|

市場調查報告書

商品編碼

1521868

共享出行:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Shared Mobility - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

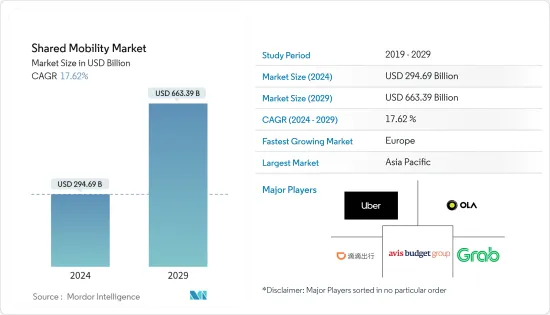

共享旅遊市場規模預計到 2024 年為 2,946.9 億美元,預計到 2029 年將達到 6,633.9 億美元,在預測期內(2024-2029 年)複合年成長率為 17.62%。

從長遠來看,隨著消費者對叫車、汽車共享和租賃服務的偏好增加,較低的出行成本可能會推動全球共享旅遊市場的發展。由於交通堵塞加劇以及購買新車相關的擁有成本不斷上升,消費者擴大轉向叫車服務進行日常通勤。此外,各種新參與企業與強大競爭對手的整合預計將擾亂市場。例如,叫車平台 inDrive 提供了一個適合司機和消費者的基於競標的平台。

主要亮點

- 2023年第三季度,北京、長春、重慶成為中國尖峰時段壅塞最嚴重的大城市。 2023年第三季尖峰時段壅塞指數為北京2.09、長春2.05、重慶1.97。

- 根據TomTom指數,2023年全球交通壅塞最嚴重的大城市是倫敦、都柏林和多倫多。倫敦行駛10公里的平均時間為37分20秒,是全世界最長的。

由於交通便利以及在交通堵塞時騎行的便利性,對兩輪網約車和共享服務的需求不斷增加,特別是在亞太地區。亞太地區共用微出行市場突出的國家包括印度、中國和越南,因為與使用叫車服務相比,申請較低。此外,近年來,為了配合政府的脫碳努力,共享旅遊產業擴大採用電動二輪車,預計這將推動2024年至2029年共享旅遊市場的成長。

主要亮點

- 2023 年 8 月,Green and Smart Mobility (GSM) 宣佈在越南推出電動自行車叫車服務,以鞏固其市場地位,並與 GoJek 和 Grab 等參與企業競爭。此外,該公司還宣布計劃在越南五個省份的道路上營運 60,000 輛電動馬達。

此外,企業部門投資的增加和世界都市化的提高正在促使消費者遷移到都市區尋找更好的就業機會。隨著越來越多的消費者遷移到都市區,這些地區預計將產生大量的就業需求,進而擴大員工交通需求的市場。為了滿足員工日益成長的出行需求,各共享出行業者正在製定策略,透過提供隨選接駁車服務進入這一領域,從而增加全球共享出行市場的需求,從而產生積極影響。

共享出行市場趨勢

預計乘用車領域將成為2024年至2029年的驅動力

乘用車廣泛應用於叫車、汽車共享、出租及租賃服務。企業和私人業主部署各種車型,包括掀背車、轎車和運動型多用途車 (SUV),以提高客戶的便利性。因此,由於對叫車和租賃服務的大規模需求,都市化的提高和全球遊客的湧入是乘用車市場成長的關鍵決定因素。此外,旨在擴大就業機會和促進經濟成長的企業部門投資增加,將導致企業要求提供員工流動租賃服務,這反過來將對乘用車領域的需求產生積極影響。

- 根據世界旅遊組織(WTO)的預測,2023年全球國際觀光遊客總數將達到12.5866億人次,而2022年為9.6019億人次,2022年至2023年比與前一年同期比較成長31.0%。

- 根據人口研究所的數據,2023年北美、拉丁美洲和歐洲是全球城市人口最多的主要大陸。 2023年,北美城市人口比例將達83%,其次是拉丁美洲(82%)和歐洲(75%)。

全球的叫車業者和租賃公司越來越傾向於採用電動乘用車,以補充政府為運輸業脫碳所做的努力。此外,越來越多的消費者要求電動乘用車作為他們的首選交通途徑,這些營運商正在大力投資,將新時代的車輛引入持有,以滿足不斷成長的需求,這預計將對該市場的成長產生正面影響。

- 2023 年 11 月,越南叫車公司 Green and Smart Mobility (GSM) 宣佈在寮國和越南推出電動計程車服務,將自有品牌定位為永續的共用交通途徑。該公司計劃部署 VinFast VF5 電動車,以擴大可供越南和寮國消費者使用的車隊。

預計全球各叫車和租賃公司將持續整合共享旅遊市場。隨著越來越多的企業融入生態系統,共享出行用乘用車將產生巨大的需求。此外,消費者的偏好正在轉向使用成本較低的私人交通,預計這將進一步推動該細分市場的成長。

亞太地區是全球最大的共享旅遊市場

由於亞太地區對個人交通便利性的需求不斷成長、網際網路普及率較高以及遊客數量不斷增加,消費者對使用個人交通出行的偏好不斷增加,這已成為移動市場成長的重要驅動力。此外,由於交通堵塞加劇以及快速城市交通的需求,該地區對兩輪叫車服務的需求強勁,這對該細分市場的成長產生了積極影響。

- 根據世界旅遊組織預測,2023年亞太地區國際觀光人數將達2.3343億人次,2022年為9,152萬人次,2022年至2023年年與前一年同期比較155.0%。

- 根據TomTom指數,印度的班加羅爾和普納分別被評為全球第6和第7最擁擠城市。在班加羅爾,通勤者行駛 10 公里的平均時間為 28 分 10 秒,而在普納那則達到 27 分 50 秒。

此外,將電動車納入共用出行可以顯著減少經濟中的碳排放。因此,亞太地區各國政府擴大制定策略,促進電動車在租賃、叫車和其他共用出行車隊中的使用。各種新參與企業正在大力投資,將電動車引入其車隊,以滿足不斷成長的消費者需求。

- 2023 年 9 月,Ola Cabs 宣佈在班加羅爾推出電動自行車服務,以加速印度各地叫車的電氣化。從2023年9月到2024年1月,該公司完成了超過175萬次乘車,標誌著該細分市場成長了40%。該公司計劃未來幾年在印度各地城市推出這項服務。

此外,中國、韓國和印度等國家的商業投資不斷成長,導致企業積極尋求租賃解決方案,預計這將進一步促進該地區共享旅遊市場的快速成長。未來幾年,亞太地區的公司將花費大量資金來增強其數位平台以吸引消費者,並積極尋求與汽車製造商的合作夥伴關係,以更低的成本購買車輛。

共享旅遊行業概況

由於生態系中存在各種國內外參與企業,共享出行市場呈現細分化且競爭激烈。知名參與企業包括Uber Technologies Inc.、ANI Technologies Pvt. Ltd.、Avis Budget Group Inc.、北京滴滴出行科技、Grab Holdings Inc.、Hertz Global Holdings、Lyft Inc.、Drive Now (BMW AG),其中包括Europcar Mobility Group、Cabify、Curb Mobility 和 BlaBlaCar。這些參與企業正在積極尋求擴展到其他地區,以提高品牌知名度,並不斷致力於改善消費者體驗。

- 2024 年 4 月,Yulu 宣布與 Yuva Mobility 合作,在印度印多爾和中央邦推出基於專利權、合作夥伴主導的共享旅遊服務。此次合作將為消費者提供電動車作為共享旅遊服務。此外,該公司的目標是擴大基本客群,以滿足這些城市的學生、休閒騎士、遊客和專業人士對電動車快速成長的需求。

- 2024年4月,Hoop Carpool宣布取得Mango Startup Studio以可轉換票據形式的投資。這項投資旨在促進為期六個月的試用期,在此期間,Mango 員工和其他汽車共享乘客將使用 Hoop Carpool 的服務進行日常通勤。

預計市場將見證生態系統中營運的公司之間的各種併購,這將提高盈利前景並有助於滿足更廣泛的客戶群。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行概述

第4章市場動態

- 市場促進因素

- 消費者對乘車服務的偏好不斷上升預計將推動市場成長

- 市場限制因素

- 監管共享出行行業的嚴格政府法規阻礙了市場成長

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔(市場規模-美元)

- 按類型

- 計程車

- 汽車共享

- 共享微型交通(電動自行車、電動Scooter等)

- 出租租賃

- 其他(接駁車服務、巴士服務等)

- 按車型

- 客車

- 輕型商用車(皮卡車等)

- 巴士/遠距巴士

- 摩托車

- 按經營模式

- P2P(P2P)

- 企業對企業交易 (B2B)

- 企業對消費者 (B2C)

- 依推進類型

- 內燃機(ICE)

- 電

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 其他

- 南美洲

- 中東/非洲

- 北美洲

第6章 競爭狀況

- 供應商市場佔有率

- 公司簡介

- Uber Technologies Inc.

- ANI Technologies Pvt. Ltd(Ola Cabs)

- Avis Budget Group Inc.

- Beijing Didi Chuxing Technology Co. Ltd

- Hertz Global Holdings

- Grab Holdings Inc.

- Lyft Inc.

- Drive Now(BMW AG)

- Europcar Mobility Group

- Cabify

- Zoomcar Holdings

- Revv

- Curb Mobility LLC

- BlaBlaCar

- Wingz Inc.

第7章市場機會與未來趨勢

- 私家車持有成本高帶動市場需求

The Shared Mobility Market size is estimated at USD 294.69 billion in 2024, and is expected to reach USD 663.39 billion by 2029, growing at a CAGR of 17.62% during the forecast period (2024-2029).

In the long term, consumers' increasing preference toward ride-hailing, car-sharing, and rental services owing to the lower cost of transportation will drive the shared mobility market across the world. Due to the increasing traffic congestion and higher ownership cost of purchasing new vehicles, consumers tend to avail ride-hailing as a preferred medium for their daily commutes. Further, the integration of various new entrants with a strong competitive edge is expected to disrupt the market. For instance, inDrive, a ride-hailing platform, offers a bid-based platform suitable for both drivers and consumers, as it helps negotiate a fixed price for short-distance travel and avoids the surge price charged by other competitors.

Key Highlights

- In Q3 2023, Beijing, Changchun, and Chongqing were the leading cities in China with the highest rush hour congestion. The rush hour congestion index in Beijing touched 2.09 in Q3 2023, followed by Changchun with an index of 2.05 and Chongqing with an index of 1.97 during the same period.

- According to the TomTom Index, London, Dublin, and Toronto were the major city centers across the world with the highest traffic congestion in 2023. The average time to travel 10 km in London is 37 minutes and 20 seconds, the highest in the world.

The ease of travel and the convenience of driving through traffic are leading to an increasing demand for two-wheeler hailing and sharing services, especially in Asia-Pacific. Some prominent countries with a significant shared micro-mobility market across Asia-Pacific include India, China, and Vietnam, which are attributed to the lower cost charged compared to availing a car-hailing service. Further, in recent years, there has been a massive penetration of electric two-wheelers in the shared mobility industry to complement the government's decarbonization effort, which is expected to foster the growth of the shared mobility market between 2024 and 2029.

Key Highlights

- In August 2023, Green and Smart Mobility (GSM) announced the commencement of its e-motorcycle-hailing service in Vietnam to solidify its market position and compete with players such as GoJek and Grab. Further, the company stated its plan to operate 60,000 e-motorcycles on Vietnamese roads in five localities across the country.

Moreover, increasing investment in the corporate sector and the worldwide urbanization rate contribute to consumers migrating to urban areas for better employment opportunities. With more consumers migrating to urban areas, there is a massive demand for jobs in these areas, which, in turn, is expected to expand the market for employee transportation needs. To cater to the increasing need for employee transportation, various shared mobility players are strategizing to enter this space by offering on-demand shuttle services, which, in turn, positively impact the demand for the shared mobility market worldwide.

Shared Mobility Market Trends

The Passengers Cars Segment is Expected to Gain Traction Between 2024 and 2029

Passenger cars are extensively utilized in ride-hailing, car-sharing, rental, and leasing services. Operators or individual owners deploy various car makes, such as hatchbacks, sedans, and sports utility vehicles (SUVs), to enhance customers' convenience. Therefore, the growing urbanization rate and the influx of tourists worldwide are significant determinants for the growth of the passenger cars segment, owing to their massive requirement for ride-hailing and rental services. Moreover, the rising investment in the corporate sector to expand job opportunities and expand economic growth leads to businesses demanding leasing services for employee transportation purposes, which, in turn, is positively impacting the demand for passenger cars segment.

- According to the World Tourism Organization, the total number of international tourist arrivals worldwide reached 1,258.66 million in 2023 compared to 960.19 million in 2022, representing a 31.0% Y-o-Y growth between 2022 and 2023.

- According to the Population Reference Bureau, North America, Latin America, and Europe were the leading continents worldwide with the highest urban population in 2023. The share of urban population as a percentage of the overall population in North America touched 83% in 2023, followed by Latin America (82%) and Europe (75%) during the same period.

To complement the government's effort to decarbonize the transport sector, ride-hailing operators and rental providers worldwide increasingly prefer deploying electric passenger cars in their fleets. Further, with more consumers demanding electric passenger cars as their preferred choice of transportation, these players are expected to invest hefty sums in acquiring new-age vehicles in their fleet to meet the surging demand, which, in turn, will positively impact the growth of this market segment.

- In November 2023, Green and Smart Mobility (GSM), a Vietnamese-based ride-hailing company, announced the launch of its electric taxi service in Laos and Vietnam to position its brand as a sustainable mode of shared transportation. The company plans to deploy Vinfast VF5 electric cars to expand its fleet, which will be available to consumers in Vietnam and Laos.

The shared mobility market is anticipated to witness the integration of various ride-hailing and rental companies worldwide, attributed to the lucrative opportunity that the market presents. As more companies integrate into the ecosystem, a massive demand will exist for passenger cars to be utilized for shared mobility. Moreover, consumers are shifting their preferences toward availing of lower-cost private transportation, which is further expected to foster the growth of this segment.

Asia-Pacific is the Largest Shared Mobility Market Across the World

Consumers' increasing preference toward availing private mediums of transportation for traveling purposes owing to the rising need for convenience in personal mobility, high internet penetration rate, and the growing number of tourists in Asia-Pacific serve as significant drivers for the growth of the shared mobility market. Moreover, this region witnesses a substantial demand for two-wheeler hailing services due to the worsening traffic congestion and the need for faster city travel, which, in turn, positively impacts the growth of this segment.

- According to the World Tourism Organization, the number of international tourist arrivals in Asia-Pacific reached 233.43 million in 2023 compared to 91.52 million in 2022, representing a Y-o-Y growth of 155.0% between 2022 and 2023.

- According to the TomTom Index, Bengaluru and Pune in India were the sixth and seventh cities with the highest traffic congestion worldwide, respectively. The average travel time for commuters to travel 10 km in Bengaluru was 28 minutes and 10 seconds, while it reached 27 minutes and 50 seconds in Pune.

Further, integrating electric vehicles in shared mobility fleets can significantly reduce carbon emissions from the economy. Hence, governments across Asia-Pacific are increasingly strategizing to promote the use of electric vehicles in rental, ride-hailing, and other shared mobility fleets. Various new entrants are investing hefty sums in deploying electric cars in their fleets to cater to the increasing consumer demand.

- In September 2023, Ola Cabs announced the launch of its e-bike service in Bengaluru to promote the electrification of ride-hailing fleets across India. Between September 2023 and January 2024, the company witnessed a 40% expansion in this segment by completing more than 1.75 million rides. The company plans to launch this service across cities in India in the coming years.

Moreover, the expanding corporate investment in countries such as China, South Korea, and India is actively leading to companies demanding rental solutions, which, in turn, is further anticipated to contribute to the surging growth of the shared mobility market in the region. In the coming years, Asia-Pacific will witness companies spending hefty sums to enhance their digital platforms to attract consumers and actively seek partnerships with automakers to acquire vehicles in their fleet at a lower cost.

Shared Mobility Industry Overview

The shared mobility market is fragmented and highly competitive due to the presence of various international and domestic players operating in the ecosystem. Some prominent players include Uber Technologies Inc., ANI Technologies Pvt. Ltd, Avis Budget Group Inc., Beijing DiDi Chuxing Technology Co. Ltd, Grab Holdings Inc., Hertz Global Holdings, Lyft Inc., Drive Now (BMW AG), Europcar Mobility Group, Cabify, Curb Mobility, and BlaBlaCar. These players actively seek to expand their business into other geographies to enhance their brand visibility and constantly focus on improving consumer experience.

- In April 2024, Yulu announced its partnership with Yuva Mobility to launch franchise-based partner-led shared mobility services in Indore and Madhya Pradesh, India. The partnership will witness the introduction of electric vehicles offered to consumers as shared mobility services. Further, the company aims to expand its customer base to cater to the surging demand for EVs among students, leisure riders, tourists, and professionals in these cities.

- In April 2024, Hoop Carpool announced that it had raised an investment from Mango Startup Studio in the form of a convertible equity loan. The investment aims to facilitate a six-month trial period during which Mango employees and other car-sharing riders will use Hoop Carpool services for their daily commutes.

The market is anticipated to witness various mergers and acquisitions between firms operating in the ecosystem, which will assist them in enhancing their profitability prospects and help cater to a broader customer base.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Preference of Consumers toward Ride-Hailing Services is Expected to Foster the Growth of the Market

- 4.2 Market Restraints

- 4.2.1 Strict Government Regulations to Govern the Shared Mobility Industry Hampers the Growth of the Market

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Type

- 5.1.1 Ride-Hailing

- 5.1.2 Car Sharing

- 5.1.3 Shared Micromobility (E-Bikes, E-Scooters, etc.)

- 5.1.4 Rental and Leasing

- 5.1.5 Others (Shuttle Services, Bus Services, etc.)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles (Pickup Vans, etc.)

- 5.2.3 Buses and Coaches

- 5.2.4 Two-Wheelers

- 5.3 By Business Model

- 5.3.1 Peer-to-Peer (P2P)

- 5.3.2 Business-to-Business (B2B)

- 5.3.3 Business-to-Consumer (B2C)

- 5.4 By Propulsion Type

- 5.4.1 Internal Combustion Engine (ICE)

- 5.4.2 Electric

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 South America

- 5.5.4.2 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Uber Technologies Inc.

- 6.2.2 ANI Technologies Pvt. Ltd (Ola Cabs)

- 6.2.3 Avis Budget Group Inc.

- 6.2.4 Beijing Didi Chuxing Technology Co. Ltd

- 6.2.5 Hertz Global Holdings

- 6.2.6 Grab Holdings Inc.

- 6.2.7 Lyft Inc.

- 6.2.8 Drive Now (BMW AG)

- 6.2.9 Europcar Mobility Group

- 6.2.10 Cabify

- 6.2.11 Zoomcar Holdings

- 6.2.12 Revv

- 6.2.13 Curb Mobility LLC

- 6.2.14 BlaBlaCar

- 6.2.15 Wingz Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 High Cost of Ownership of Private Vehicles Fuels the Market Demand

2025年共享出行全球市場報告

2025年共享出行全球市場報告 中國共享旅遊市場:2023-2030消費者之聲:印度汽油二輪車購買者概況消費者的評價:北美皮卡買家概況

中國共享旅遊市場:2023-2030消費者之聲:印度汽油二輪車購買者概況消費者的評價:北美皮卡買家概況 共享出行市場規模、佔有率、成長分析、按服務模式、按分銷管道、按車輛、按地區 - 行業預測,2024-2031 年

共享出行市場規模、佔有率、成長分析、按服務模式、按分銷管道、按車輛、按地區 - 行業預測,2024-2031 年 共享出行市場:按類型、車輛類型、經營模式- 2025-2030 年全球預測歐洲農村地區的共享出行,2024-2030全球共享旅遊市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測

共享出行市場:按類型、車輛類型、經營模式- 2025-2030 年全球預測歐洲農村地區的共享出行,2024-2030全球共享旅遊市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測 共享出行市場,按服務模式、按車輛推進、按銷售管道、按車輛類型、按國家和地區分類 - 2024-2032 年行業分析、市場規模、市場佔有率和預測2024 年全球共享出行預測與展望

共享出行市場,按服務模式、按車輛推進、按銷售管道、按車輛類型、按國家和地區分類 - 2024-2032 年行業分析、市場規模、市場佔有率和預測2024 年全球共享出行預測與展望