|

市場調查報告書

商品編碼

1640601

歐洲軟包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)Europe Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

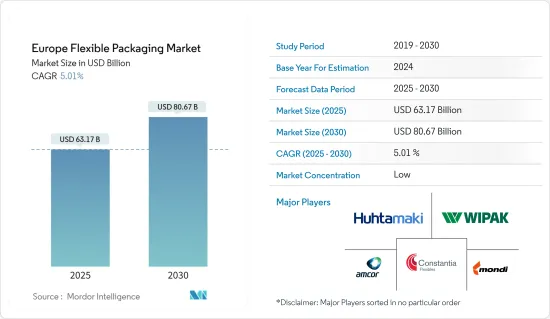

預計2025年歐洲軟包裝市場規模為631.7億美元,到2030年預計將達到806.7億美元,預測期內(2025-2030年)的複合年成長率為5.01%。

關鍵亮點

- 在歐洲,對加工食品、方便包裝食品、已調理食品和零食的需求不斷成長將推動市場成長。這一趨勢也受到非洲大陸不斷成長的城市人口和生活方式改變(如準備飯菜的時間減少)的推動。

- 此外,靈活的包裝解決方案有望促進該國對包裝、已調理食品、冷凍和優質食品的需求,因為它們可以延長此類產品的保存期限。永續軟包裝解決方案的出現也受到消費者對產品個人化日益成長的需求以及食品和飲料行業對可回收、環保包裝日益成長的需求的推動。

- 該地區生活方式的快速變化和經濟擴張導致人們對加工和包裝產品的偏好,從而推動了食品包裝市場的發展。人們對加工食品的偏好日益成長,主要是由於人口從農村到都市區的轉移。然而,該地區的塑膠包裝廢棄物數量正在增加(每年增加 2%)。歐盟委員會正在考慮禁止所有塑膠包裝,預計將減緩市場擴張。據歐盟下一任環境專員維吉尼亞斯·辛克維丘斯(Virginius Sinkevicius)稱,使用塑膠包裝和再生塑膠將被禁止。

- 乳製品產業是眾多使用塑膠的行業之一,並致力於減少塑膠的使用。英國食品和農村事務大臣盧克勳爵呼籲乳製品產業更永續發展,將牛奶包裝中使用的塑膠量減少 50%。這表明,在一個已經展現出創新多樣性的國家,綠色包裝將繼續擴大。

- 在法國,市場受到不斷擴張的化妝品產業支撐。對於化妝品來說,一些知名品牌選擇了軟包裝材料。與硬質塑膠相比,靈活的解決方案更經濟實惠,且保存期限更長。因此,化妝品行業的擴張預計將為軟包裝市場提供有利的潛力。

- 歐洲市場可能因金融危機對消費者購買力的影響、大宗商品價格上漲等問題而面臨困難。回收塑膠包裝廢棄物的過程需要現代化的基礎設施。這是一項耗時的任務,需要人力資源能力。

- 此外,由於塑膠材料在軟包裝中的廣泛使用,有關可回收性和永續性的某些環境問題可能會在一定程度內限制市場的成長。許多歐洲國家的回收和處理規則越來越嚴格,這可能會為一些企業帶來問題。所有這些都限制了歐洲軟包裝市場的成長。

歐洲軟包裝市場趨勢

食品業可望引領該地區的軟包裝市場

- 軟包裝是一種輕量級的替代品,它允許材料加工者以更少的數量運送更多的產品,從而節省與生產、破損、零件、退貨、浪費和運輸相關的成本。這是食品包裝的理想解決方案。此外,該地區的許多中小型企業正在尋求更長的保存期限和更好地防止食物因空氣、濕氣和陽光等各種原因而腐敗,從而增加了對軟包裝的需求。

- 隨著上班族的時間越來越緊張,以及食品選擇的便利性越來越高,對包裝食品的需求正在迅速成長。包裝食品具有更好的阻隔保護、遏製或累積、廣告、詳細的成分資訊、安全性、適用性和其他好處。因此,在整個預測期內,對包裝食品的需求和對網路購物的日益成長的偏好將推動全球電子商務包裝市場的成長。

- 根據 Voyado 的一項調查,疫情期間首次在網路上購買食品雜貨的消費者比例在西班牙為 30%,在法國為 22%,在英國和義大利為 20%,在瑞典和丹麥為 14%,在芬蘭為20%,英國和義大利為20%,波蘭、荷蘭、比利時和德國為10%,挪威為9%。此外,68% 的新食品雜貨購物者表示他們計劃在未來繼續這樣做。因此,人們習慣的這些改變正在對阻隔膜包裝市場產生正面的影響。

- 《英國食品雜誌》發表的一項研究發現,改用冷凍食品的家庭的食物浪費減少了 47% 以上。因此,消費者也開始選擇冷凍食品來減少浪費。預計向冷凍食品的轉變將刺激市場擴張。由於生活方式的改變、可支配收入的增加和開發中國家快速的都市化,尤其是中階人口的不斷擴大等多種因素,對冷凍食品袋的需求正在成長。

- 電子商務的日益成長的趨勢正在推動市場的成長。電子商務的擴張正在對歐洲的冷凍食品業務產生重大影響。線上零售商正在利用其廣泛的數位能力,透過提供更多種類的冷凍食品並將其直接運送到消費者家中,使客戶更容易購買和採購這些產品。宅配的便利、網路訂購的便利性以及即時追蹤訂單的能力正在推動冷凍食品市場的擴張。

- 根據德國冷凍食品協會(Deutsches Tiefkuhlinstitut)的數據,到 2023 年,冷凍烘焙點心將佔冷凍食品銷售額的 27% 左右,成為這一類別中最大的細分市場。排名第二的是冷凍蔬菜,約佔 13%,排名第三的是冷凍食品(包括燉菜和湯),約佔 12%。

- 此外,雜貨連鎖店、超級市場、大賣場和便利商店的快速發展,商品的供應和品質的提升也是推動該產業發展的主要因素。此外,食品工業的強勁成長和就業率的上升也是歐洲冷凍食品產業快速成長的重要因素。

英國發現重大市場成長機會

- 根據英國國家統計局的數據,到2030年,倫敦人口預計將成長到940萬,比2025年增加55萬。人口不斷成長,加上生活方式的改變,例如花在準備飯菜上的時間減少,正在推動人們轉向更多加工、方便包裝和已烹調食品和零食,這可能會推動所研究市場的成長。

- 此外,對包裝、已調理食品、冷凍和優質食品的需求不斷成長,預計將推動全國範圍內對此類解決方案的需求,因為靈活的包裝解決方案可以延長這些產品的保存期限。

- 由於包裝服務需求不斷成長和工業部門的不斷擴大,英國的包裝行業正在經歷急劇成長。英國包裝聯合會估計,該國包裝製造業的年營業額為 110 億英鎊(135.9 億美元)。該工廠就業人員超過 85,000 人,佔英國製造業的 3%。

- 在預測期內,菸草、寵物食品和居家醫療產品對軟包裝解決方案的需求不斷增加,可能會推動英國其他終端使用者垂直領域對軟包裝的需求。

- 此外,預計塑膠使用量的增加將對市場產生重大影響。例如,英國的塑膠包裝稅(PPT)將於2022年4月1日生效,對每噸含有30%或以下再生塑膠的塑膠包裝徵收200英鎊(247.7美元)的稅。該稅旨在鼓勵使用更環保的塑膠包裝,促進再生塑膠的使用並幫助減少塑膠廢棄物。

- 全國各地的消費者都認為,電子商務對生態不利,因為在配送和退貨過程中會產生氣體排放。 Aquapac 是一家開發促進循環經濟產品的特殊聚合物製造商,該公司在 2022 年進行的一項調查發現,超過一半 (52%) 的美國消費者在購買服飾和配件時會考慮環保包裝。說,他們願意為此付出更高的金額。

- 願意支付額外費用的受訪者中,有三分之一表示,他們願意支付1% 至4% 的高價來獲得採用永續包裝的產品,而近五分之二(39%)的受訪者表示願意額外支付5%。 15%的受訪者表示願意多支付10%至20%,8%的受訪者表示願意多支付6%至9%。

歐洲軟包裝產業概況

歐洲軟包裝市場細分為多個市場,並由 Amcor PLC、Mondi Group、Wipak Group、Huhtamaki Oyj 和 Constantia Flexibles 等大型公司主導。這些領先的公司擁有顯著的市場佔有率,並致力於透過策略合作措施擴大基本客群,以增加市場佔有率和盈利。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

- 產業價值鏈分析

第5章 市場動態

- 市場促進因素

- 加工食品需求穩定成長

- 輕量化趨勢預計將刺激批量需求

- 市場重新啟動

- 軟包裝市場競爭日益激烈,這可能會影響新參與企業的成長前景

- 與回收有關的環境問題

第6章 市場細分

- 依材料類型

- 聚乙烯 (PE)

- 雙軸延伸聚丙烯(BOPP)

- 流延聚丙烯(CPP)

- 聚氯乙烯(PVC)

- PET

- 其他材料類型(EVOH、EVA、PA 等)

- 依產品類型

- 小袋

- 包包

- 包裝膜

- PE基

- BOPET

- CPP 和 BOPP

- PVC

- 其他影片類型

- 其他

- 按最終用戶產業

- 食物

- 冷凍食品

- 乳製品

- 水果和蔬菜

- 其他食品

- 飲料

- 醫療和製藥

- 化妝品和個人護理

- 其他

- 食物

- 按國家

- 西歐

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 東歐和中歐

- 波蘭

- 捷克共和國

- 羅馬尼亞

- 匈牙利

- 西歐

第7章 競爭格局

- 公司簡介

- Amcor PLC

- Bak Ambalaj

- Bischof+Klein SE & Co. KG

- Constantia Flexibles GmbH

- Cellografica Gerosa SpA

- Coveris Management GmbH

- Danaflex Group

- Di Mauro Officine Grafiche SpA

- Gualapack SpA

- Huhtamaki Oyj

- ProAmpac LLC

- Wipak Group

- Sipospack Kft.

- ePac Holdings, LLC.

- Mondi Group

- Schur International A/S

第8章投資分析

第9章:未來市場展望

The Europe Flexible Packaging Market size is estimated at USD 63.17 billion in 2025, and is expected to reach USD 80.67 billion by 2030, at a CAGR of 5.01% during the forecast period (2025-2030).

Key Highlights

- Growing demand for processed, conveniently packaged, and pre-prepared foods and snacks in Europe will expand the market. This trend is also fueled by the continent's expanding urban population and shifting lifestyle habits, such as less time spent on meal preparation.

- Furthermore, because flexible packaging solutions can extend the shelf life of such products, the demand for packaged foods, ready-to-eat meals, frozen foods, and luxury foods is anticipated to rise in the nation. The emergence of sustainable, flexible packaging solutions has also been aided by rising consumer desire for product personalization and rising demand from food and beverage industries for recyclable and eco-friendly packaging.

- Owing to the region's fast-changing lifestyles and economic expansion, the preference for processed and packaged goods has driven the market for food packaging. The primary cause of the rising appetite for processed foods is the population's movement from rural to urban locations. However, the amount of plastic packaging waste in the area is rising (by 2% annually). The EU Commission is considering outlawing all plastic packaging, which is predicted to slow market expansion. According to Virginijus Sinkevicius, the incoming EU commissioner for the environment, plastic packaging and the use of recovered plastic would be outlawed.

- The dairy industry is one of many that uses plastic and concentrates on using less plastic. Lord Rooker, the United Kingdom's Food and Farming Minister, has urged the dairy industry to become more sustainable, with a 50% reduction in the number of plastics used in milk packaging. That suggests that greener packaging will continue to expand in a nation that has already demonstrated innovation diversity.

- The expanding cosmetics sector backs the market in France. For their cosmetic items, several well-known brands are choosing flexible packaging materials. Flexible solutions are more affordable and have a longer shelf life than stiff plastic. Consequently, the expanding cosmetics industry is anticipated to open up the lucrative potential for the flexible packaging market.

- The European market may face difficulties due to the financial crisis's effects on consumer spending power, rising commodity prices, and other similar concerns. Modern infrastructure is required for the process of recycling plastic packaging waste. It is a time-consuming operation that demands personnel competence.

- Additionally, due to the widespread usage of plastic material for flexible packaging, specific environmental issues regarding recyclability and sustainability may marginally restrict the market growth. Recycling and disposal rules are becoming stricter in a number of European nations, which could provide a problem for some merchants there. All of these things limit the expansion of the European flexible packaging market.

Europe Flexible Packaging Market Trends

Food Segment is Expected to Drive the Flexible Packaging Market in the Region

- Flexible packaging is a lightweight alternative that saves costs associated with production, damage, parts, returns, disposal, and transportation by allowing material processors to ship more products in less quantity. This is the ideal solution for food packaging. In addition, many small businesses in the region are looking for better protection with longer shelf life against various types of food spoilage, such as air, moisture, and sunlight, increasing the demand for flexible packaging.

- The demand for packaged food products is rising quickly due to working professionals' growing time limitations and the availability of more convenient food options. Packaged food products provide better barrier protection, containment or accumulation, advertising, detailed ingredient information, safety, appropriateness, and other benefits. As a result, the demand for packaged foods and the growing inclination for online shopping is expected to drive growth in the worldwide e-commerce packaging market throughout the forecast period.

- According to research conducted by Voyado, the proportion of consumers who made their first-ever online grocery purchases during the pandemic is Spain at 30%, France at 22%, the United Kingdom and Italy at 20%., Sweden and Denmark at 14%, Finland at 11%, Poland, Netherlands, Belgium, Germany at 10%, and Norway at 9%. Also, 68% of new customers who buy groceries online confirmed that keep doing so in the future. Consequently, this shift in people's habits has positively impacted the barrier film packaging market.

- A study published in the British Food Journal revealed that families that switched to frozen food reduced their food waste by over 47%. As a result, consumers are also moving to frozen food to reduce the amount of trash they produce. This shift to frozen food will spur market expansion. The demand for frozen food bags is rising due to several causes, including changing lifestyles, increasing disposable income, and the quick urbanization of developing nations, particularly the expanding middle-class population.

- The rising trend towards e-commerce is driving the growth of the market. The expansion of e-commerce has significantly impacted the frozen food business in Europe. Online retailers are leveraging extensive digital capabilities to offer a wider range of frozen foods and ship them directly to consumers' homes, making it easier for customers to purchase and source these products. The convenience of home delivery, the ease of online ordering, and the possibility of real-time order tracking are all driving the expansion of the frozen food market.

- According to Deutsches Tiefkuhlinstitut in the year 2023, frozen baked goods made up approximately 27% of frozen food sales - the largest portion in this category. Frozen vegetables came in second place with nearly 13% , while frozen meals (including stews and soups) came in third with about 12% across Germany.

- Moreover, the rapid development of grocery chains, supermarkets, hypermarkets, and convenience stores and the increasing availability and quality of products are some of the primary drivers of the industry. In addition, the strong growth of the food industry and the rising employment rate is also important for the rapid growth of the frozen food industry in Europe.

United Kingdom to Witnesses Significant Growth Opportunities in the market

- Growing urban populations in the United Kingdom According to the Office for National Statistics (UK) is projected that by 2030, the population of London will rise to 9.4 million, which represents a growth of 550,000 individuals from 2025. along with an increase in population and their altered lifestyle patterns, such as less time spent on meal preparation, are driving a shift towards more processed, conveniently packaged, and pre-prepared foods and snacks, which is anticipated to drive the growth of the market under study.

- Additionally, because flexible packaging solutions can extend the shelf life of such products, the rising demand for packaged foods, ready-to-eat foods, frozen foods, and luxury foods is projected to enhance the need for these solutions nationwide.

- The packaging industry is growing dramatically in the United Kingdom due to rising demand for packaging services and the increasing industrial sector. The Packaging Federation of the United Kingdom estimates that the country's packaging manufacturing sector had yearly sales of GBP 11 billion (USD 13.59 billion). More than 85,000 people are employed there, which is 3% of the manufacturing workforce in the United Kingdom.

- The increased demand for flexible packaging solutions for tobacco, pet food, and homecare products will drive the need for flexible packaging in the rest of the end-user verticals in the United Kingdom during the forecast period.

- In addition, the market is expected to be significantly impacted by the tightening of plastic usage laws. For instance, the United Kingdom's Plastic Packaging Tax (PPT), which went into effect on 1 April 2022, is charged at a rate of GBP 200 (USD 247.7) per metric ton of plastic packaging in the United Kingdom that has less than 30% recycled plastic content. The tax intends to promote the use of more environmentally friendly plastic packaging, boost the utilization of recycled plastic, and aid in reducing plastic waste.

- Consumers across the nation believe that e-commerce is not ecologically beneficial because of the gas emissions from deliveries and returns. In a survey conducted in 2022 by Aquapak, a manufacturer of specialized polymers that develops products to promote a circular economy, more than half (52%) of United Kingdom customers stated they would be ready to pay more for ecologically friendly packaging when buying clothing and accessories.

- One-third of those prepared to pay extra indicated they would increase the price by 1% to 4% to receive their items in sustainable packaging, while nearly two-fifths (39%) said they would pay an additional 5%. 15% of respondents said they would be willing to spend an extra 10% to 20%, while 8% said they would pay an additional 6% to 9%.

Europe Flexible Packaging Industry Overview

The Europe Flexible Packaging Market is fragmented and dominated by major players like Amcor PLC, Mondi Group, Wipak Group, Huhtamaki Oyj, and Constantia Flexibles. These major players have a prominent market share and focus on expanding their customer base by leveraging strategic collaborative initiatives to increase their market share and profitability.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Steady Rise in Demand for Processed Food

- 5.1.2 Move Toward Light Weighting Expected to Spur Volume Demand

- 5.2 Market Restarints

- 5.2.1 Flexible Packaging is Increasingly Turning into a Competitive Marketplace which Could Impact the Growth Prospects of New Entrants

- 5.2.2 Environmental Challenges Related to Recycling

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Polyethene (PE)

- 6.1.2 Biaxially Oriented Polypropylene (BOPP)

- 6.1.3 Cast Polypropylene (CPP)

- 6.1.4 Polyvinyl Chloride (PVC)

- 6.1.5 PET

- 6.1.6 Other Material Types (EVOH, EVA, PA, etc.)

- 6.2 By Product Type

- 6.2.1 Pouches

- 6.2.2 Bags

- 6.2.3 Packaging Films

- 6.2.3.1 PE-based

- 6.2.3.2 BOPET

- 6.2.3.3 CPP and BOPP

- 6.2.3.4 PVC

- 6.2.3.5 Other Film Types

- 6.2.4 Other Product Types

- 6.3 By End-user Industry

- 6.3.1 Food

- 6.3.1.1 Frozen Food

- 6.3.1.2 Dairy Products

- 6.3.1.3 Fruits and Vegetables

- 6.3.1.4 Other Food Products

- 6.3.2 Beverage

- 6.3.3 Healthcare and Pharmaceuticals

- 6.3.4 Cosmetics and Personal Care

- 6.3.5 Other End-user Industries

- 6.3.1 Food

- 6.4 By Country

- 6.4.1 Western Europe

- 6.4.1.1 United Kingdom

- 6.4.1.2 Germany

- 6.4.1.3 France

- 6.4.1.4 Italy

- 6.4.1.5 Spain

- 6.4.2 Eastern and Central Europe

- 6.4.2.1 Poland

- 6.4.2.2 Czech Republic

- 6.4.2.3 Romania

- 6.4.2.4 Hungary

- 6.4.1 Western Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 Bak Ambalaj

- 7.1.3 Bischof + Klein SE & Co. KG

- 7.1.4 Constantia Flexibles GmbH

- 7.1.5 Cellografica Gerosa SpA

- 7.1.6 Coveris Management GmbH

- 7.1.7 Danaflex Group

- 7.1.8 Di Mauro Officine Grafiche S.p.A.

- 7.1.9 Gualapack SpA

- 7.1.10 Huhtamaki Oyj

- 7.1.11 ProAmpac LLC

- 7.1.12 Wipak Group

- 7.1.13 Sipospack Kft.

- 7.1.14 ePac Holdings, LLC.

- 7.1.15 Mondi Group

- 7.1.16 Schur International A/S

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

軟包裝市場規模、佔有率及成長分析(按材料、包裝類型、印刷技術、應用和地區)-2025-2032 年產業預測

軟包裝市場規模、佔有率及成長分析(按材料、包裝類型、印刷技術、應用和地區)-2025-2032 年產業預測 中東和非洲軟包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美軟質包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)印尼軟包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲、中東和非洲軟包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)軟包裝產業:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

中東和非洲軟包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美軟質包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)印尼軟包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲、中東和非洲軟包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)軟包裝產業:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 2025年金屬化軟包裝全球市場報告軟包裝市場:按材料、產品類型、應用和地區分類轉換軟包裝市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料、應用、地區和競爭細分,2020-2030 年功能塗料市場規模、佔有率和成長分析(按產品類型、最終用戶和地區)- 產業預測 2025-2032

2025年金屬化軟包裝全球市場報告軟包裝市場:按材料、產品類型、應用和地區分類轉換軟包裝市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料、應用、地區和競爭細分,2020-2030 年功能塗料市場規模、佔有率和成長分析(按產品類型、最終用戶和地區)- 產業預測 2025-2032