|

市場調查報告書

商品編碼

1849999

3D列印:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030)3D Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

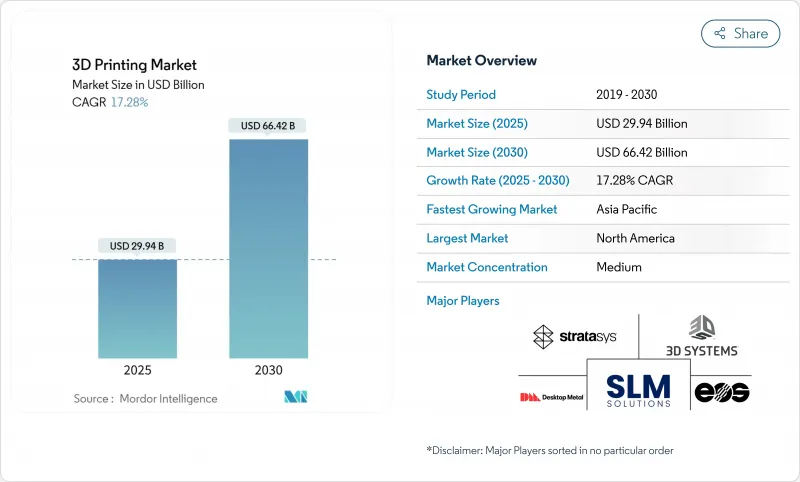

3D列印市場規模預計在2025年為299.4億美元,預計到2030年將達到664.2億美元,預測期內(2025-2030年)的複合年成長率為17.28%。

這一成長曲線得益於機器吞吐量的不斷提高、材料組合的豐富以及技術從快速原型製作向中小批量最終用途生產的逐步轉變。航太、醫療保健和汽車公司目前正在檢驗用於飛行硬體、植入式設備和結構支架的金屬和聚合物零件,這加速了對認證粉末和閉合迴路監控的需求。同時,服務機構正在擴展多雷射系統並提供雲端基礎的容量,從而降低新採用者的資本投資風險。美國和中國的戰略性政府資金正在加快認證時間表並抵消資本成本,而 ASTM主導的標準化預計將協調各地區的測試通訊協定。像 Nano Dimension 收購 Desktop Metal 這樣的合併表明投資者對增材工作流程將支撐下一代供應鏈的信心。

全球 3D 列印市場趨勢與洞察

北美政府資助的積層製造中心

聯邦和州政府計畫持續加速國內應用。 2025年1月,美國製造公司(America Makes)向計劃專注於現場計量、永續粉末回收和低成本鋁參數集的項目撥款210萬美元。該舉措將創建一個連接RTX技術研究中心、愛迪生焊接研究所和地區加工車間的協作測試平台。 ASTM標準化卓越中心提供的1500萬美元補充資金將用於協調數據格式和測試樣件,彌合研究原型與合格生產之間持續存在的差距。透過編纂製造參數包絡,該生態系統將減少重複測試,並縮短3D列印市場的認證週期,尤其是在航太和醫療設備供應鏈領域。

歐洲採用金屬積層製造技術滿足航太零件需求激增

歐洲的MRO供應商擴大使用粉末冶金熔合技術來替換停產的零件,而無需承擔倉儲費用。 SpaceX的Raptor 3艙室採用多雷射粉末床熔合技術製造,展示了從演示到飛行就緒部件的路徑。歐洲監管機構已經明確了非關鍵金屬內飾的指導方針,使30件或更少件的小批量生產在經濟上可行。漢莎技術公司、賽峰集團和勞斯萊斯現在都儲備了可在維護點觸發列印訂單的數位庫存,將前置作業時間從數週縮短到不到48小時。隨著鈦和因科鎳合金粉末達到航太級的可重複性,歐洲3D列印市場正受益於與本地生產相關的碳足跡減少。

飛行關鍵零件的認證瓶頸持續存在

渦輪噴嘴和增壓閥等飛行硬體必須符合嚴格的斷裂韌性和疲勞測試。由於現行規則是針對減材製造流程製定的,因此積層製造零件需要重複的試樣測試,導致工期延長長達18個月。只有大型主要供應商才能承擔這些成本,這限制了小型二級供應商的3D列印市場。雖然ASTM和ISO工作小組正在起草針對特定方法的標準,但全球統一仍需數年時間。

細分分析

到 2024 年,硬體部門將佔全球收入的 60.23%,這得益於工業規模金屬熔煉、高溫聚合物和自動後處理的資本投資。然而,從 2025 年到 2030 年,服務業將以 25.21% 的複合年成長率超過硬體部門。 Stratasys Direct Manufacturing、Materialize 和 Protolabs 等合約製造商利用其多站點網路來分配工作負載,使客戶能夠創建原型並在 10 天內收到 ISO-13485 製造的零件。服務業的繁榮將降低經濟障礙並擴大 3D 列印市場的用戶群。然而,隨著 3MF 超越 STL,結合晶格生成器和成本估算引擎的雲原生建構準備工具將迎來機會。

隨著原始設備製造商將基於訂閱的機器租賃與遠端監控捆綁在一起,3D列印市場受益匪淺。新參與企業模仿影印機租賃,提供按頁計費的模式,將維護、校準和粉末補充整合到一張發票中。這種混合模式模糊了硬體和服務之間的界限,使宏觀經濟週期的收益流更加平滑。

隨著汽車、能源和航太產業從原型模具轉向批量生產,工業平台將在2024年佔據3D列印支出的72.14%。多雷射粉末熔化爐的鉻鎳鐵合金沉積速度達到150cc/小時,超越了過去的速度極限。製造商利用拓樸最佳化的支架將重量減輕40%,並整合了組裝流程。隨著3D列印的首次通過率接近數控銑削,整合粉末回收和即時熔池分析的製造腔將提高3D列印市場的可靠性。

桌面系統正在經歷復興,以 Bambu Lab 的高速 CoreXY 架構為代表,儘管銷量不大,但其加速度可達 20,000 毫米/秒²。各大學正在部署多達 1,000 個單元的叢集,用於教授增材設計原理,並為業界培養人才。牙醫和珠寶商正在採用 XY 解析度達到 30 微米的 LCD 樹脂印表機,從而將 3D 列印市場拓展到工程辦公室以外的領域。

3D 列印市場報告按組件(硬體、軟體、服務)、印表機類型(工業 3D 列印機、桌上型 3D 列印機)、技術(光聚合(SLA、DLP)、其他)、材料(聚合物、金屬和合金、其他)、最終用戶產業(汽車、航太和國防、其他)和地區進行細分。

區域分析

北美佔全球整體的41.68%,是財富500強企業招聘供應商、粉末噴塗機製造商、軟體供應商和契約製造製造商的集中地。 America Makes正在將津貼用於粉末回收和即時監控,以填補材料資料表的空白。美國正在採取多層次的積層製造方法,從艦載FDM設備到基地級DED維修,從而建構結構化的需求管道。通用電氣航空航太公司投資10億美元新建一座積層製造工廠,以加強航空合金的供應安全。 metal-am.com 在戰略金屬出口限制收緊的背景下,陸基粉末生產進一步分化了北美3D列印市場。

預計亞太地區的複合年成長率將達到 26.47%,這主要得益於中國的設備補貼和印度醫療保健的普及。北京的目標是到 2027 年實現 90% 的數位研發滲透率,這支持了對設計套件和模擬軟體的廣泛需求。日本正在利用積層製造技術生產用於半導體微影術的微解析度陶瓷組件。韓國正在資助一個產學研聯合實驗室,以完善電動汽車電機銅的金屬黏合劑噴射加工,從而支持該國的電氣化目標。在東南亞,新加坡的先進再製造和技術中心正在孵化一種混合增材裂解單元,這可能對船舶和石油鑽井平台的維護具有吸引力。

歐洲仍然是科研和生產領域的強國。空中巴士、賽峰集團和MTU航空引擎公司共同主導了一個標準開發聯盟,以確保各原始設備製造商(OEM)的幾何公差保持一致。一家德國汽車製造商正在使用黏著劑噴塗噴射不銹鋼零件作為儀表板支架,理由是對於年產量低於2萬輛的汽車,這種製程的循環時間比沖壓製程更快。斯堪地那維亞透過整合回收粉末流獲得了循環經濟認證。東歐契約製造製造商正在贏得西方原始設備製造商的大量訂單,這加劇了該地區3D列印市場的差異性。

中東地區透過能源和醫療保健項目加速成長。沙烏地阿美公司正在試驗用於暴露於矯正器具鹽度鹽水的海水淡化閥的耐腐蝕格柵插件。阿拉伯聯合大公國一家醫院與一所大學合作,印製用於複雜心血管手術的解剖模型。在非洲,義肢和備件的試點生產正在進行中,但基礎設施仍有缺口。巴西的SENAI網路教授「增材設計」課程,為未來的勞動力做好準備。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 北美政府資助的積層製造中心

- 歐洲金屬積層製造技術在航太零件按需生產中的應用激增

- 中國「中國製造2025」對工業3DP設備的補貼

- 印度對患者專用整形外科植入的需求不斷成長

- 海灣合作理事會能源產業向輕型格柵熱交換器 AM 轉型

- 電動車平台的全球普及正在導致工具需求的快速成長

- 市場限制

- 飛行關鍵零件認證瓶頸仍存在

- 高性能金屬粉末價格波動

- 適用於食品接觸應用的可印刷材料種類有限

- AM 軟體與傳統 PLM 套件之間的互通性差距

- 價值鏈/供應鏈分析

- 監理展望

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- COVID-19 市場影響

- 投資分析

第5章市場規模及成長預測

- 按組件

- 硬體

- 軟體

- 服務

- 依印表機類型

- 工業3D印表機

- 桌上型3D印表機

- 依技術

- 光聚合(SLA、DLP)

- 粉體熔化成型技術(SLS、SLM、EBM)

- 材料擠壓(FDM、FFF)

- 材料噴塗

- 黏著劑噴塗成型

- 定向能量沉澱

- 片材層壓

- 按材質

- 聚合物

- 金屬和合金

- 陶瓷

- 複合材料

- 其他成分

- 按用途

- 原型製作

- 製造和生產零件

- 工具及固定裝置

- 研究與開發

- 個人化消費品

- 按最終用戶產業

- 車

- 航太和國防

- 醫療保健和牙科

- 家電

- 建築與建築

- 能源(石油與天然氣、電力)

- 食物和烹飪

- 教育研究所

- 其他行業

- 按地區

- 北美洲

- 美國

- 加拿大

- 拉丁美洲

- 墨西哥

- 巴西

- 阿根廷

- 其他拉丁美洲地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 其他亞太地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Stratasys Ltd

- 3D Systems Corporation

- EOS GmbH

- General Electric Company(GE Additive)

- Hewlett Packard Inc.

- Desktop Metal Inc.

- Materialise NV

- SLM Solutions Group AG

- Velo3D Inc.

- Renishaw plc

- Ultimaker BV

- Formlabs Inc.

- Markforged Holding Corp.

- Nano Dimension Ltd.

- Prodways Group

- Tritone Technologies

- Carbon Inc.

- HP Inc.(Personalization division)

- UnionTech Inc.

- Sisma SpA

第7章 市場機會與未來展望

The 3D Printing Market size is estimated at USD 29.94 billion in 2025, and is expected to reach USD 66.42 billion by 2030, at a CAGR of 17.28% during the forecast period (2025-2030).

This growth arc is sustained by higher machine throughput, richer material portfolios, and the technology's gradual migration from rapid prototyping to low- and mid-volume end-use production. Aerospace, healthcare, and automotive firms now validate metal and polymer parts for flight hardware, implantable devices, and structural brackets, accelerating demand for certified powders and closed-loop monitoring. At the same time, service bureaus are scaling multi-laser systems to provide cloud-based capacity that de-risks capital investments for new adopters. Strategic government funding in the United States and China compresses qualification timelines and offsets equipment costs, while ASTM-led standardization is expected to harmonize testing protocols across regions. Consolidation, such as Nano Dimension's purchase of Desktop Metal, signals investor conviction that additive workflows will underpin next-generation supply chains.

Global 3D Printing Market Trends and Insights

Government-funded Additive Manufacturing Hubs in North America

Federal and state programs continue to accelerate domestic adoption. In January 2025, America Makes awarded USD 2.1 million to projects focused on in-situ metrology, sustainable powder recycling, and low-cost aluminum parameter sets. The initiative creates collaborative testbeds linking RTX Technology Research Center, Edison Welding Institute, and regional job-shops. Complementary funding under a USD 15 million ASTM Standardization Center of Excellence harmonizes data formats and test coupons, closing a persistent gap between research prototypes and qualified production. By codifying build-parameter envelopes, the ecosystem reduces redundant trials and shortens certification cycles for the 3D printing market, particularly in aerospace and medical device supply chains.

Surging Metal AM Adoption for On-demand Aerospace Spare Parts in Europe

European MRO providers increasingly rely on powder bed fusion to replace out-of-production parts without the overhead of warehousing. SpaceX's Raptor 3 chamber, produced through multi-laser laser-powder-bed fusion, illustrates the pathway from demonstrator to flight-ready part. Euro-control agencies have clarified guidelines for non-critical metallic interiors, making small-batch economics favorable even at volumes below 30 units. Lufthansa Technik, Safran, and Rolls-Royce now stock digital inventories that trigger print orders at the point of maintenance, cutting lead times from weeks to under 48 hours. As titanium and inconel powders reach aerospace-grade repeatability, the 3D printing market in Europe benefits from reduced carbon footprints tied to localized manufacturing.

Persistent Certification Bottlenecks for Flight-critical Parts

Flight hardware like turbine nozzles or pressurization valves must comply with rigorous fracture-toughness and fatigue tests. Current rulebooks were written for subtractive machining; hence, additive parts undergo redundant coupon testing that extends schedules by up to 18 months. Only large primes can absorb the cost, limiting the 3D printing market's reach within smaller tier-two suppliers. Though ASTM and ISO working groups are drafting method-specific standards, global alignment remains a multi-year endeavor.

Other drivers and restraints analyzed in the detailed report include:

- China's 'Made in China 2025' Subsidies for Industrial 3DP Equipment

- Growing Demand for Patient-specific Orthopedic Implants in India

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, the hardware segment drew 60.23% of global revenue, driven by capital outlays for industrial-scale metal fusion, high-temperature polymers, and automated post-processing. Yet, from 2025 to 2030, services outpace with a 25.21% CAGR. Contract manufacturers such as Stratasys Direct Manufacturing, Materialize, and Protolabs leverage multi-site networks to distribute load, allowing customers to prototype and receive production ISO-13485 parts within ten days. The services boom lowers financial barriers, expanding the user base of the 3D printing market. By contrast, software suppliers evolve more slowly, hampered by fragmented data formats; however, as 3MF overtakes STL, opportunity emerges for cloud-native build-prep tools that embed lattice generators and cost estimation engines.

The 3D printing market benefits when OEMs bundle subscription-based machine leasing with remote monitoring. New entrants mimic copier leasing, offering print-per-hour models that fold maintenance, calibration, and powder refills into a single invoice. This hybrid approach blurs the line between hardware and services, smoothing revenue streams across macroeconomic cycles.

Industrial platforms command 72.14% of 2024 spending as automotive, energy, and aerospace segments transition from prototype tooling to serial production. Multi-laser powder bed fusion now reaches 150 cc/hour deposition for Inconel, cracking a historical speed ceiling. Manufacturers exploit topology-optimized brackets that drop weight by 40% and consolidate assembly steps. The 3D printing market gains credibility because first-time pass rates approach those of CNC milling when build chambers incorporate powder recycling and real-time melt-pool analytics.

Desktop systems, while smaller in revenue, experience a renaissance marked by Bambu Lab's high-speed CoreXY architectures delivering 20,000 mm/s2 accelerations. Universities deploy clusters of sub-USD 1,000 units to teach design-for-additive principles, forming a talent pipeline for industrial roles. Dentists and jewelers adopt LCD resin printers that achieve 30 µm XY resolution, widening the 3D printing market beyond engineering offices.

The 3D Printing Market Report is Segmented by Component (Hardware, Software, and Services), Printer Type (Industrial 3D Printer and Desktop 3D Printer), Technology (Vat Photopolymerization [SLA, DLP], and More), Material Type (Polymers, Metals and Alloys, and More), End-User Industry (Automotive, Aerospace and Defense, and More), and Geography.

Geography Analysis

North America holds 41.68% of global spending, anchored by Fortune 500 adopters and a tight cluster of powder atomizers, software vendors, and contract manufacturers. America Makes funnels grant dollars toward powder recycling and real-time monitoring, closing material data sheet gaps. The U.S. Navy's layered approach to additive manufacturing, from shipboard FDM units to depot-level DED repair, creates a structured demand pipeline. GE Aerospace's USD 1 billion commitment to new additive facilities cements supply security for aviation alloys metal-am.com. As export controls tighten on strategic metals, onshore powder production further differentiates the North American 3D printing market.

Asia Pacific is forecast to expand at a 26.47% CAGR, influenced by China's equipment subsidies and India's medical adoption. Beijing's 90% digital R&D penetration target by 2027 underpins broad-based demand for design suites and simulation software. Japan leverages additive manufacturing for micro-resolution ceramic components used in semiconductor lithography. South Korea funds joint university-industry labs to perfect metal binder jetting of copper for EV motors, supporting domestic electrification goals. In Southeast Asia, Singapore's Advanced Remanufacturing and Technology Centre incubates hybrid additive-subtractive cells that appeal to marine and oil-rig maintenance.

Europe remains a powerhouse for both research and production. Airbus, Safran, and MTU Aero Engines co-lead standard-development consortia, ensuring geometric tolerances align across OEMs. German automakers deploy binder-jet stainless components into dashboard support brackets, citing faster cycle times than stamped alternatives at volumes under 20,000 units annually. Scandinavia seeks circular-economy credentials by integrating recycled powder streams. Eastern Europe's contract manufacturers attract overflow orders from Western OEMs, adding to the heterogeneity of the regional 3D printing market.

Middle East oxygenates growth through energy and healthcare programs. Saudi Aramco trials corrosion-resistant lattice inserts for desalination valves exposed to high-salinity brines. UAE hospitals partner with universities to print anatomical models for complex cardiac surgeries. Africa shows pilot activity in prosthetics and spare parts, though infrastructure gaps persist. Latin America cultivates in-house tooling for consumer appliance plants; Brazil's SENAI network teaches design-for-additive curricula, prepping a future workforce.

- Stratasys Ltd

- 3D Systems Corporation

- EOS GmbH

- General Electric Company (GE Additive)

- Hewlett Packard Inc.

- Desktop Metal Inc.

- Materialise NV

- SLM Solutions Group AG

- Velo3D Inc.

- Renishaw plc

- Ultimaker B.V.

- Formlabs Inc.

- Markforged Holding Corp.

- Nano Dimension Ltd.

- Prodways Group

- Tritone Technologies

- Carbon Inc.

- HP Inc. (Personalization division)

- UnionTech Inc.

- Sisma S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-funded additive manufacturing hubs in North America

- 4.2.2 Surging metal AM adoption for on-demand aerospace spare-parts in Europe

- 4.2.3 China's 'Made in China 2025' subsidies for industrial 3DP equipment

- 4.2.4 Growing demand for patient-specific orthopedic implants in India

- 4.2.5 Energy-sector shift to AM for lightweight lattice heat-exchangers in GCC

- 4.2.6 Rapid tooling needs driven by EV platform proliferation globally

- 4.3 Market Restraints

- 4.3.1 Persistent certification bottlenecks for flight-critical parts

- 4.3.2 Volatility in high-performance metal powder pricing

- 4.3.3 Limited printable material palette for food-contact applications

- 4.3.4 Inter-operability gaps between AM software and legacy PLM suites

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of COVID-19 on the Market

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Printer Type

- 5.2.1 Industrial 3D Printer

- 5.2.2 Desktop 3D Printer

- 5.3 By Technology

- 5.3.1 Vat Photopolymerization (SLA, DLP)

- 5.3.2 Powder Bed Fusion (SLS, SLM, EBM)

- 5.3.3 Material Extrusion (FDM, FFF)

- 5.3.4 Material Jetting

- 5.3.5 Binder Jetting

- 5.3.6 Directed Energy Deposition

- 5.3.7 Sheet Lamination

- 5.4 By Material

- 5.4.1 Polymers

- 5.4.2 Metals and Alloys

- 5.4.3 Ceramics

- 5.4.4 Composites

- 5.4.5 Other Materials

- 5.5 By Application

- 5.5.1 Prototyping

- 5.5.2 Manufacturing / Production Parts

- 5.5.3 Tooling and Fixtures

- 5.5.4 Research and Development

- 5.5.5 Personalized Consumer Products

- 5.6 By End-user Industry

- 5.6.1 Automotive

- 5.6.2 Aerospace and Defense

- 5.6.3 Healthcare and Dental

- 5.6.4 Consumer Electronics

- 5.6.5 Construction and Architecture

- 5.6.6 Energy (Oil and Gas, Power)

- 5.6.7 Food and Culinary

- 5.6.8 Education and Research Institutes

- 5.6.9 Other Industries

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.2 Latin America

- 5.7.2.1 Mexico

- 5.7.2.2 Brazil

- 5.7.2.3 Argentina

- 5.7.2.4 Rest of Latin America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Middle East and Africa

- 5.7.4.1 United Arab Emirates

- 5.7.4.2 Saudi Arabia

- 5.7.4.3 South Africa

- 5.7.4.4 Rest of Middle East and Africa

- 5.7.5 Asia-Pacific

- 5.7.5.1 China

- 5.7.5.2 Japan

- 5.7.5.3 South Korea

- 5.7.5.4 India

- 5.7.5.5 Rest of Asia-Pacific

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Stratasys Ltd

- 6.4.2 3D Systems Corporation

- 6.4.3 EOS GmbH

- 6.4.4 General Electric Company (GE Additive)

- 6.4.5 Hewlett Packard Inc.

- 6.4.6 Desktop Metal Inc.

- 6.4.7 Materialise NV

- 6.4.8 SLM Solutions Group AG

- 6.4.9 Velo3D Inc.

- 6.4.10 Renishaw plc

- 6.4.11 Ultimaker B.V.

- 6.4.12 Formlabs Inc.

- 6.4.13 Markforged Holding Corp.

- 6.4.14 Nano Dimension Ltd.

- 6.4.15 Prodways Group

- 6.4.16 Tritone Technologies

- 6.4.17 Carbon Inc.

- 6.4.18 HP Inc. (Personalization division)

- 6.4.19 UnionTech Inc.

- 6.4.20 Sisma S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

3D列印市場:按組件、技術、材料、應用和銷售管道-2026-2032年全球預測

3D列印市場:按組件、技術、材料、應用和銷售管道-2026-2032年全球預測 人工智慧在3D列印領域的應用:全球產業分析、市場規模、市場佔有率及2026年至2033年預測(按組件、技術、應用、最終用戶、國家和地區分類)

人工智慧在3D列印領域的應用:全球產業分析、市場規模、市場佔有率及2026年至2033年預測(按組件、技術、應用、最終用戶、國家和地區分類) 3D 列印:材料和設備機會、趨勢和市場

3D 列印:材料和設備機會、趨勢和市場 3D列印市場規模、佔有率、趨勢和預測:按技術、工藝、材料、產品、應用、最終用戶和地區分類,2026-2034年

3D列印市場規模、佔有率、趨勢和預測:按技術、工藝、材料、產品、應用、最終用戶和地區分類,2026-2034年 FDM(熔融沈積成型)3D列印市場規模、佔有率和趨勢分析報告:按印表機類型、應用、最終用途、地區和細分市場預測(2026-2033年)3D列印石膏市場:按技術、材料、客製化類型、應用和最終用戶分類-2026年至2032年全球市場預測

FDM(熔融沈積成型)3D列印市場規模、佔有率和趨勢分析報告:按印表機類型、應用、最終用途、地區和細分市場預測(2026-2033年)3D列印石膏市場:按技術、材料、客製化類型、應用和最終用戶分類-2026年至2032年全球市場預測 教育領域3D列印市場規模、佔有率和成長分析:按產品類型/服務類型、應用、重點領域、組織結構、分銷管道和地區分類-2026-2033年產業預測3D列印市場規模、佔有率和趨勢分析報告:按組件、印表機類型、技術、軟體、應用、產業、材料、地區和細分市場預測(2026-2033年)3D列印機器人市場:依機器人類型、技術、應用、最終用戶和通路分類-2026-2032年全球市場預測

教育領域3D列印市場規模、佔有率和成長分析:按產品類型/服務類型、應用、重點領域、組織結構、分銷管道和地區分類-2026-2033年產業預測3D列印市場規模、佔有率和趨勢分析報告:按組件、印表機類型、技術、軟體、應用、產業、材料、地區和細分市場預測(2026-2033年)3D列印機器人市場:依機器人類型、技術、應用、最終用戶和通路分類-2026-2032年全球市場預測 2026年全球立體立體光固成型3D列印技術市場報告

2026年全球立體立體光固成型3D列印技術市場報告