|

市場調查報告書

商品編碼

1687149

碳纖維:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Carbon Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

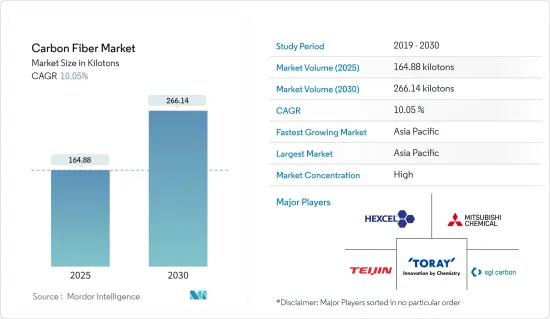

碳纖維市場規模預計在 2025 年為 164.88 千噸,預計在 2030 年達到 266.14 千噸,預測期內(2025-2030 年)的複合年成長率為 10.05%。

由於新冠疫情,2020 年汽車、建築和航太等多個行業的產量均下降。由於世界各地政府強制停工,終端用戶活動暫時停止,全球汽車和航太航太業受到了疫情的嚴重影響。然而,在疫情過後,該行業正在復甦,預計未來幾年將實現顯著成長。

主要亮點

- 從中期來看,航太和國防領域的最新進步以及風力發電領域的不斷擴大的應用是市場成長的主要驅動力。

- 另一方面,回收碳纖維的供應鏈安全和替代品的可用性是市場限制。

- 再生碳纖維的日益普及以及對使用木質素作為碳纖維原料的日益重視可能會在預測期內為市場帶來機會。

- 從數量上看,亞太地區佔據全球市場主導地位,其中中國佔據了大部分需求。

碳纖維市場趨勢

航太和國防工業佔市場主導地位

- 根據最終用戶產業,航太和國防佔據最大的市場佔有率。在過去的幾年中,該領域增添了一些新內容。碳纖維是許多航太和國防應用的絕佳選擇,因為它可以提供您所需的強度、耐用性和穩定性。

- 在國防工業中,碳纖維增強塑膠(CFRP)可用於飛彈防禦、地面防禦和軍事海洋。

- 在北美,不斷增加的消費者支出和不斷老化的民航機隊是影響航太工業整體採用碳纖維產品的主要因素。

- 預計在預測期內,亞洲航太技術市場碳纖維需求將出現最高成長率,這得益於以中國等新興經濟體為主導的整個全部區域對民航機的需求不斷增加。

- COVID-19 加速了航空航太領域的幾個現有趨勢,市場參與企業將永續技術、整合產業以及環境、社會和治理(ESG) 列為 COVID-19 後該領域的三大主題。

- 例如,波音公司的《2022-2041年商業展望》估計,到2041年,全球新飛機的交付總量將達到41,170架。隨著預期交付如此巨大,全球飛機生產對碳纖維的需求可能會增加。

- 2021年全球國防支出首次超過2兆美元。 2021年全球開支比2020年成長0.7%。國防支出排名前五名的國家分別是美國、中國、印度、英國和俄羅斯。這佔總支出的62%。預計這將增加國防應用對碳纖維的需求。

- 航太和國防工業的這些趨勢預計將推動碳纖維市場的發展。

亞太地區佔市場主導地位

- 由於中國和印度等國家各類終端用戶產業的成長,預計亞太地區將在產量方面佔據全球市場的主導地位。

- 中國航空公司計劃未來20年購買約7,690架新飛機,價值約1.2兆美元,預計將進一步推動碳纖維的市場需求。

- 根據波音《民用飛機展望2022-2041》,預計2041年中國將交付約8,485架新飛機,市場服務價值達5,450億美元。這些新交付可能會增加對碳纖維的需求。

- 根據斯德哥爾摩國際和平研究所(SIPRI)統計,印度軍費開支達766億美元,位居世界第三。這比2020年增加了0.9%。為促進國內軍火工業的加強,2021年軍事預算將64%的資本支出用於採購國產武器。

- 印度風電裝置容量目前排名世界第四,總設備容量為3,925萬千瓦(截至2021年3月31日),2,020-21年發電量約6,014.9萬單位。風電產業的擴張帶來了強大的生態系統、計劃營運能力和每年約 10,000 兆瓦的製造基地。

- 預計預測期內所有上述因素都將對該地區碳纖維市場的需求產生重大影響。

碳纖維產業概況

全球碳纖維市場呈現整合趨勢,主要企業之間為擴大市場佔有率展開激烈競爭。碳纖維市場的主要企業包括東麗工業公司、西格里碳素公司、三菱化學公司、赫氏公司、帝人株式會社等(不分先後順序)。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 航太和國防領域的最新進展

- 擴大風力發電領域的應用

- 限制因素

- 再生碳纖維供應鏈安全

- 替代產品的可用性

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 定價分析

- 技術前景 - 快速概覽

- 生產分析

第5章 市場區隔

- 原料

- 聚丙烯腈(PAN)

- 石油瀝青和人造絲

- 類型

- 原生纖維 (VCF)

- 再生碳纖維(RCF)

- 應用

- 複合材料

- 紡織品

- 微電極

- 催化劑

- 最終用戶產業

- 航太和國防

- 替代能源

- 車

- 建築與基礎設施

- 體育用品

- 其他最終用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作、協議

- 市場佔有率(%)分析

- 主要企業策略

- 公司簡介

- A&P Technology Inc.

- Anshan Sinocarb Carbon Fibers Co. Ltd

- DowAksa USA LLC

- Formosa Plastics Corporation

- Hexcel Corporation

- Holding company Composite

- Hyosung Advanced Materials

- Jiangsu Hengshen Co. Ltd

- Mitsubishi Chemical Corporation

- Nippon Graphite Fiber Co. Ltd

- SGL Carbon

- Solvay

- Teijin Limited

- Toray Industries Inc.

- Zhongfu Shenying Carbon Fiber Co. Ltd

第7章 市場機會與未來趨勢

- 再生碳纖維越來越受歡迎

- 強調使用木質素作為碳纖維的原料

The Carbon Fiber Market size is estimated at 164.88 kilotons in 2025, and is expected to reach 266.14 kilotons by 2030, at a CAGR of 10.05% during the forecast period (2025-2030).

Due to COVID-19, production in various industries, including automotive, construction, aerospace, etc., decreased in 2020. The global automotive and aerospace industry has been heavily impacted by the pandemic, considering a temporary halt in end-user activities due to government-imposed lockdowns in various parts of the world. However, in the post-pandemic scenario, the industry has recovered and is expected to grow at a significant rate during the coming years.

Key Highlights

- In the medium term, the major factors driving the growth of the market studied are recent advancements in the aerospace and defense sector and increasing applications in the wind energy sector.

- On the flip side, supply chain security for recycled carbon fiber and the availability of substitutes have been acting as restraints to the market studied.

- The increasing popularity of recycled carbon fiber and the emphasis on the usage of lignin as raw material for carbon fiber is likely to act as opportunities for the market studied over the forecast period.

- In terms of volume, Asia-Pacific dominated the market studied across the world, with China accounting for most of the demand.

Carbon Fiber Market Trends

Aerospace and Defense Industry to Dominate the Market

- Aerospace and defense account for the largest share of the market based on end-user industries. Over the past few years, there have been several new products added in this field. Carbon fibers are a perfect choice for numerous aerospace and defense applications as they provide strength, endurance, and stability as required.

- In the defense industry, the use of carbon fiber-reinforced plastics (CFRP) is present in missile defense, ground defense, and military marine.

- In North America, higher consumer spending and the constant aging of commercial aircraft are among the primary factors influencing the overall product penetration of carbon fibers in the aerospace industry.

- In Asia, the market for carbon fibers in aerospace technology is likely to witness the highest growth rate over the forecast period due to the rising demand for commercial aircraft across the region, especially in emerging economies, including China.

- COVID-19 has accelerated several pre-existing trends in aviation and aerospace, with market participants identifying sustainable technologies, industry consolidation, and environmental, social, and corporate governance (ESG) as the three biggest themes in the post-COVID-19 space.

- For instance, according to the Boeing Commercial Outlook 2022-2041, the total global deliveries of new airplanes are estimated to be 41,170 by 2041. Owing to such huge expected deliveries, the demand for carbon fiber during aircraft production is likely to rise across the world.

- The global defense expenditure crossed USD 2 trillion for the first time in 2021. Global spending was 0.7% higher in 2021 compared to 2020. The top five countries with the highest defense expenditure were the United States, China, India, the United Kingdom, and Russia. They accounted for 62% of the total spending. This is likely to increase the demand for carbon fiber used in defense applications.

- Such trends in the aerospace and defense industries are expected to drive the carbon fiber market.

Asia-Pacific to Dominate the Market

- The Asia Pacific region is expected to dominate the global market in terms of volume due to the growth of various end-user industries in countries like China and India.

- The Chinese airline companies are planning to purchase about 7,690 new aircraft in the next 20 years, which were valued at approximately USD 1.2 trillion, which is further expected to raise the market demand for carbon fiber.

- According to the Boeing Commercial Outlook 2022-2041, in China, around 8,485 new deliveries are likely to be made by 2041, with a market service value of USD 545 billion. Owing to such new deliveries in the country, the demand for carbon fiber is likely to rise.

- According to the Stockholm International Peace Research Institute (SIPRI), India's military spending of USD 76.6 billion ranked third highest in the world. This was up by 0.9% from 2020. In a push to strengthen the indigenous arms industry, 64% of capital outlays in the military budget of 2021 were earmarked for acquisitions of domestically produced arms.

- India currently has the fourth-highest wind installed capacity in the world, with a total installed capacity of 39.25 GW (as of March 31, 2021), and generated around 60.149 billion units during 2020-21. The expansion of the wind industry resulted in a strong ecosystem, project operation capabilities, and a manufacturing base of about 10,000 MW per annum.

- All the aforementioned factors are expected to show a significant impact on the demand for the carbon fiber market in the region over the forecast period.

Carbon Fiber Industry Overview

The global carbon fiber market is consolidated in nature, with intense competition among the top players to increase their share in the market. The major companies in the carbon fiber market include (not in any particular order) Toray Industries Inc., SGL Carbon, Mitsubishi Chemical Corporation, Hexcel Corporation, and Teijin Limited, among other companies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Recent Advancements in Aerospace and Defense Sector

- 4.1.2 Increasing Applications in Wind Energy Sector

- 4.2 Restraints

- 4.2.1 Supply Chain Security for Recycled Carbon Fiber

- 4.2.2 Availability of Substitutes

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Analysis

- 4.6 Technology Landscape - Quick Snapshot

- 4.7 Production Analysis

5 MARKET SEGMENTATION (Market Size in Volume and Value)

- 5.1 Raw Material

- 5.1.1 Polyacrylonitrile (PAN)

- 5.1.2 Petroleum Pitch and Rayon

- 5.2 Type

- 5.2.1 Virgin Fiber (VCF)

- 5.2.2 Recycled Carbon Fiber (RCF)

- 5.3 Application

- 5.3.1 Composite Materials

- 5.3.2 Textiles

- 5.3.3 Microelectrodes

- 5.3.4 Catalysis

- 5.4 End-user Industry

- 5.4.1 Aerospace and Defense

- 5.4.2 Alternative Energy

- 5.4.3 Automotive

- 5.4.4 Construction and Infrastructure

- 5.4.5 Sporting Goods

- 5.4.6 Other End-user Industries

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 A&P Technology Inc.

- 6.4.2 Anshan Sinocarb Carbon Fibers Co. Ltd

- 6.4.3 DowAksa USA LLC

- 6.4.4 Formosa Plastics Corporation

- 6.4.5 Hexcel Corporation

- 6.4.6 Holding company Composite

- 6.4.7 Hyosung Advanced Materials

- 6.4.8 Jiangsu Hengshen Co. Ltd

- 6.4.9 Mitsubishi Chemical Corporation

- 6.4.10 Nippon Graphite Fiber Co. Ltd

- 6.4.11 SGL Carbon

- 6.4.12 Solvay

- 6.4.13 Teijin Limited

- 6.4.14 Toray Industries Inc.

- 6.4.15 Zhongfu Shenying Carbon Fiber Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Popularity of Recycled Carbon Fiber

- 7.2 Emphasis on Usage of Lignin as Raw Material for Carbon Fiber

大絲束碳纖維市場 - 全球產業規模、佔有率、趨勢、機會和預測,按技術、應用、地區和競爭細分,2020-2030 年預測

大絲束碳纖維市場 - 全球產業規模、佔有率、趨勢、機會和預測,按技術、應用、地區和競爭細分,2020-2030 年預測 2025 年至 2033 年,運動器材市場中碳纖維的種類(PAN 基、瀝青基及其他)、應用(運動棍棒、球拍、滑雪板和滑雪板及其他)和地區報告2025 年碳纖維全球市場報告

2025 年至 2033 年,運動器材市場中碳纖維的種類(PAN 基、瀝青基及其他)、應用(運動棍棒、球拍、滑雪板和滑雪板及其他)和地區報告2025 年碳纖維全球市場報告 CABKOMA 市場規模、佔有率和成長分析(按類型、應用和地區)- 產業預測 2025-2032

CABKOMA 市場規模、佔有率和成長分析(按類型、應用和地區)- 產業預測 2025-2032 全球碳纖維市場(2025-2029)

全球碳纖維市場(2025-2029) 北美碳纖維:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲碳纖維 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

北美碳纖維:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲碳纖維 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 碳纖維建築修復市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

碳纖維建築修復市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 建築玻璃纖維紡織品市場報告:2030 年趨勢、預測與競爭分析消費性玻璃纖維紡織品市場報告:2030 年趨勢、預測與競爭分析

建築玻璃纖維紡織品市場報告:2030 年趨勢、預測與競爭分析消費性玻璃纖維紡織品市場報告:2030 年趨勢、預測與競爭分析