like LIDAR-enabled Drones, and Emergence of Data Analytics and Cloud in the Sector

6 MARKET SEGMENTATION

- 6.1 By Technology

- 6.1.1 Guidance System

- 6.1.1.1 Global Positioning System (GPS)/ Global Satellite Navigation System (GNSS)

- 6.1.1.2 Global Information System (GIS)

- 6.1.2 Remote Sensing

- 6.1.3 Variable-rate Technology

- 6.1.3.1 Variable Rate Fertilizer

- 6.1.3.2 Variable Rate Seeding

- 6.1.3.3 Variable Rate Pesticide

- 6.1.4 Drones and UAVs

- 6.1.5 Other Technologies

- 6.1.1 Guidance System

- 6.2 By Component

- 6.2.1 Hardware

- 6.2.2 Software

- 6.2.3 Services

- 6.3 By Application

- 6.3.1 Yield Monitoring

- 6.3.2 Variable Rate Application

- 6.3.3 Field Mapping

- 6.3.4 Soil Monitoring

- 6.3.5 Crop Scouting

- 6.3.6 Other Applications

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Australia

- 6.4.3.5 Rest of the Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East & Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 AGCO Corporation

- 7.1.2 Ag Junction Inc

- 7.1.3 John Deere

- 7.1.4 DICKEY-john Corporation

- 7.1.5 TeeJet Technologies

- 7.1.6 Raven Industries Inc.

- 7.1.7 Lindsay Corporation

- 7.1.8 Topcon Precision Agriculture

- 7.1.9 Land O'lakes Inc.

- 7.1.10 BASF SE

- 7.1.11 Yara International ASA

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025年全球精密農業人工智慧市場報告

2025年全球精密農業人工智慧市場報告 精準葡萄栽培市場規模、佔有率和成長分析(按組件、技術、應用和地區)- 2025-2032 年行業預測

精準葡萄栽培市場規模、佔有率和成長分析(按組件、技術、應用和地區)- 2025-2032 年行業預測 2025 年精密農業全球市場報告

2025 年精密農業全球市場報告 精準農業市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

精準農業市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 精準採收市場規模、佔有率、趨勢分析報告:按應用、產品、供應、地區、細分市場預測,2025-2030 年

精準採收市場規模、佔有率、趨勢分析報告:按應用、產品、供應、地區、細分市場預測,2025-2030 年 精密農業的全球市場:市場規模·佔有率·趨勢,產業分析 (提供內容·各技術·各用途·各地區),未來預測 (2025年~2034年)

精密農業的全球市場:市場規模·佔有率·趨勢,產業分析 (提供內容·各技術·各用途·各地區),未來預測 (2025年~2034年) 精密農業市場規模、佔有率、成長分析,按產品、按技術、按應用、按地區 - 按行業預測,2024-2031 年

精密農業市場規模、佔有率、成長分析,按產品、按技術、按應用、按地區 - 按行業預測,2024-2031 年 到 2030 年地膜材料市場預測:按產品、銷售管道、功能、應用和地區進行全球分析

到 2030 年地膜材料市場預測:按產品、銷售管道、功能、應用和地區進行全球分析 精密農業軟體市場:依軟體、交付模式、應用、最終用途分類 - 2025-2030 年全球預測

精密農業軟體市場:依軟體、交付模式、應用、最終用途分類 - 2025-2030 年全球預測 精密農業市場:按組件、技術和應用分類 - 2025-2030 年全球預測

精密農業市場:按組件、技術和應用分類 - 2025-2030 年全球預測