|

市場調查報告書

商品編碼

1640469

中東潤滑油:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Middle-East Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

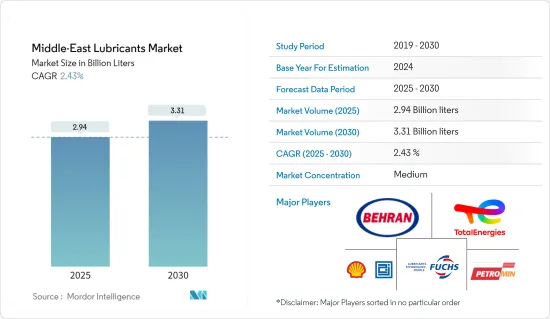

中東潤滑油市場規模預估在2025年為29.4億公升,預計2030年達到33.1億公升,預測期間(2025-2030年)的複合年成長率為2.43%。

由於新冠疫情爆發,製造業受到嚴重影響,導致2020年潤滑油使用量下降。然而,隨著許多建築計劃和其他工業活動的回暖,市場在 2021 年出現復甦。預計未來幾年這一趨勢仍將保持積極態勢。過去兩年,汽車和工程產品銷售的成長推動了市場復甦。

沙烏地阿拉伯、伊朗和阿拉伯聯合大公國的工業成長以及高性能潤滑油的使用增加是推動所調查市場成長的主要驅動力。

另一方面,高性能潤滑油的高成本預計會阻礙市場的成長。

合成潤滑油和生物基潤滑油的發展預計將在未來提供市場機會。

預計沙烏地阿拉伯將成為最大的潤滑油市場,並預計在預測期內實現最高的複合年成長率。

中東潤滑油市場趨勢

汽車產業佔市場主導地位

- 潤滑劑通常用於減少磨損、防止腐蝕並保持引擎內部平穩運轉。

- 高燃油經濟性機油因其具有防止漏油、防止油卡等特殊性能而需求很大。

- 大多數輕型和重型柴油和汽油引擎使用黏度等級為 10W40 和 15W40 的油,而 15W50 和 20W50 等多級油通常用於航空引擎。

- 汽車的平均車齡年限多年來一直在穩步成長,這為售後補油市場帶來了機會。新興經濟體中乘用車平均使用年限的提高和城市人口的增加預計將推動運輸潤滑油市場的發展。

- 汽車工業對一個國家的社會經濟發展至關重要。當地汽車行業專家表示,儘管全球電動車銷量上升,但內燃機 (ICE) 汽車預計在未來 15 至 20 年內仍將主導沙烏地阿拉伯汽車市場。

- 主導沙烏地阿拉伯汽車產業的主要企業包括豐田(佔有 30% 的市場佔有率)、現代和起亞(佔有 26% 的市場佔有率)以及雷諾-日產-三菱(佔有 9% 的市場佔有率)。通用汽車、福特和飛雅特克萊斯勒汽車公司佔據剩餘的佔有率。

- 沙烏地阿拉伯正在尋求汽車產業在地化並增加投資機會,以實現其國家汽車戰略的目標,根據該國的「2030 願景」目標發展本地製造能力。

- 過去幾年,伊朗汽車市場呈現上漲趨勢,國內生產的需求增加。例如,根據OICA預測,2022年伊朗汽車產量將成長19%,達到106.4萬輛乘用車,而2021年約為89.4萬輛。

- 國際汽車工業組織(OICA)將伊朗2022年汽車產量增幅排在全球第六位。

- 歐洲汽車工業協會(ACEA)也將伊朗評為2022年全球第11大汽車製造國。

- 由於生產和銷售需求增加,阿拉伯聯合大公國汽車市場車輛註冊量正在增加。

- 據業內人士透露,2023年1至9月,全國汽車註冊量為193,698輛,較去年同期成長20.2%。

- 此外,預計2022年全國汽車市場新車銷量將超過40萬輛,與前一年同期比較成長10%。在該國人口成長和收入提高的推動下,預計這種成長將持續下去。

- 因此,預計上述因素將在預測期內促進該地區所研究市場的成長。

沙烏地阿拉伯預計將實現快速成長

- 沙烏地阿拉伯是中東最大的經濟體。沙烏地阿拉伯的經濟主要依賴石油工業。

- 沙烏地阿拉伯是海灣合作理事會最大的汽車市場之一。乘用車約佔該地區汽車市場的80%。

- 沙烏地阿拉伯正在加強其電力部門(發電、輸電、配電和智慧電網)的能力,以有效滿足國內和商業消費者日益成長的電力需求,並支持該國能源結構的多樣化。 。

- 據能源部稱,到2030年,沙烏地阿拉伯在電力和可再生能源計劃上的支出預計將達到2,930億美元。此外,2021 年 12 月,沙烏地阿拉伯能源部長宣布計畫在 2030 年在能源發行上投入 380 億美元。

- 沙烏地阿拉伯已成為快速成長的能源消費國。隨著國家對電力的需求不斷增加,發電基礎設施也不斷增加。據估計,到 2040 年,該國需要將發電能力提高到 160GW,才能滿足不斷成長的需求。為實現這一目標,政府計劃每年在發電方面投資約 50 億美元,在配電和輸電 (D&T) 方面投資 40 億美元。該國的可再生能源發電計畫旨在2023年將可再生能源發電量提高到950萬千瓦。

- 持續潤滑對於軸承、齒輪和鏈條的壽命至關重要。與其他機械系統一樣,食品和飲料工廠中的運動部件需要適當的潤滑才能發揮最佳功能。污染、濕氣、高溫和潮濕都會對軸承、鏈條和齒輪的壽命構成威脅。沙烏地阿拉伯正在大力投資金屬產業。根據世界鋼鐵協會預測,2023年沙烏地阿拉伯粗鋼產量將比2022年成長約0.8%,產量約990萬噸。

- 2023年12月,沙國政府宣布將投資約120億美元用於鋼鐵計劃,增加鋼鐵產量,滿足國內需求的大幅成長。預計計劃總產能約620萬噸。

- 雀巢計劃於 2025 年建立一座製造廠,初期投資為 3.75 億沙烏地里亞爾(9,972 萬美元),隨後建立一個擁有研發項目的區域中心,以及首個面向中小型和小型新興企業的中心。和新創培養箱。

- 石油和天然氣探勘使用大量潤滑劑。預計這些因素將在預測期內溫和推動阿拉伯聯合大公國市場的發展。

中東潤滑油產業概況

中東潤滑油市場呈現細分化。主要企業(不分先後順序)包括 TotalEnergies、Petromin、Aljomaih、殼牌潤滑油公司 (JOSLOC)、Behran Oil Co. 和 FUCHS。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 沙烏地阿拉伯、伊朗和阿拉伯聯合大公國的產業成長

- 擴大高性能潤滑劑的使用

- 其他促進因素

- 限制因素

- 高性能潤滑油成本高

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 監理政策分析

第5章 市場區隔(市場規模(基於數量))

- 團體

- 第一組

- 第二組

- 第三組

- 第四組 (PAO)

- 環烷

- 基料

- 生物性潤滑劑

- 礦物油潤滑劑

- 合成潤滑油

- 半合成潤滑油

- 產品類型

- 機油

- 傳動液和液壓油

- 金屬加工油

- 通用工業用油

- 齒輪油

- 潤滑脂

- 加工油

- 其他產品類型(渦輪機油、冷凍機油、航空油、船舶油、變壓器油)

- 最終用戶產業

- 發電

- 汽車及其他運輸設備

- 重型機械

- 飲食

- 冶金與金屬加工

- 化學製造

- 其他終端用戶產業(海洋、紡織、製造、石油和天然氣)

- 地區

- 沙烏地阿拉伯

- 伊朗

- 伊拉克

- 阿拉伯聯合大公國

- 科威特

- 其他中東地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Aljomaih And Shell Lubricating Oil Company Limited

- AMSOIL INC.

- Behran Oil Co.

- Emarat

- Exxon Mobil Corporation

- FUCHS

- GP Global MAG LLC

- GULF OIL Middle East Limited(Gulf Oil International Ltd.)

- Idemitsu Kosan Co., Ltd.

- IRANOL(LLP)

- Lubrex FZC

- Pars Oil Company

- Petromin

- Saudi Arabian Oil Co.

- Sepahan Oil Company

- TotalEnergies

第7章 市場機會與未來趨勢

- 合成潤滑油和生物基潤滑劑的開發

- 其他機會

The Middle-East Lubricants Market size is estimated at 2.94 billion liters in 2025, and is expected to reach 3.31 billion liters by 2030, at a CAGR of 2.43% during the forecast period (2025-2030).

Due to the COVID-19 outbreak, the manufacturing industry was severely affected, and this resulted in a decrease in the use of lubricants in 2020. However, with the recovery of many construction projects and other industrial activities, the market saw a recovery phase in the year 2021. It is expected to see a positive trend in the forecasted years. An increase in automotive sales and engineering goods has been leading the market recovery over the last two years.

The industrial growth in Saudi Arabia, Iran, and the United Arab Emirates and the growing usage of high-performance lubricants are the major driving factors augmenting the growth of the market studied.

On the flip side, costlier high-performance lubricants are expected to hinder the growth of the market.

Developments in synthetic and bio-based lubricants are projected to act as an opportunity for the market in the future.

Saudi Arabia emerged as the largest market for lubricants and is expected to register the highest CAGR during the forecast period.

Middle East Lubricants Market Trends

Automotive Sector to Dominate the Market

- Lubricants are typically used for applications such as wear reduction, corrosion protection, and ensuring smooth operation of the engine internals.

- High-mileage engine oils are experiencing great demand owing to specific properties, such as oil leak prevention and reduction in oil burn-off.

- Most light and heavy vehicle diesel and gasoline engines use 10W40 and 15W40 viscosity grade oils, while multi-grade oils, such as 15W50 and 20W50, are commonly used for aircraft engines.

- The average vehicle age has been increasing at a constant rate over the years, which is an opportunity in terms of the aftermarket refill market. The increasing average age of passenger cars and the growing urban population in developing countries is expected to drive the market for lubricants in transportation.

- The automotive industry is essential to the country's socio-economic development. According to some local automotive industry experts, despite the growing electric vehicle sales worldwide, Saudi Arabia expects internal combustible engines (ICE) vehicles to make up the majority of cars driven in for the next 15-20 years.

- Some of the major players controlling the automotive industry in the country include Toyota, with a 30% share, followed by Hyundai and KIA, with 26%, and Renault-Nissan-Mitsubishi, with 9%. General Motors, Ford, and Fiat Chrysler Automobiles comprise the remaining share.

- Saudi Arabia aims to localize the automotive sector and increase investment opportunities to achieve the national strategy's objectives for the industry in developing local manufacturing capabilities in line with the goals of the Kingdom's Vision 2030.

- The Iran automotive market has witnessed a rise over the historic period, with demand for production increasing in the country. For instance, according to the OICA, car manufacturing in Iran increased by 19% in 2022, as the country manufactured 1.064 million vehicles in 2022, while the passenger vehicles produced were around 894,000 units in 2021.

- The International Organization of Motor Vehicle Manufacturers (known as OICA) ranked Iran sixth in the world in terms of car manufacturing growth in 2022.

- Also, as per the European Automobile Manufacturers' Association (ACEA), the organization ranked Iran as the world's 11th largest automaker in 2022.

- The United Arab Emirates automotive market has been experiencing a rise in vehicle registrations over the current period, with demand in production and sales increasing in the country.

- As per industry sources, the country's automotive vehicle registration in the period January to September 2023 stood at 193,698, up 20.2% in comparison to the same period in the previous year.

- Moreover, in 2022, the country's car market sold over 400,000 new cars, representing a 10% increase over the previous year. This growth is expected to continue in the coming years, driven by the country's growing population and rising incomes.

- Thus, the factors above are expected to augment the growth of the market studied in the region during the forecast period.

Saudi Arabia is Expected to Experience a Surge in Growth

- Saudi Arabia is the largest economy in the Middle East region. Saudi Arabia's economy is mainly dependent on the oil industry.

- Saudi Arabia is one of the largest automotive markets in the GCC. Passenger cars account for approximately 80% of the region's automotive market.

- Saudi Arabia is enhancing the capacity of its power sector (electricity generation, transmission, distribution, and smart grid) to meet increasing demand efficiently from residential and commercial consumers for electricity and to support the diversification of its domestic energy mix.

- According to the Ministry of Energy, Saudi Arabia's spending on power and renewable energy projects is expected to reach USD 293 billion by 2030. Additionally, in December 2021, Saudi Arabia's Energy Minister announced the country's plan to spend USD 38 billion on energy distribution by 2030.

- Saudi Arabia emerged as a rapidly growing energy consumer. With the increasing demand for electricity in the country, the power generation infrastructure has been growing. It is estimated that the country is required to increase its power generation capacity to 160 GW by 2040 to fulfill its increasing demand. To achieve this, the government is planning to make an annual investment of around USD 5 billion in generation and USD 4 billion in distribution (D&T). The National Renewable Energy Program in the country aims to increase the generation of renewable energy to 9.5 GW by 2023.

- Consistent lubrication is vital to the life of bearings, gears, and chains. Like any mechanical system, moving parts in a food and beverage plant need proper lubrication to function optimally. Contamination, moisture, high temperatures, and humidity are all threats to bearing, chain, and gear service life. Saudi Arabia is heavily investing in metal industries. According to the World Steel Association, Saudi Arabia's crude steel production in 2023 observed an increase of about 0.8% as compared to 2022 and produced approximately 9.9 million metric tons of steel.

- In December 2023, the Saudi Arabian government announced to investment of about USD 12 billion in steel projects to increase steel production and meet the significant growth in domestic demand. The project is planned to have a total production capacity of about 6.2 million tons.

- Nestle has announced an initial investment of SAR 375 million (USD 99.72 million) with the establishment of a manufacturing plant in 2025, followed by a regional center with a research and development program and its first business incubator for small and medium-sized companies and start-ups.

- A significant amount of lubricants are used in oil and gas exploration. These factors are expected to drive the market slowly over the forecast period in the United Arab Emirates.

Middle East Lubricants Industry Overview

The Middle-East lubricants market is fragmented. The major companies (in no particular order) include TotalEnergies, Petromin, Aljomaih, Shell Lubricating Oil Company (JOSLOC), Behran Oil Co., and FUCHS, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Industrial Growth in Saudi Arabia, Iran, and the United Arab Emirates

- 4.1.2 Growing Usage of High-performance Lubricants

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Costlier High Performance Lubricants

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Regulatory Policy Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Group

- 5.1.1 Group I

- 5.1.2 Group II

- 5.1.3 Group III

- 5.1.4 Group IV (PAO)

- 5.1.5 Naphthenics

- 5.2 Base Stock

- 5.2.1 Bio-based Lubricant

- 5.2.2 Mineral Oil Lubricant

- 5.2.3 Synthetic Lubricant

- 5.2.4 Semi-synthetic Lubricant

- 5.3 Product Type

- 5.3.1 Engine Oil

- 5.3.2 Transmission and Hydraulic Fluid

- 5.3.3 Metalworking Fluid

- 5.3.4 General Industrial Oil

- 5.3.5 Gear Oil

- 5.3.6 Greases

- 5.3.7 Process oils

- 5.3.8 Other Product Types (Turbine oils, Refrigeration oils, Aviation oils, Marine oils, and Transformer oils)

- 5.4 End-user Industry

- 5.4.1 Power Generation

- 5.4.2 Automotive and Other Transportation

- 5.4.3 Heavy Equipment

- 5.4.4 Food and Beverage

- 5.4.5 Metallurgy and Metalworking

- 5.4.6 Chemical Manufacturing

- 5.4.7 Other End-user Industries (Marine, Textiles, Manufacturing, and Oil and gas)

- 5.5 Geography

- 5.5.1 Saudi Arabia

- 5.5.2 Iran

- 5.5.3 Iraq

- 5.5.4 United Arab Emirates

- 5.5.5 Kuwait

- 5.5.6 Rest of Middle-East

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aljomaih And Shell Lubricating Oil Company Limited

- 6.4.2 AMSOIL INC.

- 6.4.3 Behran Oil Co.

- 6.4.4 Emarat

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 FUCHS

- 6.4.7 GP Global MAG LLC

- 6.4.8 GULF OIL Middle East Limited (Gulf Oil International Ltd.)

- 6.4.9 Idemitsu Kosan Co., Ltd.

- 6.4.10 IRANOL (LLP)

- 6.4.11 Lubrex FZC

- 6.4.12 Pars Oil Company

- 6.4.13 Petromin

- 6.4.14 Saudi Arabian Oil Co.

- 6.4.15 Sepahan Oil Company

- 6.4.16 TotalEnergies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Developments in Synthetic and Bio-based Lubricants

- 7.2 Other Opportunities

固態/乾潤滑劑:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

固態/乾潤滑劑:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 潤滑油 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

潤滑油 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 水性潤滑油市場規模、佔有率、成長分析、按產品類型、分銷管道、按地區 - 產業預測,2025-2032 年

水性潤滑油市場規模、佔有率、成長分析、按產品類型、分銷管道、按地區 - 產業預測,2025-2032 年 手術潤滑劑市場:按類型、應用和最終用戶分類 - 2025-2030 年全球預測

手術潤滑劑市場:按類型、應用和最終用戶分類 - 2025-2030 年全球預測 潤滑油市場:依基礎油、產品、最終用途產業、通路分類 - 2025-2030 年全球預測

潤滑油市場:依基礎油、產品、最終用途產業、通路分類 - 2025-2030 年全球預測 精加工潤滑油的市場規模:基礎油,各產品類型,各終端用戶,各地區,範圍及預測

精加工潤滑油的市場規模:基礎油,各產品類型,各終端用戶,各地區,範圍及預測 到 2030 年潤滑油分散黏度調節劑市場預測:按類型、配方、分銷管道、應用、最終用戶和地區進行的全球分析

到 2030 年潤滑油分散黏度調節劑市場預測:按類型、配方、分銷管道、應用、最終用戶和地區進行的全球分析 中美洲潤滑油市場規模和預測以及區域佔有率、趨勢和成長機會分析報告範圍:按基礎油、產品類型、最終用途和國家/地區

中美洲潤滑油市場規模和預測以及區域佔有率、趨勢和成長機會分析報告範圍:按基礎油、產品類型、最終用途和國家/地區 拉絲潤滑劑市場:按類型和進程內應用分類 - 2025-2030 年全球預測

拉絲潤滑劑市場:按類型和進程內應用分類 - 2025-2030 年全球預測 豆油基潤滑油市場:按產品、最終用戶分類 - 全球預測 2025-2030 年

豆油基潤滑油市場:按產品、最終用戶分類 - 全球預測 2025-2030 年