|

市場調查報告書

商品編碼

1708241

汽車熱泵市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Automotive Pump for Thermal System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

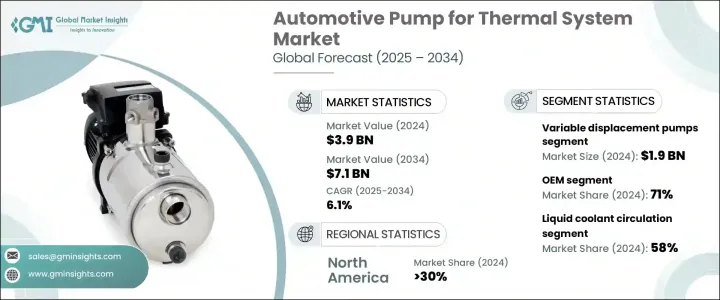

2024 年全球汽車熱系統幫浦市場價值為 39 億美元,預計 2025 年至 2034 年的複合年成長率為 6.1%。隨著汽車產業向電動車 (EV) 和混合動力電動車 (HEV) 轉變,對高效能熱管理系統的需求正在上升。這些系統對於維持車輛各個零件(包括電池和電力電子設備)的最佳溫度至關重要,而這些零件對於電動車的性能至關重要。由於這些熱系統透過保持溫度穩定性來幫助增強車輛功能和電池壽命,因此對先進冷卻解決方案的需求正在成長。

推動這一市場發展的一個重要因素是熱能回收系統(TERS)的興起,該系統用於捕獲引擎或排氣系統產生的廢熱。這些系統提高了整體能源效率,並進一步推動了對汽車幫浦的需求。這些幫浦透過在系統中循環冷卻劑、傳輸加熱的液體能量來操作輔助功能或增強駕駛性能發揮至關重要的作用。它們對於現代汽車(包括電動車和混合動力汽車)的開發至關重要。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 39億美元 |

| 預測值 | 71億美元 |

| 複合年成長率 | 6.1% |

市場根據泵浦類型細分,主要包括離心泵浦、正排量泵浦和變數泵浦。變數排氣量幫浦在 2024 年佔據 19 億美元的市場佔有率,預計在預測期內將呈現顯著成長。這些泵浦因其在複雜熱系統中的靈活性和響應性而受到青睞,它們可以在不同的駕駛條件下提供更好的控制,例如高性能駕駛或寒冷天氣和交通堵塞情況。

市場也根據銷售管道分為OEM和售後市場。 2024 年, OEM部門佔據 71% 的主導市場。 OEM 使用直接面對消費者的平台(包括電子商務)來分銷替換零件和售後泵。這種方法不僅擴大了他們的市場覆蓋範圍,而且還增強了客戶支援和回饋。

根據冷媒類型,市場分為油性冷媒、液體冷卻劑循環冷媒和空氣基冷媒。受電動和混合動力汽車對高效電池溫度管理的需求不斷成長的推動,液體冷卻劑循環領域在 2024 年佔據 58% 的多數佔有率。

汽車熱力系統幫浦市場進一步按推進類型分類,其中內燃機 (IC) 部分在 2024 年佔據最大佔有率。熱管理對於渦輪增壓引擎尤其重要,因為需要有效的冷卻系統來防止過熱並確保持久性能。

在北美,市場由美國主導,到 2024 年,該地區將佔據全球市場佔有率的 30% 以上。由於電池技術的進步和對更節能汽車的追求,對電動車熱管理系統的需求正在增加。

目錄

第1章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究與驗證

- 主要來源

- 資料探勘來源

- 市場定義

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 原物料供應商

- 零件供應商

- 泵浦裝配工

- 服務提供者

- 技術提供者

- 最終用途

- 利潤率分析

- 成本細分分析

- 技術與創新格局

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 電動和混合動力汽車需求不斷成長

- 熱能回收系統的採用日益增多

- 售後市場和更換需求的擴大

- 自動駕駛和連網汽車的成長

- 產業陷阱與挑戰

- 先進泵浦技術成本高昂

- 改造先進熱泵的複雜性

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按泵浦分類,2021 - 2034 年

- 主要趨勢

- 離心泵

- 電動水泵

- 機械水泵

- 容積泵

- 齒輪泵浦

- 葉片泵

- 活塞泵

- 螺桿泵

- 變數泵

第6章:市場估計與預測:按瓦特,2021 - 2034 年

- 主要趨勢

- 低於50瓦

- 50瓦 – 100瓦

- 100瓦 – 500瓦

- 500W以上

第7章:市場估計與預測:按推進方式,2021 - 2034 年

- 主要趨勢

- 冰

- 純電動車

- 插電式混合動力

- 油電混合車

第8章:市場估計與預測:按冷媒,2021 - 2034 年

- 主要趨勢

- 油基

- 液體冷卻劑循環(LCC)

- 空基

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 東南亞

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Aisin

- BorgWarner

- Bosch (Robert Bosch)

- Continental

- Denso

- Eberspaecher

- Fluid-o-Tech

- Grayson

- Hanon Systems

- Hitachi Astemo

- Infineon Technologies

- Johnson Electric Holdings Limited

- MAHLE

- Marelli

- Modine

- Nidec Corporation

- Rheinmetall AG

- Schaeffler

- Valeo

- ZF

The Global Automotive Pump for Thermal System Market, valued at USD 3.9 billion in 2024, is projected to grow at a CAGR of 6.1% from 2025 to 2034. As the automotive industry shifts towards electric vehicles (EVs) and hybrid electric vehicles (HEVs), the demand for efficient thermal management systems is rising. These systems are crucial for maintaining optimal temperatures in various vehicle components, including batteries and power electronics, which are critical to EV performance. The demand for advanced cooling solutions is growing as these thermal systems help enhance vehicle functionality and battery life by maintaining temperature stability.

A significant factor driving this market is the rise of thermal energy recovery systems (TERS), which are used to capture waste heat produced by engine or exhaust systems. These systems improve overall energy efficiency and further boost the demand for automotive pumps. These pumps play a vital role by circulating coolant through the system, transferring heated liquid energy to operate auxiliary features, or enhancing driving performance. They are essential in the development of modern vehicles, including EVs and HEVs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.9 Billion |

| Forecast Value | $7.1 Billion |

| CAGR | 6.1% |

The market is segmented based on pump type, with centrifugal pumps, positive displacement pumps, and variable displacement pumps being the main categories. Variable displacement pumps accounted for USD 1.9 billion of the market in 2024 and are expected to show significant growth over the forecast period. These pumps are preferred for their flexibility and responsiveness in complex thermal systems, where they provide better control under varying driving conditions, such as high-performance driving or in cold weather and heavy traffic situations.

The market is also divided by sales channel into OEM and aftermarket segments. In 2024, the OEM segment held a dominant market share of 71%. OEMs use direct-to-consumer platforms, including e-commerce, to distribute replacement parts and aftermarket pumps. This approach not only improves their market reach but also enhances customer support and feedback.

By refrigerant type, the market is segmented into oil-based, liquid coolant circulation, and air-based refrigerants. The liquid coolant circulation segment held a majority share of 58% in 2024, driven by the growing demand for efficient battery temperature management in electric and hybrid vehicles.

The automotive pump for thermal system market is further categorized by propulsion type, with the internal combustion (IC) engine segment holding the largest share in 2024. Thermal management is particularly crucial in turbocharged engines, where effective cooling systems are required to prevent overheating and ensure long-lasting performance.

In North America, the market was dominated by the U.S., with the region accounting for over 30% of the global market share in 2024. The demand for thermal management systems in EVs is increasing due to advancements in battery technology and the push for more energy-efficient vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material supplier

- 3.2.2 Component supplier

- 3.2.3 Pump assemblers

- 3.2.4 Service provider

- 3.2.5 Technology provider

- 3.2.6 End use

- 3.3 Profit margin analysis

- 3.4 Cost breakdown analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising demand for electric and hybrid vehicles

- 3.8.1.2 Growing adoption of thermal energy recovery systems

- 3.8.1.3 Expansion of aftermarket and replacement demand

- 3.8.1.4 Growth of autonomous and connected vehicles

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High cost of advanced pump technologies

- 3.8.2.2 Complexity in retrofitting advanced thermal pumps

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Pump, 2021 - 2034 ($Mn & Units)

- 5.1 Key trends

- 5.2 Centrifugal pumps

- 5.2.1 Electric water pump

- 5.2.2 Mechanical water pump

- 5.3 Positive displacement pumps

- 5.3.1 Gear pump

- 5.3.2 Vane pump

- 5.3.3 Piston pump

- 5.3.4 Screw pump

- 5.4 Variable displacement pumps

Chapter 6 Market Estimates & Forecast, By Watt, 2021 - 2034 ($Mn & Units)

- 6.1 Key trends

- 6.2 Below 50 W

- 6.3 50W – 100W

- 6.4 100W – 500W

- 6.5 Above 500W

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn & Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 BEV

- 7.4 PHEV

- 7.5 HEV

Chapter 8 Market Estimates & Forecast, By Refrigerant, 2021 - 2034 ($Mn & Units)

- 8.1 Key trends

- 8.2 Oil-based

- 8.3 Liquid Coolant Circulation (LCC)

- 8.4 Air-based

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aisin

- 10.2 BorgWarner

- 10.3 Bosch (Robert Bosch)

- 10.4 Continental

- 10.5 Denso

- 10.6 Eberspaecher

- 10.7 Fluid-o-Tech

- 10.8 Grayson

- 10.9 Hanon Systems

- 10.10 Hitachi Astemo

- 10.11 Infineon Technologies

- 10.12 Johnson Electric Holdings Limited

- 10.13 MAHLE

- 10.14 Marelli

- 10.15 Modine

- 10.16 Nidec Corporation

- 10.17 Rheinmetall AG

- 10.18 Schaeffler

- 10.19 Valeo

- 10.20 ZF

汽車電動真空幫浦 (EVP) 市場:全球產業分析、規模、佔有率、成長、趨勢與預測,2025-2032 年

汽車電動真空幫浦 (EVP) 市場:全球產業分析、規模、佔有率、成長、趨勢與預測,2025-2032 年 汽車燃油供給幫浦市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

汽車燃油供給幫浦市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 汽車電動真空幫浦市場,按推進類型、按應用、按車輛類型、按國家和地區 - 2025 年至 2032 年的行業分析、市場規模、市場佔有率和預測汽車燃油輸送幫浦市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

汽車電動真空幫浦市場,按推進類型、按應用、按車輛類型、按國家和地區 - 2025 年至 2032 年的行業分析、市場規模、市場佔有率和預測汽車燃油輸送幫浦市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 2025 年全球汽車電動真空幫浦市場報告

2025 年全球汽車電動真空幫浦市場報告 汽車電動真空幫浦市場規模、佔有率和成長分析(按類型、車型、銷售管道、應用和地區)- 產業預測 2025-2032汽車電動燃油幫浦全球市場規模、佔有率和趨勢分析報告:按產品、技術、應用、地區和細分市場預測(2025-2030 年)2025 年全球汽車幫浦市場報告汽車電動燃油幫浦市場規模、佔有率、成長分析(按馬達類型、技術、地區)- 產業預測,2024-2031 年汽車幫浦市場規模、佔有率、成長分析、按類型、按技術、按排量、按車輛類型、按銷售管道、按地區 - 行業預測,2024-2031 年

汽車電動真空幫浦市場規模、佔有率和成長分析(按類型、車型、銷售管道、應用和地區)- 產業預測 2025-2032汽車電動燃油幫浦全球市場規模、佔有率和趨勢分析報告:按產品、技術、應用、地區和細分市場預測(2025-2030 年)2025 年全球汽車幫浦市場報告汽車電動燃油幫浦市場規模、佔有率、成長分析(按馬達類型、技術、地區)- 產業預測,2024-2031 年汽車幫浦市場規模、佔有率、成長分析、按類型、按技術、按排量、按車輛類型、按銷售管道、按地區 - 行業預測,2024-2031 年