|

市場調查報告書

商品編碼

1645090

美國屋頂:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)United States Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

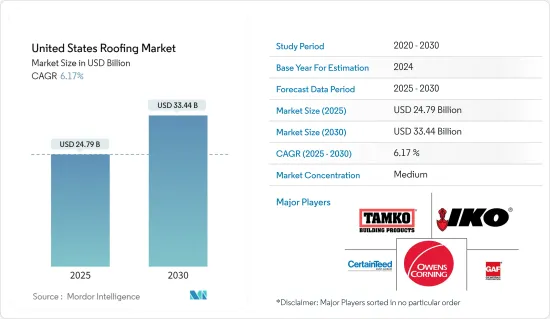

美國屋頂市場規模預計將在 2025 年達到 247.9 億美元,到 2030 年將達到 334.4 億美元,預測期內(2025-2030 年)的複合年成長率為 6.17%。

美國屋頂產業是世界上發展最快的產業之一。都市化、建築、環境問題和技術創新都在促進屋頂產業的發展。屋頂市場為世界各地的住宅、商業和工業建築提供各種各樣的屋頂產品和技術。預計到 2022 年,美國屋頂承包行業在市場規模方面將排名第 17 位,在建設產業中排名第 213 位。

北達科他州屋頂承包商的平均薪資為 55,877 美元,而德克薩斯州屋頂承包商的平均薪資略高於 27,000 美元。預計 2018 年至 2023 年期間,屋頂承包商產業將在美國僱用 212,000 名工人,未來五年內將成長到 220,989 名。截至 2023 年,美國共有 79,139 名屋頂承包商,較 2022 年略有下降。屋頂承包商最多的州是加州,有 9,303 名,其次是德克薩斯州,有 6,561 名,佛羅裡達州有 6,398 名。

隨著越來越多的公司進入市場以及技術不斷提高音質,美國屋頂市場預計將繼續成長。由於屋頂在各行業的應用範圍不斷擴大,其市場多年來一直在穩步成長。汽車和建築業在屋頂市場的成長中發揮著重要作用。

美國屋頂市場的趨勢

單層屋頂可望贏得市場佔有率

預計到 2027 年,美國單層屋頂膜市場(塑膠和橡膠屋頂產品)都將成長,這主要是由於瀝青膜市場佔有率下降。單膜相對於瀝青膜的優異性能將成為推動該市場成長的主要因素。自黏單層薄膜由於使用方便,其使用量不斷增加,預計將推動塑膠單層薄膜的需求,這對於時間緊迫、經常與缺乏經驗的工作人員一起工作的承包商來說是一個關鍵因素。此外,塑膠屋頂膜也可用於涼爽屋頂用途,製造商正在努力提供具有更厚的片材以改善抗衝擊和抗撕裂性能的產品。

美國的一項調查發現,最受歡迎的商業建築系統是單層建築,81% 的受訪者採用這種建築系統。該系統還佔商業屋頂承包商銷售額的 36%。單層屋頂銷售主要由安裝 TPO 系統的承包商 (41%) 推動。接下來是 EPDM(30%)、PVC(17%)和 KEE(10%)。平均而言,低梯度瀝青銷售額的 48% 為改質瀝青 (SBS),其次是改質瀝青 (APP),佔 27%,然後是建築屋頂,佔 25%。 71% 的受訪者使用低坡度瀝青,約佔銷售額的 10%。使用單層屋頂的承包商也預期 2024 年商業銷售額將會成長。

預計商業領域屋頂材料銷售的成長將推動市場的發展。

2023年,商業領域的屋頂銷售持續成長,成為經濟的動力。在調查中,近四分之三的受訪者(74%)表示,2023年的銷售額將增加或維持不變,而26%的受訪者表示,他們的銷售額將與2022年相比大幅增加。此外,74% 的企業表示明年的年銷售額將會增加,85% 的企業表示未來三年的銷售額將會提高。另有 10% 的受訪者表示銷售量將下降,4% 的受訪者認為銷售量將大幅下降,7% 的受訪者認為 2024 年後銷售量將進一步下降。

調查顯示,53% 的受訪者預計 2024 年銷售額將小幅成長,另有 68% 的受訪者預計 2026 年銷售額將小幅成長。總部所在地對區域分佈影響不大,東北部、中西部、南部和西部地區超過一半(54%)的用戶預計年終收入將增加。該地區近 60% 的承包商預計與前一年同期比較的年銷售額成長將持續到 2026 年。在中西部和西部,73% 的企業預計到 2026 年銷售額將實現成長。

美國屋頂產業概況

美國屋頂產業是世界上最大的產業之一,競爭非常激烈。許多公司在美國屋頂市場佔有重要地位。屋頂製造商正在實施多項措施,包括改變其製造和供應鏈,以滿足日益成長的屋頂需求。進入該市場的公司包括 GAF Materials Corporation、CertainTeed Corporation、Owens Corning 和 IKO Industries。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 屋頂產業的技術創新

- 產業價值鏈/供應鏈分析

- 政府法規和舉措對建設產業的影響

- 對政府基礎設施發展計劃的見解和說明

- 新冠肺炎疫情對市場的影響

第5章 市場動態

- 市場促進因素

- 可支配所得增加和中階擴大

- 提高對屋頂解決方案的認知

- 市場限制

- 假冒仿冒品屋頂的存在是一大挑戰。

- 屋頂產業面臨技術純熟勞工短缺的問題

- 市場機會

- 快速都市化與建築熱潮

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第6章 市場細分

- 按行業

- 商業建設

- 住宅建築

- 產業建設

- 按材質

- 改性瀝青

- 三元乙丙橡膠

- 熱塑性聚烯

- PVC 膜

- 金屬

- 瓦

- 其他

- 依屋頂類型

- 平屋頂

- 斜屋頂

第7章 競爭格局

- 公司簡介

- GAF Materials Corporation

- CertainTeed Corporation

- Owens Corning

- IKO Industries

- Tamko Building Products

- Atlas Roofing Corporation

- Beacon Building Products

- IronHead Roofing

- Centimark Corp.

- Tecta America

- Flynn Group

- Baker Roofing*

- *List Not Exhaustive

- 其他公司

第 8 章:市場的未來

第 9 章 附錄

The United States Roofing Market size is estimated at USD 24.79 billion in 2025, and is expected to reach USD 33.44 billion by 2030, at a CAGR of 6.17% during the forecast period (2025-2030).

The US roofing industry is one of the fastest-growing industries in the world. Urbanization, construction, environmental issues, and technological innovation have all contributed to the growth of the roofing industry. The roofing market offers a wide variety of roofing materials and technologies for residential, commercial, and industrial buildings worldwide. The roofing contracting industry in the United States ranks as the 17th largest construction industry in terms of market size and the 213rd largest in the United States in 2022.

The median roofing contractor salary in North Dakota is USD 55,877, while the median roofing wage in Texas is just over USD 27,000. The roofing contractor industry employs 212,000 workers in the United States from 2018 to 2023 and is expected to grow to 220,989 workers in the next five years. As of 2023, the roofing contractor business in the United States totaled 79,139, a slight decrease from 2022. The state with the most roofing contractor businesses is California, with 9,303, followed by Texas, with 6,561, and Florida, with 6,398.

The US roofing market is expected to continue to grow as more companies enter the market and as technology continues to improve the quality of audio. The roofing market has been growing steadily over the years due to its growing applications in a variety of industries. Automotive and construction industries have played a major role in the growth of the roofing market.

United States Roofing Market Trends

Single-Ply Roofing Products are Expected to Gain Market Share

The US roofing single-ply membrane market is expected to grow for both plastic and rubber roofing products by 2027, mainly due to the decrease in bituminous membrane market share. The advantages of single-ply over bituminous in terms of performance will be the main drivers of this market growth. The demand for plastic single-ply membranes is expected to be driven by the increasing use of self-adhesive single-ply membranes due to ease of installation, an important factor for time-strapped contractors who often work with inexperienced crews, the ability of plastic roofing membranes to be used for cool roofing purposes, and manufacturer's efforts to provide products with thicker sheets that offer improved impact and tear resistance.

According to a survey in the United States, the most popular commercial installation system in the survey was single-ply, which was used by 81% of respondents. It also generated 36% of revenue for commercial roofers. Single-ply sales were driven by 41% of contractors who installed TPO systems. EPDM followed with 30%, PVC with 17%, and KEE with 10%. On average, 48% of low slope asphalt sales were made of modified bitumen - SBS, followed by modified bitumen - APP with 27% and built-up roofing with 25%. Low-slope asphalt was used by 71% of respondents, accounting for about 10% of revenue. Contractors using single-ply roofs also indicated that they expected commercial sales to grow in 2024.

Increasing Sales of Roofing in the Commercial Sector is Expected to Drive the Market in the Future

Roofing sales increased in the commercial space again in 2023 as the economy gained traction. About three-quarters (74%) of respondents in a survey said sales increased or remained stable in 2023, while 26% said they expected sales to increase significantly compared to 2022. Another 74% said annual sales volume would increase next year, while 85% said sales would improve over the next 3 years. Another 10% said sales volume would decrease, with 4% expecting a significant drop and 7% expecting further declines in 2024 and beyond.

According to a survey, 53% expect revenues to increase slightly in 2024, and even more (68%) expect a slight increase through 2026. Geographic headquarters had little impact on the regional breakdown, and more than half (54%) of all contractors across the Northeast, Midwest, South, and West expected year-end sales growth. Around 60% of contractors across the same territory expected Y-o-Y sales growth in 2024 that would continue through 2026. 73% of contractors in the Midwest and West expected sales volume growth through 2026.

United States Roofing Industry Overview

The US roofing industry is one of the largest and most competitive in the world. Many companies have a significant presence in the US roofing market. Roofing manufacturers are implementing several measures to meet the increased demand for roofing materials, including increased manufacturing and supply chain changes. Some of the companies operating in the market are GAF Materials Corporation, CertainTeed Corporation, Owens Corning, and IKO Industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Innovations in the Roofing Sector

- 4.3 Industry Value Chain/Supply Chain Analysis

- 4.4 Impact of Government Regulations and Initiatives taken in the Construction

- 4.5 Review and Commentary on the Extent of Government Infrastructure Development Schemes

- 4.6 Impact of the COVID-19 Pandemic on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Disposable Income and Middle-Class Expansion

- 5.1.2 Increased Awareness of Roofing Solutions

- 5.2 Market Restraints

- 5.2.1 The presence of counterfeit or substandard roofing materials in the market poses a significant challenge

- 5.2.2 The roofing industry faces a shortage of skilled labor

- 5.3 Market Opportunities

- 5.3.1 Rapid Urbanization and Construction Boom

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitutes

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Sector

- 6.1.1 Commercial Construction

- 6.1.2 Residential Construction

- 6.1.3 Industrial Construction

- 6.2 By Material

- 6.2.1 Modified Bitumen

- 6.2.2 EPDM Rubber

- 6.2.3 Thermoplastic Polyolefin

- 6.2.4 PVC Membrane

- 6.2.5 Metals

- 6.2.6 Tiles

- 6.2.7 Others

- 6.3 By Roofing Type

- 6.3.1 Flat Roof

- 6.3.2 Slope Roof

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 GAF Materials Corporation

- 7.1.2 CertainTeed Corporation

- 7.1.3 Owens Corning

- 7.1.4 IKO Industries

- 7.1.5 Tamko Building Products

- 7.1.6 Atlas Roofing Corporation

- 7.1.7 Beacon Building Products

- 7.1.8 IronHead Roofing

- 7.1.9 Centimark Corp.

- 7.1.10 Tecta America

- 7.1.11 Flynn Group

- 7.1.12 Baker Roofing*

- 7.2 *List Not Exhaustive

- 7.3 Other Companies

8 FUTURE OF THE MARKET

9 APPENDIX

屋頂瓦片:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲屋頂瓦:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

屋頂瓦片:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲屋頂瓦:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 2025年全球屋頂市場報告

2025年全球屋頂市場報告 屋頂材料市場規模、佔有率和成長分析(按材料、建築類型、設計、應用、銷售管道和地區)- 2025-2032 年行業預測屋頂系統市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料、產品、建築類型、最終用戶部門、地區和競爭進行細分,2020-2030 年預測屋頂市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分,按產品類型、按應用、按地區、按競爭,2020-2030F印度屋頂:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)2024 年住宅低坡屋頂全球市場報告屋頂瓦市場規模、佔有率、成長分析,按材料類型、按建築類型、按最終用戶、按地區 - 行業預測,2024-2031 年屋頂材料市場規模、佔有率和成長分析(按產品、應用和地區):產業預測(2024-2031)

屋頂材料市場規模、佔有率和成長分析(按材料、建築類型、設計、應用、銷售管道和地區)- 2025-2032 年行業預測屋頂系統市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料、產品、建築類型、最終用戶部門、地區和競爭進行細分,2020-2030 年預測屋頂市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分,按產品類型、按應用、按地區、按競爭,2020-2030F印度屋頂:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)2024 年住宅低坡屋頂全球市場報告屋頂瓦市場規模、佔有率、成長分析,按材料類型、按建築類型、按最終用戶、按地區 - 行業預測,2024-2031 年屋頂材料市場規模、佔有率和成長分析(按產品、應用和地區):產業預測(2024-2031)