|

市場調查報告書

商品編碼

1628802

義大利紙包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)Italy Paper Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

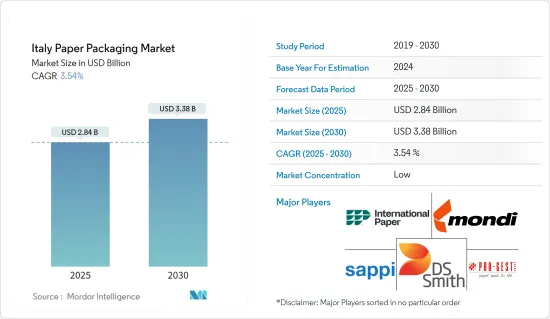

義大利紙包裝市場規模預估至2025年為28.4億美元,預估至2030年將達33.8億美元,預測期間(2025-2030年)複合年成長率為3.54%。

主要亮點

- 近年來,由於對永續性和環境的日益關注,義大利對紙包裝的需求穩步成長。義大利已採用歐盟法規來減少塑膠廢棄物,鼓勵企業轉向紙張替代品。由於紙質包裝解決方案的可回收性和永續性,歐洲的一次性塑膠指令鼓勵各行業的公司採用紙質包裝解決方案。

- 義大利消費者高度的環保意識對紙質包裝的採用產生了重大影響。食品和飲料、化妝品和奢侈品行業的公司正在從塑膠包裝轉向紙包裝。這項轉變旨在滿足環境標準並展示對永續性的承諾。

- 食品和飲料行業接受紙質產品,包括各種食品的紙盒、袋子和包裝紙。消費者對永續性的興趣以及有機和健康食品的興起正在推動對紙包裝的需求。隨著餐飲業外帶和外送服務的擴展,紙質包裝已成為首選。

- 電子商務的擴張增加了對耐用和永續包裝解決方案的需求。隨著義大利網路購物的成長,公司開始採用紙質包裝進行運輸和交付。電商公司普遍使用瓦楞紙箱和紙包裝,它們具有成本效益、重量輕且可回收,同時滿足了具有環保意識的消費者的需求。

- 公司正在透過開發新的解決方案和技術來創新紙包裝市場。例如,2024年6月,Saika集團與億滋共同開發了一種用於多包裝糖果零食、餅乾和巧克力產品的可回收紙質包裝解決方案。該包裝設計為透過標準紙張回收流程進行處理。這種包裝材料與熱封包裝工藝相容,有塗層和無塗層兩種版本。這項發展符合歐洲造紙工業聯合會 (CEPI) 制定的永續性標準。

- 由於原料成本上升和外包趨勢,義大利紙包裝市場的成長面臨限制。主要原料紙漿價格上漲,增加了製造商的生產成本。這些成本增加轉嫁給消費者時,可能會減少需求,特別是對價格敏感的中小型企業造成影響。義大利公司將生產外包到低成本地區的趨勢正在影響當地供應鏈,延長交貨時間並降低品管能力。儘管外包具有成本優勢,但它可能會阻礙創新和永續實踐,因為公司將降低成本置於環保措施之上。儘管對環保包裝解決方案的需求不斷增加,但這些綜合因素正在限制市場成長。

義大利紙包裝市場趨勢

瓦楞紙箱佔較大市場佔有率

- 在電子商務、物流和製造業的推動下,義大利對瓦楞紙箱的需求持續成長。網路購物的擴張增加了對直接面對消費者運輸的可靠且經濟高效的包裝解決方案的需求。電子商務公司需要可客製化的包裝選項,而瓦楞紙箱因其保護品質、成本效益和品牌潛力而極具吸引力。

- 義大利作為全球重要出口國的地位影響瓦楞包裝的需求。時尚、食品和汽車等行業依靠紙板來安全地進行產品的國際運輸。該國以出口為導向的經濟需要符合國際運輸標準的包裝。瓦楞紙箱提供遠距運輸所需的耐用性和保護,並確保產品在運輸過程中的完整性。

- 2023年義大利出口額將達6,769.6億美元,增加瓦楞紙箱的需求。義大利是機械、汽車、食品和時尚的主要出口國,需要可靠的國際運輸包裝解決方案。瓦楞紙箱在運輸過程中為貨物提供必要的保護,同時符合環境永續標準。義大利出口活動的不斷擴大正在支持瓦楞包裝市場的成長。

- 永續性已成為包裝產業的重要因素,義大利公司正在優先考慮環保選擇。由可回收廢紙生產的瓦楞紙板符合這些環保要求。歐盟 (EU) 實施嚴格的回收和廢棄物法規,增加了對包括紙板在內的可回收材料的需求。

- 義大利食品和飲料行業需要廣泛的瓦楞包裝解決方案。出口到世界各地的義大利食品需要安全和保護性的運輸包裝。紙板對於包裝葡萄酒、橄欖油、義式麵食和其他食品至關重要。該行業需要能夠在國內和國際運輸過程中保持產品新鮮度和安全性的包裝解決方案。

- 在電子商務擴張、永續性要求和該國出口活動的支持下,義大利瓦楞紙箱市場預計將保持成長軌跡。包裝設計的發展,包括更輕的重量和更高的強度,預計將增加瓦楞包裝在整個行業的採用。出口對耐用、高品質包裝的需求可能繼續成為市場的基本驅動力。

飲料領域預計將佔據很大的市場佔有率

- 在義大利,由於對永續性的擔憂日益增加,飲料包裝對紙張的需求持續增加。作為葡萄酒、烈酒和軟性飲料等飲料的主要生產國和出口國,義大利需要既能提供保護又具有環境效益的包裝解決方案。紙包裝已成為飲料製造商的首選,因為它具有高度生物分解性和可回收性,滿足生態學要求和消費者偏好。

- 在義大利葡萄酒產業,紙包裝(主要是紙箱和盒子)被廣泛用於出口過程中的安全運輸。受消費者偏好和環境合規要求的影響,隨著生產商轉向永續包裝解決方案,葡萄酒出口的紙包裝需求預計將增加。

- 預計到2024年,義大利非碳酸飲料市場銷售額將達到6.7446億美元,銷售量將達到4.95億公升,推動紙包裝需求不斷成長。果汁、瓶裝水和茶的消費量不斷增加,需要有效且永續的包裝解決方案。紙包裝因其生物分解性和可回收的特性而成為這些飲料的首選,解決了消費者和生產商的環境問題。

- 由於非碳酸飲料在義大利飲料行業佔據主導地位,製造商已轉向紙盒和瓶子。這項轉變符合歐盟減少塑膠使用和促進永續包裝的法規。紙盒和多層紙包裝擴大用於果汁、茶和水產品,以滿足消費者對環保解決方案的偏好和監管要求。非碳酸飲料領域的穩健表現繼續鞏固了紙張作為義大利飲料行業主要包裝材料的地位。

- 歐盟 (EU) 法規對義大利飲料業的紙包裝需求產生重大影響。歐盟嚴格的包裝廢棄物指南要求公司使用可回收和可重複使用的材料。這個法律規範促使義大利飲料製造商引入紙質包裝解決方案,以滿足永續性要求並減少塑膠廢棄物。

- 紙包裝技術的創新正在增強義大利的需求。最近的趨勢,包括紙質瓶子和多層紙盒,正在增加飲料保護,同時保持永續性標準。這些技術改進增加了紙包裝對生產商和消費者的吸引力,並使義大利飲料產業處於永續包裝趨勢之中。

義大利紙包裝產業概況

義大利紙包裝市場較為分散。這是一個有多家公司參與的競爭市場。 DS Smith Plc、International Paper Company、Sappi Limited、Mondi Group 和 Pro-Gest SpA 等在該國營運的公司不斷創新、投資並建立戰略夥伴關係,以保持市場佔有率。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 消費者議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 產業價值鏈分析

第5章市場動態

- 市場促進因素

- 消費者對紙包裝的認知不斷增強

- 電子商務銷售成長

- 餐飲業需求增加

- 封閉式回收工作有助於將紙質包裝材料推向市場

- 市場限制因素

- 對紙包裝引起的森林砍伐的擔憂

- 原料成本上升與外包

第6章 市場細分

- 依產品類型

- 折疊式紙盒

- 瓦楞紙箱

- 其他產品類型(撓性紙、液體包裝等)

- 按最終用戶產業

- 食品

- 飲料

- 衛生保健

- 個人護理

- 電氣/電子產品

- 其他最終用戶產業

第7章 競爭格局

- 公司簡介

- DS Smith Plc

- International Paper Company

- Sappi Limited

- Smurfit Westrock

- Mondi Group

- Seda International Packaging Group

- Tetra Pak International SA

- Pro-Gest SpA

第8章投資分析

第9章 市場未來展望

The Italy Paper Packaging Market size is estimated at USD 2.84 billion in 2025, and is expected to reach USD 3.38 billion by 2030, at a CAGR of 3.54% during the forecast period (2025-2030).

Key Highlights

- The demand for paper packaging in Italy has experienced a steady rise in recent years, driven by the growing emphasis on sustainability and environmental concerns. Italy has adopted European Union regulations to reduce plastic waste, prompting businesses to shift towards paper alternatives. The EU's Single-Use Plastics Directive has encouraged companies across sectors to adopt paper-based packaging solutions due to their recyclability and sustainability.

- Italian consumers' eco-conscious attitudes have significantly influenced the adoption of paper packaging. Companies in the food and beverages, cosmetics, and luxury goods industries are transitioning from plastic to paper packaging. This shift serves to meet environmental standards and demonstrate their commitment to sustainability.

- The food and beverage industry has embraced paper-based products, including cartons, bags, and wraps for various food items. Consumer focus on sustainability and the growth of organic and health-conscious food products has increased paper packaging demand. The food service industry's expansion in takeout and delivery services has established paper packaging as the preferred choice.

- E-commerce expansion has increased the need for durable and sustainable packaging solutions. As online shopping grows in Italy, businesses adopt paper packaging for shipping and delivery. E-commerce companies commonly use corrugated cardboard boxes and paper wraps, which are cost-effective, lightweight, and recyclable while meeting environmentally conscious consumer demands.

- Companies are innovating in the paper packaging market by developing new solutions and technologies. For instance, in June 2024, Saica Group and Mondelez collaborated to create a recyclable paper-based packaging solution for multipack confectionery, biscuits, and chocolate products. The packaging is designed to be processed through standard paper recycling streams. The packaging material is compatible with heat-sealable packing processes and is available in coated and uncoated variants. The development aligns with the sustainability standards established by the Confederation of European Paper Industries (CEPI).

- The paper packaging market in Italy faces growth limitations due to increasing raw material costs and outsourcing trends. The rising prices of paper pulp, a primary raw material, have increased production costs for manufacturers. These cost increases can reduce demand when transferred to consumers, particularly affecting price-sensitive small and medium-sized businesses. The trend of Italian companies outsourcing production to lower-cost regions impacts the local supply chain, extends delivery times, and reduces quality control capabilities. While outsourcing offers cost advantages, it can hinder innovation and sustainable practices implementation as companies focus on cost reduction rather than environmental initiatives. These combined factors create market growth constraints despite the growing demand for environmentally friendly packaging solutions.

Italy Paper Packaging Market Trends

Corrugated Boxes to Hold Significant Market Share

- The demand for corrugated boxes in Italy continues to grow, driven by e-commerce, logistics, and manufacturing sectors. The expansion of online shopping has increased the need for reliable and cost-effective packaging solutions for direct-to-consumer shipping. E-commerce companies require customizable packaging options, making corrugated boxes attractive for their protective qualities, cost efficiency, and branding potential.

- Italy's position as a significant global exporter influences the demand for corrugated packaging. Industries, including fashion, food, and automotive, depend on corrugated boxes for safe international product transportation. The country's export-focused economy necessitates packaging that meets international shipping standards. Corrugated boxes provide the durability and protection needed for long-distance transportation, ensuring product integrity during transit.

- Italy's export value reached USD 676.96 billion in 2023, increasing demand for corrugated boxes. The country's significant machinery, vehicles, food, and fashion exports require reliable packaging solutions for international shipping. Corrugated boxes provide the necessary protection for goods during transport while meeting environmental sustainability standards. The continuous expansion of Italy's export activities sustains the growth of the corrugated packaging market.

- Sustainability has become a significant factor in the packaging industry, with Italian businesses prioritizing eco-friendly options. Corrugated boxes, produced from recyclable and recycled paper, meet these environmental requirements. Implementing strict European Union recycling and waste regulations has increased demand for recyclable materials, including corrugated cardboard.

- The Italian food and beverage industry requires extensive corrugated packaging solutions. Italian food products, exported globally, need secure and protective packaging for transportation. Corrugated boxes are essential for packaging wine, olive oil, pasta, and other food items. The sector requires packaging solutions that maintain product freshness and safety during domestic and international shipping.

- The Italian corrugated box market is expected to maintain its growth trajectory, supported by e-commerce expansion, sustainability requirements, and the country's export activities. Packaging design developments, including weight reduction and strength improvements, are expected to increase the adoption of corrugated packaging across industries. The requirement for durable, high-quality packaging in exports will remain a fundamental market driver.

Beverages Segment Expected to Hold Significant Share in the Market

- The demand for paper in beverage packaging in Italy continues to rise, driven by increased focus on sustainability. As a major producer and exporter of beverages, including wine, spirits, and soft drinks, Italy requires packaging solutions that offer both protection and environmental benefits. Paper packaging has emerged as a preferred choice among beverage producers due to its biodegradable and recyclable properties, meeting both ecological requirements and consumer preferences.

- The Italian wine industry extensively uses paper packaging, mainly cartons and boxes, for safe bottle transportation during export. The demand for paper packaging in wine exports is projected to increase as producers transition to sustainable packaging solutions, influenced by consumer preferences and environmental compliance requirements.

- The non-carbonated beverage market in Italy is projected to reach 674.46 million USD in sales value and 495 million liters in volume by 2024, driving increased demand for paper packaging. The growth in consumption of juices, bottled water, and tea necessitates effective and sustainable packaging solutions. Paper packaging has emerged as a preferred choice for these beverages due to its biodegradable and recyclable properties, addressing the environmental concerns of both consumers and producers.

- The substantial market share of non-carbonated beverages in Italy's beverage industry has prompted manufacturers to adopt paper-based cartons and bottles. This transition aligns with European Union regulations to reduce plastic usage and promote sustainable packaging practices. Paper cartons and multi-layer paper packaging are increasingly utilized for juices, teas, and water products, meeting consumer preferences for eco-friendly solutions and regulatory requirements. The robust performance of the non-carbonated beverage segment continues to strengthen the position of paper as a primary packaging material in Italy's beverage industry.

- European Union regulations significantly influence paper-based packaging demand in Italy's beverage sector. The EU's stringent packaging waste guidelines require companies to use recyclable and reusable materials. This regulatory framework has prompted Italian beverage companies to implement paper packaging solutions to meet sustainability requirements and reduce plastic waste.

- Innovations in paper packaging technology have strengthened demand in Italy. Recent developments, including paper-based bottles and multi-layer paper cartons, enhance beverage protection while maintaining sustainability standards. These technological improvements increase the appeal of paper packaging for producers and consumers, positioning Italy's beverage industry within sustainable packaging trends.

Italy Paper Packaging Industry Overview

The Italy Paper Packaging Market is fragmented. It is a highly competitive market with several players. Companies operating in the country, such as DS Smith Plc, International Paper Company, Sappi Limited, Mondi Group, and Pro-Gest S.p.A., keep innovating, investing, and entering into strategic partnerships to retain their market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Consumer Awareness on Paper Packaging

- 5.1.2 Growth in E-commerce Sales

- 5.1.3 Rising Demand from the Foodservice Sector

- 5.1.4 Recycling Initiatives Involving Closed-loop Systems to Aid Market Adoption of Paper Packaging-based Materials

- 5.2 Market Restraints

- 5.2.1 Deforestation Concerns Due to Paper Packaging

- 5.2.2 Increasing Raw Material Costs and Outsourcing

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Folding Cartons

- 6.1.2 Corrugated Boxes

- 6.1.3 Other Product Types (Flexible Paper, Liquid Cartons, Etc.)

- 6.2 By End-User Industry

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Healthcare

- 6.2.4 Personal and Household Care

- 6.2.5 Electrical and Electronics Products

- 6.2.6 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 DS Smith Plc

- 7.1.2 International Paper Company

- 7.1.3 Sappi Limited

- 7.1.4 Smurfit Westrock

- 7.1.5 Mondi Group

- 7.1.6 Seda International Packaging Group

- 7.1.7 Tetra Pak International S.A.

- 7.1.8 Pro-Gest S.p.A.

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

撓性紙包裝市場規模、佔有率和成長分析(按材料、包裝類型、印刷技術、裝飾類型和地區)- 2025-2032 年行業預測

撓性紙包裝市場規模、佔有率和成長分析(按材料、包裝類型、印刷技術、裝飾類型和地區)- 2025-2032 年行業預測 紙板包裝市場規模、佔有率和成長分析(按材料類型、產品類型、厚度、最終用途和地區)- 產業預測 2025-2032

紙板包裝市場規模、佔有率和成長分析(按材料類型、產品類型、厚度、最終用途和地區)- 產業預測 2025-2032 2025-2033 年按產品類型、等級、包裝水平、最終用途行業和地區分類的紙包裝市場報告

2025-2033 年按產品類型、等級、包裝水平、最終用途行業和地區分類的紙包裝市場報告 中東和非洲的紙包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030)

中東和非洲的紙包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030) 亞太紙包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)

亞太紙包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030 年) 北美紙包裝:市場佔有率分析、行業趨勢、統計和成長預測(2025-2030)

北美紙包裝:市場佔有率分析、行業趨勢、統計和成長預測(2025-2030) 印尼紙包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

印尼紙包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 拉丁美洲紙包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

拉丁美洲紙包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 日本紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

日本紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 歐洲紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

歐洲紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)