|

市場調查報告書

商品編碼

1636523

中國混合動力汽車電池市場:佔有率分析、產業趨勢/統計、成長預測(2025-2030)China Hybrid Electric Vehicle Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

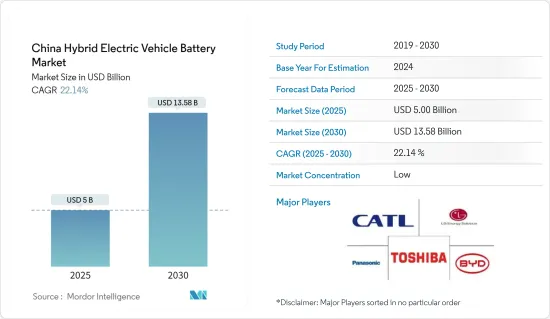

預計2025年中國混合動力汽車電池市場規模將達50億美元,2030年將達135.8億美元,預測期間(2025-2030年)複合年成長率為22.14%。

主要亮點

- 從中期來看,電動車(EV)普及率的提高和鋰離子電池價格的下降預計將在預測期內推動混合動力電動車電池的需求。

- 另一方面,電池電動車和插電式混合動力電動車等替代技術的出現預計將阻礙電池市場的發展。

- 電池材料的技術進步,例如提高能量密度、縮短充電時間、提高安全性和延長使用壽命,預計將在不久的將來為混合動力電動車電池市場的參與企業提供重大機會。

中國混合動力汽車電池市場趨勢

鋰離子電池類型主導市場

- 中國鋰離子混合動力汽車電池市場是一個充滿活力的市場,機會與挑戰並存。由於其良好的容量重量比,鋰離子混合動力電動車電池比其他電池技術更受歡迎。優越的性能(特別是長壽命和低維護)、長壽命和較低的價格等優點進一步推動了鋰離子電池的採用。

- 鋰離子電池歷來比同類產品昂貴,但市場領導者正在加大投資。對實現規模經濟和加強研發力度的關注加劇了競爭並壓低了鋰離子電池的價格。

- 2023年,電池價格將大幅下降,穩定在139美元/kWh。隨著技術創新和製造流程的持續改進,預計電價將進一步下降,目標是 2025 年達到 113 美元/千瓦時,2030 年達到 80 美元/度。

- 此外,電池技術在能量密度、充電速度和壽命方面的不斷進步正在推動鋰離子電池在全國混合動力電動車中的採用。中國正在大力投資先進電池技術,旨在延長電池壽命並成為混合動力電動車的冠軍。

- 例如,2024 年 5 月,中國累計60 億元人民幣(8.45 億美元)的巨額預算來開拓下一代電池技術,重點是電動和混合動力汽車。固態電池(ASSB)是傳統鋰離子電池的演變,具有更高的安全性(降低火災和爆炸的風險)和卓越的能量密度。此類創新將增強對先進鋰離子電池的需求,並刺激對混合動力電動車的需求。

- 此外,鋰離子電池價格暴跌、需求激增以及中國各地新生產設施的建立相互動態,正在重塑能源和汽車格局。

- 到 2023 年,中國企業將擴大整合其供應鏈,以確保從鋰和鈷等原料的提取到最終電池生產的持續供應和成本效率。這種趨勢可能會在未來幾年發展。

- 在這些發展的支持下,混合動力電動車的產量預計將在預測期內激增,對鋰離子電池的需求預計也將相應增加。

乘用車板塊實現大幅成長

- 由於消費者對環境問題的認知不斷提高以及對省油車的需求不斷增加,乘用混合動力汽車市場正在經歷強勁成長。與傳統汽油動力汽車相比,混合動力汽車結合了內燃機和馬達,具有卓越的燃油效率並減少了排放氣體。

- 此外,隨著電動車(EV)的採用迅速增加,對混合動力電動車(HEV)(包括乘用車)的需求也在增加。例如,根據國際能源總署(IEA)的報告,2023年國內電動車銷量將達到約810萬輛,較2022年成長37.2%。隨著政府推出多項舉措來促進混合動力汽車的銷售和需求,未來幾年的銷售量將會增加。

- 中國正透過多項政府措施促進混合動力電動車(HEV)的採用,包括乘用車。這些措施符合應對空氣污染和減少對石化燃料依賴的更大挑戰。

- 例如,2023 年,政府推出了一項報廢計劃,獎勵駕駛員用電動或插電式混合動力汽車更換老化的內燃機汽車 (ICE)。該計劃為購買新電動車或插電式混合動力汽車提供最高 10,000 元人民幣(約 1,375 美元)的財務支持。預計這些發展將在預測期內增加該地區對混合動力乘用車的需求,從而增加對混合動力汽車電池的需求。

- 此外,中國政府積極支持混合動力汽車和電動車的電池技術、電力傳動系統以及其他關鍵零件的研發。透過與研究機構合作並激勵私人公司,政府旨在快速實現技術突破。

- 例如,2024年6月,中國工業和資訊化部宣布了鋰離子電池產業的新指南。該指南旨在提高行業地位,以應對汽車,特別是混合動力電動車的快速成長。這些積極措施預計將在不久的將來加強混合動力乘用車市場並增加對混合動力電池的需求。

- 此類計劃的進展凸顯了乘用車混合動力電池解決方案的可行性和重要性,並表明明年全國對混合動力電池的需求將激增。

中國混合動力汽車電池產業概況

中國混合動力汽車電池市場處於半瓜分狀態。主要企業(排名不分先後)包括LG能源解決方案有限公司、東芝公司、松下控股公司、比亞迪公司、寧德時代新能源科技有限公司。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 電動車 (EV) 產量增加

- 鋰離子電池價格下降

- 抑制因素

- 替代電動車技術的可能性

- 促進因素

- 供應鏈分析

- PESTLE分析

- 投資分析

第5章市場區隔

- 電池類型

- 鋰離子電池

- 鉛酸電池

- 鈉離子電池

- 其他

- 車型

- 客車

- 商用車

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- BYD Company Ltd

- Contemporary Amperex Technology Co. Limited

- LG Energy Solution Ltd

- Panasonic Holdings Corporation

- Toshiba Corporation

- Duracell Inc.

- Okaya Power Group

- Guoxuan High-Tech Co., Ltd

- Clarios

- EVE Energy Co., Ltd.

- 其他知名公司名單

- 市場排名/佔有率分析

第7章 市場機會及未來趨勢

- 電池材料技術進步

簡介目錄

Product Code: 50003892

The China Hybrid Electric Vehicle Battery Market size is estimated at USD 5.00 billion in 2025, and is expected to reach USD 13.58 billion by 2030, at a CAGR of 22.14% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, rising adoption of electric vehicles (EV) and declining lithium-ion battery prices are expected to drive the demand for hybrid electric vehicle batteries during the forecast period.

- On the other hand, the availability of alternate technology like battery electric vehicles and plug-in hybrid electric vehicles are likely to hinder the battery market.

- Nevertheless, technological advancements in battery materials like higher energy density, faster charging times, improved safety, and longer lifespan are expected to create significant opportunities for hybrid electric vehicle battery market players in the near future.

China Hybrid Electric Vehicle Battery Market Trends

Lithium-Ion Battery Type Dominate the Market

- China's lithium-ion hybrid electric vehicle battery market is a dynamic arena, teeming with both opportunities and challenges. Lithium-ion hybrid EV batteries are outpacing other battery technologies in popularity, thanks to their favorable capacity-to-weight ratio. Their adoption is further fueled by advantages like superior performance (notably long life and low maintenance), an extended shelf life, and declining prices.

- While lithium-ion batteries traditionally commanded a premium over their counterparts, leading market players have been ramping up investments. Their focus on achieving economies of scale and bolstering R&D efforts has intensified competition, subsequently driving down lithium-ion battery prices.

- In 2023, battery prices saw a notable dip, settling at USD 139/kWh-a drop exceeding 13%. With ongoing technological innovations and manufacturing refinements, projections suggest a further decline: targeting USD 113/kWh by 2025 and an ambitious USD 80/kWh by 2030.

- Moreover, relentless advancements in battery technology-spanning energy density, charging speed, and lifespan-are propelling the adoption of lithium-ion batteries in hybrid EVs nationwide. China is heavily investing in battery tech advancements, aiming to prolong battery life and champion hybrid EVs.

- For example, in May 2024, China earmarked a substantial 6 billion yuan (USD 845 million) for pioneering next-gen battery tech, with a spotlight on electric and hybrid vehicles. Solid-state batteries (ASSBs), an evolution of traditional lithium-ion batteries, boast enhanced safety (lower fire/explosion risk) and superior energy density. Such innovations are poised to bolster the demand for advanced lithium-ion batteries, subsequently fueling hybrid EV demand.

- Additionally, the intertwined dynamics of plummeting lithium-ion battery prices, surging demand, and the establishment of new production facilities across China are reshaping the energy and automotive landscapes.

- By 2023, Chinese firms are increasingly consolidating their supply chains-from extracting raw materials like lithium and cobalt to the final battery production-ensuring consistent supply and cost-effectiveness. This trend is set to gain momentum in the coming years.

- Given these developments, the forecast period anticipates a surge in hybrid EV production and a corresponding uptick in lithium-ion battery demand.

Passengers Cars Segment to Witness Significant Growth

- Driven by heightened consumer awareness of environmental concerns and a growing demand for fuel-efficient vehicles, the passenger hybrid car segment is witnessing robust growth. Hybrid cars, which merge an internal combustion engine with an electric motor, boast superior fuel efficiency and reduced emissions when stacked against traditional gasoline-powered vehicles.

- Moreover, as the adoption of electric vehicles (EVs) surges, so does the demand for hybrid electric vehicles (HEVs), encompassing passenger cars. For example, the International Energy Agency (IEA) reported that in 2023, EV sales in the country reached approximately 8.1 million, marking a 37.2% uptick from 2022. With the government rolling out multiple initiatives to bolster the sales and demand for hybrid cars, this sales trajectory is poised to ascend in the forthcoming years.

- China is championing the adoption of hybrid electric vehicles (HEVs), including passenger cars, through a slew of government initiatives. These measures align with a larger agenda to combat air pollution and curtail reliance on fossil fuels.

- As a case in point, in 2023, the government rolled out a scrappage scheme incentivizing drivers to swap their aging internal combustion engine (ICE) vehicles for newer electric or plug-in hybrid models. This initiative offers buyers a financial boost of up to 10,000 yuan (approximately USD 1,375) when acquiring a new EV or plug-in hybrid. Such moves are set to amplify the demand for hybrid passenger cars in the region and subsequently, the need for HEV batteries during the forecast period.

- Moreover, the Chinese government is actively backing research and development in battery technology, electric drivetrains, and other pivotal components for hybrid and electric vehicles. By partnering with research institutions and motivating private enterprises, the government aims to fast-track technological breakthroughs.

- For instance, in June 2024, China's Ministry of Industry and Information Technology unveiled fresh directives for the lithium-ion battery sector. These guidelines seek to elevate the industry, ensuring it aligns with the swift growth in sectors like automobiles, particularly those involving hybrid electric vehicles. Such proactive measures are anticipated to bolster the hybrid passenger car market and escalate the demand for hybrid batteries in the near future.

- These project advancements underscore the viability and significance of HEV battery solutions for passenger vehicles, hinting at a burgeoning demand for HEV batteries nationwide in the upcoming year.

China Hybrid Electric Vehicle Battery Industry Overview

The China Hybrid Electric Vehicle battery market is semi-fragmented. Some of the key players (not in particular order) are LG Energy Solution Ltd, Toshiba Corporation, Panasonic Holdings Corporation, BYD Company, Contemporary Amperex Technology Co. Limited, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Increasing Electric Vehicle (EV) Production

- 4.5.1.2 Declining Lithium-ion Battery Prices

- 4.5.2 Restraints

- 4.5.2.1 Avalibility of Alternate Electric Vehicle Technology

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Sodium-ion Battery

- 5.1.4 Others

- 5.2 Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Company Ltd

- 6.3.2 Contemporary Amperex Technology Co. Limited

- 6.3.3 LG Energy Solution Ltd

- 6.3.4 Panasonic Holdings Corporation

- 6.3.5 Toshiba Corporation

- 6.3.6 Duracell Inc.

- 6.3.7 Okaya Power Group

- 6.3.8 Guoxuan High-Tech Co., Ltd

- 6.3.9 Clarios

- 6.3.10 EVE Energy Co., Ltd.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in Battery Materials

02-2729-4219

+886-2-2729-4219

中東和非洲混合動力電動車電池市場佔有率分析、產業趨勢、統計和成長預測(2025-2030)

中東和非洲混合動力電動車電池市場佔有率分析、產業趨勢、統計和成長預測(2025-2030) 亞太地區混合電動汽車電池 -市場佔有率分析、產業趨勢、成長預測(2025-2030)

亞太地區混合電動汽車電池 -市場佔有率分析、產業趨勢、成長預測(2025-2030) 北美混合電動汽車電池:市場佔有率分析、行業趨勢和成長預測(2025-2030)

北美混合電動汽車電池:市場佔有率分析、行業趨勢和成長預測(2025-2030) 南美混合電動汽車電池:市場佔有率分析、行業趨勢和成長預測(2025-2030)

南美混合電動汽車電池:市場佔有率分析、行業趨勢和成長預測(2025-2030) 印度混合電動汽車電池 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030)

印度混合電動汽車電池 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030) 德國混合動力電動車電池:市場佔有率分析、產業趨勢、成長預測(2025-2030)

德國混合動力電動車電池:市場佔有率分析、產業趨勢、成長預測(2025-2030) 東南亞國協混合動力汽車電池:市場佔有率分析、產業趨勢與成長預測(2025-2030)

東南亞國協混合動力汽車電池:市場佔有率分析、產業趨勢與成長預測(2025-2030) 歐洲混合動力電動車電池 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

歐洲混合動力電動車電池 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 法國混合動力汽車電池市場:佔有率分析、產業趨勢、成長預測(2025-2030)

法國混合動力汽車電池市場:佔有率分析、產業趨勢、成長預測(2025-2030) 混合動力電動車電池:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

混合動力電動車電池:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

▼