|

市場調查報告書

商品編碼

1636467

中國電動汽車電池製造:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)China Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

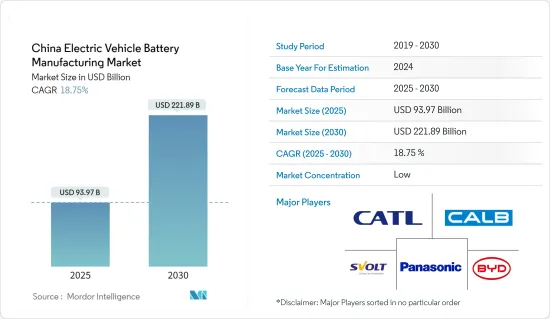

預計2025年中國電動車電池製造市場規模為939.7億美元,2030年將達2,218.9億美元,預測期間(2025-2030年)複合年成長率為18.75%。

主要亮點

- 從長遠來看,增加電池產能的投資和電池原料成本下降等因素預計將成為預測期內中國電動車電池製造市場的最大推動力之一。

- 另一方面,關鍵電池原料依賴進口,導致產業容易受到價格波動和發展不平衡的影響。這對預測期內的中國電動車電池製造市場構成威脅。

- 我們對電動車的長期雄心仍在繼續。預計這一因素將在未來為市場創造一些機會。

中國電動汽車電池製造市場趨勢

鋰離子電池類型主導市場

- 鋰離子電池以其高能量密度和長生命週期而聞名,已成為電動車製造商的首選。該技術不僅確保了高效的電動車生產,而且滿足了消費者的期望和行業基準。

- 為了普及電動車並加強國內電池生產,中國政府實施了一系列強力的措施。新能源汽車(NEV)指令等舉措以及補貼和稅收優惠正在刺激電動車產業的快速擴張。此外,「中國製造2025」舉措凸顯了中國鞏固其作為先進製造業全球領跑者地位的雄心。

- 中國減少碳排放和解決空氣污染的努力是電動車市場蓬勃發展的重要動力。支持清潔能源汽車的政策正在加速從內燃機轉向電動車的轉變。中國是全球最大的電動車市場,其需求快速成長是由都市化、環保意識增強和嚴格的汽車排放法規所推動的,所有這些都增加了對國產電池的需求。

- 2024年5月,中國將投資約60億元人民幣(8.45億美元)開發下一代電動車(EV)電池技術。全固態電池(ASSB)是傳統鋰離子電池(LIB)的前沿進步,利用固體導電電解質來提高安全性和能量密度。 CATL 是一家領先的電動車電池公司,它認知到了這一潛力,並準備好獲得政府對這項技術飛躍的支持。

- 中國大規模的充電基礎設施建設對於電動車在國內的普及至關重要。這項策略性投資將確保電動車用戶輕鬆獲得高效的充電解決方案,進一步增加對電動車電池的需求。同時,中國企業正投入資源進行研發,旨在提高電池技術並降低生產成本。與國際高科技公司和研究機構的合作是電池製造創新的催化劑。

- 例如,2024年5月,國營上汽集團宣布計畫在2025年將固態電池整合到其電動車品牌中,並於2026年實現量產。此電池能量密度超過400Wh/kg,續航里程至少1000公里。去年6月,國內電動車製造商蔚來成功測試了固態電池,取得了360Wh/kg能量密度和1044公里續航里程的驚人紀錄。此外,上汽集團部分控股的 IM Motors 於 4 月推出了 IM L6 EV 車型。該車型搭載超快充固態電池,電量為130kWh,支援1000公里續航里程和900V超快充電能力。

- 中國的製造能力接近900吉瓦時,佔全球整體的77%。此外,全球十大電池製造商中有六家在中國。中國對從金屬開採到汽車生產的整個電動車供應鏈的全面控制進一步強化了這一優勢。全球超過一半的電動車持有在中國,中國的鋰離子電池製造能力在2023年達到1,705GWh,預計2027年將激增至6,197GWh。

- 鑑於這一發展和投資,隨著對鋰離子電池的需求不斷成長,預計未來幾年全部區域的電動車電池產量將激增。

投資加強電池產能

- 中國正在策略性地提高電池產能,以滿足快速成長的電動車(EV)需求。補貼和投資誘因等政府措施正在刺激國內企業提高產能。此次合作旨在鞏固中國作為電動車電池製造領域全球領導者的地位,並確保為不斷擴大的電動車市場穩定供應優質電池。

- 中國各地正在建立新的電池生產工廠,推動電動車電池製造市場的發展。 CATL和比亞迪等工業巨頭正在安裝最先進的設備來擴大生產。這些最先進的工廠配備了先進技術,並有望提高產量和效率,成為滿足快速成長的國內外電動車電池需求的關鍵要素。

- 漿料攪拌機浮動競標對於改進電池生產流程起著至關重要的作用。這些攪拌機保證了電池材料配方的均勻性,直接影響鋰離子電池的品質和性能。透過對如此重要的攪拌機進行競標,中國不僅增強了其電池製造技術,而且提高了整個電動車電池市場的成長和效率,支持了該行業的快速擴張。

- 例如,2024年6月,中國電池製造商國軒高科發布了一款革命性的電動車電池,可在10分鐘內完成充電,使其成為全球領先企業寧德時代的有力競爭對手。這種快速充電創新直接解決了消費者對充電時間的擔憂。 Gothion已開始大量生產遠距混合動力汽車的G-Current電池。同時,一條電動車電池生產線也在興建中,計畫年內開始量產。

- 中國政府仍堅定支持電動車產業,推出稅收優惠、對製造商和消費者的補貼以及加強充電基礎設施等措施。這些舉措旨在提高電動車的可負擔性和便利性,提高採用率,進而擴大對電池材料的需求。電池技術的創新也正在改變電動車的格局。例如,比亞迪正在開創磷酸鋰鐵(LFP)電池等新化學電池,其能量密度比傳統鋰離子電池略低,但更安全、更經濟。這些突破對於電動車在市場上的廣泛採用至關重要。

- 展望未來,中國電動車電池製造市場可望走上看漲軌道。憑藉著堅定不移的政府支持、技術進步和戰略產業合作,中國將保持在全球電動車領域的主導地位。主要電池製造商產能的不斷擴張,加上對永續實踐的關注,導致對關鍵材料的穩定需求,推動了電動車電池製造業的快速崛起。

- 中國鋰離子電池產能已達到驚人的1.2兆瓦時(TWh),佔全球76%的佔有率。隨著全球一半以上的電動車在中國道路上行駛,預計到 2030 年產能將激增至 4.65TWh。

- 這種投資和生產擴張預計將放大對鋰離子電池產能的需求。

中國電動汽車電池製造業概況

中國電動車電池製造市場已被削減一半。市場的主要企業(排名不分先後)包括比亞迪、寧德時代新能源科技有限公司、松下電器產業株式會社、中航鋰電、蜂巢能源科技。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 投資增加電池產能

- 電池原物料成本下降

- 抑制因素

- 主要電池材料依賴進口

- 促進因素

- 供應鏈分析

- PESTLE分析

- 投資分析

第5章市場區隔

- 電池

- 鋰離子

- 鉛酸

- 鎳氫電池

- 其他

- 電池形式

- 方形

- 袋型

- 圓柱形

- 車輛

- 客車

- 商用車

- 其他

- 晉升

- 電池電動車

- 油電混合車

- 插電式混合動力電動車

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- BYD Co. Ltd

- Contemporary Amperex Technology Co. Limited

- EnerSys

- GS Yuasa Corporation

- LG Chem Ltd

- Exide Industries

- Panasonic Corporation

- CALB(China Aviation Lithium Battery)

- SVOLT Energy Technology

- EVE Energy

- 其他知名公司名單

- 市場排名分析

第7章 市場機會及未來趨勢

- 電動車的長期目標

簡介目錄

Product Code: 50003734

The China Electric Vehicle Battery Manufacturing Market size is estimated at USD 93.97 billion in 2025, and is expected to reach USD 221.89 billion by 2030, at a CAGR of 18.75% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors such as investments to enhance the battery production capacity and a decline in the cost of battery raw materials are expected to be among the most significant drivers for the China Electric Vehicle Battery Manufacturing Market during the forecast period.

- On the other hand, import dependency for key battery materials leaves the industry vulnerable to price fluctuations and imbalanced development. This poses a threat to the China Electric Vehicle Battery Manufacturing Market during the forecast period.

- Nevertheless, continued Long-term ambitious targets for electric vehicles. This factor is expected to create several opportunities for the market in the future.

China Electric Vehicle Battery Manufacturing Market Trends

Lithium-ion Battery Type to Dominate the Market

- Li-ion batteries, known for their high energy density and long life cycles, have become the go-to choice for EV manufacturers. This technology not only ensures the production of efficient electric vehicles but also meets both consumer expectations and industry benchmarks.

- To bolster EV adoption and domestic battery production, the Chinese government has rolled out a series of robust policies. Initiatives like the New Energy Vehicle (NEV) mandate, alongside subsidies and tax incentives, are fueling the rapid expansion of the EV sector. Furthermore, the "Made in China 2025" initiative underscores China's ambition to cement its status as a global frontrunner in advanced manufacturing.

- China's drive to cut carbon emissions and tackle air pollution is a pivotal force behind its booming EV market. With policies championing clean energy vehicles, the nation is witnessing a swift transition from internal combustion engines to electric mobility. As the globe's largest EV market, China's surging demand is propelled by urbanization, heightened environmental consciousness, and stringent vehicle emission regulations, all of which amplify the need for domestically produced batteries.

- In May 2024, China is set to channel approximately CNY 6 billion (USD 845 million) into pioneering next-generation battery technologies for electric vehicles (EVs). All Solid State Batteries (ASSBs), a cutting-edge advancement over traditional lithium-ion batteries (LIBs), utilize a solid conductive electrolyte, enhancing safety and energy density. Recognizing their potential, EV battery titan CATL is poised to receive government backing for this technological leap.

- China's expansive charging infrastructure development is pivotal for the country's electric vehicle adoption. This strategic investment guarantees EV users easy access to efficient charging solutions, further amplifying the demand for EV batteries. Concurrently, Chinese firms are pouring resources into R&D, aiming to refine battery technologies and curtail production costs. Collaborations with international tech giants and research entities are catalyzing innovations in battery manufacturing.

- For example, in May 2024, state-owned SAIC announced plans to integrate full solid-state batteries into its EV brands by 2025, with mass production slated for 2026. Boasting an energy density exceeding 400Wh/kg, this battery promises a driving range of at least 1,000km. Last June, domestic EV maker Nio successfully tested a solid-state battery achieving a 360Wh/kg energy density and a remarkable 1,044km range. Additionally, IM Motors, partially owned by SAIC, revealed in April its IM L6 EV model, featuring an ultra-fast charging solid-state battery with 130kWh power, supporting a 1,000km range and 900V ultra-fast charging capability.

- China dominates the global battery landscape, boasting a manufacturing capacity nearing 900 gigawatt-hours, which translates to a commanding 77% share of the worldwide total. Furthermore, six of the top ten battery manufacturers globally hail from China. This dominance is further reinforced by China's holistic control over the entire EV supply chain, from metal mining to vehicle production. With more than half of the world's electric vehicle fleet residing in China, the nation's lithium-ion battery cell manufacturing capacity, recorded at 1705 GWh in 2023, is projected to skyrocket to 6197 GWh by 2027.

- Given these developments and investments, a surge in EV battery production across the region is anticipated, alongside a growing demand for lithium-ion batteries in the coming years.

Investments to Enhance the Battery Production Capacity

- China is strategically ramping up its battery manufacturing capacity to cater to the surging demand for electric vehicles (EVs). Government initiatives, including subsidies and investment incentives, are spurring domestic companies to bolster their production capabilities. This concerted effort seeks to cement China's status as a global frontrunner in EV battery manufacturing, guaranteeing a consistent supply of premium batteries for the expanding EV market.

- The establishment of new battery production plants throughout China is propelling the EV battery manufacturing market. Industry giants like CATL and BYD are rolling out cutting-edge facilities to amplify their production. These state-of-the-art plants, outfitted with advanced technologies, promise heightened output and efficiency-key factors in satisfying the surging domestic and international appetite for EV batteries.

- Floating tenders for slurry mixers play a pivotal role in refining the battery production process. These mixers ensure uniformity in battery material blending, directly influencing the quality and performance of lithium-ion batteries. By soliciting tenders for these crucial mixers, China is not only enhancing its battery manufacturing technology but also bolstering the overall growth and efficiency of the EV battery market, fueling the industry's swift expansion.

- For example, in June 2024, Gotion High-tech, a Chinese battery cell manufacturer, unveiled a groundbreaking electric vehicle battery capable of charging in under 10 minutes, positioning it as a formidable competitor to global leader CATL. This swift-charging innovation directly addresses consumer concerns about charging durations. Gotion has commenced mass production of its G-Current batteries, tailored for extended-range hybrids. Meanwhile, production lines for all-electric vehicle batteries are under construction, with mass production slated to kick off by year's end.

- China's government remains steadfast in its support for the EV sector, rolling out measures like tax incentives, subsidies for manufacturers and consumers, and bolstering charging infrastructure. Such initiatives aim to enhance the affordability and convenience of EVs, driving up adoption rates and, in turn, amplifying the demand for battery materials. Battery technology innovations are also reshaping the landscape. For instance, BYD is pioneering new chemistries like lithium iron phosphate (LFP) batteries-safer and more economical, albeit with a marginally lower energy density than conventional lithium-ion counterparts. These breakthroughs are pivotal in making EVs more accessible to the broader market.

- Looking ahead, China's EV battery manufacturing market is poised for a bullish trajectory. With unwavering government backing, technological strides, and strategic industry collaborations, China is set to uphold its dominance in the global EV arena. The relentless expansion of production capacities by leading battery manufacturers, coupled with a focus on sustainable practices, bodes well for a consistent demand for essential materials, propelling the swift ascent of the EV battery manufacturing sector.

- China's lithium-ion battery manufacturing capacity stands at a staggering 1.2 terawatt hours (TWh), commanding a robust 76 percent share of the global landscape. With more than half of the world's electric vehicles gracing Chinese roads, projections indicate this capacity will surge to 4.65 TWh by 2030.

- Such investments and production expansions are set to amplify the demand for lithium-ion battery capacity.

China Electric Vehicle Battery Manufacturing Industry Overview

The China Electric Vehicle Battery Manufacturing Market is semi-fragmented. Some of the key players in this market (in no particular order) are BYD Co. Ltd., Contemporary Amperex Technology Co. Limited, Panasonic Corporation, CALB (China Aviation Lithium Battery), and SVOLT Energy Technology.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Investments to Enhance the battery production capacity

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 Import Dependency for Key Battery Material

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Nickel Metal Hydride Battery

- 5.1.4 Others

- 5.2 Battery Form

- 5.2.1 Prismatic

- 5.2.2 Pouch

- 5.2.3 Cylindrical

- 5.3 Vehicle

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.3.3 Others

- 5.4 Propulsion

- 5.4.1 Battery Electric Vehicle

- 5.4.2 Hybrid Electric Vehicle

- 5.4.3 Plug-in Hybrid Electric Vehicle

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd

- 6.3.2 Contemporary Amperex Technology Co. Limited

- 6.3.3 EnerSys

- 6.3.4 GS Yuasa Corporation

- 6.3.5 LG Chem Ltd

- 6.3.6 Exide Industries

- 6.3.7 Panasonic Corporation

- 6.3.8 CALB (China Aviation Lithium Battery)

- 6.3.9 SVOLT Energy Technology

- 6.3.10 EVE Energy

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Long-term ambitious targets for electric vehicles

02-2729-4219

+886-2-2729-4219

2025 年電池製造設備全球市場報告

2025 年電池製造設備全球市場報告 電池製造設備市場規模、佔有率、成長分析,按產品、按電池類型、按設備類型、按應用、按地區 - 行業預測,2025 年至 2032 年2025 年全球電池製造機市場報告

電池製造設備市場規模、佔有率、成長分析,按產品、按電池類型、按設備類型、按應用、按地區 - 行業預測,2025 年至 2032 年2025 年全球電池製造機市場報告 全球電池製造機械市場(至 2029 年):按電極層壓機、壓延機、分切機、攪拌機、塗佈和乾燥機、組裝機、成型和測試機以及鋰離子電池(NMC、LFP、NCA、LCO、LMO、LTO)

全球電池製造機械市場(至 2029 年):按電極層壓機、壓延機、分切機、攪拌機、塗佈和乾燥機、組裝機、成型和測試機以及鋰離子電池(NMC、LFP、NCA、LCO、LMO、LTO) 電池製造中的泵浦和閥門 2023-2027

電池製造中的泵浦和閥門 2023-2027 中國電動汽車電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中國電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中東和非洲電動車電池製造設備:市場佔有率分析、產業趨勢和成長預測(2025-2030)中東和非洲電動車電池製造:市場佔有率分析、產業趨勢和成長預測(2025-2030)亞太地區電動汽車電池製造設備:市場佔有率分析、產業趨勢與成長預測(2025-2030)

中國電動汽車電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中國電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)中東和非洲電動車電池製造設備:市場佔有率分析、產業趨勢和成長預測(2025-2030)中東和非洲電動車電池製造:市場佔有率分析、產業趨勢和成長預測(2025-2030)亞太地區電動汽車電池製造設備:市場佔有率分析、產業趨勢與成長預測(2025-2030)

▼