|

市場調查報告書

商品編碼

1637913

亞太網路安全:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)APAC Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

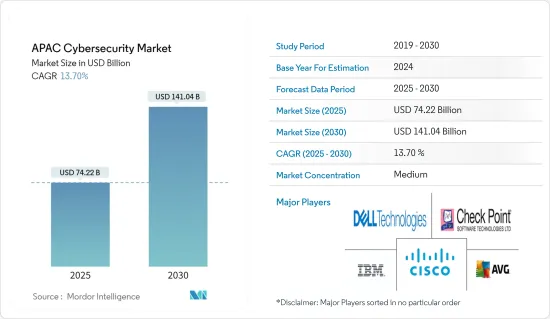

2025年亞太地區網路安全市場規模預估為742.2億美元,預估至2030年將達1,410.4億美元,預測期間(2025-2030年)複合年成長率為13.7%。

隨著物聯網的出現以及該地區數位轉型的速度和範圍的不斷擴大,目前的網路基礎設施更容易受到網路攻擊。近年來,網路、社群媒體和行動裝置的使用均大幅成長,推動該地區網路安全水準的強勁提升。由於這些攻擊的嚴重性日益增加以及政府立法的嚴格,亞太地區的網路安全產業預計將進一步擴大。

主要亮點

- 已開發國家和新興國家網際網路使用量的不斷增加正在推動網路安全解決方案的採用。此外,行動裝置無線網路的擴展帶來了資料脆弱性的增加,這使得網路安全成為任何組織的關鍵因素。

- 包括印度、中國、新加坡和日本在內的許多新興國家正面臨日益嚴峻的網路安全相關挑戰。印度的 DNS 劫持案件數量位居第三,這顯示登記的網路犯罪急劇增加。此外,根據IBM X-Force威脅情報指數2022,亞洲將在2021年遭受全球26%的攻擊,成為全球受攻擊最嚴重的地區。印度是亞洲遭受攻擊最頻繁的國家。澳洲網路安全成長網路最近進行的一項研究顯示,未來十年網路安全產業的規模可能會擴大兩倍。

- 近年來,網路安全事件屢屢發生,但大部分仍處於隱蔽狀態。最近一些備受矚目的案件對眾多公眾產生了重大影響,使其成為公眾討論的焦點以及政府和監管機構的關注。例如,印度官方網路安全組織CERT-In已就資訊安全實務、程序、網路事件的預防、回應和報告發布了指示,以確保網路的安全可靠,並引入了嚴格的網路安全報告要求。據該機構稱,截至 2022 年 2 月,印度已發生 212 多起網路安全事件。

- 行業內部網路設備的數量正在增加,例如家用電器、連網汽車和工廠,這不僅透過降低設備成本,而且還透過創建新的商業模式和應用程式,推動了物聯網的採用並加強了企業的網路安全。因此,M2M/IoT 連接的採用正在推動網路安全市場的發展。

- 挑戰在於準備程度低和對傳統身分驗證技術的高度依賴。在安全專家建議採用臉部認證和生物識別等身分管理解決方案的市場環境中,超過 80% 的組織仍然僅依靠使用者名稱和密碼登錄,這可能會對成長構成挑戰。

亞太地區網路安全市場趨勢

雲端部署推動市場成長

- 隨著企業越來越意識到將資料遷移到雲端以節省成本和資源(而不是建置和維護新的資料儲存)的重要性,對雲端基礎的解決方案的需求正在成長。正在增加。

- 這些優勢正在推動該地區大大小小的企業採用雲端基礎的解決方案。未來幾年,雲端平台和生態系統有望成為爆發數位創新速度和規模的發射台。

- 根據思科網路安全報告,亞太地區國家更有可能將其基礎架構的更高比例託管在雲端而不是本地端。此外,2023 年 3 月舉行的思科印度峰會上,將舉辦一個論壇,以促進網路安全能力,增強印度企業的安全韌性,並幫助他們利用數位化作為競爭優勢。 ,思科宣布將在清奈建立一個新的資料中心,並資料位於孟買的現有資料中心進行現代化改造。

- 隨著 Google Drive、Dropbox 和 Microsoft Azure 等雲端服務擴大被採用,並且這些工具成為業務流程不可或缺的一部分,企業必須解決對敏感資料失去控制等安全性問題。這導致按需網路安全解決方案的採用率增加。

- 該地區的微軟等公司正在提供雲端基礎的端點保護技術,使員工可以在他們想要的時間、地點和方式下工作,並幫助他們完成工作。對你有益。

中國佔有最大市場佔有率

- 國內網路攻擊的增多促使中國加強防禦能力。在世界其他地區,政府也是網路攻擊的主要來源。根據Cloudflare提供的數據,2022年3月,中國佔全球網路攻擊事件的45%。

- 預計在預測期內,政府和相關監管機構將加大力度加強雲端安全,從而推動基於網路安全的解決方案的採用。

- 2022年1月,國家網路資訊辦公室宣布了對購買可能影響國家安全的網路產品和服務的關鍵資訊基礎設施營運商(CIIO)進行網路安全審查的新措施。該措施包括對關鍵通訊產品、高效能電腦及伺服器、大容量儲存設備、大型資料庫及應用程式、雲端運算服務以及其他對關鍵資訊基礎設施安全有重大影響的網路產品和服務進行限制。向網路安全審查辦公室(CRO)申請網路安全審查。

- 此外,加密在中國面臨更大的阻力。該國政府的加密法規和執行是世界上最嚴格的之一,政府可以完全存取其境內的所有加密內容。 《中華人民共和國密碼法》第三十一條規定,國家密碼管理局有權對密碼系統進行檢查、存取。該規則適用於所有行業,包括微信等社交媒體平台,因為對話不是端對端加密的。

- 技術進步正在增加中國聯網設備的數量。它是全球最大的物聯網(IoT)市場。此外,5G和支援5G的設備將大大提高設備互聯互通性。由此帶來的連網設備的增加直接增加了安全產品的市場需求。

亞太網路安全產業概況

亞太網路安全市場處於半分散狀態。企業對行動安全意識的不斷提高,促使市場參與者採取併購、合作和新產品等策略性舉措。

- 2022 年 2 月:上述日期投資的印度 IBM 安全指揮中心標誌著對亞太地區組織安全事件回應和培訓的一項重大投資。該中心旨在透過高度逼真的網路攻擊模擬,為從高管到技術人員的每個人提供網路安全回應技術培訓。這項投資還包括一個全新的安全營運中心 (SOC),這將擴大 IBM 廣泛的全球 SOC 網路,為全球客戶提供全天候的安全回應服務。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業指引及政策

- COVID-19 市場影響評估

第5章 市場動態

- 市場促進因素

- 網路安全事件和報告法規迅速增加

- 日益增加的 M2M/IoT 連線要求企業加強網路安全措施

- 市場限制

- 網路安全專家短缺

- 高度依賴傳統身分驗證方法且缺乏準備

- 市場機會

- 物聯網、BYOD、人工智慧和機器學習在網路安全領域的發展趨勢

第6章 市場細分

- 依產品類型

- 解決方案

- 身分和存取管理

- 威脅偵測和預防(統一威脅管理和威脅緩解)

- 安全和漏洞管理

- DDoS 緩解

- 新一代防火牆

- IDS/IPS

- 安全資訊和事件管理

- 其他解決方案

- 按服務

- 解決方案

- 按部署

- 在雲端

- 本地

- 按最終用戶產業

- 航太和國防

- 銀行、金融服務和保險

- 衛生保健

- 製造業

- 零售

- 資訊科技/通訊

- 其他最終用戶產業

- 按國家

- 中國

- 印度

- 日本

- 韓國

第7章 競爭格局

- 公司簡介

- AVG Technologies(Avast Software sro)

- IBM Corporation

- Check Point Software Technologies Ltd

- Cisco Systems Inc.

- Cyber Ark Software Ltd

- Dell Technologies Inc.

- Fireeye Inc.

- Fortinet Inc.

- Imperva Inc.

- Intel Security(Intel Corporation)

- Palo Alto Networks Inc.

- Proofpoint Inc.

- Rapid7 Inc.

- Broadcom Inc.

- Trend Micro Inc.

第8章投資分析

第9章:市場的未來

The APAC Cybersecurity Market size is estimated at USD 74.22 billion in 2025, and is expected to reach USD 141.04 billion by 2030, at a CAGR of 13.7% during the forecast period (2025-2030).

Due to the advent of IoT and the growing speed and scope of digital transformation in this region, the current network infrastructure is becoming more exposed to cyberattacks. Internet, social media, and mobile users have all seen significant increases in recent years, contributing to the region's strong rise in cybersecurity. The Asia-Pacific cybersecurity industry is expected to expand even more due to the increasing severity of these attacks and strict government laws.

Key Highlights

- The growing internet usage in both developed and developing countries increases the adoption of cybersecurity solutions. Additionally, due to increased data susceptibility brought on by the expansion of the wireless network for mobile devices, cybersecurity has become a crucial component of every organization.

- Many emerging countries, such as India, China, Singapore, and Japan, face increasing cybersecurity-related issues. India ranks third in the number of DNS hijacks, indicating a sharp rise in cybercrime registration. Additionally, Asia received 26% of all worldwide attacks in 2021, according to IBM X-Force Threat Intelligence Index 2022, making it the most attacked area globally. India tops the list of the most frequently attacked country in Asia. Recent research by the Australian Cyber Security Growth Network entitled the cybersecurity sector might triple in size over the next ten years.

- Although there have been several cybersecurity events in recent years, most of them have remained hidden. Recent high-profile incidents that significantly impacted many common persons have brought public conversation and government and regulatory body attention to the forefront. For Instance, CERT-In, India's official cybersecurity organization, issued a direction relating to Information security practices, procedures, prevention, response, and reporting of cyber incidents for safe and trusted internet to impose stringent cybersecurity reporting requirements. It stated that India had recorded over 2.12 lakh cybersecurity incidents as of February 2022.

- The industry is being driven by new business models and applications as well as reducing device costs, such as an increasing number of connected devices, including consumer electronics, connected cars, factories, etc., which is driving the adoption of IoT and strengthening cybersecurity in enterprises. So, The adoption of M2M/IoT connections drives the cybersecurity market.

- Low preparedness and a high reliance on conventional authentication techniques are challenging. In a market environment where security professionals advise identity-management solutions like facial recognition and biometric identification, more than 80% of organizations still rely solely on usernames and passwords for login, which could challenge growth.

Asia Pacific Cyber Security Market Trends

Cloud Deployment Drives Market Growth

- The increasing realization among companies about the importance of saving money and resources by moving their data to the cloud rather than building and maintaining new data storage drives the demand for cloud-based solutions, hence increasing the adoption of on-demand security services.

- Owing to these benefits, large enterprises and SMEs in the region are increasingly adopting cloud-based solutions. Over the next few years, cloud platforms and ecosystems are expected to serve as the launch pad for an explosion in the pace and scale of digital innovation.

- Countries in the Asia-Pacific tend to have higher percentages of their infrastructures hosted in the cloud rather than on-premise, according to the CISCO Cybersecurity report. Additionally, in March 2023, during the Cisco India Summit 2023, the company announced that it has been growing its cyber security capabilities to support Indian businesses in strengthening their security resilience and utilizing digitalization as a competitive advantage and to provide its clients with better security options, Cisco has been establishing a new data center in Chennai and modernizing the one that already exists in Mumbai.

- With the rising adoption of cloud services, like Google Drive, Dropbox, and Microsoft Azure, and with these tools emerging as an integral part of business processes, enterprises must deal with security issues, such as losing control over sensitive data. This gives rise to the increased incorporation of on-demand cyber-security solutions.

- The company, such as Microsoft in the region, offers Cloud-based endpoint protection technology that enables employees to work when, where, and how they need to function and can allow them to use the devices and apps they find most beneficial to get their work done.

China to Occupy the Largest Market Share

- Growing cyber-attacks in the country have propelled China to strengthen its defensive capabilities. The government is also a major source of cyberattacks in other parts of the world. According to the statistics provided by Cloudflare, in March 2022, China accounted for 45% of the world's cyberattack incidents.

- The increasing initiatives by the government and the related regulatory bodies to strengthen cloud security are expected to fuel the adoption of cyber security-based solutions over the forecast period.

- The Cyberspace Administration of China issued new measures for cybersecurity review in January 2022 for critical information infrastructure operators (CIIO) purchasing network products and services, which may influence national security. Under this measure, Important communications products, high-performance computers or servers, mass storage equipment, large database or application, cloud computing service, or any other network product or service that has an important influence on the security of any critical information infrastructure, CIIO should apply to Cybersecurity Review Office (CRO) for cybersecurity review.

- Moreover, encryption has met greater resistance in China. The government's encryption regulations and implementation are among the most restrictive in the world, giving the government full access to all encrypted content within its domestic territory. Article 31 of China's Cryptography Law allows the State Cryptography Administration to inspect and access encrypted systems. Since conversations are not end-to-end encrypted, this rule applies to all industries, including social media platforms like WeChat, which are required (and able) to turn over all user data.

- Owing to technological advancements, there is an increase in the number of connected devices in China. It is the world's largest Internet of Things (IoT) market. Furthermore, 5G and 5G enabled devices will exponentially increase the devices' interconnectivity. As a result, it increases connected devices, directly augmenting the market's need for security products.

Asia Pacific Cyber Security Industry Overview

The Asia-Pacific cybersecurity market is semi fragmented. Players in the market adopt strategic initiatives such as mergers and acquisitions, partnerships, and new product offerings due to increasing awareness regarding mobility security among enterprises.

- February 2022: The IBM Security Command Center in India, for which investments were made on the aforementioned date, represents a sizeable investment in security incident response and training for organizations throughout the Asia-Pacific. It is designed to prepare everyone from the C-Suite to technical staff by training cybersecurity response techniques through highly realistic, simulated cyberattacks. The investment also includes a brand-new Security Operation Center (SOC), which would be added to IBM's extensive worldwide network of SOCs and would offer clients all over the world round-the-clock security response services.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Competitive Rivalry within the Industry

- 4.4 Industry Guidelines and Policies

- 4.5 Assessment of the Impact of the COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapidly Increasing Cybersecurity Incidents and Regulations Requiring Their Reporting

- 5.1.2 Growing M2M/IoT Connections Demanding Strengthened Cybersecurity in Enterprises

- 5.2 Market Restraints

- 5.2.1 Lack of Cybersecurity Professionals

- 5.2.2 High Reliance on Traditional Authentication Methods and Low Preparedness

- 5.3 Market Opportunities

- 5.3.1 Rise in the Trends of IoT, BYOD, Artificial Intelligence, and Machine Learning in Cybersecurity

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Solutions

- 6.1.1.1 Identity and Access Management

- 6.1.1.2 Threat Detection and Prevention (Unified Threat Management and Threat Mitigation)

- 6.1.1.3 Security and Vulnerability Management

- 6.1.1.4 DDoS Mitigation

- 6.1.1.5 Next Generation Firewall

- 6.1.1.6 IDS/IPS

- 6.1.1.7 Security Information and Event Management

- 6.1.1.8 Other Solutions

- 6.1.2 Services

- 6.1.1 Solutions

- 6.2 By Deployment

- 6.2.1 On-cloud

- 6.2.2 On-premises

- 6.3 By End-user Industry

- 6.3.1 Aerospace and Defense

- 6.3.2 Banking, Financial Services, and Insurance

- 6.3.3 Healthcare

- 6.3.4 Manufacturing

- 6.3.5 Retail

- 6.3.6 IT and Telecommunication

- 6.3.7 Other End-user Industries

- 6.4 By Country

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.4.4 South Korea

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 AVG Technologies (Avast Software s.r.o.)

- 7.1.2 IBM Corporation

- 7.1.3 Check Point Software Technologies Ltd

- 7.1.4 Cisco Systems Inc.

- 7.1.5 Cyber Ark Software Ltd

- 7.1.6 Dell Technologies Inc.

- 7.1.7 Fireeye Inc.

- 7.1.8 Fortinet Inc.

- 7.1.9 Imperva Inc.

- 7.1.10 Intel Security (Intel Corporation)

- 7.1.11 Palo Alto Networks Inc.

- 7.1.12 Proofpoint Inc.

- 7.1.13 Rapid7 Inc.

- 7.1.14 Broadcom Inc.

- 7.1.15 Trend Micro Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025 年至 2029 年全球網路安全市場

2025 年至 2029 年全球網路安全市場 網路安全培訓市場,全球 2025-2029

網路安全培訓市場,全球 2025-2029 2025 年十大網路安全成長機會

2025 年十大網路安全成長機會 網路安全軟體市場報告:2031 年趨勢、預測與競爭分析

網路安全軟體市場報告:2031 年趨勢、預測與競爭分析 整合企業 IT 通訊解決方案的全球市場

整合企業 IT 通訊解決方案的全球市場 全球資料二極體市場(~2030):外形規格(DIN導軌、機架安裝、小型/可攜式)、類型(高耐用性、非高耐用性)、主要技術(光隔離、通訊協定轉換、流量過濾、資料包檢測)

全球資料二極體市場(~2030):外形規格(DIN導軌、機架安裝、小型/可攜式)、類型(高耐用性、非高耐用性)、主要技術(光隔離、通訊協定轉換、流量過濾、資料包檢測) 中國網路安全:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

中國網路安全:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 中東和非洲的網路安全 -市場佔有率分析、行業趨勢/統計、成長預測(2025-2030)

中東和非洲的網路安全 -市場佔有率分析、行業趨勢/統計、成長預測(2025-2030) 北美汽車網路安全:市場佔有率分析、產業趨勢與成長預測(2025-2030)

北美汽車網路安全:市場佔有率分析、產業趨勢與成長預測(2025-2030) 北美網路安全:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

北美網路安全:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)