|

市場調查報告書

商品編碼

1699427

柴油動力房地產發電機市場機會、成長動力、產業趨勢分析及 2025-2034 年預測Diesel Powered Real Estate Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

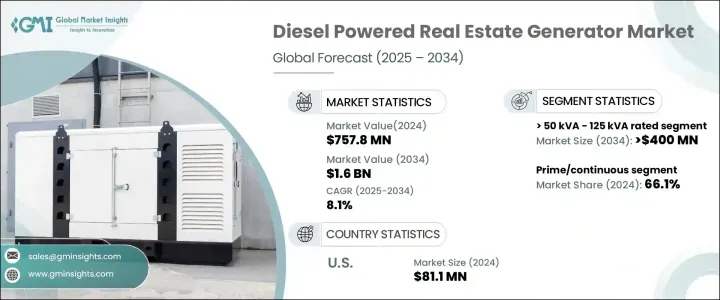

2024 年全球柴油動力房地產發電機市場規模達到 7.578 億美元,預計 2025 年至 2034 年期間的複合年成長率為 8.1%。隨著全球城市化進程的加速,對可靠、穩定的電力解決方案的需求不斷增加,市場正經歷顯著的發展勢頭。基礎設施的快速發展,尤其是在新興經濟體,正在擴大對備用和持續電源的需求。隨著房地產項目在住宅和商業領域的擴張,開發商正在投資高效且經濟的柴油發電機,以確保不間斷的電力供應。極端天氣條件導致的停電頻率增加、電網老化以及能源消耗增加進一步推動了市場擴張。

技術進步在推動市場成長方面繼續發揮關鍵作用。自動負載管理系統、電子燃油噴射和渦輪增壓機制等創新正在提高燃油效率並減少排放。旨在減少碳足跡的監管壓力促使製造商開發更清潔、更安靜、更節能的柴油發電機。政府和私人利益相關者正在大力投資備用電源解決方案,以減輕與電網故障相關的風險,確保房地產行業的業務連續性。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 7.578億美元 |

| 預測值 | 16億美元 |

| 複合年成長率 | 8.1% |

2024 年額定功率 <= 50 kVA 的柴油驅動房地產發電機的價值為 1.2 億美元。這些小型發電機的需求不斷成長,因為它們能夠在容易停電或缺乏可靠電網基礎設施的地區提供穩定的電力。燃油效率和噪音降低的進步使得這些發電機成為尋求穩定能源解決方案的屋主和企業的首選。這些裝置結構緊湊、性能卓越,在需要臨時或補充電力的城市和半城市發展中越來越受歡迎。

市場分為兩個主要應用領域:備用和主要/連續發電。 2024年,主要/連續發電機佔據總市場佔有率的66.1%,這得益於營運效率的提高和燃料節省能力的增強。公共和私人對採用先進噴射技術和智慧電源管理系統的下一代柴油引擎的投資正在提高採用率。隨著工業和房地產開發商優先考慮永續且強大的能源解決方案,對技術先進的柴油發電機的需求持續上升。

2024 年,美國柴油動力房地產發電機市場價值為 8,110 萬美元。極端天氣條件、電網老化和電力需求激增造成的電力中斷日益增多,加劇了對可靠備用電源解決方案的需求。房地產開發商、商業房地產所有者和基礎設施規劃人員正在轉向使用柴油發電機來維持不間斷運作並降低與電力故障相關的風險。美國市場仍是能源供應商的焦點,其投資主要集中在提高發電機效率、降低排放和擴大獨立於電網的電力解決方案。隨著人們對電力可靠性的擔憂日益加劇,柴油發電機在房地產應用中的作用變得比以往任何時候都更加重要。

目錄

第1章:方法論與範圍

- 市場範圍和定義

- 市場估計和預測參數

- 預測計算

- 資料來源

- 基本的

- 次要

- 有薪資的

- 民眾

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 戰略展望

- 創新與永續發展格局

第5章:市場規模及預測:依實力評級

- 主要趨勢

- ≤50千伏安

- > 50千伏安 - 125千伏安

- > 125 千伏安 - 200 千伏安

- > 200 千伏安 - 350 千伏安

- > 350千伏安 - 500千伏安

- > 500千伏安

第6章:市場規模與預測:按應用

- 主要趨勢

- 支援

- 主/連續

第7章:市場規模及預測:按地區

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 俄羅斯

- 英國

- 德國

- 法國

- 西班牙

- 奧地利

- 義大利

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 印尼

- 馬來西亞

- 泰國

- 越南

- 菲律賓

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 土耳其

- 伊朗

- 阿曼

- 非洲

- 埃及

- 奈及利亞

- 阿爾及利亞

- 南非

- 安哥拉

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 智利

第8章:公司簡介

- Aggreko

- Atlas Copco

- Caterpillar

- Cooper

- Cummins

- DEUTZ Power Center

- Generac Power Systems

- Greaves Cotton

- HIMOINSA

- JC Bamford Excavators

- Kirloskar

- Mahindra Powerol

- Rehlko

- Rolls-Royce

- YANMAR HOLDINGS

The Global Diesel Powered Real Estate Generator Market reached USD 757.8 million in 2024 and is projected to grow at a CAGR of 8.1% between 2025 and 2034. The market is witnessing significant momentum as urbanization accelerates worldwide, increasing the demand for reliable and stable power solutions. Rapid infrastructure development, especially in emerging economies, is amplifying the need for backup and continuous power sources. With real estate projects expanding in both residential and commercial sectors, developers are investing in efficient and cost-effective diesel generators to ensure uninterrupted power supply. The increasing frequency of power outages due to extreme weather conditions, aging grid networks, and growing energy consumption further fuels market expansion.

Technological advancements continue to play a critical role in driving market growth. Innovations such as automatic load management systems, electronic fuel injection, and turbocharging mechanisms are improving fuel efficiency and reducing emissions. Regulatory pressures aimed at minimizing carbon footprints have pushed manufacturers to develop cleaner, quieter, and more energy-efficient diesel generators. Governments and private stakeholders are heavily investing in backup power solutions to mitigate risks associated with grid failures, ensuring business continuity across real estate sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $757.8 Million |

| Forecast Value | $1.6 Billion |

| CAGR | 8.1% |

Diesel-powered real estate generators with a rating of <= 50 kVA were valued at USD 120 million in 2024. The rising demand for these smaller generators stems from their ability to deliver consistent power in regions prone to outages or lacking reliable grid infrastructure. Advancements in fuel efficiency and noise reduction have made these generators a preferred choice for homeowners and businesses seeking stable energy solutions. Compact and high-performing, these units are gaining traction in urban and semi-urban developments where temporary or supplemental power is essential.

The market is divided into two primary application segments: standby and prime/continuous power generation. In 2024, prime/continuous generators accounted for 66.1% of the total market share, driven by improvements in operational efficiency and enhanced fuel-saving capabilities. Public and private investments in next-generation diesel engines featuring advanced injection technologies and intelligent power management systems are bolstering adoption rates. As industries and real estate developers prioritize sustainable yet powerful energy solutions, the demand for technologically superior diesel generators continues to rise.

The U.S. diesel-powered real estate generator market was valued at USD 81.1 million in 2024. Increasing power disruptions caused by extreme weather conditions, an aging power grid, and surging electricity demand have intensified the need for reliable backup power solutions. Real estate developers, commercial property owners, and infrastructure planners are turning to diesel generators to maintain uninterrupted operations and mitigate risks associated with power failures. The U.S. market remains a focal point for energy providers, with investments directed toward upgrading generator efficiency, lowering emissions, and expanding grid-independent power solutions. As electricity reliability concerns grow, the role of diesel-powered generators in real estate applications is becoming more critical than ever.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Rating (USD Million & Units)

- 5.1 Key trends

- 5.2 ≤ 50 kVA

- 5.3 > 50 kVA - 125 kVA

- 5.4 > 125 kVA - 200 kVA

- 5.5 > 200 kVA - 350 kVA

- 5.6 > 350 kVA - 500 kVA

- 5.7 > 500 kVA

Chapter 6 Market Size and Forecast, By Application (USD Million & Units)

- 6.1 Key trends

- 6.2 Standby

- 6.3 Prime/continuous

Chapter 7 Market Size and Forecast, By Region (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Russia

- 7.3.2 UK

- 7.3.3 Germany

- 7.3.4 France

- 7.3.5 Spain

- 7.3.6 Austria

- 7.3.7 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.4.6 Indonesia

- 7.4.7 Malaysia

- 7.4.8 Thailand

- 7.4.9 Vietnam

- 7.4.10 Philippines

- 7.5 Middle East

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Turkey

- 7.5.5 Iran

- 7.5.6 Oman

- 7.6 Africa

- 7.6.1 Egypt

- 7.6.2 Nigeria

- 7.6.3 Algeria

- 7.6.4 South Africa

- 7.6.5 Angola

- 7.7 Latin America

- 7.7.1 Brazil

- 7.7.2 Mexico

- 7.7.3 Argentina

- 7.7.4 Chile

Chapter 8 Company Profiles

- 8.1 Aggreko

- 8.2 Atlas Copco

- 8.3 Caterpillar

- 8.4 Cooper

- 8.5 Cummins

- 8.6 DEUTZ Power Center

- 8.7 Generac Power Systems

- 8.8 Greaves Cotton

- 8.9 HIMOINSA

- 8.10 J C Bamford Excavators

- 8.11 Kirloskar

- 8.12 Mahindra Powerol

- 8.13 Rehlko

- 8.14 Rolls-Royce

- 8.15 YANMAR HOLDINGS

西北歐柴油發電機組:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)柴油發電機 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)中東和非洲柴油發電機市場:佔有率分析、行業趨勢、統計數據和 2025-2030 年預測亞太地區柴油發電機:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美柴油發電機市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印度柴油發電機市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲柴油發電機組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國柴油發電機市場佔有率分析、產業趨勢和成長預測(2025-2030 年)

西北歐柴油發電機組:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)柴油發電機 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)中東和非洲柴油發電機市場:佔有率分析、行業趨勢、統計數據和 2025-2030 年預測亞太地區柴油發電機:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美柴油發電機市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印度柴油發電機市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲柴油發電機組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國柴油發電機市場佔有率分析、產業趨勢和成長預測(2025-2030 年) 到 2030 年風冷發電機市場預測:按產品、類型、功率、系統、最終用戶和地區進行的全球分析

到 2030 年風冷發電機市場預測:按產品、類型、功率、系統、最終用戶和地區進行的全球分析 2024 年風冷發電機全球市場報告

2024 年風冷發電機全球市場報告