|

市場調查報告書

商品編碼

1636530

東南亞國協混合動力汽車電池:市場佔有率分析、產業趨勢與成長預測(2025-2030)ASEAN Countries Hybrid Electric Vehicle Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

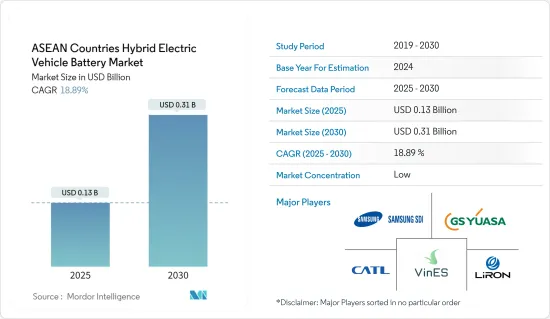

預計2025年東南亞國協混合動力汽車電池市場規模將達1.3億美元,2030年將達3.1億美元,預測期間(2025-2030年)複合年成長率為18.89%。

主要亮點

- 從中期來看,鋰離子電池價格的下降和電動車滲透率的提高預計將在預測期內推動東南亞國協混合動力電動車電池市場的需求。

- 另一方面,原料供需不匹配預計將阻礙預測期內的市場成長。

- 電池技術的進步以及汽車製造商和電池製造商之間的合作預計將為未來東南亞國協的混合動力電動車電池市場創造重大機會。

- 泰國尤其脫穎而出,在致力於增加電動車在汽車產業的普及的推動下,預計將顯著成長。

東南亞國協混合動力汽車電池市場趨勢

乘用車板塊實現大幅成長

- 東協(東南亞國家聯盟)國家準備實現混合動力電動車(HEV)電池市場的顯著成長,特別是乘用車電池。這種快速成長的推動因素包括電動車 (EV) 的日益普及、政府支持清潔能源的舉措以及消費者對環境問題意識的不斷增強。近年來,印尼、馬來西亞、泰國、越南和菲律賓等國家已成為電動車領域的關鍵參與企業。

- 東協汽車聯合會(AAF)資料顯示,2023年東協地區乘用車產量為274.8萬輛,比2022年的266.5萬輛成長3.11%。 2022年產量約221.2萬輛,2023年產量228.3萬輛,成長3.21%。值得注意的是,印尼、馬來西亞和泰國佔該地區乘用車產量的83%以上。

- 展望未來,政府推動電動車採用的措施預計將促進該地區乘用車的成長,這也將推動對混合動力汽車電池的需求。由於政府的支持措施,泰國、印尼、新加坡、馬來西亞和菲律賓等國家預計電動車將迅速普及。例如,菲律賓的目標是到 2030 年電動車佔所有車輛的 21%,到 2040 年達到 50%。除其他福利外,菲律賓電動車協會 (EVAP) 大膽地將其電動車普及率目標從 2030 年的 30 萬輛提高到 100 萬輛,提高了行業獎勵、監管透明度和對電動車優勢的認知,我期待這一成長。

- 印尼的野心同樣引人注目,該國的目標是到 2025 年電動車佔汽車銷量的 20%,到 2030 年國內電動車產量達到 60 萬輛。這些目標包括電動車供應鏈中的各種里程碑,包括銷售、生產和充電基礎設施,所有這些都將推動混合動力汽車電池的成長。

- 2024 年初,泰國電動車委員會批准了 EV 3.5 包裝,這是一項為期四年(2024-2027 年)的舉措,旨在加速電動車行業的發展並吸引對當地核准的投資。這項全面的一攬子計畫不僅旨在振興整個電動車生態系統,還包括針對車型和電池容量的電動車購買的政府補貼,為混合動力汽車電池市場創造了有利的環境。

- 2023年,菲律賓能源部(DOE)宣布計畫在2040年擁有630萬輛電動車(EV),目標是佔道路交通量的50%。這一雄心勃勃的目標也將透過安裝約 147,000 個電動車充電站來實現。美國能源部的近期目標包括 2028 年部署 245 萬輛電動車、摩托車和巴士。如此大規模的計畫證實了乘用車領域電池市場的快速成長,並將進一步支撐HEV電池市場的成長。

- 鑑於這些動態,乘用車領域預計在未來幾年將顯著成長。

泰國正在經歷顯著的成長

- 泰國是汽車領域的投資目的地。 50年來,泰國已從一個簡單的汽車零件組裝國家發展成為東南亞首屈一指的汽車生產和出口中心。隨著汽車製造商投資的增加,泰國的電池產業有望穩定成長,特別是隨著包括混合動力汽車在內的電動車 (EV) 產量的激增。

- 根據泰國電動車協會(EVAT)的報告,2023年泰國新登記的混合動力電動車(HEV)約為85,069輛,與前一年同期比較大幅增加32%。此外,到2024年2月底,新註冊的混合動力汽車數量將達到約26,134輛,支援泰國電池的快速成長和不斷成長的需求。

- 電動車(尤其是混合動力車)的快速成長得益於政府對購買者的激勵措施和對製造商的支持措施。例如,泰國推出了國產電動車購買補貼計劃,凸顯其成為東南亞電動車生產中心的雄心。 EV3.5 計畫的有效期為 2024 年至 2027 年,為每輛車提供 50,000泰銖(1,397.02 美元)至 100,000泰銖(2,794.04 美元)的補貼,以培育電動汽車顯汽車的承諾。

- 泰國的目標是到 2030 年電動車佔汽車銷售量的 30%。這項雄心壯志和目前的努力使泰國成為未來混合動力汽車電池(尤其是鋰離子電池)的中心,為電池製造商創造了巨大的機會。

- 為了實現這一願景,許多電池製造商正在增加在泰國的產能。例如,2024年3月,BMW集團在泰國舉行了「Gen-5」高壓電池製造工廠的奠基儀式。這座佔地4000平方公尺的電池組裝廠位於東海岸羅勇府,併入寶馬現有的汽車工廠。隨著BMW準備在 2025 年底在羅勇工廠推出電動車,新的電池組裝將在將進口電池轉換為高壓電池模組方面發揮至關重要的作用。據稱,寶馬已在該合資企業中投資了超過 4,500 萬美元。

- 鑑於這些發展,預計泰國將在預測期內引領東協地區的混合動力汽車電池市場。

東南亞國協混合動力汽車電池產業概況

東南亞國協的混合動力汽車電池已減少一半。市場主要企業(排名不分先後)包括三星 SDI、VinES Energy Solutions Joint Stock Company、Contemporary Amperex Technology (CATL)、LiRON LIB Power Pte Ltd 和 GS Yuasa Corporation。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 鋰離子電池價格下降

- 電動車的擴張

- 抑制因素

- 原料供需不匹配

- 促進因素

- 供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品/服務的威脅

- 競爭公司之間的敵對關係

- 投資分析

第5章市場區隔

- 電池類型

- 鋰離子電池

- 鉛酸電池

- 鈉離子電池

- 其他電池類型

- 車型

- 客車

- 商用車

- 地區

- 泰國

- 印尼

- 菲律賓

- 馬來西亞

- 越南

- 其他東南亞國協

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Panasonic Corporation

- Samsung SDI Co., Ltd.

- Contemporary Amperex Technology Co. Ltd(CATL)

- LG Energy Solution Ltd.

- LiRON LIB Power Pte Ltd

- GS Yuasa Corporation

- VinES Energy Solutions Joint Stock Company

- SVOLT Energy Technology Co., Ltd.

- Energy Absolute Public Company Limited

- 其他知名公司名單(公司名稱、總部地點、相關產品及服務、聯絡等)

- 市場排名/佔有率分析

第7章 市場機會及未來趨勢

- 電池技術的技術進步

The ASEAN Countries Hybrid Electric Vehicle Battery Market size is estimated at USD 0.13 billion in 2025, and is expected to reach USD 0.31 billion by 2030, at a CAGR of 18.89% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, declining lithium-ion battery prices, and growing adoption of electric vehicles are expected to drive the demand for the ASEAN countries hybrid electric vehicle battery market during the forecast period.

- On the other hand, the demand-supply mismatch of raw materials is expected to hinder the market's growth during the forecast period.

- Nevertheless, the technological advancements in battery technologies and the automaker-battery manufacturer collaborations are expected to create vast opportunities for ASEAN countries hybrid electric vehicle battery market in the future.

- Particularly, Thailand stands out, anticipating notable growth, driven by its commitment to amplifying the electric vehicle's presence in its automotive sector.

ASEAN Countries Hybrid Electric Vehicle Battery Market Trends

Passenger Vehicle Segment to Witness Significant Growth

- The ASEAN (Association of Southeast Asian Nations) countries are poised for significant growth in the market for hybrid electric vehicle (HEV) batteries, especially for passenger vehicles. This surge is driven by the increasing adoption of electric vehicles (EVs), government initiatives championing clean energy, and heightened consumer awareness of environmental concerns. In recent years, nations like Indonesia, Malaysia, Thailand, Vietnam, and the Philippines have emerged as pivotal players in the EV landscape.

- Data from the ASEAN Automotive Federation (AAF) reveals that the ASEAN region produced 2.748 million passenger vehicles in 2023, marking a 3.11% rise from 2.665 million in 2022. In 2022, production was approximately 2.212 million units, and the 2023 figure of 2.283 million units represents a 3.21% uptick. Notably, Indonesia, Malaysia, and Thailand collectively accounted for over 83% of the region's passenger vehicle output.

- Looking ahead, the region's growth in passenger vehicles is anticipated to be bolstered by government initiatives promoting electric vehicle adoption, subsequently driving demand for HEV batteries. Countries like Thailand, Indonesia, Singapore, Malaysia, and the Philippines are set to experience swift EV adoption, thanks to supportive government measures. For instance, the Philippines aims for EVs to constitute 21% of its total vehicles by 2030 and 50% by 2040. Additionally, the Electric Vehicle Association of the Philippines (EVAP) has upped its e-vehicle adoption target from 300,000 units in 2030 to a bold 1.0 million, banking on sector incentives, clearer regulations, and rising EV benefits awareness.

- Indonesia's ambitions are equally pronounced, targeting 20% EV representation in car sales by 2025 and a goal of 600,000 domestically produced EVs by 2030. These targets encompass various milestones in the EV supply chain, including sales, production, and charging infrastructure, all of which are set to spur HEV battery growth.

- In early 2024, Thailand's EV Board greenlit the EV 3.5 package, a four-year initiative (2024-2027) aimed at propelling the EV industry's momentum and attracting investments in local manufacturing. This comprehensive package not only seeks to invigorate the entire EV ecosystem but also includes government subsidies for EV purchases, tailored to vehicle types and battery capacities, fostering a conducive environment for the HEV battery market.

- In 2023, the Philippines' Department of Energy (DOE) unveiled plans to have 6.3 million electric vehicles (EVs) by 2040, targeting 50% of the road traffic. This ambitious goal is complemented by the installation of approximately 147,000 EV charging stations. The DOE's immediate objective includes deploying 2.45 million electric cars, motorcycles, and buses by 2028. Such expansive plans underscore the burgeoning battery market within the passenger vehicle segment, further propelling the HEV battery market's growth.

- Given these dynamics, the passenger vehicle segment is set for substantial growth in the coming years.

Thailand to Witness a Significant Growth

- Thailand stands out as a prime destination for investments in the automobile sector. Over the past five decades, Thailand has evolved from merely assembling auto components to becoming Southeast Asia's foremost automotive production and export hub. With rising investments from automakers, Thailand's battery industry is poised for steady growth, especially with the surge in electric vehicle (EV) production, including hybrids.

- As reported by the Electric Vehicle Association of Thailand (EVAT), Thailand registered approximately 85,069 new hybrid electric vehicles (HEVs) in 2023, marking a significant 32% increase from the previous year. Furthermore, by the end of February 2024, new HEV registrations reached around 26,134 units, underscoring the rapid growth and heightened demand for batteries in the nation.

- The surge in EV adoption, particularly HEVs, can be attributed to government incentives for buyers and supportive measures for manufacturers. For instance, Thailand's introduction of a purchase subsidy scheme for domestically produced EVs underscores its ambition to be Southeast Asia's EV production hub. The EV3.5 scheme, active from 2024 to 2027, offers subsidies between THB 50,000 (USD 1,397.02) and THB 100,000 (USD 2,794.04) per vehicle, highlighting the government's dedication to nurturing the EV sector and drawing in foreign investments.

- Thailand aims to have EVs make up 30% of all vehicle sales by 2030. This ambition, coupled with current initiatives, positions Thailand as a future hub for HEV batteries, especially lithium-ion types, presenting vast opportunities for battery manufacturers.

- In line with this vision, numerous battery manufacturers are ramping up their production capabilities in Thailand. For instance, in March 2024, BMW Group broke ground on its 'Gen-5' high-voltage battery manufacturing facility in Thailand. Situated in Rayong, on the eastern coast, the 4,000 square meter battery assembly is integrated into BMW's existing car plant. As BMW gears up to launch EVs from this Rayong facility in the latter half of 2025, the new battery assembly line will play a pivotal role, converting imported battery cells into modules for high-voltage batteries. BMW has reportedly invested over USD 45 million in this venture.

- Given these developments, Thailand is poised to lead the HEV battery market in the ASEAN region during the forecast period.

ASEAN Countries Hybrid Electric Vehicle Battery Industry Overview

The ASEAN Countries Hybrid Electric Vehicle Battery is semi-fragmented. Some of the key players in the market (not in any particular order) include Samsung SDI Co. Ltd., VinES Energy Solutions Joint Stock Company, Contemporary Amperex Technology Co. Ltd (CATL), LiRON LIB Power Pte Ltd and GS Yuasa Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Declining Lithium-Ion Battery Prices

- 4.5.1.2 Increasing Adoption of Electric Vehicles

- 4.5.2 Restraints

- 4.5.2.1 Demand-Supply Mismatch of Raw Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-acid Battery

- 5.1.3 Sodium-ion Battery

- 5.1.4 Others Battery Types

- 5.2 Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 Geography

- 5.3.1 Thailand

- 5.3.2 Indonesia

- 5.3.3 Philippines

- 5.3.4 Malaysia

- 5.3.5 Vietnam

- 5.3.6 Rest of ASEAN Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Panasonic Corporation

- 6.3.2 Samsung SDI Co., Ltd.

- 6.3.3 Contemporary Amperex Technology Co. Ltd (CATL)

- 6.3.4 LG Energy Solution Ltd.

- 6.3.5 LiRON LIB Power Pte Ltd

- 6.3.6 GS Yuasa Corporation

- 6.3.7 VinES Energy Solutions Joint Stock Company

- 6.3.8 SVOLT Energy Technology Co., Ltd.

- 6.3.9 Energy Absolute Public Company Limited.

- 6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 6.5 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in Battery Technologies

中國混合動力汽車電池市場:佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國混合動力汽車電池市場:佔有率分析、產業趨勢/統計、成長預測(2025-2030) 中東和非洲混合動力電動車電池市場佔有率分析、產業趨勢、統計和成長預測(2025-2030)

中東和非洲混合動力電動車電池市場佔有率分析、產業趨勢、統計和成長預測(2025-2030) 亞太地區混合電動汽車電池 -市場佔有率分析、產業趨勢、成長預測(2025-2030)

亞太地區混合電動汽車電池 -市場佔有率分析、產業趨勢、成長預測(2025-2030) 北美混合電動汽車電池:市場佔有率分析、行業趨勢和成長預測(2025-2030)

北美混合電動汽車電池:市場佔有率分析、行業趨勢和成長預測(2025-2030) 南美混合電動汽車電池:市場佔有率分析、行業趨勢和成長預測(2025-2030)

南美混合電動汽車電池:市場佔有率分析、行業趨勢和成長預測(2025-2030) 印度混合電動汽車電池 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030)

印度混合電動汽車電池 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030) 德國混合動力電動車電池:市場佔有率分析、產業趨勢、成長預測(2025-2030)

德國混合動力電動車電池:市場佔有率分析、產業趨勢、成長預測(2025-2030) 歐洲混合動力電動車電池 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

歐洲混合動力電動車電池 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 法國混合動力汽車電池市場:佔有率分析、產業趨勢、成長預測(2025-2030)

法國混合動力汽車電池市場:佔有率分析、產業趨勢、成長預測(2025-2030) 混合動力電動車電池:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

混合動力電動車電池:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)