|

市場調查報告書

商品編碼

1628805

北美影像感測器:市場佔有率分析、產業趨勢、成長預測(2025-2030)North America Image Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

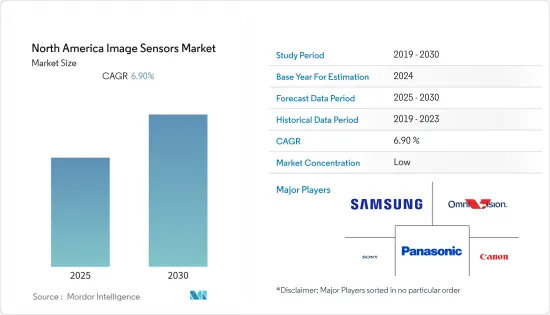

北美影像感測器市場預計在預測期內複合年成長率為 6.9%

主要亮點

- 由於智慧型手機、保全攝影機、高清攝影機、攝影機等的需求不斷增加,影像感測器市場預計在預測期內將出現高成長率。該地區的製造商正在努力提高解析度、性能和像素尺寸等關鍵參數。

- IC 技術的進步使得透過在同一晶片上整合感測器來整合先前獨立的功能成為可能。例如,標準行動電話具有獨立功能,例如相機、無線連接和音樂播放功能。如今,這些功能都可以在一台設備中實現,而且由於它們的普及,CMOS 和 CCD 等影像感測器的產量有所增加。

- 在消費性電子設備中,智慧型手機已成為主要的拍照設備,壓倒了靜態相機和數位單眼相機。智慧型手機領域的激烈競爭促使製造商提供更好的相機以保持競爭優勢,從而導致該領域對相機技術創新進行了大量投資。

- 此外,該地區的製造公司正在認知到機器視覺系統的優勢,特別是在需要準確執行檢查等冗餘任務的領域。工業4.0刺激了機器人等在工業自動化中發揮關鍵作用的技術的發展,工業中的許多核心業務都由機器人來管理。機器視覺支援視覺引導機器人等新應用。

- 此外,無人機在北美廣泛用於勘測,製造商一直在尋找能夠從高空捕捉影像的相機。具有較高百萬像素解析度和較小感測器尺寸的相機可能會受到影像衍射效應的影響。因此,這些缺點為市場上的影像感測器供應商提供了推出更大感測器的機會,這些感測器在相同解析度下表現出更好的聚光能力。

北美影像感測器市場趨勢

智慧型手機等中搭載的CMOS影像感測器顯著成長。

- 多個供應商正在開發 CMOS 影像感測器技術,並且擴大在低成本相機中採用。儘管通常與以相同價格提供卓越影像品質的電荷耦合元件 (CCD) 感測器進行比較,但 CMOS 感測器透過提供可簡化相機設計的晶片功能,在低成本終端佔據一席之地。

- 2022年3月,先進CMOS影像感測器供應商SmartSens推出首款50MP超高解析度1.0μm像素尺寸影像感測器產品SC550XS。此新產品採用先進的22奈米HKMG堆疊製程和SmartSens多項專有技術,包括SmartClarity-2技術、SFCPixel技術和PixGain HDR技術,提供卓越的成像性能。此外,AllPix ADAF技術提供100%全像素全向自動對焦覆蓋,並配備MIPI C-PHY 3.0Gsps高速資料傳輸介面。它還配備了MIPI C-PHY 3.0Gsps高速資料傳輸介面。該產品支援旗艦智慧型手機的關鍵相機需求:全彩夜視成像、高動態範圍和低功耗。

- 消費性電子、汽車、安全性和監控都是 CMOS 影像感測器不斷成長的市場。內建前置相機和後置鏡頭的智慧型手機的日益普及推動了消費性電子產業的崛起。

- 此外,自動駕駛汽車的創新以及透過 ADAS 提高駕駛安全性正在刺激車載應用的擴展。 CMOS影像感測器在低光源、黑暗和低照度等不同照明條件下運作,從而增加了CMOS影像感測器在安全應用中的使用,加強了安全性和監控CMOS影像感測器市場。

預計美國將佔據最大的市場佔有率

- 影像感測器是智慧型手機、平板電腦和穿戴式裝置等消費性電子產品的重要元件。現今消費性電子產品中內建的影像感測器採用 CCD 或 CMOS 技術。隨著此類設備在該國的普及,預計在預測期內對影像感測器的需求將會增加。

- 與專為工業或科學應用設計的 CCD 相比,許多專為家庭使用而開發的 CCD 影像感測器都具有內建的抗光暈功能。

- 此外,安森美半導體也宣布推出一款新型 5000 萬像素解析度 CCD 影像感測器。 KAI-50140是市售CCD影像感測器中解析度最高的行間傳輸CCD影像感測器,不僅適用於智慧型手機顯示器檢查,還適用於電路基板和機械組裝檢查,甚至還提供航空監控。細節和高影像均勻性。 KAI-50140 採用 2.18:1 的長寬比設計,以配合最新的智慧型手機格式,減少檢查整個顯示器所需的影像數量。

- 此外,過去幾年該地區的消費性電子產品銷售持續成長。包括智慧型手機和平板電腦在內的多種產品越來越注重增強這些產品的影像捕捉能力,導致購買各種家用電器的趨勢不斷增加,對市場產生了積極影響。

北美影像感測器產業概況

北美影像感測器市場較為分散,競爭公司之間競爭激烈。由於市場成長率較高,這是一個巨大的投資機會,並且新進入者正在不斷進入該市場。主要企業包括Canon、三星和SONY。

- 2022 年 1 月 - LUCID Vision Labs, Inc. 是一家獨特且創新的工業視覺相機設計商和製造商,宣布推出全新 Atlas SWIR IP67 標準 1.3MP 和 0.3MP 相機。 Atlas SWIR 是一款 GigE PoE+ 相機,配備寬頻和高靈敏度索尼 SenSWIR 1.3 MP IMX990 和 0.3 MP IMX991 InGaAs 感測器,能夠捕捉可見光和不可見頻譜中的影像,像素尺寸僅為 5μm,我們對此感到自豪。

- 2021 年5 月- 先進數位成像解決方案的領先開發商OMNIVISION Technologies, Inc. 在COMPUTEX Virtual 之前支援優質窄邊框筆記型電腦、平板電腦和物聯網設備的全高清(HD) 視訊性能,我們宣布了業界第一個 1 /7吋、200萬像素影像感測器OV02C。該感測器在最薄的 3mm 模組 Y 尺寸中以每秒 60 幀 (fps) 的速度提供出色的像素性能,適用於高螢幕佔比設計。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 買方議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

- 產業價值鏈分析

- COVID-19 市場影響評估

第5章市場動態

- 市場促進因素

- 汽車領域需求增加

- 降低電子設備中安裝 CMOS 影像感測器的成本

- 各種應用中手勢姿態辨識/控制的需求

- 市場限制因素

- 空間和電池消耗問題

- 製造成本高,市場競爭加劇

第6章 市場細分

- 按類型

- CMOS

- CCD

- 按最終用戶產業

- 家用電子產品

- 衛生保健

- 工業的

- 安全和監控

- 汽車/交通

- 航太/國防

- 其他最終用戶產業

- 國家名稱

- 美國

- 加拿大

第7章 競爭格局

- 公司簡介

- Canon Inc.

- Omnivision Technologies Inc.

- Panasonic Corporation

- Samsung Electronics Co. Ltd

- Sony Corporation

- STMicroelectronics NV

- Teledyne DALSA Inc.

- Aptina Imaging Corporation

- CMOSIS NV

- ON Semiconductor Corporation

- SK Hynix Inc.

第8章投資分析

第9章市場的未來

簡介目錄

Product Code: 54763

The North America Image Sensors Market is expected to register a CAGR of 6.9% during the forecast period.

Key Highlights

- Due to the growing demand for smartphones, security cameras, high-definition cameras, and camcorders, the image sensors market is expected to record a high growth rate during the forecast period. Manufacturers in the region have been striving to improve major parameters, such as resolution, performance, and pixel size.

- IC technology advancements have allowed the incorporation of previously independent functions by integrating sensors in the same chip. For example, a standard mobile phone has independent features, such as a camera, wireless connectivity, and music-playback capabilities. Now, all these functionalities are made available in a single device and have resulted in popularity, thus increasing the production volumes for image sensors, such as CMOS and CCD.

- In terms of consumer electronics, the smartphone has become the primary camera device, dominating still-cameras and DSLRs. Heavy competition in the smartphone segment has driven manufacturers to provide better cameras to have the edge over the competition, which has resulted in high investments in camera technology innovations in this field.

- Further, manufacturing firms in the region realize the benefits of machine vision systems, particularly in areas where redundant tasks, such as inspection, should be performed precisely. Industry 4.0 fueled the development of technologies, like robots playing a crucial role in industrial automation, with many core operations in industries managed by robots. Machine vision supports new applications, like vision-guided robotics, etc.

- Moreover, drones are widely used in North America to conduct surveys, and manufacturers are constantly looking for cameras that can capture images from altitudes. Cameras with higher megapixel resolution and small sensor sizes can be subject to image diffraction effects. Therefore, such disadvantages provide opportunities for the image sensor vendors in the market to introduce larger sensors that showcase better light-gathering ability at the same resolutions.

North America Image Sensors Market Trends

CMOS Image Sensor in Smartphone and Other Products to Witness Significant Growth

- CMOS image sensor technology, which several vendors are ramping, is sustaining its vigorous move into low-cost camera designs. Although often disparagingly compared to charge-coupled device (CCD) sensors with superior image quality at the same price, CMOS sensors are establishing a foothold at the low-cost end of the consumer market by offering more functions on-chip that simplify camera design.

- In March 2022, SmartSens, an advanced CMOS image sensor supplier, launched its first 50MP ultra-high-resolution 1.0μm pixel size image sensor product - SC550XS. The new product adopts the advanced 22nm HKMG Stack process and SmartSens' multiple proprietary technologies, including SmartClarity-2 technology, SFCPixel technology, and PixGain HDR technology, to enable excellent imaging performance. In addition, it can achieve 100% all pixel all-direction autofocus coverage via AllPix ADAF technology and is equipped with MIPI C-PHY 3.0Gsps high-speed data transmission interface. The product addresses the flagship smartphone's main camera requirements in night vision full-color imaging, high dynamic range, and low power consumption.

- Consumer electronics, automotive, security, and surveillance are all growing markets for CMOS image sensors. The rise of the consumer electronics sector has been spurred by the increasing popularity of smartphones with built-in front and rear cameras.

- Further, the expansion of the automotive application has been spurred by the innovation of self-driving automobiles and advancements in driver safety with the help of ADAS. The capacity of CMOS image sensors to work in various lighting conditions, including dim light, darkness, and low light, has raised the use of CMOS image sensors for security applications, bolstering the CMOS image sensor market for security and surveillance.

United States is Expected to Account for the Largest Market Share

- Image sensors are an integral part of consumer electronic products, such as smartphones, tablets, and wearables. The image sensors that are built in today's consumer electronic devices use either CCD or CMOS technology. With the growing adoption of such devices in the country, the demand for image sensors is expected to increase over the forecast period.

- Most CCD image sensors that have been developed for consumer applications possess the built-in anti-blooming capability, in contrast to most of the CCDs that have been specifically designed for industrial and scientific applications.

- Moreover, ON Semiconductor introduced a new 50-megapixel-resolution CCD image sensor. As the highest-resolution interline transfer CCD image sensor commercially available, the KAI-50140 provides the critical imaging detail and high image uniformity needed not only for the inspection of smartphone displays but also for circuit board and mechanical assembly inspection, as well as aerial surveillance. The KAI-50140 is designed in a 2.18-to-1 aspect ratio to match the format of modern smartphones, reducing the number of images captured to inspect a full display.

- Further, the region has also witnessed continuous consumer electronics sales growth over the past couple of years. The growing inclination towards purchasing various consumer electronics products is positively impacting the market as several products, including smartphones and tablets, are increasingly focusing on enhancing the image-capturing capabilities of these products.

North America Image Sensors Industry Overview

The North America Image Sensors Market is fragmented in nature due to intense competitive rivalry. Due to the high market growth rate, it is a significant investment opportunity, and therefore, new entrants are entering the market. Key players are Canon Inc., Samsung, Sony, etc.

- January 2022 - LUCID Vision Labs, Inc., a designer and manufacturer of unique and innovative industrial vision cameras, announced the launch of the new Atlas SWIR IP67-rated 1.3 MP and 0.3 MP cameras. The Atlas SWIR is a GigE PoE+ camera featuring wide-band and high-sensitivity Sony SenSWIR 1.3 MP IMX990 and 0.3 MP IMX991 InGaAs sensors, capable of capturing images across both visible and invisible light spectrums and boasting a miniaturized pixel size of 5μm.

- May 2021 - OMNIVISION Technologies, Inc., a significant developer of advanced digital imaging solutions, announced in advance of COMPUTEX Virtual the industry's first 1/7-inch, 2-megapixel image sensor, the OV02C, for full high definition (HD) video performance in thin bezel premium notebooks, tablets, and IoT devices. The sensor offers 60 frames per second (fps) and excellent pixel performance in the thinnest 3 mm module Y size for high screen-to-body ratio designs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID -19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand in Automotive Sector

- 5.1.2 Low-Cost Availability of CMOS Image Sensors Deployed in Electronic Devices

- 5.1.3 Demand for Gesture Recognition/Control in Various Applications

- 5.2 Market Restraints

- 5.2.1 Space and Battery Consumption issues

- 5.2.2 High Manufacturing Costs and Increased Market Competition

6 MARKET SEGMENTATION

- 6.1 Type

- 6.1.1 CMOS

- 6.1.2 CCD

- 6.2 End-User Industry

- 6.2.1 Consumer Electronics

- 6.2.2 Healthcare

- 6.2.3 Industrial

- 6.2.4 Security and Surveillance

- 6.2.5 Automotive and Transportation

- 6.2.6 Aerospace and Defense

- 6.2.7 Other End-user Industries

- 6.3 Country

- 6.3.1 United States

- 6.3.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Canon Inc.

- 7.1.2 Omnivision Technologies Inc.

- 7.1.3 Panasonic Corporation

- 7.1.4 Samsung Electronics Co. Ltd

- 7.1.5 Sony Corporation

- 7.1.6 STMicroelectronics N.V

- 7.1.7 Teledyne DALSA Inc.

- 7.1.8 Aptina Imaging Corporation

- 7.1.9 CMOSIS N.V.

- 7.1.10 ON Semiconductor Corporation

- 7.1.11 SK Hynix Inc.

8 INVESTMENTS ANALYSIS

9 FUTURE OF THE MARKET

02-2729-4219

+886-2-2729-4219

影像感測器市場:未來預測(2025-2030)

影像感測器市場:未來預測(2025-2030) 影像感測器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

影像感測器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 全球汽車監控雷達市場按組件、連接性、技術、車輛類型、應用和最終用戶分類 - 預測 2025-2030 年

全球汽車監控雷達市場按組件、連接性、技術、車輛類型、應用和最終用戶分類 - 預測 2025-2030 年 車載監控系統(ICMS)市場:技術、市場、機會與競爭(2025-2035年)

車載監控系統(ICMS)市場:技術、市場、機會與競爭(2025-2035年) 2025年全球農業影像感測器市場報告

2025年全球農業影像感測器市場報告 InGaAs 影像感測器市場報告:趨勢、預測和競爭分析(至 2031 年)

InGaAs 影像感測器市場報告:趨勢、預測和競爭分析(至 2031 年) 2030 年影像感測器市場預測:按處理類型、陣列類型、頻譜、解析度、技術、應用和地區進行分析

2030 年影像感測器市場預測:按處理類型、陣列類型、頻譜、解析度、技術、應用和地區進行分析 全球快門影像感測器市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)中東和非洲影像感測器:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030)安全應用影像感測器:全球市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

全球快門影像感測器市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)中東和非洲影像感測器:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030)安全應用影像感測器:全球市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

▼