|

市場調查報告書

商品編碼

1643209

歐洲光伏 (PV) -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Europe Solar Photovoltaic (PV) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

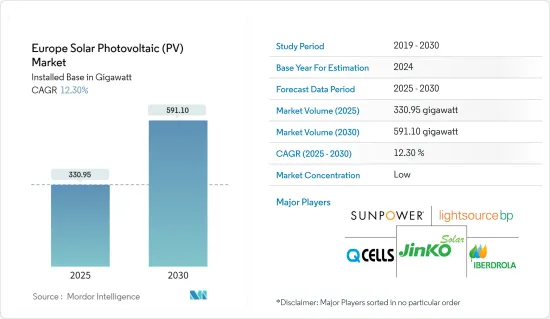

歐洲太陽能光電 (PV) 市場規模(安裝基數)預計將從 2025 年的 330.95 GW 成長到 2030 年的 591.10 GW,預測期內(2025-2030 年)的複合年成長率為 12.3%。

關鍵亮點

- 從中期來看,全部區域對電力的需求不斷成長、太陽能計劃投資不斷增加以及可再生能源發電正在推動市場成長。

- 另一方面,對天然氣發電的日益重視以及用於發電的天然氣的低可用性正在抑制歐洲市場的成長。

- 然而,為推動太陽能應用而實施的雄心勃勃的太陽能目標預計將在預測期內為市場創造有利可圖的機會。

- 德國擁有最大的裝置容量,預計在預測期內將主導歐洲太陽能光電 (PV) 市場。

歐洲光伏 (PV) 市場趨勢

屋頂市場預計將出現顯著的市場成長

- 預計預測期內歐洲屋頂市場將顯著成長。歐洲的屋頂安裝具有巨大的潛力,因為歐洲大多數屋頂都未被使用。歐洲多個國家正在修改其薪酬水準評估方法。

- 挪威、波羅的海地區和愛爾蘭等國家擁有安裝屋頂太陽能設施的有利地理條件。因此,預測期內歐洲屋頂太陽能光電安裝量預計會增加。此外,在一些國家,越來越多的住宅開始安裝屋頂光電模組以減少電費。根據國際可再生能源機構(IRENA)的預測,2023年歐洲太陽能發電裝置與前一年同期比較將達到285.80吉瓦,年增23.45%。

- 2023年12月,歐洲議會和理事會就加強建築物能源性能指令(EPBD)達成臨時協議,旨在促進建築物的能源性能,並強制要求新建建築具備光伏性能。 EPBD也要求歐盟成員國確保新建築適合安裝屋頂光電發電和熱能發電廠。自2027年起,現有公共建築和非住宅建築必須安裝太陽能發電系統。

- 一些政府已經採取了支持政策,以擴大該地區屋頂太陽能板的部署。例如,2023 年 3 月,歐洲各國政府通過了修訂後的《房屋能源性能指令》,要求到 2028 年所有新建建築都必須安裝屋頂太陽能發電系統,到 2032 年住宅重建都必須安裝屋頂太陽能發電系統。

- 2023年,德國太陽能光電裝置容量將達到創紀錄的14吉瓦,達到一個里程碑。根據德國光電協會(BSW)通報,與前一年相比,發電容量增加了 85%。容量的激增主要受到住宅需求的推動,尤其是屋頂太陽能光電系統。 BSW 注意到一個顯著的成長,2023 年第一季將有 159,000 個太陽能光電系統運作,是 2022 年同期的兩倍多。

- 鑑於上述情況,預計預測期內屋頂太陽能光電將在歐洲太陽能光電市場中見證顯著成長。

德國可望主導市場

- 德國是歐洲可再生能源生產(包括太陽能)最有利可圖的市場之一。由於國家製定了減少二氧化碳排放的目標,太陽能發電的安裝量大幅成長,預計未來這一趨勢仍將持續。

- 近年來,該國太陽能發電能力顯著成長。 2023年太陽能發電裝置容量約為81.73GW,而2022年為67.47GW,複合年成長率超過21%,顯示太陽能發電系統的滲透率正在提高。

- 該國已實施多項法規和激勵措施,鼓勵在都市區安裝太陽能板。 2023年6月,德國經濟部宣布政府將提供新的資金來重組該國的太陽能產業。經濟部將很快推出新的資金籌措工具,並將根據新的歐盟補貼框架準備未來的競標。

- 德國一些城市已強制要求新建建築配備太陽能發電系統,有助於擴大德國國內市場。 2022年12月,歐盟核准了德國280億歐元的可再生能源計畫。該舉措的目的是迅速擴大包括太陽能發電在內的自然能源的使用。這是德國到2030年實現80%電力來自可再生能源的目標的一部分。

- 因此,鑑於上述情況,預計德國太陽能將在預測期內主導歐洲太陽能市場。

歐洲光電產業概況

歐洲太陽能光電市場是分散的。市場的主要企業(不分先後順序)包括 Hanwha Q CELLS Technology、Iberdrola SA、SunPower Corporation、JinkoSolar Holding 和 Lightsource BP Renewable Energy Investments Limited。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究範圍

- 市場定義

- 調查前提

第2章調查方法

第3章執行摘要

第4章 市場概況

- 介紹

- 至2029年裝置容量及預測(單位:GW)

- 最新趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 全部區域的電力需求增加

- 增加對太陽能計劃的投資

- 限制因素

- 更加重視天然氣發電

- 驅動程式

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場區隔

- 類型

- 薄膜

- 矽晶型

- 最終用戶

- 住宅

- 商業和工業(包括中小企業)

- 擴張

- 地面安裝

- 屋頂安裝類型

- 2029 年市場規模與需求預測(按地區)

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 比利時

- 北歐的

- 土耳其

- 歐洲其他地區

第6章 競爭格局

- 併購、合資、合作與協議

- 主要企業策略

- 公司簡介

- First Solar Inc.

- Electricite de France SA(EDF)

- Hanwha Q CELLS Technology Co. Ltd

- Iberdrola SA

- JinkoSolar Holding Co. Ltd

- SunPower Corporation

- Lightsource bp Renewable Energy Investments Limited

- Enel SpA

- Centrotherm International AG

- 市場排名/佔有率(%)分析

第7章 市場機會與未來趨勢

- 雄心勃勃的太陽能目標

The Europe Solar Photovoltaic Market size in terms of installed base is expected to grow from 330.95 gigawatt in 2025 to 591.10 gigawatt by 2030, at a CAGR of 12.3% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as rising demand for electricity across the region, increasing investments in solar energy projects, and producing most of the electricity from renewable sources have driven the growth of the market.

- On the other hand, the rising emphasis on natural gas power generation and the availability of natural gas at lower prices for power generation restrain the market growth in the European region.

- However, the ambitious solar energy targets implemented to boost solar PV installation are expected to create lucrative opportunities for the market during the forecast period.

- Germany, with the largest installed capacity of solar photovoltaics, is expected to dominate the European solar photovoltaics (PV) market during the forecast period.

Europe Solar Photovoltaic (PV) Market Trends

The Rooftop Segment Anticipated to Witness Significant Market Growth

- The rooftop segment is estimated to witness significant growth during the forecast period in Europe. The European region's rooftop installation has lots of potential as most of Europe's roof surfaces are unused. Several countries in Europe are working on modifying their policies to assess remuneration levels.

- Norway, the Baltic region, Ireland, and others have geographical conditions favorable to rooftop PV installation. This is expected to increase rooftop solar PV installation in Europe during the forecast period. Also, in several countries, homeowners are willing to install rooftop PV modules to reduce their electricity bills. According to the International Renewable Energy Agency (IRENA), in 2023, Europe's solar PV installed reached 285.80 GW, with a growth rate of 23.45% over the previous year.

- In December 2023, the European Parliament and the European Council reached an interim agreement on the strengthened Energy Performance of Buildings Directive (EPBD), aspiring to stimulate the energy performance of buildings and requiring new buildings to be solar-ready. The EPBD also mandates that EU member states ensure new buildings are fit to host rooftop solar PV or thermal installations. Existing public and non-residential building solar will require to be installed commencing from 2027.

- Governments in several countries have adopted supportive policies to increase the deployment of rooftop PV arrays within the region. For instance, in March 2023, the European government adopted the revised Energy Performance of Business Directive mandating rooftop solar systems for all new buildings by 2028 and renovating residential buildings by 2032.

- In 2023, Germany achieved a milestone by installing a record 14GW of solar energy capacity, facilitated by adding over a million new solar power systems, a significant portion of which were residential rooftop installations. This surge reflects an impressive 85% increase in capacity compared to the previous year, as the German Solar Association (BSW) reported. The surge in capacity was primarily fueled by residential demand, particularly for rooftop solar power systems. The BSW noted a substantial increase, with 159,000 PV systems operational in the first quarter of 2023, more than double the number recorded during the same period in 2022.

- Therefore, from the above points, the rooftop solar photovoltaic segment is anticipated to witness significant growth in the European solar photovoltaic market during the forecast period.

Germany Expected to Dominate the Market

- Germany is one of the most lucrative markets in the European region for renewable energy production, including solar. The country has experienced significant developments in solar PV installation due to its target of reducing carbon emissions, and it is likely to continue witnessing growth in solar installation.

- The country's solar PV installed capacity has witnessed massive growth in recent years. In 2023, the installed solar PV was around 81.73 GW compared to 67.47 GW in 2022, registering a CAGR of over 21%, signifying the country's growing penetration of solar PV systems.

- The country has implemented several regulations and incentive schemes to promote the installation of solar modules in cities. In June 2023, Germany's economy ministry announced new government funding to rebuild the country's solar industry. The economy ministry is expected to present the new funding instrument soon and is preparing a tender in line with a new EU subsidy framework in the future.

- The mandates for solar photovoltaic installation on new buildings in a few German cities have helped expand the market in Germany. In December 2022, the European Union approved a EUR 28 billion German renewable energy scheme. The policy aims to increase the use of renewables, including solar power rapidly. It is designed to deliver Germany's target of producing 80% of its electricity from renewable sources by 2030.

- Therefore, based on the above points, solar photovoltaic in Germany will dominate the European solar photovoltaic market during the forecast period.

Europe Solar Photovoltaic (PV) Industry Overview

The European solar photovoltaic (PV) market is fragmented. Some of the major companies in the market (in no particular order) include Hanwha Q CELLS Technology Co. Ltd, Iberdrola SA, SunPower Corporation, JinkoSolar Holding Co. Ltd, and Lightsource BP Renewable Energy Investments Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definiton

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Installed Capacity and Forecast, in GW, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Demand for Electricity across the Region

- 4.5.1.2 Increasing Investments on Solar Energy Projects

- 4.5.2 Restraints

- 4.5.2.1 Rising Emphasis on Natural Gas Power Generation

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Thin Film

- 5.1.2 Crystalline Silicon

- 5.2 End User

- 5.2.1 Residential

- 5.2.2 Commercial and Industrial (including SMEs)

- 5.3 Deployment

- 5.3.1 Ground-Mounted

- 5.3.2 Rooftop Solar

- 5.4 Geography Regional Market Analysis {Market Size and Demand Forecast till 2029 (for regions only)}

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Netherlands

- 5.4.7 Belgium

- 5.4.8 Nordic

- 5.4.9 Turkey

- 5.4.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 First Solar Inc.

- 6.3.2 Electricite de France S.A. (EDF)

- 6.3.3 Hanwha Q CELLS Technology Co. Ltd

- 6.3.4 Iberdrola SA

- 6.3.5 JinkoSolar Holding Co. Ltd

- 6.3.6 SunPower Corporation

- 6.3.7 Lightsource bp Renewable Energy Investments Limited

- 6.3.8 Enel SpA

- 6.3.9 Centrotherm International AG

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Ambitious Solar Energy Targets

2025 年至 2033 年太陽能光電 (PV) 市場規模、佔有率、趨勢及預測(按類型、電網類型、部署、最終用戶和地區)

2025 年至 2033 年太陽能光電 (PV) 市場規模、佔有率、趨勢及預測(按類型、電網類型、部署、最終用戶和地區) 2025年全球光電市場報告

2025年全球光電市場報告 2025年全球太陽能發電面板製造市場報告

2025年全球太陽能發電面板製造市場報告 資料中心現場太陽能光電市場預測至 2030 年:按組件、資料中心類型、部署類型、技術、應用和地區進行的全球分析

資料中心現場太陽能光電市場預測至 2030 年:按組件、資料中心類型、部署類型、技術、應用和地區進行的全球分析 全球太陽能光電材料市場研究報告-產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球太陽能光電材料市場研究報告-產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 美國社區太陽能展望:2025 年上半年

美國社區太陽能展望:2025 年上半年 光伏材料市場規模、佔有率及成長分析(按組件、產品、材料、電池類型、安裝類型、應用和地區)- 2025-2032 年產業預測

光伏材料市場規模、佔有率及成長分析(按組件、產品、材料、電池類型、安裝類型、應用和地區)- 2025-2032 年產業預測 光伏 (PV) 市場:市場分析和預測至 2033 年 - 按類型、產品、服務、技術、組件、應用、材料類型、安裝類型、最終用戶、功能

光伏 (PV) 市場:市場分析和預測至 2033 年 - 按類型、產品、服務、技術、組件、應用、材料類型、安裝類型、最終用戶、功能 亞太光伏 (PV) -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

亞太光伏 (PV) -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 資料中心現場太陽能發電-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

資料中心現場太陽能發電-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)