|

市場調查報告書

商品編碼

1536884

氣凝膠:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Aerogel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

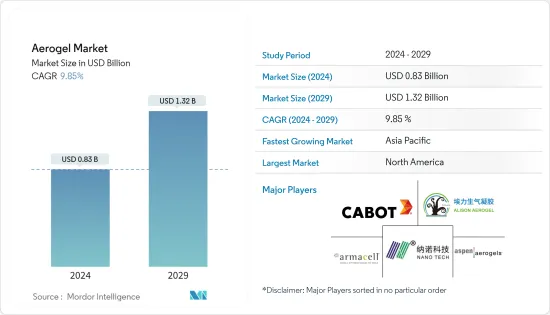

預計2024年全球氣凝膠市場規模將達8.3億美元,2029年將達13.2億美元,2024-2029年預測期間複合年成長率為9.85%。

COVID-19 大流行對全球氣凝膠市場產生了顯著影響。需求最初下降是由於建築和製造業的中斷,這些行業是隔熱氣凝膠的主要消費者。然而,限制解除後,市場出現了顯著的成長,疫情後人們更加關注節能建築材料,帶動了對氣凝膠隔熱材料的需求。

*從中期來看,隨著建築和石油和天然氣行業需求的激增,可重複使用和可回收氣凝膠的採用越來越多,預計將推動市場需求。

*另一方面,高製造成本預計將阻礙市場發展。

*技術進步和投資增加為市場成長提供了各種機會。

*預計北美將主導市場,亞太地區預計將在 2024 年至 2029 年保持最高複合年成長率。

氣凝膠市場趨勢

石油和天然氣產業主導市場

*氣凝膠因其優異的性能而廣泛應用於石油和天然氣行業。氣凝膠可用於管道隔熱、選擇性吸收污染物和碳氫化合物等特定分子的吸收劑以及提高採收率。

*氣凝膠具有結構輕質、耐腐蝕、降噪、過濾能力等多種優點,使其成為油氣管道產業很有前景的材料。

*氣凝膠產品有多種形式,可以滿足石油和天然氣行業的各種需求。氣凝膠產品易於安裝,可為加工商和安裝商節省成本,而營運商則受益於更低的資本成本、更長的冷卻時間、穩定的生命場U 值和更低的風險,並透過卓越的熱性能提供多種優勢。它提供最佳的熱性能、防止腐蝕並提供機械強度。

*根據國際能源總署 (IEA)資料,到 2026 年,世界石油消費量預計將達到每天 1.041 億桶以上。這將比目前水準高出 440 萬桶/日。

*根據美國能源情報署報告,2023年全球原油產量將達到10175萬桶/日,較2022年的9999萬桶/日增加。

*美國、俄羅斯、加拿大、沙烏地阿拉伯和中國是全球市場的主要石油生產國。

*根據美國能源情報署的數據,2023年全球原油產量增加1.76%至101,749,000桶/日。

*到 2045 年,印度預計每天需要 1,100 萬桶石油,是目前數量的兩倍。此外,多家公司正在投資擴大全國各地的探勘設施。例如,ONGC於2022年5月宣布計劃在2022會計年度和2025會計年度投資40億美元,擴大在印度的探勘活動。

*沙烏地阿拉伯擁有世界已探明石油蘊藏量的約17%,是最大的石油淨出口國之一。沙烏地阿拉伯已探明的石油蘊藏量位居世界第二。沙烏地阿美公司繼續在其上游領域採取重大擴張措施和管道投資,包括原油、冷凝油油、天然氣和液態天然氣(NGL) 的探勘和生產。

*在歐洲,英國正在探索擴大石油和天然氣生產的新領域。例如,該國政府預計在 2023 年至 2027 年間示範 66 個新的石油和天然氣發電計劃。此外,2023年7月,該國宣布計劃在北海發放多個新的石油和天然氣許可證,以確保其能源蘊藏量。

*因此,由於上述因素,石油和天然氣行業預計將顯著成長,這反過來又會增加所研究市場的需求。

北美市場佔據主導地位

*在北美,美國預計將引領市場。

*美國政府更嚴格的環境標準、環保產品意識的增強以及對氣凝膠製造產品和工藝開拓的廣泛研究是美國在調查市場中保持領先地位的關鍵因素。氣凝膠廣泛用作隔熱材料、隔音材料。

*美國能源局(DOE) 正在投資創新隔熱材料節省工業領域的能源和成本。

*此外,由於建築業以及石油和天然氣行業的快速成長,預計美國市場在預測期內將迅速擴張。

*美國石油和天然氣產業最近取得了重大發展。根據美國能源情報署預計,2023年美國原油產量將達到1,290萬桶/日,比2022年的1,190萬桶/日成長8.5%。二疊紀地區的產量增加和墨西哥灣(GOM)的產量增加正在推動預期的產量增加。增加石油產量需要全面運作的煉油廠和高效率的運輸網路來支援市場需求。

*根據加拿大建築協會的數據,建築業是加拿大最大的雇主之一,也是加拿大經濟成功的主要貢獻者。該產業每年產值約 1,410 億美元,佔國內生產總值(GDP) 的 7.5%。 2023年,加拿大的建築開工量增加了5.8%。新開非住宅建築成長15.4%,土木工程成長16.2%。

*為了實現永續目標,聯邦政府已投資 1.5 億加元(1.114 億美元)來制定加拿大永續建築戰略。該策略預計將動員國家行動來降低成本和轉變市場,以在 2023 會計年度實現這一目標。

*墨西哥的戰略定位、有利的商業環境和熟練的勞動力使其成為尋求建立生產設施的汽車公司的重要目的地。對無排放氣體汽車的需求不斷增加,導致德國、中國和美國等國家對汽車製造業,特別是電動車製造業的外國直接投資增加,從而增加了電動車對氣凝膠的需求。

*由於所有這些因素,預計北美地區將在預測期內影響市場。

氣凝膠產業概況

氣凝膠市場已部分整合。市場主要企業(排名不分先後)包括Aspens Aerogels Inc.、Cabot Corporation、Armacell、Nano Tech和廣東艾利森高科。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 由於再生性和可回收性,氣凝膠的採用率增加

- 建築業需求快速成長

- 石油和天然氣產業主導氣凝膠需求

- 抑制因素

- 生產成本高

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模:金額)

- 類型

- 二氧化矽

- 碳

- 氧化鋁

- 其他類型

- 形狀

- 毯子

- 粒子

- 堵塞

- 控制板

- 最終用戶產業

- 石油和天然氣

- 建造

- 車

- 海洋

- 航太

- 其他最終用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭狀況

- 合併、收購、合資、合作夥伴關係和協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- Active Aerogels

- Aerogel Technologies LLC

- Aerogel-it Gmbh

- Amracell

- Aspen Aerogels Inc.

- Cabot Corporation

- Enersens

- Guangdong Alison Technology Co. Ltd

- Jios Aerogel

- Nano Tech Co. Ltd

- Ningbo Surnano Aerogel Co. Ltd

- Sino Aerogel

- Svenska Aerogel

- Taasi Corporation

- Thermablok Aerogels Limited

第7章 市場機會及未來趨勢

- 技術進步和投資增加拉動市場需求

The Aerogel Market size is estimated at USD 0.83 billion in 2024, and is expected to reach USD 1.32 billion by 2029, growing at a CAGR of 9.85% during the forecast period (2024-2029).

The COVID-19 pandemic had a notable impact on the global aerogel market. Initially, demand declined due to disruptions in the construction and manufacturing sectors, which are key consumers of aerogel for insulation purposes. However, the market registered a significant growth rate after the restrictions were lifted due to increased focus on energy-efficient building materials post-pandemic, which is driving demand for aerogel insulation.

* Over the medium term, a rise in the adoption of aerogel due to its reusability and recyclability, as well as rapidly growing demand from the construction and oil and gas industries, is expected to drive the market demand.

* On the flip side, the high cost of production is expected to hinder the market.

* Technological advancements and increasing investments offer various opportunities for the growth of the market studied.

* North America is expected to dominate the market, while Asia-Pacific is expected to witness the highest CAGR between 2024 and 2029.

Aerogel Market Trends

The Oil and Gas Industry to Dominate the Market

* Aerogels are widely used in the oil and gas industry due to their exceptional properties. They are used for insulating pipelines, as an absorbent to selectively absorb specific molecules, such as contaminants or hydrocarbons, and for enhanced oil recovery.

* They offer a range of advantages, such as lightweight construction, corrosion resistance, noise reduction, and filtration capabilities, making them a promising material for the oil and gas pipeline industry.

* Aerogel products are available in a wide range of forms to meet the different requirements of the oil and gas sector. Aerogel products are easy to install, which results in cost savings for fabricators and installers while delivering operators various benefits of exceptional thermal performance, such as lower capital costs, longer cool-down times, consistent life-offield U-values, and reduced risk. They offer the highest thermal performance, prevent corrosion, and offer mechanical strength.

* Global oil consumption is expected to reach over 104.1 million barrels per day by 2026, as per the International Energy Agency data. This would be a 4.4 mb/d increase over current levels.

* As per the US Energy Information Administration report, global crude oil production reached 101.75 million barrels per day in 2023, as compared to 99.99 million barrels per day in 2022, registering a growth.

* The United States, Russia, Canada, Saudi Arabia, and China are the leading oil producers in the global market.

* According to the United States Energy Information Administration, global crude oil production in 2023 increased by 1.76% and was valued at 101.749 million barrels per day.

* By 2045, India is expected to need 11 million barrels of oil per day, which is double what it needs now. Moreover, various companies are investing in expanding exploration facilities across the country. For instance, in May 2022, ONGC announced plans to invest USD 4 billion in FY 2022 and FY 2025 to increase its exploration efforts in India.

* Saudi Arabia has approximately 17% of the world's proven petroleum reserves and is one of the largest net petroleum exporters. Saudi Arabia has the world's second-largest proven oil reserves. Saudi Aramco continues its primary expansionary phase and channel investments in its upstream segment, which includes exploration & production of crude oil, condensate, natural gas, and natural gas liquids (NGL).

* In Europe, the United Kingdom is exploring new grounds to produce more oil and gas. For instance, the government expects the country to witness 66 new oil and gas generation projects between 2023 and 2027. Moreover, the country announced in July 2023 that it plans to issue several new oil and gas licenses in the North Sea to secure energy reserves.

* Thus, due to the abovementioned factors, the oil and gas industry is expected to grow significantly, which, in turn, will enhance the demand for the market studied.

North America to Dominate the Market

* The United States is expected to be the leading country in North America for the studied market.

* The growing stringent environmental norms by the United States government, growing awareness of eco-friendly products, and extensive research on product and process development to manufacture aerogel are the key factors helping the United States remain in the top position in the market studied. Aerogel is highly used in thermal and acoustic insulation.

* The US Department of Energy (DOE) is investing in innovative insulation materials that save energy and money in the industrial sector.

* Furthermore, with the rapidly growing building and construction sector and oil and gas industries, the market studied in the United States is expected to increase rapidly over the forecast period.

* The oil and gas sector in the United States has witnessed significant developments in recent years. According to the United States Energy Information Administration, the US crude oil production reached 12.9 million barrels per day (b/d) in 2023, an increase of 8.5% compared to 2022, which was 11.9 million barrels per day. Increased production in the Permian region and increased production of the Gulf of Mexico (GOM) are driving projected production growth. Increasing oil production requires fully operational refineries and an efficient transport network to work consistently, thus supporting the demand for the market studied.

* According to the Canadian Construction Association, the construction sector is one of Canada's largest employers and a significant contributor to the country's economic success. The industry generates about USD 141 billion annually and contributes 7.5% of the country's Gross Domestic Product (GDP). In 2023, Canadian construction starts rose by 5.8%. Both new non-residential building and civil engineering increased by 15.4% and 16.2%, respectively.

* To achieve sustainable goals, the federal government has committed CAD 150 million (USD 111.40 million) to developing the Canada Sustainable Buildings Strategy. This strategy is projected to reduce costs and mobilize national action to transform markets to meet this goal in FY 2023.

* Owing to its strategic location, favorable business environment, and skilled labor force, Mexico has become an important destination for automotive companies looking to establish their production facilities. As the demand for non-emission vehicles is increasing, FDIs from countries such as Germany, China, the United States, and others into automotive manufacturing, especially electric vehicle manufacturing in the country, are increasing, thereby boosting the demand for aerogels in electric vehicles.

* The North American region is expected to influence the market during the forecast period due to all these factors.

Aerogel Industry Overview

The aerogel market is partially consolidated in nature. Some of the major players in the market (not in any particular order) include Aspens Aerogels Inc., Cabot Corporation, Armacell, Nano Tech Co. Ltd, and Guangdong Alison Hi-tech Co. Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rise in Adoption of Aerogel due to their Reusability and Recyclability

- 4.1.2 Rapid Growing Demand from Construction Industry

- 4.1.3 Oil and Gas Industry Dominating the Aerogel Demand

- 4.2 Restraints

- 4.2.1 High Cost of Production

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Silica

- 5.1.2 Carbon

- 5.1.3 Alumina

- 5.1.4 Other Types

- 5.2 Form

- 5.2.1 Blanket

- 5.2.2 Particles

- 5.2.3 Blocks

- 5.2.4 Panels

- 5.3 End-user Industry

- 5.3.1 Oil and Gas

- 5.3.2 Construction

- 5.3.3 Automotive

- 5.3.4 Marine

- 5.3.5 Aerospace

- 5.3.6 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Active Aerogels

- 6.4.2 Aerogel Technologies LLC

- 6.4.3 Aerogel-it Gmbh

- 6.4.4 Amracell

- 6.4.5 Aspen Aerogels Inc.

- 6.4.6 Cabot Corporation

- 6.4.7 Enersens

- 6.4.8 Guangdong Alison Technology Co. Ltd

- 6.4.9 Jios Aerogel

- 6.4.10 Nano Tech Co. Ltd

- 6.4.11 Ningbo Surnano Aerogel Co. Ltd

- 6.4.12 Sino Aerogel

- 6.4.13 Svenska Aerogel

- 6.4.14 Taasi Corporation

- 6.4.15 Thermablok Aerogels Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements and Increasing Investments Propelling the Market Demand

2025年氣凝膠全球市場報告

2025年氣凝膠全球市場報告 氣凝膠的全球市場(2025年~2035年)

氣凝膠的全球市場(2025年~2035年) 氣凝膠市場規模、佔有率和成長分析(按類型、形式、加工、應用、最終用途和地區)- 2025-2032 年產業預測

氣凝膠市場規模、佔有率和成長分析(按類型、形式、加工、應用、最終用途和地區)- 2025-2032 年產業預測 氣凝膠隔熱材料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

氣凝膠隔熱材料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 氣凝膠市場:按類型、加工、形式、應用分類 - 2025-2030 年全球預測氣凝膠市場規模、佔有率、趨勢分析報告:按產品、按形式、按最終用途、按技術、按地區、細分市場預測,2025-2030

氣凝膠市場:按類型、加工、形式、應用分類 - 2025-2030 年全球預測氣凝膠市場規模、佔有率、趨勢分析報告:按產品、按形式、按最終用途、按技術、按地區、細分市場預測,2025-2030 全球氣凝膠市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測2030 年氣凝膠市場預測:按產品、形狀、應用、最終用戶和地區進行的全球分析氣凝膠市場 - 2024 年至 2029 年預測

全球氣凝膠市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測2030 年氣凝膠市場預測:按產品、形狀、應用、最終用戶和地區進行的全球分析氣凝膠市場 - 2024 年至 2029 年預測 全球氣凝膠市場:按類型、形狀、加工、應用、地區分類 - 預測(截至 2029 年)

全球氣凝膠市場:按類型、形狀、加工、應用、地區分類 - 預測(截至 2029 年)