|

市場調查報告書

商品編碼

1683147

南美種子處理市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)South America Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

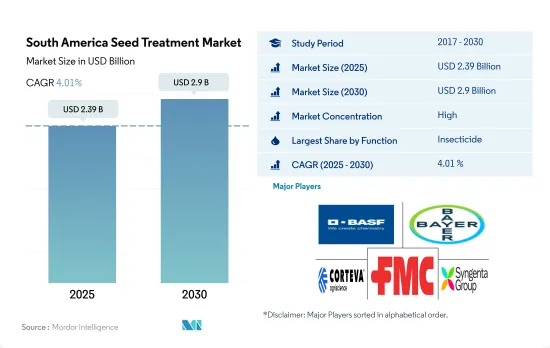

南美種子處理市場規模預計在 2025 年將達到 23.9 億美元,預計到 2030 年將達到 29 億美元,預測期內(2025-2030 年)的複合年成長率為 4.01%。

提高生產力和培育健康幼苗的需求正在推動市場成長

- 南美的種子處理產業正在經歷顯著的成長。 2022 年的市值與 2017 年相比成長了 51.7%。推動這一成長的原因是人們越來越意識到種子應用技術在保護和建立健康幼苗方面的好處,以及提高整體生產力的必要性。

- 巴西和阿根廷是著名的農業國家,廣泛使用種子處理來保護作物免受各種真菌疾病的侵害。巴西和阿根廷在種子處理市場佔有率總合的佔有率,其中巴西佔該區域市場的 77.9%,阿根廷佔約 3.1%。

- 殺蟲劑種子處理佔主要佔有率,預計 2023 年至 2029 年市值將大幅成長 35.3%。

- 近年來,由於南美洲主要作物(如大豆、玉米、小麥和水果)的真菌病害盛行,殺菌劑種子處理變得越來越重要。這些疾病包括大豆銹病、白粉病和赤黴病,對作物的產量和品質構成了嚴重風險。因此,南美洲的農民越來越依賴殺菌劑種子處理來保護作物並減少產量損失。由於這些因素,殺菌劑領域的市場規模預計在預測期內將成長 33.6%。

- 預計在預測期內,種子處理在作物保護和提高產量的接受度不斷提高,以及農民對其益處的認知不斷提高,將推動市場成長。

在生長初期保護種子和幼苗免受病蟲害侵害的需求將推動種子處理的採用

- 由於農民越來越意識到保護種子和幼苗免受早期作物病蟲害侵害的必要性,南美的種子處理市場正在經歷顯著成長。該地區的主要作物——大豆、玉米、小麥、水果和蔬菜——都適合使用種子處理劑。值得注意的是,種子處理市場在 2017-2022 年的歷史時期內表現出了 51.7% 的驚人成長率。

- 2022年,巴西成為南美洲最大的市場,佔該地區77.9%的市場佔有率。該國令人矚目的擴張歸功於多種因素,包括對糧食安全日益成長的需求以及大豆等主要作物中種子處理產品的使用日益增多。

- 阿根廷是南美洲種子處理產業第二大市場,面臨乾旱和高溫等嚴峻的環境條件。這些因素促使農民在作物生長初期採用種子處理技術。透過採用種子處理方法,農民可以促進種子更快發芽並有效控制土傳疾病。這種方法對於減輕該國惡劣氣候的不利影響至關重要,使農民能夠提高作物產量並維持永續的農業生產力。

- 預計預測期內南美種子處理市場的複合年成長率將達到 4.3%。這種成長歸因於農民越來越意識到種子處理在保護作物、提高產量和應對病蟲害帶來的早期作物生長挑戰方面發揮的巨大價值。

南美洲種子處理市場趨勢

抗病耕作機等替代方法減少了該地區每公頃種子處理劑的消費量

- 過去一段時間,每公頃種子處理劑的消費量大幅下降,與 2017 年的資料相比,2022 年的消耗量大幅下降了 1,000 克/公頃。這種下降主要是由於多種因素造成的,其中一個重要原因是耐除草劑耕作機的採用越來越多。這些分蘗經過基因改造,可以耐受除草劑的使用,讓農民無需進行額外的種子處理即可控制雜草。因此,對傳統種子處理的需求正在下降。巴西、阿根廷、巴拉圭等主要農業國家已在大豆、小麥、玉米等主要作物上採用這些耐除草劑種子。

- 除了除草劑抗性之外,基因改造作物的廣泛種植也對種子處理劑的消費產生了重大影響。基因改造作物經過改造,具有抵抗各種害蟲和疾病的特性,因此有些作物不再需要種子處理。因此,種植基改作物的農民不再依賴傳統的種子處理方法。

- 導致每公頃種子處理消費量下降的另一個重要因素是採用抗病耕作機。這些品種經過培育或基因改造,可以抵抗常見的植物疾病,從而減少了針對特定疾病的種子處理的需要。隨著越來越多的農民採用抗病耕作方法,每公頃土地使用的某些種子處理劑的整體需求量已大幅下降。

Azoxystrobin的系統運輸特性使其能夠被處理過的植物吸收,從而提供長期的害蟲防治效果。

- Cypermethrin、Metalaxyl、Malathion、Avermectin和Azoxystrobin是南美洲常用的種子處理有效成分。種子處理可以為種子和幼苗提供早期保護,防止其受到病蟲害的侵害。當你將它們播種到土壤中時,你也會在種子周圍創建一個保護屏障,保護它們免受潛在威脅。

- 作為一種接觸性殺蟲劑,Cypermethrin能夠對多種害蟲發揮快速擊倒作用,主要透過停留在經過處理的種子或植物表面並形成保護屏障。 2022 年的價格為每噸 21,100 美元。Cypermethrin的作用方式是破壞昆蟲的神經系統,導致癱瘓並最終死亡。

- Malathion的系統作用使其能夠有效控制多種害蟲,包括蚜蟲、葉蟬、薊馬、介殼蟲和某些毛蟲,2022 年其價格為每噸 124,000 美元。Malathion的作用機制涉及抑制乙醯膽鹼酯酶,這種酶對於昆蟲的正常神經功能至關重要。

- 甲霜靈 2022 年的價格為每噸 4,400 美元,可為種子和幼苗提供早期保護,防止其受到腐霉菌、疫黴菌和某些霜霉病等土壤傳播病原體的侵害。甲霜靈透過抑制真菌細胞中 RNA 的形成發揮作用。這種抑制會阻止必需蛋白質的合成並抑制真菌的生長和繁殖。

- 2022 年的價格為每噸 4,500 美元,由於Azoxystrobin的系統活性,它可以被經過處理的植物吸收並抑制真菌細胞中的線粒體呼吸,從而為植物的各個部位(包括嫩枝和葉子)提供持久保護。

南美洲種子處理產業概況

南美種子處理市場相當集中,前五大公司佔了65.66%的市場。市場的主要企業是BASF公司、拜耳公司、科迪華農業科技、富美實公司和先正達集團。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 每公頃農藥消費量

- 有效成分價格分析

- 法律規範

- 阿根廷

- 巴西

- 智利

- 價值鏈與通路分析

第5章 市場區隔

- 功能

- 殺菌劑

- 殺蟲劑

- 殺線蟲劑

- 作物類型

- 經濟作物

- 水果和蔬菜

- 糧食

- 豆類和油籽

- 草坪和觀賞植物

- 原產地

- 阿根廷

- 巴西

- 智利

- 南美洲其他地區

第6章 競爭格局

- 重大策略舉措

- 市場佔有率分析

- 業務狀況

- 公司簡介(包括全球概況、市場層級概況、主要業務部門、財務狀況、員工人數、關鍵資訊、市場排名、市場佔有率、產品和服務、最新發展分析)

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 53759

The South America Seed Treatment Market size is estimated at 2.39 billion USD in 2025, and is expected to reach 2.9 billion USD by 2030, growing at a CAGR of 4.01% during the forecast period (2025-2030).

The need to improve productivity and establish healthy seedlings is fueling the growth of the market

- The South American seed treatment industry is experiencing significant growth. The market value increased by 51.7% in 2022 compared to 2017. This growth was driven by growing awareness of the benefits of seed-applied technologies in protecting and establishing healthy seedlings and the need to improve overall productivity.

- Brazil and Argentina are prominent agricultural nations that heavily utilize seed treatments to protect their crops from a range of fungal diseases. The combined market share of seed treatments in Brazil and Argentina is significant, with Brazil accounting for 77.9% and Argentina accounting for around 3.1% of the regional market.

- The insecticide seed treatments held the major share, and their market value is expected to increase significantly by 35.3% between 2023 and 2029 because of the growing recognition of the effectiveness of seed treatments in combatting insect vectors and safeguarding crop productivity.

- Fungicide seed treatment in South America has gained significant importance in recent years due to the prevalence of fungal diseases that affect key crops like soybeans, corn, wheat, and fruits. These diseases, including soybean rust, powdery mildew, and Fusarium head blight, pose a significant risk to crop yields and quality. Consequently, farmers in South America are increasingly relying on fungicide seed treatments to safeguard their crops and reduce yield losses. These factors are expected to increase the market value of the fungicide segment by 33.6% during the forecast period.

- The growing acceptance of seed treatment to enhance crop protection and yield, coupled with the increasing awareness among farmers regarding its advantages, is anticipated to drive the market's growth in the forecast period.

The need to protect seeds and seedlings from early-growth pests and diseases will increase the adoption rate of seed treatment

- The seed treatment market in South America is experiencing significant growth, driven by the increasing awareness among farmers regarding the need to protect seeds and seedlings from early crop diseases and insect pests. The region's major crops, including soybean, maize, wheat, fruits, and vegetables, have embraced seed treatment applications. Notably, the market for seed treatment exhibited impressive growth of 51.7% over the historical period spanning from 2017 to 2022.

- In 2022, Brazil held the dominant position as the largest market in South America, representing 77.9% of the region's market share. The country's remarkable expansion can be attributed to several factors, including the growing need for food security and the escalating utilization of seed treatment products in key crops like soybeans.

- Argentina, the second-largest market in the South American seed treatment industry, experiences challenging environmental conditions such as drought and hot temperatures. These factors drove farmers to adopt seed treatment techniques during the early stages of crop growth. By employing seed treatment methods, farmers can promote faster germination and effectively control soil-borne diseases. This approach proves crucial in mitigating the adverse effects of the country's harsh climate, enabling farmers to enhance crop yields and sustainably maintain agricultural productivity.

- The South American seed treatment market is projected to register a CAGR of 4.3% during the forecast period. This growth can be attributed to the increasing recognition among farmers regarding the immense value offered by seed treatments in safeguarding their crops, enhancing yields, and countering early crop growth challenges posed by infestations.

South America Seed Treatment Market Trends

Alternative approaches like disease-resistant cultivators reduce the seed treatment consumption per hectare in the region

- Over the historical period, there was a remarkable decrease in the consumption of seed treatments per hectare, with a significant reduction of 1,000 g per ha noted in 2022 when compared to the data from 2017. This decline was primarily attributed to various factors, including one of the pivotal reasons contributing to the decline in seed treatment usage is the increasing adoption of herbicide-resistant cultivators. These cultivators are genetically engineered to withstand the application of herbicides, allowing farmers to control weeds without the need for additional seed treatments. As a result, the demand for conventional seed treatments has reduced. Major agricultural countries like Brazil, Argentina, and Paraguay adopt these herbicide resistance cultivators in their major crops like soybeans, wheat, and maize.

- In addition to herbicide resistance, the widespread cultivation of genetically modified crops has significantly impacted seed treatment consumption. Genetically modified crops are engineered to possess built-in traits that offer resistance to various pests and diseases, rendering some seed treatments unnecessary for these crops. Consequently, farmers planting genetically modified crops have reduced their reliance on traditional seed treatments.

- Another crucial factor contributing to the decline in seed treatment consumption per hectare is the adoption of disease-resistant cultivators. These cultivators have been bred or engineered to resist common plant diseases, thereby reducing the need for disease-specific seed treatments. As more farmers adopt disease-resistant cultivators, the overall demand for certain types of seed treatment usage per hectare has decreased significantly.

Azoxystrobin's systemic activity allows it to be absorbed by treated plants, providing extended protection

- Cypermethrin, metalaxyl, malathion, abamectin, and azoxystrobin are commonly used active ingredients in seed treatment chemicals in South America. Seed treatment provides early protection to seeds and seedlings against pests and diseases. It creates a protective barrier around the seed, shielding it from potential threats as soon as it is sown in the soil.

- Cypermethrin, as a contact insecticide, remained primarily on the surface of treated seeds or plants, forming a protective barrier for quick knockdown action against a wide range of insect pests. It was priced at USD 21.1 thousand per metric ton in 2022. The mode of action of cypermethrin involves disrupting the nervous systems of insects, leading to paralysis and, ultimately, their death.

- Malathion's systemic action enabled effective control of diverse insect pests, including aphids, leafhoppers, thrips, scales, and certain caterpillar species, with a price of USD 124 thousand per metric ton in 2022. Malathion's mode of action involves inhibiting acetylcholinesterase, an enzyme essential for proper nerve function in insects.

- Metalaxyl, priced at USD 4.4 thousand per metric ton in 2022, provided early protection to seeds and seedlings from soil-borne pathogens such as Pythium, Phytophthora, and certain downy mildews. Metalaxyl works by inhibiting the formation of RNA in fungal cells. This disruption prevents the synthesis of essential proteins, leading to the inhibition of fungal growth and reproduction

- With a price of USD 4.5 thousand per metric ton in 2022, azoxystrobin's systemic activity allowed it to be absorbed by treated plants, providing extended protection to different plant parts, including new growth and foliage, by inhibiting the mitochondrial respiration in fungal cells.

South America Seed Treatment Industry Overview

The South America Seed Treatment Market is fairly consolidated, with the top five companies occupying 65.66%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.3.3 Chile

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Insecticide

- 5.1.3 Nematicide

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Chile

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 FMC Corporation

- 6.4.5 Sumitomo Chemical Co. Ltd

- 6.4.6 Syngenta Group

- 6.4.7 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

亞太種子處理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美種子處理市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印度種子處理:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲種子處理:市場佔有率分析、行業趨勢和成長預測(2025-2030)種子處理:市場佔有率分析、產業趨勢與成長預測(2025-2030)稻米種子處理:市場佔有率分析、產業趨勢與成長預測(2025-2030)美國種子處理:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

亞太種子處理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美種子處理市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印度種子處理:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲種子處理:市場佔有率分析、行業趨勢和成長預測(2025-2030)種子處理:市場佔有率分析、產業趨勢與成長預測(2025-2030)稻米種子處理:市場佔有率分析、產業趨勢與成長預測(2025-2030)美國種子處理:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 2025 年全球種子處理市場報告

2025 年全球種子處理市場報告 2025 年至 2033 年種子處理市場規模、佔有率、趨勢及預測(按類型、應用技術、作物類型、功能和地區分類)

2025 年至 2033 年種子處理市場規模、佔有率、趨勢及預測(按類型、應用技術、作物類型、功能和地區分類) 種子處理市場:2033 年市場分析與預測 - 按類型、產品、技術、應用、形式、原材料類型、最終用戶、階段、功能

種子處理市場:2033 年市場分析與預測 - 按類型、產品、技術、應用、形式、原材料類型、最終用戶、階段、功能

▼