|

市場調查報告書

商品編碼

1640501

中東和非洲穿戴式感測器市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Middle East And Africa Wearable Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

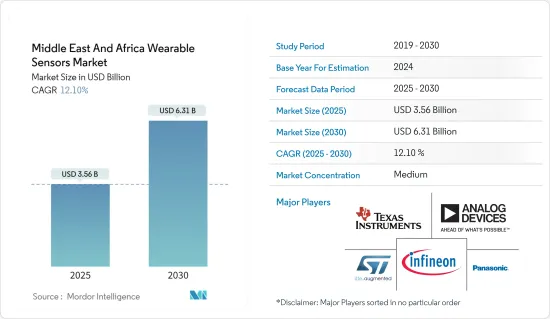

中東和非洲的穿戴式感測器市場規模預計在 2025 年為 35.6 億美元,預計到 2030 年將達到 63.1 億美元,預測期內(2025-2030 年)的複合年成長率為 12.1%。

由於現代技術和小型化電路的發展,穿戴式感測器在健康監測系統等數位系統中越來越受歡迎。穿戴式技術通常包含感測器和無線連接,允許用戶監控、追蹤和分析資料。腕帶、眼鏡、耳機和智慧型手機等各種配件都與這些穿戴式感測器系統結合。

關鍵亮點

- 家用電子電器產品支出的增加、生活方式的改善和都市化進程的加快,正在推動人們健康和安全意識的增強。隨著可支配收入的增加,智慧腕帶、智慧型手錶、健身追蹤器、 VR頭戴裝置、活動追蹤器、運動手錶、醫療應用、企業和工業應用等設備越來越受歡迎。 2023 年 6 月,Uniccon Group 在 2023 年 GITEX Africa 展會上推出了備受期待的VR頭戴裝置。

- 據沙烏地貨幣管理局稱,預計沙烏地阿拉伯私人消費將在 2022 年第一季成長至3,433.74 億沙烏地里亞爾(915.54 億美元),高於2020 年第四季的3335.55 億沙烏地里亞爾(889.36億美元)。此外,根據經合組織的預測,以色列2022年經濟成長率為4.9%,2023年將為4%。

- 預測期內推動穿戴式感測器市場發展的關鍵因素之一是老年人口的增加。未來幾十年沙烏地阿拉伯老齡人口將迅速成長。

- 根據聯合國預測,沙烏地阿拉伯老年人口比例將從2017年的5.6%成長至2050年的22.9%。此外,根據聯合國人口基金的數據,埃及60 歲及以上人口預計將在2020 年至2050 年間增加一倍以上,從840 萬人(佔總人口的8%)增加到2,200 萬(佔總人口的14% )。

- 現今市場充滿了智慧互聯產品,而且數量還在快速成長。實現正確的感測器資料和資訊交流的首要條件是標準化。有幾家公司正在製定感測器通訊標準。

- OGC 感測器網路支援 (SWE) 計畫滿足了高度複雜和基礎應用對改進感測器連接的需求。借助 SWE 標準,使用 OGC 和其他標準的數千個地理空間應用程式可以輕鬆合併這些資料。感測器通訊缺乏通用標準也帶來了互通性問題。

- 隨著消費者對智慧型穿戴裝置的追求日益成長,裝置的價格也隨之上漲,零件成本也不斷上升,限制了市場普及。智慧型手錶和健身追蹤器採用低成本組件,吸引了大量消費者的注意。然而,隨著技術的進步,其他設備如鞋類、眼鏡產品和內衣產品價格高昂,採用率低。目前大多數穿戴式科技價格較高,對市場採用產生了負面影響。

- 俄羅斯和烏克蘭之間持續的衝突可能會對電子產業產生重大影響。競爭已經加劇了影響該行業一段時間的半導體供應鏈問題和晶片短缺問題。這些影響可能表現為鎳、鈀、銅、鈦、鋁和鐵礦石等主要原料的價格波動,導致材料短缺。這被認為對穿戴式感測器的生產造成了阻礙。

中東和非洲穿戴式感測器市場趨勢

醫療領域預計將顯著成長

- 穿戴式感測器廣泛應用於醫療領域。穿戴式感測器附著在患者的身上,用於密切監測患者的生理狀況。穿戴式醫療感測器監測患者的生命徵象(例如體溫、心率、血壓、血氧飽和度)。隨著穿戴式生命徵象感測器和位置標籤的興起,各種感測器在醫療應用中的出現正獲得發展勢頭,這些感測器可以即時持續追蹤醫護人員和患者的狀況和位置。

- 2023年10月,華為在阿拉伯聯合大公國推出了全新智慧型手錶、freebuds、智慧眼鏡和MatePad系列,開創了時尚、注重健康和運動的穿戴式設備的新時代。華為Watch GT 4是熱門智慧型手錶系列的新成員,高階的華為手錶Ultimate Design,高傳真TWS耳機華為Freebuds Pro 3,智慧眼鏡華為Eyewear 2,以及光干擾等多款新品即將發表的還有華為MatePad 11吋Paper Matte版、MatePad 11.5吋Paper Matte版等多款新品,噪音降低97%,實現如紙般閱讀、書寫體驗。

- 根據 AppDynamics 2022 年的一項研究(調查了全球超過 12,000 名消費者),阿拉伯聯合大公國的大多數人計劃在未來 12 個月內購買穿戴式健康技術或應用程式。調查發現,88% 的海灣受訪者打算在 2023 年使用 Fitbit 和智慧型手錶等醫療穿戴裝置。此外,約 90% 的阿拉伯聯合大公國受訪者希望透過手錶或其他穿戴式裝置獲取心率、血壓、心律、體力活動和呼吸頻率。阿拉伯聯合大公國的受訪者表示,他們相信穿戴式科技可以改變個人健康和公共健康。

- 這個市場正在見證企業之間的合作與協作,利用彼此的能力來開發創新的整合解決方案。 2023 年 11 月,提供個人化、臨床級健康洞察的全球知名手錶品牌 LifeQ 與 AAIC Investment 合作。此消息由 LifeQ 執行長兼聯合創始人勞倫斯 (Laurie) 奧利維爾 (Laurence (Laurie) Olivier) 宣布。 AAIC Investment 專注於非洲醫療保健領域快速發展的公司,並致力於改善非洲的醫療保健。

- 為了滿足對穿戴式醫療感測器的激增需求,2022年3月,持續健康監測和臨床智慧公司BioIntelliSense與穆巴達拉投資公司旗下的綜合醫療網路Mubadala Health建立了策略夥伴關係。合作夥伴關係。此次合作將把 BioIntelliSense 的創新遠距照護技術融入穆巴達拉醫療的持續照護模式,以推動更高效的臨床工作流程,解鎖資料主導的臨床見解並提供個人化護理。體驗。

- 該地區人們對心臟病、糖尿病、癌症和呼吸系統疾病等健康問題的興趣日益濃厚,這可能會導致穿戴式感測器的採用率增加。例如,根據沙烏地阿拉伯衛生署的數據,到2026年,預計沙烏地阿拉伯成年人口的24.3%將患有糖尿病。預計這些因素將推動市場的成長。

沙烏地阿拉伯佔主要市場佔有率

- 穿戴式感測器在沙烏地阿拉伯正在經歷強勁成長。穿戴式科技正擴大融入全國各地的日常生活和各個行業,其應用包括健身追蹤、醫療監測和工業應用。根據世界衛生組織預測,2022年沙烏地阿拉伯的衛生支出總額將達607億美元。報告稱,預計2027年沙烏地阿拉伯醫療保健支出將達771億美元。

- 對塑造體形、增強身體免疫力和控制壓力的關注推動了健身類穿戴裝置的流行度激增。智慧型手錶作為使用者身體的延伸和智慧型手機的配件,發揮著至關重要的作用。這些設備可以全天佩戴並充當用戶的智慧助手,幫助他們主動管理健康,同時探索身臨其境型的應用體驗。

- 2022年3月,華為與沙烏地阿拉伯全民運動聯合會(SFA)聯手推廣專為跑者設計的先進穿戴式裝置。沙烏地阿拉伯足球協會舉辦這場馬拉松賽事是為了促進公民健康,提高公民的體育活動水平,並符合沙烏地阿拉伯 2030 願景目標。

- 結果,超過 10,000 名跑者參加了首屆馬拉鬆比賽。華為向所有馬拉松參賽者贈送了價值 200 沙烏地里亞爾的代金券,可透過華為官方網站購買。其中包括令人興奮的HUAWEI WATCH GT系列,其中包括該公司首款專業跑步手錶HUAWEI WATCH GT Runner,它提供廣泛的健康和幸福感監測功能以及數十款智慧手錶,可幫助用戶提高健身水平。運動模式。這些努力提高了人們對用於監測健康和健身的現代穿戴式感測器的認知,從而促進了市場的成長。

- 該國智慧型手機用戶數量的不斷增加,使得穿戴式裝置的整合成為可能,預計將提供有利可圖的市場成長機會。根據歐盟統計局的數據,2023 年 1 月沙烏地阿拉伯的網路用戶數量為 3,630 萬,高於去年的 3,580 萬。

- 癌症患者接受化療和/或放射線治療來治療其癌症狀況。此外,由於關注健康的人數迅速增加,對穿戴式醫療感測器的需求也在增加。根據世界銀行的數據,到 2050 年,該國人口可能達到 4,510 萬,複合年成長率為 1.02%。預計人口成長將增加該國對醫療保健服務的需求。

中東和非洲穿戴式感測器產業概況

中東和非洲的穿戴式感測器市場是半固體的,其中有幾家主要參與者,例如意法半導體、英飛凌科技股份公司、德州儀器公司和 ADI 公司。公司不斷投資於策略聯盟和產品開發以獲得市場佔有率。

- 2023年11月:小米智慧型手錶Redmi K70系列在阿拉伯聯合大公國獲得TDRA認證。智慧型手錶註冊為短距離智慧型手錶設備。小米子品牌 Redmi 即將推出 Redmi K70 系列,包括 Redmi K70e、Redmi K70 和 Redmi K70 Pro。 Redmi K70e 配備 6.67 吋 OLED 顯示螢幕,刷新率為 120Hz,解析度為 2712 x 1220 像素。

- 2023 年 10 月:Google推出 Pixel Watch 2 ,智慧型手錶,包括心率追蹤和睡眠追蹤。該設備採用光電脈衝光子光譜 (PPG) 感測器,透過在使用者的手腕上照射綠色 LED 燈來測量血液循環。我們也改進了我們的人工智慧演算法,為您提供更準確的心率資料。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第 2 章執行摘要

第3章調查方法

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 價值鏈分析

- 評估宏觀經濟趨勢對市場的影響

第5章 市場動態

- 市場促進因素

- 擁抱最新技術與創新

- 更重視健康與健身

- 市場限制

- 與電子產品相關的高成本

第6章 市場細分

- 按類型

- 溫度

- 壓力

- 成像/光學

- 運動

- 其他感測器

- 按應用

- 健康與福祉

- 安全監控

- 運動與健身

- 其他

- 按國家

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

第7章 競爭格局

- 公司簡介

- STMicroelectronics

- Infineon Technologies AG

- Texas Instruments Incorporated

- Analog Devices

- Panasonic Corporation

- InvenSense Inc.

- NXP Semicondutors

- TE Connectivity Ltd

- Bosch Sensortec GmbH(Robert Bosch GmbH)

- Broadcom Limited

第8章投資分析

第9章:市場的未來

The Middle East And Africa Wearable Sensors Market size is estimated at USD 3.56 billion in 2025, and is expected to reach USD 6.31 billion by 2030, at a CAGR of 12.1% during the forecast period (2025-2030).

Wearable sensors are gaining popularity in digital systems like health monitoring systems due to ongoing developments in modern technologies and miniature circuits. Wearable technology generally includes sensors and wireless connections, allowing users to monitor, track, and analyze data. Various accessories, including wristbands, eyeglasses, headphones, and smartphones, are combined with these wearable sensor systems.

Key Highlights

- Increased spending on consumer electronics, improved lifestyles, and a surge in urbanization have led to a rise in health and safety awareness. With rising disposable incomes, devices like smart wristbands, smartwatches, fitness trackers, VR headsets, activity trackers, sports watches, healthcare applications, and enterprise and industrial applications are gaining tremendous traction. In June 2023, the Uniccon Group launched a highly anticipated VR headset at the GITEX Africa 2023.

- According to the Saudi Arabian Monetary Agency, consumer spending in Saudi Arabia increased to SAR 343,374 million (USD 91.554 billion) in the first quarter of 2022 from SAR 333,555 million (USD 88.936 billion) in the fourth quarter of the previous year. Furthermore, according to the OECD, Israel's economy grew by 4.9% in 2022 and 4% in 2023.

- One significant factor anticipated to drive the wearable sensors market during the forecast period is the growing elderly population. Over the coming decades, Saudi Arabia's aging population will rapidly grow.

- According to UN projections, the senior population in Saudi Arabia will rise from 5.6% in 2017 to 22.9% by 2050. Furthermore, according to the UN Population Fund, Egypt is undergoing a demographic transition as the number of people over 60 is predicted to more than double from 8.4 million (8% of the overall population) to 22 million between 2020-2050 (14%).

- The market is currently flooded with smart, Internet-connected products, and the number is expanding quickly. The primary condition for enabling adequate sensor data and information exchange is standardization. A few businesses have developed standards for sensor communication.

- The OGC's Sensor Web Enablement (SWE) measures satisfy the need for improved sensor connectivity in highly complicated and basic applications. Thousands of geospatial applications that use the OGC or other standards may easily incorporate this data due to the SWE standards. Interoperability problems are also brought on by the absence of universal standards for sensor communication.

- With the growing propensity of consumers toward smart wearables, the prices of instruments are also soaring, along with the increasing cost of components, thereby limiting adoption in the market. Smartwatches and fitness trackers have low-cost components that drive significant attention from consumers. However, with the increase of technology, other devices such as footwear, eyewear, and body wear products are highly priced and have lower adoption rates. Most wearable technologies are currently highly priced, negatively impacting adoption in the market.

- The ongoing conflict between Russia and Ukraine will significantly impact the electronics industry. The competition has already exacerbated the semiconductor supply chain issues and the chip shortage that have affected the industry for some time. The disruption may come in the form of volatile pricing for critical raw materials such as nickel, palladium, copper, titanium, aluminum, and iron ore, resulting in material shortages. This would obstruct the manufacturing of wearable sensors.

Middle East And Africa Wearable Sensors Market Trends

The Healthcare Sector is Expected to Register Significant Growth

- Wearable sensors are widely used in the healthcare sector. They are arranged on a patient's body and can be utilized to closely monitor patients' physiological condition. Wearable medical sensors monitor the patient's vital body signs (for example, temperature, heart rate, blood pressure, and oxygen saturation). The emergence of various sensors in healthcare applications is gaining momentum through the increasing array of wearable vital sign sensors and place tags, which can continuously track healthcare personnel and patient status/ location in real time.

- In October 2023, Huawei entered a new era of stylish, health-focused, and sport-ready wearables by introducing a new line-up of smartwatches, freebuds, smart glasses, and MatePad in the UAE. The range of new devices, including the Huawei Watch GT 4, the new addition to the popular smartwatch series, the high-end Huawei Watch Ultimate Design, Huawei Freebuds Pro 3 high-fidelity TWS earbuds, Huawei Eyewear 2 smart glasses, and the Huawei MatePad 11-inch PaperMatte Edition and MatePad 11.5-inch PaperMatte Edition that offer a paper-like reading and writing with 97% light interference reduction.

- According to a survey published by AppDynamics in 2022 (a study of more than 12,000 consumers worldwide), most people in the UAE bought more wearable health technology or applications in the following 12 months. The survey found that 88% of respondents in the Gulf country intended to use medical wearables, like Fitbit or smartwatches, in 2023. Further, around 90% of respondents in the UAE wanted access to heart rate, blood pressure, heart rhythms, physical activity, and respiratory rate from a watch or other wearable gadget. The UAE respondents said they believed wearable technology could transform both personal and public health.

- The market is witnessing collaborations as companies partner to develop innovative integrated solutions by leveraging each other's capabilities. In November 2023, LifeQ, a company using globally recognized watch brands to generate personalized, clinical-grade health insights, partnered with AAIC Investment. LifeQ co-founder Laurence (Laurie) Olivier, CEO, made the announcement. AAIC Investment focuses on fast-growing companies in Africa's healthcare sector and is deeply committed to improving healthcare in Africa.

- To cater to the upsurge in demand for healthcare wearable sensors, in March 2022, BioIntelliSense, Inc., a continuous health monitoring and clinical intelligence company, announced its strategic collaboration with Mubadala Health, an integrated healthcare network of Mubadala Investment Company. The partnership incorporates BioIntelliSense's innovative remote care technologies with Mubadala Health's continuous care model to drive clinical workflow efficiencies, unlock data-driven clinical insights, and deliver a personalized care experience.

- Increasing health concerns like heart ailments, diabetes, cancer, and respiratory diseases in the region are likely to drive the population toward adopting wearable sensors. For instance, according to the Ministry of Health, Saudi Arabia, 24.3% of the adult population in Saudi Arabia is expected to have diabetes by 2026. Such factors are expected to boost the market's growth.

Saudi Arabia Holds a Significant Market Share

- Wearable Sensors are experiencing significant growth in Saudi Arabia. Wearable technology has become increasingly integrated into daily life and various industries nationwide, utilized for fitness tracking, healthcare monitoring, and industrial applications. According to the WHO, in 2022, Saudi Arabia's expenditure on healthcare totaled USD 60.7 billion. According to the report, the healthcare expenditure of Saudi Arabia in 2027 is expected to reach USD 77.1 billion.

- A dedicated focus on getting in shape, building the body's immunity, and managing stress drives the surge in the popularity of wearables in the fitness category. Smartwatches play a vital role by becoming extensions of the user's body and a smartphone accessory. These devices can be worn all day and work as the user's smart assistant to aid them in actively managing their health while exploring immersive application experiences.

- In March 2022, Huawei and SFA (Saudi Sports for All Federation) joined forces to promote advanced wearable devices designed specifically for runners. The SFA organized a marathon event to promote well-being and increase physical activity levels across the population in line with the Saudi Vision 2030 objectives.

- As a result, more than 10,000 runners participated in the inaugural marathon. Huawei gifted all marathon participants with a 200 SAR voucher to buy anything from the official Huawei website, such as the stunning HUAWEI WATCH GT Series, including the company's first professional running watch, the HUAWEI WATCH GT Runner, which has a wide range of health and well-being monitoring features as well as dozens of sport modes to help users level up their fitness. Such initiatives spread awareness about the latest wearable sensors to monitor health and fitness, thereby driving the growth of the market.

- The country's increasing number of smartphone users is expected to offer lucrative market growth opportunities as they enable wearable device integration. According to Eurostat, the number of internet users in Saudi Arabia in January 2023 was 36.3 million users, up from 35.8 million users in the previous year.

- Cancer patients are undergoing chemotherapy and radiotherapy as therapeutic treatments for their cancer conditions. Demand for wearable medical sensors is also increasing due to the rapidly growing population concerned about health conditions. According to the World Bank, the country's population may reach 45.1 million by 2050, with a 1.02% average annual growth. This increase in population is anticipated to boost the demand for healthcare services in the country.

Middle East And Africa Wearable Sensors Industry Overview

The Middle East and African wearable sensor market is semi-consolidated, with the presence of a few significant companies like STMicroelectronics, Infineon Technologies AG, Texas Instruments Incorporated, and Analog Devices. The companies continuously invest in strategic collaborations and product developments to gain market share.

- November 2023: The upcoming Redmi K70 series, a Xiaomi Smartwatch, surfaced on the UAE's TDRA certification. Bearing the model code M2320W1, the smartwatch was registered as a short-range smartwatch device. Xiaomi's subbrand Redmi plans to launch the Redmi K70 Series, which consists of the Redmi K70e, Redmi K70, and Redmi K70 Pro. The Redmi K70e will come with a 6.67-inch OLED display with a 120Hz refresh rate and a resolution of 2712 x 1220 pixels.

- October 2023: Google launched its Pixel Watch 2 smartwatch, featuring advanced health-related characteristics such as heart rate tracking and sleep tracking. The device uses a photoplethysmography (PPG) sensor that measures blood circulation by shining a green LED light onto the user's wrist. The watch also includes improved AI-powered algorithms to provide more accurate heart rate data.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Value Chain Analysis

- 4.4 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Adoption of Latest Technology and Innovations

- 5.1.2 Increased Focus on Health and Fitness

- 5.2 Market Restraints

- 5.2.1 High Costs Associated with Gadgets

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Temperature

- 6.1.2 Pressure

- 6.1.3 Image/Optical

- 6.1.4 Motion

- 6.1.5 Other Types of Sensors

- 6.2 By Application

- 6.2.1 Health and Wellness

- 6.2.2 Safety Monitoring

- 6.2.3 Sports and Fitness

- 6.2.4 Other Applications

- 6.3 By Country

- 6.3.1 United Arab Emirates

- 6.3.2 Saudi Arabia

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 STMicroelectronics

- 7.1.2 Infineon Technologies AG

- 7.1.3 Texas Instruments Incorporated

- 7.1.4 Analog Devices

- 7.1.5 Panasonic Corporation

- 7.1.6 InvenSense Inc.

- 7.1.7 NXP Semicondutors

- 7.1.8 TE Connectivity Ltd

- 7.1.9 Bosch Sensortec GmbH (Robert Bosch GmbH)

- 7.1.10 Broadcom Limited

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

穿戴式感測器市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、形狀、材料類型、最終用戶和功能分類

穿戴式感測器市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、形狀、材料類型、最終用戶和功能分類 穿戴式感測器市場規模、佔有率、成長及全球產業分析:按感測器類型、裝置類型、最終用戶和地區劃分的洞察與預測(2026-2034年)

穿戴式感測器市場規模、佔有率、成長及全球產業分析:按感測器類型、裝置類型、最終用戶和地區劃分的洞察與預測(2026-2034年) 穿戴式感測器市場規模、佔有率和成長分析(按應用、感測器類型、最終用戶、外形規格和地區分類)—2026-2033年產業預測

穿戴式感測器市場規模、佔有率和成長分析(按應用、感測器類型、最終用戶、外形規格和地區分類)—2026-2033年產業預測 穿戴式感測器市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭格局分類,2020-2030 年預測)

穿戴式感測器市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭格局分類,2020-2030 年預測) 穿戴式裝置市場中的 HMI 感測器,按感測器類型、穿戴式裝置類型、應用、技術、國家和地區分類 - 2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測

穿戴式裝置市場中的 HMI 感測器,按感測器類型、穿戴式裝置類型、應用、技術、國家和地區分類 - 2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測 穿戴式裝置中的 HMI 感測器市場規模、佔有率、趨勢分析報告:按感測器類型、裝置類型、應用、最終用途、地區、細分市場預測,2025 年至 2030 年2026 年至 2032 年穿戴式感測器市場類型、裝置、應用和地區分佈

穿戴式裝置中的 HMI 感測器市場規模、佔有率、趨勢分析報告:按感測器類型、裝置類型、應用、最終用途、地區、細分市場預測,2025 年至 2030 年2026 年至 2032 年穿戴式感測器市場類型、裝置、應用和地區分佈 北美穿戴式感測器:市場佔有率分析、產業趨勢和成長預測(2025-2030)拉丁美洲穿戴式感測器:市場佔有率分析、產業趨勢、產業趨勢、成長預測(2025-2030)歐洲穿戴式感測器 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

北美穿戴式感測器:市場佔有率分析、產業趨勢和成長預測(2025-2030)拉丁美洲穿戴式感測器:市場佔有率分析、產業趨勢、產業趨勢、成長預測(2025-2030)歐洲穿戴式感測器 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)