|

市場調查報告書

商品編碼

1640604

亞太地區軟包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)APAC Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

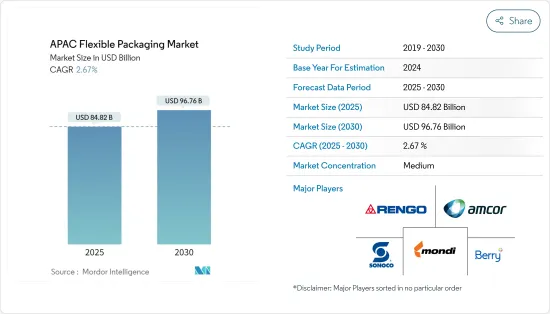

亞太地區軟包裝市場規模預計在 2025 年為 848.2 億美元,預計到 2030 年將達到 967.6 億美元,預測期內(2025-2030 年)的複合年成長率為 2.67%。

關鍵亮點

- 預計預測期內亞太地區的軟包裝將保持穩定的成長。該地區的一些知名供應商正在加快步伐,透過在包裝生命週期的三個階段(生產、運輸和處置)採用高效的製造技術,解決日益成長的環境永續性問題。 。

- 隨著零售額的飆升,市場趨於擴大,新產品不斷推出,現有產品的覆蓋範圍也不斷擴大。從食品飲料到藥品和個人護理等各行各業都使用軟包裝。因此,零售額的成長將會增強軟包裝市場的各個部分。日本經濟產業省報告顯示,2023年日本零售業銷售額預計將實現約163兆日元,創15年來最高水準。

- 在亞太地區,中國和印度等新興經濟體的快速都市化正推動國內對軟包裝的龐大需求。該地區終端用戶的健康成長進一步推動了對軟包裝產品的需求,主要是在包裝和包裝袋領域,主要是為了滿足該地區不斷成長的中等收入人口的小批量零售需求。

- 軟包裝產品的需求主要由該地區的千禧世代消費者推動,他們熱衷於單份、便攜的食品和飲料。這些產品通常設計為便攜、耐用和輕巧的,使得軟包裝成為一種流行的選擇。成長最快的零食食品(包括生鮮食品和加工食品)預計將主導食品和飲料行業的軟包裝需求。在印度的膨化零嘴零食公司中,Bingo 和 Kurkure 在 2023 年的市場佔有率均超過 10%。緊隨其後的是Taka Tak,同期的市場佔有率為 6%。

- 飲料行業為整個全部區域的軟包裝提供了潛在的成長機會。為了滿足日益成長的需求,食品公司正在跨地域、跨產品線擴張。例如,壽全齋是中國最古老的食品公司之一,成立於1760年,現已透過新的即飲產品系列擴展到飲料產業。

- 2024年1月:中國飲料品牌透過提供一致的高品質產品和服務,在國際市場取得突破,並在當地社區站穩腳步。米雪集團是一家總部位於河南鄭州、全球擁有超過 36,000 家門市的公司,該公司已申請在香港首次股票公開發行,邁出了重要一步。飲料業的這種擴張可能會進一步推動市場成長。

- 俄烏戰爭導致全球油價波動,直接影響了軟包裝所使用原料的成本,如塑膠、聚乙烯、聚丙烯等石化衍生物。這些原料對於生產軟包裝所使用的薄膜、袋子和包裝紙至關重要。石油基產品成本的上升增加了該地區軟包裝製造商的生產成本,從而導致最終產品價格上漲。

亞太軟包裝市場趨勢

食品業擴張可望推動市場成長

- 軟包裝通常用於冰沙、小吃、乳製品和糖果零食等食品。典型的軟性食品包裝應用包括用於包裝起司、肉類、麵包、蔬菜等的薄膜、小袋、鋁蓋和紙袋。這種軟包裝不僅可用作一次包裝,在某些情況下還可用作二次包裝。

- 在食品加工技術創新和消費者生活方式改變的推動下,包裝食品產業正在經歷成長。預計這些趨勢最終將在預測期內刺激產品需求並推動市場成長。例如,百事印度公司於 2024 年 2 月在其薯片產品線中推出了新的子品牌樂事 Shapez。這款創新產品推出了由馬鈴薯製成的心形顆粒。

- 同樣在 2024 年 8 月,斯里蘭卡歷史最悠久的糖果零食製造商 Uswatte Confectionery Works Pvt. Ltd 宣布重啟其著名洋芋片品牌 Chirpy Chips。由於政府採取措施限制優質馬鈴薯的進口,該公司先前已停止生產該品牌。斯里蘭卡糖果零食製造商重新進入馬鈴薯零食市場預計將支持市場成長。

- 多層薄膜和層壓板等軟包裝材料具有重要的阻隔性能,可保護食品免受濕氣、氧氣和污染物的侵害。這有助於延長乳製品、肉類和烘焙點心等生鮮產品的保存期限。消費者和食品製造商都在尋找既能保持產品新鮮度又能確保食品安全的包裝解決方案,因此軟包裝成為首選。

- 到 2023 年,日本軟性飲料的線上零售額將達到約 26 億美元,成為食品電子商務產業中最大的細分市場。根據中國國家統計局預測,2023年中國餐飲業年銷售額將達到約5.3兆元。這與前一年同期比較成長了約 20%。電子商務和食品宅配服務的擴張加速了對能夠承受運輸嚴格考驗的輕質、耐用的保護包裝的需求。軟包裝非常適合這些需求,因為它具有成本效益,並且可以容納乾燥流質食品。

印度:預計市場將大幅成長

- 印度由於其經濟、社會和工業的快速發展,在推動軟包裝市場成長方面發揮關鍵作用。印度人口超過14億,是全球最大的消費市場之一。快速的都市化正在改變人們的生活方式,越來越多的人遷入城市,對包裝商品的需求也隨之增加。 Bikaji 表示,到 2026 年,包裝食品市場規模可能會超過 5 兆印度盧比。

- 由於消費者偏好的改變以及對加工和包裝食品的支出增加,印度食品和飲料行業正在經歷顯著成長。該行業是該國最大的軟包裝終端用戶。 2023 年,熱飲在印度天然健康飲料零售中最高,超過 11 億美元。此外,同年天然保健飲料的零售超過16億美元。

- 零嘴零食市場在印度等新興經濟體中不斷擴大,由於軟包裝在零嘴零食袋、保鮮膜、袋子等製造中的應用,為市場供應商創造了成長機會。此外,印度零食品牌 Bikaji 報告稱,2023 年 7 月印度鹹味零食市場有所成長。

- 印度在全球製藥業佔有重要地位,這導致對軟包裝的需求不斷成長。軟包裝為錠劑、膠囊、糖漿等藥品提供防篡改、防潮和保護解決方案。隨著醫療保健產業的擴大以及人們對衛生和安全的關注度不斷提高,尤其是在新冠肺炎疫情之後,軟包裝在確保產品完整性和安全性方面發揮著越來越重要的作用。

- 印度消費者和企業越來越意識到永續性和減少塑膠廢棄物的重要性。這推動了對環保和可回收軟包裝材料的需求。印度政府已推出禁止使用一次性塑膠等措施並推出提倡永續做法的措施。這些法規正在推動製造商走向創新的包裝解決方案,例如生物分解性和可堆肥的軟包裝。

亞太地區軟包裝產業概況

亞太地區軟包裝市場由 Amcor Ltd、Berry Plastics Corporation、Mondi Group、Sonoco Products Company 和 Rengo 等重要參與者組成。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- 評估主要宏觀經濟趨勢的市場影響

第5章 市場動態

- 市場促進因素

- 便捷包裝需求不斷成長

- 對更長保存期限和創新包裝的需求

- 市場限制

- 環境和包裝回收問題

第6章 市場細分

- 按類型

- 小袋

- 包包

- 裹

- 其他

- 按材質

- 塑膠

- 紙

- 鋁/複合材料

- 按最終用戶產業

- 食物

- 飲料

- 製藥和醫療

- 家庭和個人護理

- 其他

- 按國家

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太地區

第7章 競爭格局

- 公司簡介

- Amcor Ltd

- Berry Plastics Corporation

- Mondi Group

- Sonoco Products Company

- Rengo Co. Ltd

- Sealed Air Corporation

- Formosa Flexible Packaging Corp

- Wapo Corporation Ltd

- Chuan Peng Enterprise Co. Ltd

- TCPL Packaging Ltd

- Ester Industries Ltd(Wilemina Finance Corporation)

第8章投資分析

第9章:市場的未來

簡介目錄

Product Code: 55595

The APAC Flexible Packaging Market size is estimated at USD 84.82 billion in 2025, and is expected to reach USD 96.76 billion by 2030, at a CAGR of 2.67% during the forecast period (2025-2030).

Key Highlights

- Flexible packaging in Asia-Pacific is expected to witness a stable growth rate during the forecast period. Some of the prominent vendors in the region are focusing on the ever-growing concern regarding environmental sustainability by adopting efficient manufacturing techniques throughout the three stages of the packaging life cycle: manufacturing, transportation, and disposal.

- As retail sales surge, markets tend to expand, introducing new products and broadening the reach of existing ones. Diverse industries, ranging from food and beverages to pharmaceuticals and personal care, utilize flexible packaging due to its versatility across various product categories. Consequently, a rise in retail sales stands to bolster various segments of the flexible packaging market. In 2023, Japan's retail industry achieved sales of approximately JPY 163 trillion, marking its highest value over the previous 15 years, as reported by METI (Japan).

- There is a considerable increase in domestic demand for flexible packaging in Asia-Pacific, owing to the rapid urbanization across emerging economies, such as China and India. Healthy growth across end users in the region is further driving the need for flexible packaging products, primarily in the wraps and pouches segment, majorly to address the small quantity retailing needs of the rising middle-income population in the region.

- The demand for flexible packaging products is mainly driven by millennial consumers in the region, as they have an avid preference for single-serving and on-the-go style food and beverage products. As these products are generally designed to be portable, durable, and lightweight, flexible packaging is a popular option. The fastest-growing areas of snack foods, both in terms of fresh items and processed foods, are expected to govern the demand for flexible packaging from the food and beverage industry. In 2023, Bingo and Kurkure had the highest market share of over 10% each among the puffed snacks companies in India. This was followed by Taka Tak, with a 6% market share during the same period.

- The beverage industry offers potential growth opportunities for flexible packaging across the region. Food companies are expanding their businesses in terms of geography and product lines to cater to this rising demand. For instance, Shou Quan Zhai, founded in 1760 and one of the oldest food companies in China, expanded into the beverage industry with a new line of ready-to-drink products.

- In January 2024, Chinese beverage brands made strides in international markets, embedding themselves into local communities by offering consistent quality products and services. Mixue Group, hailing from Zhengzhou in Henan province and boasting a network of over 36,000 stores globally, took a significant step by filing for an initial public offering in Hong Kong. Such expansion in the beverage industry may further propel market growth.

- The Russia-Ukraine War caused fluctuations in global oil prices, directly impacting the cost of raw materials used in flexible packaging, such as plastics, polyethylene, polypropylene, and other petrochemical derivatives. These materials are essential for producing films, pouches, and wraps used in flexible packaging. The increased cost of petroleum-based products raised the production costs for flexible packaging manufacturers in the region, leading to price increases for end products.

APAC Flexible Packaging Market Trends

Expanding Food Industry Expected to Drive Market Growth

- Flexible packaging is commonly used for food products such as smoothies, snacks, dairy, confectionery, etc. Typical flexible food packaging applications include films, pouches, aluminum lids, and paper bags to package cheeses, meats, bread, and vegetables. This flexible packaging can be used as primary packaging as well as secondary packaging in some cases.

- The packaged food industry has been witnessing growth owing to innovations in food processing techniques and changes in consumer lifestyles. These trends are anticipated to eventually boost product demand, propelling the growth of the market during the forecast period. For instance, in February 2024, PepsiCo India introduced a new sub-brand, Lay's Shapez, to its potato chips lineup. The innovative product showcases heart-shaped pellets made from potatoes.

- Also, in August 2024, Uswatte Confectionery Works Pvt. Ltd, Sri Lanka's oldest confectionery manufacturer, announced the revival of its famous potato chip brand, Chirpy Chips. The company had previously discontinued the brand due to government policies restricting the import of high-quality potatoes into the country. This re-entry of potato snacks by confectionery manufacturers in Sri Lanka is expected to support market growth.

- Flexible packaging materials, such as multilayer films and laminates, provide significant barrier properties that protect food from moisture, oxygen, and contaminants. This helps to extend the shelf life of perishable items like dairy products, meat, and baked goods. Consumers and food manufacturers alike seek packaging solutions that maintain product freshness while also ensuring food safety, making flexible packaging a preferred choice.

- In 2023, online retail sales of soft drinks in Japan amounted to around USD 2.6 billion, making it the largest segment within the food-based e-commerce industry. According to the National Bureau of Statistics of China, in 2023, the annual revenue of the foodservice industry in China amounted to around CNY 5.3 trillion. This indicated an increase in revenue of approximately 20% compared to the previous year. Such expansion of e-commerce and food delivery services has accelerated the need for lightweight, durable, and protective packaging that can withstand the rigors of shipping. Flexible packaging fits these needs by being cost-effective and adaptable for both dry and liquid food products.

India Is Expected to Witness Significant Market Growth

- India is playing a significant role in driving the growth of the flexible packaging market due to its rapidly evolving economic, social, and industrial landscape. With a population of over 1.4 billion, India is one of the largest consumer markets in the world. Rapid urbanization is leading to lifestyle changes, with more people moving to cities and a higher demand for packaged goods. According to Bikaji, the market value of packaged food is likely to surpass INR 5 trillion by 2026.

- India's food and beverage industry is experiencing significant growth, driven by changing consumer preferences and increasing spending on processed and packaged foods. This industry is the largest end user of flexible packaging in the country. In 2023, the retail sales value of naturally healthy beverages in India was the highest for hot drinks at over USD 1.1 billion. Furthermore, the retail sales value of the naturally healthy beverages surpassed USD 1.6 billion that same year.

- The snacks market has been expanding in emerging economies, including India, creating a growth opportunity for market vendors due to the application of flexible packaging in making snack pouches, wraps, bags, and others. Additionally, Bikaji, a snack brand in India, reported that the savory snacks market in India witnessed growth in July 2023.

- India is a significant player in the global pharmaceutical industry, and the demand for flexible packaging is growing. Flexible packaging offers tamper-evident, moisture-resistant, and protective solutions for pharmaceutical products, including tablets, capsules, and syrups. As the healthcare sector expands, especially with the increasing focus on hygiene and safety post-COVID-19, flexible packaging plays an increasingly crucial role in ensuring product integrity and safety.

- There is growing awareness among Indian consumers and companies about the importance of sustainability and reducing plastic waste. This has led to improved demand for eco-friendly and recyclable flexible packaging materials. The Indian government has introduced policies such as the ban on single-use plastics and initiatives promoting sustainable practices. These regulations are pushing manufacturers toward innovative packaging solutions like biodegradable and compostable flexible packaging.

APAC Flexible Packaging Industry Overview

The APAC flexible packaging market is fragmented, with the presence of significant companies like Amcor Ltd, Berry Plastics Corporation, Mondi Group, Sonoco Products Company, and Rengo Co. Ltd. The companies continuously invest in strategic collaborations and product developments to gain market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of Key Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Convenient Packaging

- 5.1.2 Demand for Longer Shelf Life and Innovative Packaging

- 5.2 Market Restraints

- 5.2.1 Concerns About the Environment and Recycling of Packaging Material

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Pouches

- 6.1.2 Bags

- 6.1.3 Wraps

- 6.1.4 Other Types

- 6.2 By Material

- 6.2.1 Plastic

- 6.2.2 Paper

- 6.2.3 Aluminum/Composites

- 6.3 By End-user Industry

- 6.3.1 Food

- 6.3.2 Beverages

- 6.3.3 Pharmaceutical and Medical

- 6.3.4 Household and Personal Care

- 6.3.5 Other End-user Industries

- 6.4 By Country

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.4.4 Australia

- 6.4.5 Rest of Asia Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Ltd

- 7.1.2 Berry Plastics Corporation

- 7.1.3 Mondi Group

- 7.1.4 Sonoco Products Company

- 7.1.5 Rengo Co. Ltd

- 7.1.6 Sealed Air Corporation

- 7.1.7 Formosa Flexible Packaging Corp

- 7.1.8 Wapo Corporation Ltd

- 7.1.9 Chuan Peng Enterprise Co. Ltd

- 7.1.10 TCPL Packaging Ltd

- 7.1.11 Ester Industries Ltd (Wilemina Finance Corporation)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

02-2729-4219

+886-2-2729-4219

中東和非洲軟包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

中東和非洲軟包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 北美軟質包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

北美軟質包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 印尼軟包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

印尼軟包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 歐洲、中東和非洲軟包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

歐洲、中東和非洲軟包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 2025年金屬化軟包裝全球市場報告

2025年金屬化軟包裝全球市場報告 軟包裝市場:按材料、產品類型、應用和地區分類

軟包裝市場:按材料、產品類型、應用和地區分類 轉換軟包裝市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料、應用、地區和競爭細分,2020-2030 年

轉換軟包裝市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料、應用、地區和競爭細分,2020-2030 年 功能塗料市場規模、佔有率和成長分析(按產品類型、最終用戶和地區)- 產業預測 2025-2032

功能塗料市場規模、佔有率和成長分析(按產品類型、最終用戶和地區)- 產業預測 2025-2032 2025-2033 年按產品類型、原料、印刷技術、應用和地區分類的軟包裝市場報告

2025-2033 年按產品類型、原料、印刷技術、應用和地區分類的軟包裝市場報告 2025-2033 年按材料類型、包裝類型、應用、最終用途產業和地區分類的金屬化軟包裝市場

2025-2033 年按材料類型、包裝類型、應用、最終用途產業和地區分類的金屬化軟包裝市場

▼