|

市場調查報告書

商品編碼

1698606

太陽能追蹤器市場機會、成長動力、產業趨勢分析及 2025-2034 年預測Solar Tracker Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

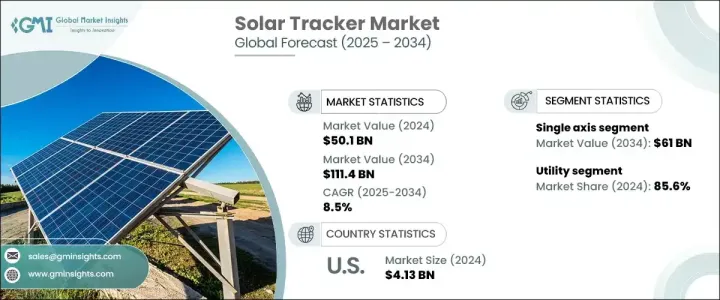

2024 年全球太陽能追蹤器市場價值為 501 億美元,預計 2025 年至 2034 年的複合年成長率為 8.5%。太陽能發電系統效率的提高,加上太陽能追蹤器成本的下降,正在推動產業成長。這些系統提高了太陽能電池板的性能,與固定傾斜裝置相比,單軸追蹤器可將能量輸出提高 10-25%,雙軸追蹤器可將能量輸出提高高達 40%。智慧電網技術與物聯網的整合可以改善能源生產的監控、控制和最佳化,從而加速市場擴張。與傳統單面系統相比,配備單軸追蹤器的雙面太陽能組件的採用預計將使平準化電力成本降低約 16%,從而進一步刺激產品需求。太陽能追蹤器技術的不斷進步正在透過降低成本、提高效率和增加太陽能在多種應用中的可及性來重塑產業。

市場還受益於能源儲存解決方案的整合、混合太陽能追蹤系統的出現以及環保材料的使用以最大限度地減少對環境的影響。支持性監管政策、激勵計畫以及美國《通膨削減法案》和澳洲的Solar Sunshot計畫等政府措施預計將增強商業前景。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 501億美元 |

| 預測值 | 1114億美元 |

| 複合年成長率 | 8.5% |

根據產品,市場分為單軸追蹤器和雙軸追蹤器。預計到 2034 年,單軸追蹤器的收入將超過 610 億美元,與固定傾斜系統相比,效率將提高 25-35%。材料和設計的進步提高了可靠性,降低了維護成本並延長了使用壽命,從而提高了產品的採用率。此外,更高的能源產量和效率的提高可以帶來更好的投資回報,從而改善產業格局。

市場分為住宅、商業和工業以及公用事業應用。 2024年,公用事業部門佔據85.6%的市佔率。社區太陽能計畫日益普及,多個家庭受益於共享的太陽能追蹤系統,這有助於該領域的擴張。與智慧家庭技術的日益融合也使屋主能夠更有效地監控和最佳化能源消耗,從而促進市場成長。

在區域分析中,美國太陽能追蹤器市場在 2022 年的價值為 26 億美元,2023 年為 41 億美元,2024 年為 41.3 億美元。受優惠政策、豐富的太陽能資源和大型公用事業項目擴張的推動,北美在 2024 年將佔據全球 8.5% 以上的市場佔有率。預計聯邦和州的激勵措施以及旨在使追蹤器更經濟實惠、更適合住宅應用的持續創新將增強產業前景。持續開發具有成本效益的追蹤解決方案,以及增加對太陽能基礎設施的投資,將繼續為整個地區創造巨大的成長機會。

目錄

第1章:方法論與範圍

- 研究設計

- 基礎估算與計算

- 預測模型

- 初步研究與驗證

- 主要來源

- 資料探勘來源

- 市場定義

第2章:執行摘要

第3章:行業洞察

- 產業生態系統

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 價格趨勢分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 戰略儀表板

- 創新與技術格局

第5章:市場規模及預測:依產品,2021 年至 2034 年

- 主要趨勢

- 單軸

- 水平的

- 垂直的

- 雙軸

第6章:市場規模及預測:依技術分類,2021 年至 2034 年

- 主要趨勢

- 光電

- 雲端服務供應商

第7章:市場規模及預測:依應用,2021 年至 2034 年

- 主要趨勢

- 住宅

- 商業和工業

- 公用事業

第8章:市場規模及預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 法國

- 荷蘭

- 德國

- 瑞典

- 西班牙

- 奧地利

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 印尼

- 馬來西亞

- 新加坡

- 泰國

- 紐西蘭

- 菲律賓

- 越南

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 約旦

- 以色列

- 非洲

- 南非

- 埃及

- 阿爾及利亞

- 奈及利亞

- 摩洛哥

- 拉丁美洲

- 巴西

- 智利

第9章:公司簡介

- ArcelorMittal

- Array Technologies

- Arctech

- All Earth Renewables

- Convert Italia

- Degerenergie

- GameChange Solar

- Gonvarri Solar Steel

- Haosolar

- Ideematec

- Mecasolar

- Nclave

- Nextracker

- Powerway Renewable Energy

- PVHardware

- Scorpius Trackers

- SmartTrak Solar Systems

- Soltec

- STI Norland

- SunPower Corporation

- Trina Solar

The Global Solar Tracker Market was valued at USD 50.1 billion in 2024 and is projected to grow at a CAGR of 8.5% from 2025 to 2034. The increasing efficiency of solar power systems, coupled with the declining costs of solar trackers, is driving industry growth. These systems enhance solar panel performance, with single-axis trackers boosting energy output by 10-25% and dual-axis trackers by up to 40% compared to fixed-tilt installations. The integration of smart grid technologies and IoT allows for improved monitoring, control, and optimization of energy production, accelerating market expansion. The rising adoption of bifacial solar modules with single-axis trackers is expected to reduce the levelized cost of electricity by around 16% compared to traditional monofacial systems, further fueling product demand. Ongoing advancements in solar tracker technology are reshaping the industry by lowering costs, enhancing efficiency, and increasing the accessibility of solar energy across multiple applications.

The market is also benefiting from the integration of energy storage solutions, the emergence of hybrid solar tracking systems, and the use of eco-friendly materials to minimize environmental impact. Supportive regulatory policies, incentive programs, and government initiatives such as the U.S. Inflation Reduction Act and Australia's Solar Sunshot program are expected to strengthen business prospects.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $50.1 Billion |

| Forecast Value | $111.4 Billion |

| CAGR | 8.5% |

By product, the market is categorized into single-axis and dual-axis trackers. Single-axis trackers are projected to generate over USD 61 billion by 2034, offering an efficiency increase of 25-35% compared to fixed-tilt systems. Advancements in materials and design have improved reliability, reducing maintenance costs and extending lifespan, which enhances product adoption. Additionally, higher energy yields and efficiency improvements lead to better returns on investment, strengthening the industry landscape.

The market is segmented into residential, commercial & industrial, and utility applications. In 2024, the utility sector held an 85.6% share of the market. The growing popularity of community solar projects, where multiple households benefit from shared solar tracking systems, is contributing to segment expansion. Increasing integration with smart home technologies is also enabling homeowners to monitor and optimize energy consumption more effectively, fostering market growth.

In regional analysis, the U.S. solar tracker market recorded values of USD 2.6 billion in 2022, USD 4.1 billion in 2023, and USD 4.13 billion in 2024. North America held over 8.5% of the global market share in 2024, driven by favorable policies, abundant solar resources, and the expansion of large-scale utility projects. Federal and state incentives, along with continuous innovations aimed at making trackers more affordable and user-friendly for residential applications, are expected to reinforce the industry outlook. The ongoing development of cost-effective tracking solutions, alongside increasing investments in solar infrastructure, will continue to create significant growth opportunities across the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research Design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Price trend analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2021 – 2034 (USD Billion & MW)

- 5.1 Key trends

- 5.2 Single axis

- 5.2.1 Horizontal

- 5.2.2 Vertical

- 5.3 Dual axis

Chapter 6 Market Size and Forecast, By Technology, 2021 – 2034 (USD Billion & MW)

- 6.1 Key trends

- 6.2 PV

- 6.3 CSP

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Billion & MW)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial & industrial

- 7.4 Utility

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion & MW)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Netherlands

- 8.3.4 Germany

- 8.3.5 Sweden

- 8.3.6 Spain

- 8.3.7 Austria

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Australia

- 8.4.6 Indonesia

- 8.4.7 Malaysia

- 8.4.8 Singapore

- 8.4.9 Thailand

- 8.4.10 New Zealand

- 8.4.11 Philippines

- 8.4.12 Vietnam

- 8.5 Middle East

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Jordan

- 8.5.4 Israel

- 8.6 Africa

- 8.6.1 South Africa

- 8.6.2 Egypt

- 8.6.3 Algeria

- 8.6.4 Nigeria

- 8.6.5 Morocco

- 8.7 Latin America

- 8.7.1 Brazil

- 8.7.2 Chile

Chapter 9 Company Profiles

- 9.1 ArcelorMittal

- 9.2 Array Technologies

- 9.3 Arctech

- 9.4 All Earth Renewables

- 9.5 Convert Italia

- 9.6 Degerenergie

- 9.7 GameChange Solar

- 9.8 Gonvarri Solar Steel

- 9.9 Haosolar

- 9.10 Ideematec

- 9.11 Mecasolar

- 9.12 Nclave

- 9.13 Nextracker

- 9.14 Powerway Renewable Energy

- 9.15 PVHardware

- 9.16 Scorpius Trackers

- 9.17 SmartTrak Solar Systems

- 9.18 Soltec

- 9.19 STI Norland

- 9.20 SunPower Corporation

- 9.21 Trina Solar

太陽能追蹤器的全球市場的評估:各類型,各技術,各用途,各地區,機會,預測(2018年~2032年)

太陽能追蹤器的全球市場的評估:各類型,各技術,各用途,各地區,機會,預測(2018年~2032年) 太陽能追蹤器的印度市場評估:各類型,各技術,各用途,各地區,機會,預測(2018年度~2032年度)

太陽能追蹤器的印度市場評估:各類型,各技術,各用途,各地區,機會,預測(2018年度~2032年度) 全球太陽能追蹤器市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球太陽能追蹤器市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 2025 年太陽能追蹤器全球市場報告

2025 年太陽能追蹤器全球市場報告 2025 年發電用太陽能追蹤器全球市場報告

2025 年發電用太陽能追蹤器全球市場報告 太陽能追蹤器市場、規模、佔有率、趨勢、行業分析報告(依類型、應用和地區)- 市場預測,2025-2034年

太陽能追蹤器市場、規模、佔有率、趨勢、行業分析報告(依類型、應用和地區)- 市場預測,2025-2034年 中東和非洲太陽能追蹤器 -市場佔有率分析、行業趨勢、統計、成長預測(2025-2030)

中東和非洲太陽能追蹤器 -市場佔有率分析、行業趨勢、統計、成長預測(2025-2030) 亞太地區太陽能追蹤器:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)

亞太地區太陽能追蹤器:市場佔有率分析、產業趨勢和成長預測(2025-2030 年) 北美單軸太陽能追蹤器:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)

北美單軸太陽能追蹤器:市場佔有率分析、產業趨勢和成長預測(2025-2030 年) 北美太陽能追蹤器:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

北美太陽能追蹤器:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)