|

市場調查報告書

商品編碼

1644493

印度屋頂:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)India Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

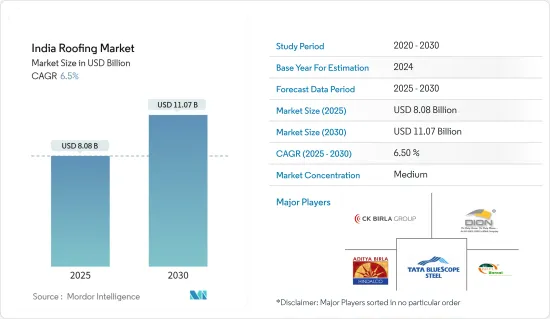

印度屋頂市場規模預計在 2025 年為 80.8 億美元,預計到 2030 年將達到 110.7 億美元,預測期內(2025-2030 年)的複合年成長率為 6.5%。

受快速都市化、工業發展和大型基礎設施計劃的推動,印度屋頂材料市場正在經歷強勁成長。隨著政府優先考慮智慧城市、機場和高速公路等舉措,住宅、商業和工業領域對優質屋頂解決方案的需求正在飆升。為了應對這一趨勢,製造商正在推出創新、耐用且節能的產品,以滿足多樣化的市場需求。

印度收入水準的提高促使消費者從傳統屋頂材料轉向更可靠的替代品,從而顯著促進了市場成長。聚碳酸酯屋頂板由於易於安裝在工業和大型商業建築上而變得越來越受歡迎。聚碳酸酯屋頂材料具有很強的耐候性,具有多種紋理和設計,並且維護成本低。除了傳統的應用外,它還用於天窗、游泳池、人行道、標誌等。聚碳酸酯屋頂材料用途廣泛且耐用,因此用於各種用途,從而導致市場對其的需求不斷成長。

據行業報告稱,技術創新,尤其是新屋頂技術的出現,將推動印度屋頂市場的成長。綠色屋頂尤其引人注目,具有吸收雨水、隔熱和改善美觀等好處。綠屋頂不僅提高能源效率,還有助於城市生物多樣性並減少城市熱島效應。此外,預計在預測期內,實現屋頂材料無縫安裝和現有基礎設施升級的先進機械和設備將加速市場的發展。尖端機械的整合確保了屋頂施工計劃的精確性和效率,進一步促進了市場擴張。

印度屋頂市場趨勢

印度蓬勃發展的建築與城市發展:外國直接投資成長與未來前景

房地產部分包括住宅、辦公、零售、旅館、休閒公園等。同時,城市發展部分包括供水、衛生、城市交通、學校、醫療保健等。根據2023年產業報告,到2047年,印度人口預計將達到16.4億,其中51%將居住在都市區。 2000 年 4 月至 2024 年 3 月期間,建築業(基礎設施)共吸引了 339.1 億美元的外國直接投資(FDI)流入,成為該國最大的 FDI 接受產業之一。

根據自動化路線,已完成的城鎮、商場、購物中心和商業機構的營運和管理計劃允許 100% 的外國直接投資。同樣,城市交通、供水、排污和污水處理等城市基礎設施領域也允許透過自動途徑進行 100% 的外國直接投資。

預測表明,到 2047 年,印度一半以上的人口將居住在都市區,這將增加對住宅、商業和基礎設施計劃的需求。此外,印度政府的優惠政策,例如允許透過自動途徑進行 100% 外國直接投資 (FDI),使這些領域對全球投資者更具吸引力。隨著外國直接投資穩步流入基礎設施和房地產領域,印度建築業預計將繼續擴張和快速成長。

政府主導的經濟適用住宅:印度屋頂材料市場的關鍵催化劑

根據一家領先的行業融資平台報道,2022 年國家預算強調了政府對住宅行業的承諾,向住房與城市發展部(MoHUA)撥款 5000 億印度盧比(61114.3 億美元),並設立 35 億美元的基金來推動停滯的住宅計劃。到 2030 年,印度的都市化預計將從 33% 上升到 40% 以上,Invest India 預計印度將需要額外 2,500 萬套中檔和經濟適用住宅。

2023 年,根據 Pradhan Mantri Awas Yojana (PMAY)(也稱為總理住宅計劃),都市區已建成 540 萬套住宅。然而,到2020年,都市區貧困階級的住宅需求預計將達到約1,100萬套。

政府的承諾透過大量的財政投資和 PMAY 等項目來體現,凸顯了其解決住宅短缺問題的決心。都市化的加快以及對住宅的需求不斷成長,住宅這一領域成為投資和開發的有利可圖的途徑。但要真正滿足日益成長的城市居民的住宅需求,還必須持續努力填補現有的缺口。

印度屋頂產業概況

聖戈班、Mongia Roofing、JSW Steel、Boral Roofing、Etex 和 Visaka Industries 等主要企業在國內和國際上佔據主導地位。這些公司透過持續提供優質的屋頂解決方案並不斷提高其市場佔有率,確立了其主要企業。

金屬屋頂、瀝青瓦、粘土屋頂瓦、混凝土屋頂、瀝青膜和綠色屋頂等多種屋頂材料正在推動市場的發展。每種材料都具有耐用性、成本效益和環境永續性等獨特優勢,以滿足不同消費者的偏好和需求。

屋頂材料市場高度分散,既有大型製造商,也有當地供應商。這些製造商滿足不同細分市場的需求,從高階屋頂材料到經濟實惠的屋頂材料。這種分散性導致了競爭格局的蓬勃發展,技術創新和以客戶為中心的解決方案為消費者提供了廣泛的選擇,以滿足他們的特定需求。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 屋頂領域的技術創新

- 產業價值鏈/供應鏈分析

- 政府法規和舉措對建築業的影響

- 審查並說明政府基礎設施發展計劃

- 地緣政治與疫情將如何影響市場

第5章 市場動態

- 市場促進因素

- 可支配所得增加,中階擴大

- 屋頂解決方案意識不斷增強

- 市場限制

- 仿冒品偽劣屋頂材料是一大挑戰

- 屋頂產業面臨技術純熟勞工短缺的問題

- 市場機會

- 快速都市化與建築熱潮

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第6章 市場細分

- 按行業

- 商業建設

- 住宅建築

- 工業建築

- 按材質

- 瀝青

- 瓦

- 金屬

- 其他

- 按屋頂類型

- 平屋頂

- 斜屋頂

第7章 競爭格局

- 公司簡介

- Tata Bluescope Steel

- CK Birla Group

- Hindalco Ind Ltd

- Bansal Roofing Products Limited

- Dion Incorporation

- Everest Industries Limited

- Moon Pvc Roofing

- Aqua Star

- Indian Roofing Industries Pvt. Ltd

- Metecno India Pvt. Limited*

- 其他公司

第8章 市場機會與未來趨勢

第 9 章 附錄

The India Roofing Market size is estimated at USD 8.08 billion in 2025, and is expected to reach USD 11.07 billion by 2030, at a CAGR of 6.5% during the forecast period (2025-2030).

The Indian roofing market is experiencing robust growth, propelled by swift urbanization, industrial growth, and extensive infrastructure projects. As the government prioritizes initiatives like smart cities, airports, and highways, the demand for premium roofing solutions surges across residential, commercial, and industrial domains. In response, manufacturers are rolling out innovative, durable, and energy-efficient products tailored to diverse market demands.

In India, rising income levels are prompting consumers to shift from traditional roofing materials to more reliable alternatives, significantly driving market growth. Polycarbonate roofing sheets, favored for their easy installation in industrial and large-scale commercial buildings, are becoming increasingly popular. These sheets are weather-resistant, come in various textures and designs, and boast low maintenance costs. Beyond traditional uses, they're also employed in skylights, swimming pools, walkways, and display signboards. The versatility and durability of polycarbonate roofing sheets make them a preferred choice for various applications, contributing to their growing demand in the market.

According to an industry report, technological innovations, especially the emergence of new roofing technologies, are set to propel the growth of the roofing market in India. Notably, green roofing stands out, offering benefits like rainwater absorption, insulation, and enhanced aesthetic appeal. Green roofing systems not only improve energy efficiency but also contribute to urban biodiversity and reduce the urban heat island effect. Furthermore, the market is expected to gain momentum during the forecast period, thanks to the seamless installation of roofing components and upgrades to existing infrastructure, facilitated by advanced machinery. The integration of cutting-edge machinery ensures precision and efficiency in roofing projects, further driving market expansion.

India Roofing Market Trends

Booming Construction and Urban Development in India: FDI Growth and Future Projections

The real estate segment includes residential properties, offices, retail spaces, hotels, and leisure parks. In contrast, the urban development segment covers areas such as water supply, sanitation, urban transport, schools, and healthcare. As per industry reports from 2023, India's population was expected to reach 1.64 billion by 2047, with an estimated 51% residing in urban centers. From April 2000 to March 2024, the construction (infrastructure) sector attracted foreign direct investment (FDI) inflows totaling USD 33.91 billion, making it one of the top recipients of FDI in the country.

Under the automatic route, 100% FDI is permitted in completed projects for the operations and management of townships, malls, shopping complexes, and business constructions. Similarly, 100% FDI is also allowed for urban infrastructures, including urban transport, water supply, sewerage, and sewage treatment, all under the automatic route.

Projections indicate that by 2047, more than half of India's populace will reside in urban locales, amplifying the demand for residential, commercial, and infrastructural projects. Furthermore, the Indian government's favorable policies, such as permitting 100% Foreign Direct Investment (FDI) through the automatic route, enhance the allure of these sectors for global investors. With a steady influx of FDI into both infrastructure and real estate, India's construction landscape is primed for ongoing expansion and burgeoning opportunities.

Government-Driven Growth in Affordable Housing: A Key Catalyst for the Roofing Market in India

As reported by an industry-leading financial platform, the 2022 national budget underscored the government's commitment to the housing sector, allocating INR 50,000 crore (USD 6111.43 billion) to the Ministry of Housing and Urban Development (MoHUA) and establishing a USD 3.5 billion fund to expedite stalled housing projects. With urbanization in India projected to rise from 33% to over 40% by 2030, Invest India estimates a demand for an additional 25 million mid-range and affordable housing units.

In 2023, under the Pradhan Mantri Awas Yojana (PMAY), also known as The Prime Minister's Housing Plan, India saw the completion of 5.4 million houses in urban areas. However, in 2020, the demand for housing among the urban poor was estimated at around 11 million housing complexes.

The government's commitment is evident through substantial financial investments and programs like PMAY, underscoring its determination to address the housing shortage. As urbanization accelerates and the demand for mid-range and affordable housing intensifies, the sector emerges as a lucrative avenue for investment and development. Yet, to truly cater to the housing needs of India's burgeoning urban populace, sustained efforts are essential to bridge the existing deficit.

India Roofing Industry Overview

Leading companies, including Saint-Gobain, Mongia Roofing, JSW Steel, Boral Roofing, Etex, and Visaka Industries, hold a dominant position in the market, boasting both national and international reach. These companies have established themselves as key players by consistently delivering high-quality roofing solutions and expanding their market presence.

Diverse roofing materials, including metal roofing, asphalt shingles, clay tiles, concrete roofing, bituminous membranes, and green roofing solutions, drive the market. Each material offers unique benefits, such as durability, cost-effectiveness, and environmental sustainability, catering to the varied preferences and needs of consumers.

The roofing market exhibits high fragmentation, accommodating both large-scale manufacturers and local suppliers. These players cater to a spectrum of segments, ranging from premium to budget-friendly roofing materials. This fragmentation allows for a competitive landscape where innovation and customer-centric solutions thrive, ensuring that consumers have access to a wide range of options to meet their specific requirements.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Innovations in the Roofing Sector

- 4.3 Industry Value Chain/Supply Chain Analysis

- 4.4 Impact of Government Regulations and Initiatives taken in the Construction Industry

- 4.5 Review and Commentary on the Extent of Government Infrastructure Development Schemes

- 4.6 Impact of Geopolitics and Pandemics on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Disposable Income and Middle-Class Expansion

- 5.1.2 Increased Awareness of Roofing Solutions

- 5.2 Market Restraints

- 5.2.1 The presence of counterfeit or substandard roofing materials in the market poses a significant challenge

- 5.2.2 The roofing industry faces a shortage of skilled labor

- 5.3 Market Opportunities

- 5.3.1 Rapid Urbanization and Construction Boom

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitutes

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Sector

- 6.1.1 Commercial Construction

- 6.1.2 Residential Construction

- 6.1.3 Industrial Construction

- 6.2 By Material

- 6.2.1 Bituminous

- 6.2.2 Tiles

- 6.2.3 Metal

- 6.2.4 Other Materials

- 6.3 By Roofing Type

- 6.3.1 Flat Roof

- 6.3.2 Slope Roof

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Tata Bluescope Steel

- 7.1.2 CK Birla Group

- 7.1.3 Hindalco Ind Ltd

- 7.1.4 Bansal Roofing Products Limited

- 7.1.5 Dion Incorporation

- 7.1.6 Everest Industries Limited

- 7.1.7 Moon Pvc Roofing

- 7.1.8 Aqua Star

- 7.1.9 Indian Roofing Industries Pvt. Ltd

- 7.1.10 Metecno India Pvt. Limited*

- 7.2 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

屋頂瓦片:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲屋頂瓦:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

屋頂瓦片:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲屋頂瓦:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 2025年全球屋頂市場報告

2025年全球屋頂市場報告 屋頂材料市場規模、佔有率和成長分析(按材料、建築類型、設計、應用、銷售管道和地區)- 2025-2032 年行業預測屋頂系統市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料、產品、建築類型、最終用戶部門、地區和競爭進行細分,2020-2030 年預測屋頂市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分,按產品類型、按應用、按地區、按競爭,2020-2030F美國屋頂:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)2024 年住宅低坡屋頂全球市場報告屋頂瓦市場規模、佔有率、成長分析,按材料類型、按建築類型、按最終用戶、按地區 - 行業預測,2024-2031 年屋頂材料市場規模、佔有率和成長分析(按產品、應用和地區):產業預測(2024-2031)

屋頂材料市場規模、佔有率和成長分析(按材料、建築類型、設計、應用、銷售管道和地區)- 2025-2032 年行業預測屋頂系統市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料、產品、建築類型、最終用戶部門、地區和競爭進行細分,2020-2030 年預測屋頂市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分,按產品類型、按應用、按地區、按競爭,2020-2030F美國屋頂:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)2024 年住宅低坡屋頂全球市場報告屋頂瓦市場規模、佔有率、成長分析,按材料類型、按建築類型、按最終用戶、按地區 - 行業預測,2024-2031 年屋頂材料市場規模、佔有率和成長分析(按產品、應用和地區):產業預測(2024-2031)