|

市場調查報告書

商品編碼

1708124

汽車燃油輸送幫浦市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Automotive Fuel Transfer Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

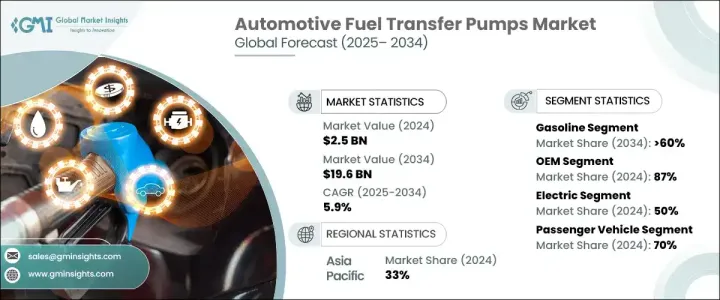

2024 年全球汽車燃油輸送幫浦市場價值為 25 億美元,預計 2025 年至 2034 年期間的複合年成長率為 5.9%。受汽車產量成長和對節油解決方案的需求不斷增加的推動,全球汽車產業不斷擴張,推動市場向前發展。隨著人們對高性能汽車的青睞日益成長,製造商正專注於提高引擎效率和耐用性的先進燃油輸送泵技術。新興經濟體,尤其是亞洲和拉丁美洲的新興經濟體,由於城市化進程加快、可支配收入增加以及政府支持本地汽車製造的政策,汽車銷售正在激增。由於汽車製造商強調車輛效率和法規遵循性,這直接促進了燃油輸送泵的採用率不斷提高。此外,全球範圍內向嚴格的燃油效率標準轉變,對最佳化燃料使用和減少排放的創新燃料轉移解決方案產生了需求。

汽車燃油輸送幫浦市場分為汽油和柴油兩類。 2024 年,汽油市場佔 60% 的佔有率,反映出其在乘用車領域的強勁地位。汽油動力汽車的廣泛使用,加上燃油效率技術的進步,加強了該領域的主導地位。由於汽油引擎排放量較低且燃料價格實惠,在許多地區,尤其是在環境法規影響汽車偏好的市場,消費者繼續青睞汽油引擎。旨在提高行駛里程和減少碳足跡的下一代汽油引擎的採用進一步推動了對高效燃油輸送泵的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 25億美元 |

| 預測值 | 196億美元 |

| 複合年成長率 | 5.9% |

原始設備製造商 (OEM) 在汽車燃油輸送泵市場中佔據領先地位。汽車製造商依賴OEM組件,因為它們具有相容性、可靠性和卓越的性能。 OEM 和主要汽車品牌之間建立的關係確保了供應鏈的一致性,促進了長期合約並加強了OEM供應商的主導地位。對OEM製造的燃油輸送泵的信任源於其能夠滿足嚴格的行業標準,從而確保現代車輛的最佳性能。

2024 年,亞太地區汽車燃油輸送泵市場將佔據 33% 的佔有率,主要汽車製造國的需求將激增。隨著產量的增加推動市場擴張,汽車工業蓬勃發展的國家繼續成為燃油輸送泵的主要消費國。政府支持的促進國內汽車製造業的激勵措施進一步加速了區域成長。亞太地區的基礎設施發展正在提高汽車供應鏈效率,支援各個車輛領域對先進燃油輸送泵的需求。

目錄

第1章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 材料供應商

- 製造商

- 經銷商

- 最終用途

- 利潤率分析

- 供應商格局

- 技術與創新格局

- 專利分析

- 成本明細

- 價格趨勢

- 監管格局

- 衝擊力

- 成長動力

- 對輕量和人體工學座椅的需求不斷成長

- 嚴格的安全和排放法規

- 電子商務和物流的成長

- 永續材料的進步

- 產業陷阱與挑戰

- 先進座椅技術成本高

- 供應鏈中斷

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 機械的

- 電力

第6章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 商用車

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第7章:市場估計與預測:按燃料,2021 - 2034 年

- 主要趨勢

- 汽油

- 柴油引擎

第8章:市場估計與預測:依銷售管道,2021 - 2034 年

- 主要趨勢

- OEM

- 售後市場

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Airtex Pumps

- Aisin Seiki

- Carter Fuel Systems

- Continental Automotive

- Cummins Fuel

- Delphi Technologies

- Denso Corporation

- Edelbrock Group

- GMB

- Hitachi Astemo

- Holley Performance Products

- Mitsubishi Electric

- Pierburg

- Robert Bosch

- Spectra Premium

- Stanadyne

- TI Fluid Systems

- UFI Filters

- VDO Automotive

- Walbro

The Global Automotive Fuel Transfer Pumps Market was valued at USD 2.5 billion in 2024 and is projected to grow at a CAGR of 5.9% between 2025 and 2034. The expanding global automotive industry, driven by rising vehicle production and increasing demand for fuel-efficient solutions, is propelling the market forward. With the growing preference for high-performance vehicles, manufacturers are focusing on advanced fuel transfer pump technologies that enhance engine efficiency and durability. Emerging economies, particularly in Asia and Latin America, are witnessing a surge in automobile sales due to rapid urbanization, rising disposable incomes, and government policies favoring local vehicle manufacturing. This has directly contributed to the increasing adoption of fuel transfer pumps as automakers emphasize vehicle efficiency and regulatory compliance. Additionally, the shift toward stringent fuel efficiency standards worldwide has created a demand for innovative fuel transfer solutions that optimize fuel usage and reduce emissions.

The automotive fuel transfer pumps market is segmented into gasoline and diesel fuel categories. The gasoline segment accounted for a 60% market share in 2024, reflecting its strong presence in the passenger vehicle sector. The widespread use of gasoline-powered cars, coupled with advancements in fuel efficiency technology, has strengthened the segment's dominance. Consumers continue to favor gasoline engines due to their lower emissions and affordable fuel prices in many regions, particularly in markets where environmental regulations influence vehicle preferences. The adoption of next-generation gasoline engines, designed for improved mileage and reduced carbon footprints, is further driving demand for efficient fuel transfer pumps.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 billion |

| Forecast Value | $19.6 billion |

| CAGR | 5.9% |

Original Equipment Manufacturers (OEMs) hold a leading position in the automotive fuel transfer pumps market. Automakers rely on OEM components due to their compatibility, reliability, and superior performance. Established relationships between OEMs and major automotive brands ensure a consistent supply chain, fostering long-term contracts and reinforcing the dominance of OEM suppliers. The trust in OEM-manufactured fuel transfer pumps stems from their ability to meet stringent industry standards, guaranteeing optimal performance in modern vehicles.

The Asia Pacific automotive fuel transfer pumps market commanded a 33% share in 2024, with demand surging in top vehicle manufacturing nations. Countries with robust automotive industries continue to be major consumers of fuel transfer pumps as increased production volumes drive market expansion. Government-backed incentives to promote domestic vehicle manufacturing further accelerate regional growth. Infrastructure developments across the Asia Pacific are enhancing automotive supply chain efficiency, supporting the demand for advanced fuel transfer pumps across various vehicle segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Material providers

- 3.1.1.2 Manufacturers

- 3.1.1.3 Distributors

- 3.1.1.4 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Cost breakdown

- 3.5 Price trend

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising demand for lightweight and ergonomic seating

- 3.7.1.2 Stringent safety and emission regulations

- 3.7.1.3 Growth in e-commerce and logistics

- 3.7.1.4 Advancements in sustainable materials

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High cost of advanced seating technologies

- 3.7.2.2 Supply chain disruptions

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Mechanical

- 5.3 Electrical

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Medium Commercial Vehicles (MCV)

- 6.3.3 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Gasoline

- 7.3 Diesel

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Airtex Pumps

- 10.2 Aisin Seiki

- 10.3 Carter Fuel Systems

- 10.4 Continental Automotive

- 10.5 Cummins Fuel

- 10.6 Delphi Technologies

- 10.7 Denso Corporation

- 10.8 Edelbrock Group

- 10.9 GMB

- 10.10 Hitachi Astemo

- 10.11 Holley Performance Products

- 10.12 Mitsubishi Electric

- 10.13 Pierburg

- 10.14 Robert Bosch

- 10.15 Spectra Premium

- 10.16 Stanadyne

- 10.17 TI Fluid Systems

- 10.18 UFI Filters

- 10.19 VDO Automotive

- 10.20 Walbro

汽車熱泵市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

汽車熱泵市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 汽車電動真空幫浦 (EVP) 市場:全球產業分析、規模、佔有率、成長、趨勢與預測,2025-2032 年汽車燃油供給幫浦市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

汽車電動真空幫浦 (EVP) 市場:全球產業分析、規模、佔有率、成長、趨勢與預測,2025-2032 年汽車燃油供給幫浦市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 汽車電動真空幫浦市場,按推進類型、按應用、按車輛類型、按國家和地區 - 2025 年至 2032 年的行業分析、市場規模、市場佔有率和預測

汽車電動真空幫浦市場,按推進類型、按應用、按車輛類型、按國家和地區 - 2025 年至 2032 年的行業分析、市場規模、市場佔有率和預測 2025 年全球汽車電動真空幫浦市場報告

2025 年全球汽車電動真空幫浦市場報告 汽車電動真空幫浦市場規模、佔有率和成長分析(按類型、車型、銷售管道、應用和地區)- 產業預測 2025-2032汽車電動燃油幫浦全球市場規模、佔有率和趨勢分析報告:按產品、技術、應用、地區和細分市場預測(2025-2030 年)2025 年全球汽車幫浦市場報告汽車電動燃油幫浦市場規模、佔有率、成長分析(按馬達類型、技術、地區)- 產業預測,2024-2031 年汽車幫浦市場規模、佔有率、成長分析、按類型、按技術、按排量、按車輛類型、按銷售管道、按地區 - 行業預測,2024-2031 年

汽車電動真空幫浦市場規模、佔有率和成長分析(按類型、車型、銷售管道、應用和地區)- 產業預測 2025-2032汽車電動燃油幫浦全球市場規模、佔有率和趨勢分析報告:按產品、技術、應用、地區和細分市場預測(2025-2030 年)2025 年全球汽車幫浦市場報告汽車電動燃油幫浦市場規模、佔有率、成長分析(按馬達類型、技術、地區)- 產業預測,2024-2031 年汽車幫浦市場規模、佔有率、成長分析、按類型、按技術、按排量、按車輛類型、按銷售管道、按地區 - 行業預測,2024-2031 年