|

市場調查報告書

商品編碼

1636250

歐洲貨櫃運輸:市場佔有率分析、產業趨勢、成長預測(2025-2030)Europe Container Drayage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

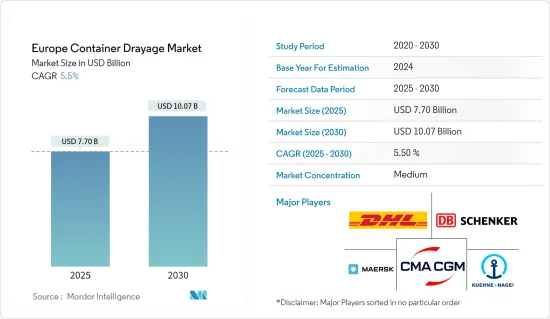

預計2025年歐洲貨櫃運輸市場規模為77億美元,預計2030年將達100.7億美元,預測期內(2025-2030年)複合年成長率為5.5%。

主要亮點

- 歐洲貨櫃運輸市場由貿易成長、基礎設施發展、技術進步和永續發展措施推動。

- 國際貿易量和通過歐洲港口的貨櫃貨物量的增加是貨櫃運輸市場的主要驅動力。歐洲正步入強勁復甦的軌道,預計2024年出口成長將成長2.2%,顯著高於2023年的0.4%。相應地,2023年下降的進口貿易量預計2024年將恢復1.6%。

- 利率上升、通膨飆升、烏克蘭曠日持久的衝突以及全球需求疲軟等挑戰將給 2023 年歐洲貿易量帶來壓力。然而,隨著利率預計在 2024 年放緩,經濟活動預計將復甦並刺激對歐洲出口的需求。

- 2023年,歐洲跨境電商市場激增,銷售額達2,370億歐元(2,565.4億美元),較2022年成長32%。歐洲線上零售商為跨境電子商務總額貢獻了 1,070 億歐元(1,158.2 億美元)。更廣泛的歐洲 B2C 電子商務市場也蓬勃發展,銷售額達到 7,410 億歐元(8,020.9 億美元),成長了 13%,令人印象深刻。目前,跨國交易佔歐洲線上銷售額的 32%。

- 基礎設施投資,特別是道路網路、港口和多式聯運設施,對於確保貨櫃運輸服務的無縫運作、從而推動市場向前發展至關重要。

歐洲貨櫃運輸市場趨勢

跨境電商帶動貨櫃需求

2023年,歐洲跨境電商市場呈現顯著成長,銷售額達2,370億歐元(2,565.4億美元),較2022年成長32%。歐洲線上零售商發揮了至關重要的作用,跨境電子商務總額達到1,070億歐元(1,158.2億美元)。更廣泛的歐洲 B2C 電子商務市場也蓬勃發展,銷售額達到 7,410 億歐元(8,020.9 億美元),強勁成長 13%。值得注意的是,跨境交易佔歐洲所有線上銷售額的 32%。

跨國銷售額成長 28%,達到 430 億歐元(465.4 億美元),其中德國線上零售商居首。相較之下,英國略有下降 1.8%,跨境銷售額為 275 億歐元(297.7 億美元),低於 2022 年的 280 億歐元(303.1 億美元)。

法國網路商店的跨境銷售額顯著成長 30%,達到 320 億歐元(346.4 億美元)。此外,西班牙平台成長了50%,達到180億歐元(194.8億美元),而荷蘭平台也出現了強勁成長,成長了45%,達到70億歐元(75.8億美元)。

2023年,服飾鞋類已成為歐洲跨境電商的主導產品類型。據透露,60%的受訪者強烈傾向於透過國際線上平台購買此類產品。相較之下,家用電子電器產品則位居第二,只有27%的受訪者更喜歡從海外採購。

義大利正成為貨櫃運輸服務中心

義大利港口在國家港口生態系統中擁有獨特的雙重功能。與許多國家一樣,港口主要促進進出口活動,但義大利港口因其作為南歐重要樞紐的角色而脫穎而出。

從地理上看,義大利半島不僅是歐洲與東馬格里布之間的橋樑,也是通往地中海心臟地帶的重要門戶。特別是蘇伊士運河出口至直布羅陀海峽之間的地中海主要海上航線靠近義大利海岸。

此外,義大利港口與匈牙利、奧地利和瑞士等中歐內陸國家建立了密切的聯繫。尤其是的里雅斯特,是通往奧地利和匈牙利的門戶。

義大利有20個港口,分佈在當地半島、撒丁島和西西里島。 2023年,主要港口管理總合運力為1,103萬個標箱,較2022年下降6.3%。然而,這個數字超過了 2020 年和 2021 年的運輸量。值得注意的是,這種下降反映了整個歐洲的趨勢,幾乎所有主要貨櫃港口在 2023 年都面臨挫折。

2023 年,義大利的貨櫃運輸量幾乎是法國的兩倍,吞吐量約為 500 萬標準箱。令人驚訝的是,儘管義大利的港口數量相似,但其表現卻優於法國。值得注意的是,焦亞陶羅、熱那亞和拉斯佩齊亞這三個義大利港口已加入專屬「百萬富翁俱樂部」。焦亞陶羅作為主要港口而蓬勃發展,而熱那亞和拉斯佩齊亞則主要充當通往內陸的重要紐帶。

Gioia Tauro 在 2023 年尤其表現出色,流量增加了 5%。港口當局將這一激增歸因於 MSC 在碼頭的大量存在。焦亞陶羅碼頭最初由康世集團開發,經歷了一系列變化,包括被馬士基收購,最終成為 MSC 集團的關鍵樞紐,此舉鞏固了這家瑞士公司在地中海的地位。

歐洲貨櫃運輸業概況

歐洲貨櫃運輸市場由幾家主要企業主導。我們擁有多元化的員工群體,從全球主要物流公司到區域公司和中小企業。著名的公司包括 DHL、DB Schenker 和 Kuehne+Nagel,以及 CMA CGM 和 Maersk Line 等業界巨頭。

歐洲貨櫃貨運市場的主要趨勢包括向數位化營運的轉變、對環保實踐的興趣日益濃厚、物聯網和遠端資訊處理的即時監控整合以及對多式聯運解決方案的日益偏好。這些趨勢正在大幅改變市場格局。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

- 分析方法

- 調查階段

第3章執行摘要

第4章市場動態與洞察

- 目前的市場狀況

- 市場動態

- 促進因素

- 國際貿易帶動市場成長

- 環境永續性的重要性日益增加正在推動市場發展

- 抑制因素

- 影響市場的監管因素

- 影響市場的基礎建設挑戰

- 機會

- 市場驅動的技術進步

- 促進因素

- 價值鏈/供應鏈分析

- 政府法規、貿易協定與舉措

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 地緣政治與 COVID-19 大流行對市場的影響

第5章市場區隔

- 透過交通工具

- 鐵路

- 路

- 其他交通工具

- 按國家/地區

- 德國

- 法國

- 英國

- 西班牙

- 歐洲其他地區

第6章 競爭狀況

- 市場集中度概覽

- 公司簡介

- DHL

- DB Schenker

- Kuehne+Nagel

- CMA CGM

- Maersk Line

- Hapag-Lloyd

- MSC(Mediterranean Shipping Company)

- COSCO Shipping

- Evergreen Marine

- Yang Ming*

- 其他公司

第7章 市場的未來

第8章附錄

- GDP 分佈(依活動、地區)

- 資本流動洞察

The Europe Container Drayage Market size is estimated at USD 7.70 billion in 2025, and is expected to reach USD 10.07 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

Key Highlights

- The European container drayage market is driven by trade growth, infrastructure development, technological advancements, and sustainable initiatives.

- The increasing volume of international trade and containerized cargo moving through European ports is a significant driver for the container drayage market. Europe is poised for a robust recovery, with export growth projected to surge by 2.2% in 2024, marking a significant uptick from the 0.4% growth in 2023. Correspondingly, after a dip in 2023, import trade volumes have been forecast to rebound by 1.6% in 2024.

- Challenges, including elevated interest rates, surging inflation, the prolonged conflict in Ukraine, and weakened global demand, weighed heavily on European trade volumes in 2023. However, with a projected easing of interest rates in 2024, economic activity is anticipated to rebound, spurring demand for European exports.

- In 2023, the European cross-border e-commerce market surged, hitting a turnover of EUR 237 billion (USD 256.54 billion), a remarkable 32% leap from 2022. European online retailers have been instrumental in contributing EUR 107 billion (USD 115.82 billion) to this cross-border total. The broader European B2C e-commerce market also flourished, culminating in a turnover of EUR 741 billion (USD 802.09 billion), up by a notable 13%. Cross-border transactions notably comprised 32% of all online sales in Europe.

- Investments in infrastructure, particularly in road networks, ports, and intermodal facilities, are pivotal for ensuring the seamless operation of container drayage services, thereby driving the market forward.

Europe Container Drayage Market Trends

Demand for Containers Driven by Cross-border E-commerce

In 2023, the European cross-border e-commerce market witnessed a significant surge, reaching a turnover of EUR 237 billion (USD 256.54 billion), marking a notable 32% leap over 2022. European online retailers played a pivotal role, contributing EUR 107 billion (USD 115.82 billion) to this cross-border total. The broader European B2C e-commerce market also thrived, achieving a turnover of EUR 741 billion (USD 802.09 billion), reflecting a substantial 13% increase. Notably, cross-border transactions accounted for 32% of all online sales in Europe.

German online retailers led the way, achieving a substantial 28% increase in cross-border sales, totaling EUR 43 billion (USD 46.54 billion). In contrast, the United Kingdom experienced a slight dip of 1.8%, with cross-border sales amounting to EUR 27.5 billion (USD 29.77 billion), down from EUR 28 billion (USD 30.31 billion) in 2022.

French online stores saw a notable 30% surge, reaching EUR 32 billion (USD 34.64 billion) in cross-border sales. Additionally, Spanish platforms witnessed a significant 50% rise, reaching EUR 18 billion (USD 19.48 billion), while Dutch platforms also experienced a substantial uptick, hitting EUR 7 billion (USD 7.58 billion), marking a 45% increase.

In 2023, clothing and footwear emerged as the dominant product category in European cross-border e-commerce. A significant 60% of respondents surveyed extensively revealed a strong preference for purchasing items from this category through international online platforms. In contrast, consumer electronics secured the second spot, with only 27% of respondents opting to procure these goods from overseas.

Italy Emerging as a Lucrative Hub for Container Drayage Services

Italian ports boast a unique dual function within the nation's port ecosystem. While, like in most countries, they primarily facilitate import and export activities, Italian ports distinguish themselves by assuming a pivotal role as key hubs in southern Europe.

Geographically, Italy's peninsula not only bridges Europe with the eastern Maghreb but also serves as a prominent gateway to the heart of the Mediterranean. Notably, the primary maritime route in the Mediterranean, linking the Suez Canal's exit with the Strait of Gibraltar, runs near Italy's coast.

Furthermore, Italian ports have cultivated strong ties with Central European landlocked nations like Hungary, Austria, and Switzerland. Among these connections, Trieste emerges as the premier port, serving as the gateway to Austria and Hungary.

Italy boasts 20 ports spread across its mainland peninsula and the islands of Sardinia and Sicily. In 2023, the primary ports collectively managed 11.03 million TEUs, marking a 6.3% dip over 2022. However, this figure still surpassed the volumes seen in both 2020 and 2021. Notably, this decline mirrors a broader European trend, with nearly all major container ports facing setbacks in 2023.

In 2023, Italy managed nearly double the container traffic of France, handling around 5 million TEUs. Surprisingly, despite having a similar number of ports, Italy outpaced France. Notably, three Italian ports - Gioia Tauro, Genoa, and La Spezia - joined the exclusive 'millionaire club.' While Gioia Tauro thrives as a primary hub, Genoa and La Spezia primarily serve as crucial links to the hinterland.

Gioia Tauro, in particular, shone in 2023, boasting a 5% growth in its traffic. The port's authority attributed this surge to the significant presence of MSC at the terminal. Originally developed by Contship, the terminal at Gioia Tauro saw a transition, with Maersk acquiring a stake before it eventually became a pivotal hub for the MSC group, a move that solidified the Swiss company's foothold in the Mediterranean.

Europe Container Drayage Industry Overview

The European container drayage market is dominated by some key players. It boasts a diverse mix, ranging from major global logistics firms to regional players and a host of small to medium-sized enterprises. Noteworthy names include DHL, DB Schenker, and Kuehne + Nagel, alongside industry behemoths like CMA CGM and Maersk Line.

Key trends in the European container drayage market encompass a shift toward digital operations, a growing focus on eco-friendly practices, the integration of IoT and telematics for real-time monitoring, and a rising preference for intermodal transportation solutions. These trends are significantly altering the market's landscape.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increasing International Trade Driving the Market

- 4.2.1.2 Increasing Importance of Environmental Sustainability Driving the Market

- 4.2.2 Restraints

- 4.2.2.1 Regulatory Factors Affecting the Market

- 4.2.2.2 Infrastructure Challenges Affecting the Market

- 4.2.3 Opportunities

- 4.2.3.1 Technological Advancements Driving the Market

- 4.2.1 Drivers

- 4.3 Value Chain/Supply Chain Analysis

- 4.4 Government Regulations, Trade Agreements, and Initiatives

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Impact of Geopolitics and the COVID-19 Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Mode of Transport

- 5.1.1 Rail

- 5.1.2 Road

- 5.1.3 Other Modes of Transport

- 5.2 By Country

- 5.2.1 Germany

- 5.2.2 France

- 5.2.3 United Kingdom

- 5.2.4 Spain

- 5.2.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 DHL

- 6.2.2 DB Schenker

- 6.2.3 Kuehne + Nagel

- 6.2.4 CMA CGM

- 6.2.5 Maersk Line

- 6.2.6 Hapag-Lloyd

- 6.2.7 MSC (Mediterranean Shipping Company)

- 6.2.8 COSCO Shipping

- 6.2.9 Evergreen Marine

- 6.2.10 Yang Ming*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 GDP Distribution, by Activity and Region

- 8.2 Insights into Capital Flows

歐洲冷藏貨櫃運輸:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

歐洲冷藏貨櫃運輸:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 2025-2033 年日本海運貨櫃市場報告(按產品、貨櫃尺寸(小型貨櫃、大型貨櫃、高立方貨櫃等)、應用和地區)

2025-2033 年日本海運貨櫃市場報告(按產品、貨櫃尺寸(小型貨櫃、大型貨櫃、高立方貨櫃等)、應用和地區) 負載約束裝置市場:按類型、材料和應用分類 - 2025-2030 年全球預測

負載約束裝置市場:按類型、材料和應用分類 - 2025-2030 年全球預測 海運貨櫃市場:按類型、尺寸、運輸方式、最終用途分類 - 2025-2030 年全球預測

海運貨櫃市場:按類型、尺寸、運輸方式、最終用途分類 - 2025-2030 年全球預測 2024-2032 年按產品、貨櫃尺寸(小型貨櫃、大型貨櫃、高立方貨櫃等)、應用和地區分類的海運貨櫃市場報告

2024-2032 年按產品、貨櫃尺寸(小型貨櫃、大型貨櫃、高立方貨櫃等)、應用和地區分類的海運貨櫃市場報告 冷凍和冷藏貨櫃運輸:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029)

冷凍和冷藏貨櫃運輸:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029) 貨櫃運輸:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)

貨櫃運輸:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029) 全球海運貨櫃市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測

全球海運貨櫃市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測 海運貨櫃市場 - 全球產業規模、佔有率、趨勢、機會和預測,按貨櫃大小、產品類型、運輸貨物、地區和競爭細分,2019-2029F

海運貨櫃市場 - 全球產業規模、佔有率、趨勢、機會和預測,按貨櫃大小、產品類型、運輸貨物、地區和競爭細分,2019-2029F 海運貨櫃市場:2024-2033 年全球產業分析、規模、佔有率、成長、趨勢、預測

海運貨櫃市場:2024-2033 年全球產業分析、規模、佔有率、成長、趨勢、預測