|

市場調查報告書

商品編碼

1630362

資料中心現場太陽能發電-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)On-Site Photovoltaic Solar Power For Data Centers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

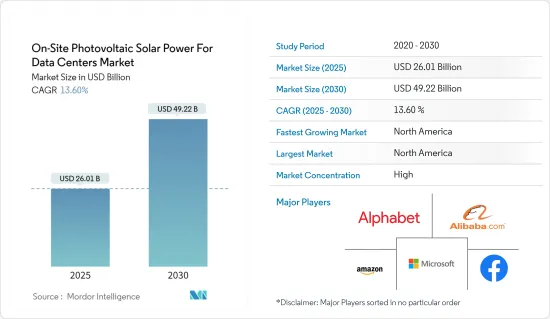

資料中心現場太陽能發電市場規模預計2025年為260.1億美元,2030年將達492.2億美元,預測期內(2025-2030年)複合年成長率為13.6%。

主要亮點

- 從中期來看,太陽能光電安裝成本的下降和對實施永續商業實踐的關注預計將推動資料中心的現場太陽能光電市場。

- 另一方面,小型資料中心缺乏安裝太陽能板的空間預計將阻礙預測期內資料中心現場太陽能發電市場的成長。

- 小型資料中心建築太陽能建築一體化技術的大規模商業化預計將成為預測期內資料中心現場太陽能光電市場的重大機會。

- 北美佔據市場主導地位,預計在預測期內仍將保持最高的複合年成長率。這一成長是由於政府加大了對安裝太陽能發電系統為該地區(包括美國和加拿大)資料中心供電的支持和投資的推動。

資料中心現場太陽能發電市場趨勢

安裝太陽能發電成本的下降正在推動市場

- 資料中心被定義為建築物的一部分、建築物本身或專用於容納電腦系統、儲存系統、通訊系統和所有其他相關組件的一組建築物。在資料中心,具有備用電源的不斷電系統對於資料擷取至關重要。

- 典型的資料中心消耗的電力從幾千瓦到數十兆瓦不等。對電力供應的高度依賴是資料中心營運成本較高的原因之一。

- 一些資料中心正在選擇太陽能等現場可再生能源,以降低營運成本並減少對環境的影響。隨著全球加權平均平準化能源成本 (LCOE) 從 2015 年的 0.129 美元/千瓦下降到 2022 年的約 0.049 美元/千瓦,多家營業單位正在採用太陽能光電發電。

- 此外,微軟計劃在 2025年終其資料中心將 100% 使用可再生能源運作。因此,隨著安裝成本下降,現場太陽能發電裝置預計將逐年成長。

- 因此,太陽能發電安裝成本的下降預計將在預測期內增加資料中心現場太陽能發電市場。

北美市場佔據主導地位

- 根據Cloudscene統計,截至2022年,美國是全球最大的資料中心市場之一,擁有近5,375個資料中心。此外,加拿大(335)在全球資料中心市場也佔有重要佔有率。

- 艾默生位於密蘇裡州的資料中心是美國領先的資料中心之一,採用校園太陽能技術為其資料中心供電。該中心安裝了一座 100 千瓦的太陽能電池板設施,耗資約 5,000 萬美元。加州的 Aiso.net 和亞利桑那州的 i/o 資料中心是少數擁有現場太陽能發電設施的資料中心。

- 資料中心營運商儲備的再生能源電量在一年內增加了 50%,該產業目前消耗了美國企業可用再生能源的三分之二。

- 2023 年 3 月,Meta 透露可再生能源部署每年以 30% 的速度成長。 Meta 已部署了 356 萬千瓦的太陽能發電容量,並在其長期開發平臺中擁有超過 900 萬千瓦的太陽能發電容量。 Meta 是美國最大的商業和工業太陽能採購商。

- 北美市場預計將成長,因為人們專注於透過使用可再生能源來滿足資料中心的能源需求,使計劃和營運更具永續性。

資料中心現場太陽能發電產業概述

資料中心的現場太陽能市場正在整合。該市場的主要企業(排名不分先後)包括亞馬遜公司、Alphabet公司、微軟公司、阿里巴巴集團控股有限公司、Facebook公司、戴爾技術公司、Affordable Internet Services Online Inc等。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 降低引入太陽能發電的成本

- 越來越關注永續商業實踐

- 抑制因素

- 小型資料中心缺乏太陽能板安裝空間

- 促進因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 北歐的

- 土耳其

- 俄羅斯

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 阿拉伯聯合大公國

- 卡達

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 埃及

- 北美洲

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Amazon.com, Inc.

- Alphabet Inc.

- Microsoft Corporation

- Alibaba Group Holding Ltd.

- Facebook Inc.

- Dell Technologies Inc.

- Affordable Internet Services Online Inc.

- Market Player Ranking

第7章 市場機會及未來趨勢

- 太陽能建築一體化技術規模化商業化

The On-Site Photovoltaic Solar Power For Data Centers Market size is estimated at USD 26.01 billion in 2025, and is expected to reach USD 49.22 billion by 2030, at a CAGR of 13.6% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the decreasing solar power installation costs and growing focus on implementing sustainable business practices are expected to drive the on-site photovoltaic solar power for data centers market.

- On the other hand, the lack of space for small data centers to install solar panels is expected to hinder on-site photovoltaic solar power for data centers market growth during the forecast period.

- Nevertheless, the large-scale commercialization of building-integrated photovoltaic technology into small data centers is expected to be a significant opportunity for the on-site photovoltaic solar power for data centers market duringthe forecast period

- North America is expected to dominate the market and likely witness the highest CAGR during the forecast period. This growth is attributed due to the increasing investments, coupled with supportive government policies for installing solar PV systems to power data centers in the region, including the United States of America (USA) and Canada.

On-Site Photovoltaic Solar Power For Data Centers Market Trends

Decrease in Solar Power Installation Cost is Likely to Drive the Market

- Data centers are defined as a part of a building, a building itself, or a cluster of buildings dedicated to housing computer systems, storage systems, telecommunication systems, and all other associated components. An uninterrupted power supply with backup power is the utmost importance in data centers for data capturing.

- A typical data center consumes power between a few kilowatts to several tens of megawatts. High dependency on the power supply is one of the high operating costs of the data center.

- Several data centers are opting for onsite renewable power sources like solar photovoltaic to reduce operating costs and have a less environmental impact. With decrease in Global Weighted Average Solar PV Levelized Cost of Energy (LCOE) from USD 0.129/kW in 2015 to nearly USD 0.049/kW in 2022 several entities have started adopting it.

- Moreover, Microsoft is planning to run 100% of its data center by renewable energy by the end of 2025. Thus, with a decrease in installation cost, onsite solar photovoltaic facilities are expected to grow over the years.

- Hence, deceresing solar power installation costs are expected to aid the growth of the on-site photovoltaic solar power for data centers market during the forecast period.

North America to Dominate the Market

- North America is one of the largest software and information technology markets globally, and according to Cloudscene, as of 2022, the United States was the largest data centre market in the world, housing nearly 5375 data centres. Additionally, Canada (335) also held signficant shares in the global datacentre market.

- Emerson data center in Missouri is one of the key data centers in the United States that is using solar photovoltaic technology on its campus to power its data center. The center has a 100-kilowatt solar panel facility, that was installed at the cost of around USD 50 million. Aiso.net in California, i/o Data Centers in Arizona are few other data centers that are facilitated with onsite photovoltaic solar power facilities.

- The amount of renewable power booked by data center operators increased by 50 percent in a year, and the sector now consumes two-thirds of the renewable power available to corporates in the United States.

- In March 2023, Meta revealed that its renewable energy deployments are growing by 30% each year. Meta has already deployed 3.56 GW of solar capacity, and has over 9 GW in its long-term development pipeline. Meta stands as the largest commercial and industrial purchaser of solar power in the United States.

- Hence, due to rising focus on increasing project and business sustainability by using renewable energy to power the energy needs of datacentres, the market is expected to witness a positive growth in North America.

On-Site Photovoltaic Solar Power For Data Centers Industry Overview

The on-site photovoltaic solar power for data centers market is consolidated. Some of the key players in this market (in no particular order) includes Amazon.com Inc, Alphabet Inc, Microsoft Corporation, Alibaba Group Holding Ltd, Facebook Inc, Dell Technologies Inc, and Affordable Internet Services Online Inc among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Decreasing Solar Power Installation Costs

- 4.5.1.2 Growing focus on Implementing Sustainable Business Practices

- 4.5.2 Restraints

- 4.5.2.1 Lack of Space for Small Data Centers to Install Solar Panels

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Geography

- 5.1.1 North America

- 5.1.1.1 United States

- 5.1.1.2 Canada

- 5.1.1.3 Rest of North America

- 5.1.2 Europe

- 5.1.2.1 Germany

- 5.1.2.2 France

- 5.1.2.3 United Kingdom

- 5.1.2.4 Italy

- 5.1.2.5 Spain

- 5.1.2.6 NORDIC

- 5.1.2.7 Turkey

- 5.1.2.8 Russia

- 5.1.2.9 Rest of Europe

- 5.1.3 Asia-Pacific

- 5.1.3.1 China

- 5.1.3.2 India

- 5.1.3.3 Japan

- 5.1.3.4 Australia

- 5.1.3.5 Malaysia

- 5.1.3.6 Thailand

- 5.1.3.7 Indonesia

- 5.1.3.8 Vietnam

- 5.1.3.9 Rest of Asia-Pacific

- 5.1.4 South America

- 5.1.4.1 Brazil

- 5.1.4.2 Argentina

- 5.1.4.3 Chile

- 5.1.4.4 Colombia

- 5.1.4.5 Rest of South America

- 5.1.5 Middle-East and Africa

- 5.1.5.1 United Arab Emirates

- 5.1.5.2 Qatar

- 5.1.5.3 Saudi Arabia

- 5.1.5.4 South Africa

- 5.1.5.5 Nigeria

- 5.1.5.6 Egypt

- 5.1.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Amazon.com, Inc.

- 6.3.2 Alphabet Inc.

- 6.3.3 Microsoft Corporation

- 6.3.4 Alibaba Group Holding Ltd.

- 6.3.5 Facebook Inc.

- 6.3.6 Dell Technologies Inc.

- 6.3.7 Affordable Internet Services Online Inc.

- 6.4 Market Player Ranking

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Large-scale Commercialization of Building-integrated Solar PV Technology

2025 年至 2033 年太陽能光電 (PV) 市場規模、佔有率、趨勢及預測(按類型、電網類型、部署、最終用戶和地區)

2025 年至 2033 年太陽能光電 (PV) 市場規模、佔有率、趨勢及預測(按類型、電網類型、部署、最終用戶和地區) 2025年全球光電市場報告

2025年全球光電市場報告 2025年全球太陽能發電面板製造市場報告

2025年全球太陽能發電面板製造市場報告 資料中心現場太陽能光電市場預測至 2030 年:按組件、資料中心類型、部署類型、技術、應用和地區進行的全球分析

資料中心現場太陽能光電市場預測至 2030 年:按組件、資料中心類型、部署類型、技術、應用和地區進行的全球分析 全球太陽能光電材料市場研究報告-產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球太陽能光電材料市場研究報告-產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 美國社區太陽能展望:2025 年上半年

美國社區太陽能展望:2025 年上半年 光伏材料市場規模、佔有率及成長分析(按組件、產品、材料、電池類型、安裝類型、應用和地區)- 2025-2032 年產業預測

光伏材料市場規模、佔有率及成長分析(按組件、產品、材料、電池類型、安裝類型、應用和地區)- 2025-2032 年產業預測 光伏 (PV) 市場:市場分析和預測至 2033 年 - 按類型、產品、服務、技術、組件、應用、材料類型、安裝類型、最終用戶、功能

光伏 (PV) 市場:市場分析和預測至 2033 年 - 按類型、產品、服務、技術、組件、應用、材料類型、安裝類型、最終用戶、功能 亞太光伏 (PV) -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

亞太光伏 (PV) -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 歐洲光伏 (PV) -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

歐洲光伏 (PV) -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)