|

市場調查報告書

商品編碼

1686297

亞太種子處理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Asia Pacific Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

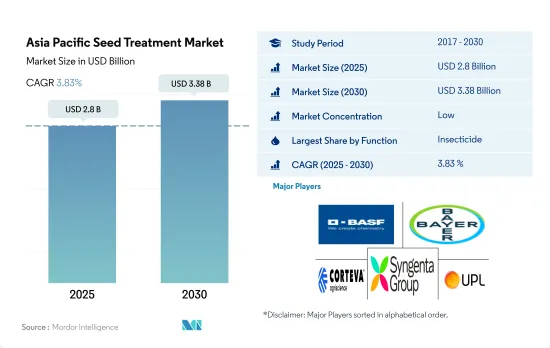

亞太種子處理市場規模預計在 2025 年為 28 億美元,預計到 2030 年將達到 33.8 億美元,預測期內(2025-2030 年)的複合年成長率為 3.83%。

由於種子易受土壤中昆蟲的侵害,殺蟲劑在亞太地區的種子處理市場中佔據主導地位

- 種子處理已成為亞太地區保護種子、提升作物表現的重要做法。這些處理有助於控制種子傳播的疾病、害蟲和線蟲,確保幼苗健康並改善作物生長。

- 種子處理市場的規模在歷史時期內成長了29.2%。這種上升趨勢的動力是人們越來越意識到種子處理對保護幼苗、促進生長和生產力的好處。

- 中國和印度是亞太地區種子處理化學品市場的主要農業國家。中國約佔該地區市值的 16.8%,而印度在 2022 年約佔 12.4% 的市場佔有率。

- 殺蟲劑種子處理將佔據市場主導地位,到 2022 年將佔亞太地區種子處理市場的 77.6%。昆蟲會對種子和幼苗造成嚴重損害,導致幼苗生長不良、發芽有限和產量下降。使用殺蟲劑種子處理可以防止這些害蟲的破壞,從而使幼苗更加健康、更有活力。

- 在種子上施用殺菌劑可以形成保護屏障,有助於預防和控制猝倒病、幼苗猝倒病和根腐病等疾病。 2022 年,殺菌劑種子處理將佔據亞太地區殺菌劑市場的很大佔有率,達到 21.2%。

- 預計預測期內(2023-2029 年),市場複合年成長率為 4.0%。預計這一成長主要將受到為滿足不斷成長的人口需求而不斷成長的糧食生產需求的推動。為了提高作物產量並減少病蟲害造成的損失,農民擴大採用種子處理。

在生長早期階段保護種子和幼苗免受病蟲害侵害的需求可能會導致種子處理的應用增加。

- 由於農民越來越意識到保護種子和幼苗免受早期作物病蟲害侵害的必要性,亞太地區的種子處理市場正在經歷顯著成長。該地區主要作物(包括水稻、小麥、芒果、葡萄、香蕉和棉花)的農民都採用了種子處理技術。

- 2022年,中國將成為亞太地區領先市場,佔16.7%的顯著市場。這一優勢是由多種因素共同推動的,這些因素推動了該國的快速成長。這些因素包括對糧食安全的需求日益成長,以及水稻和小麥等作物種子處理產品的採用日益增加。

- 亞太地區的種子處理市場以穀物和穀類作物為主。到2022年,該部分將佔整個市場的50.3%。這一優勢可能是因為穀類是該地區的主要作物,而且相當一部分農業用地用於種植穀類。由於其經濟重要性以及對各種病蟲害的高度敏感性,種子處理在生長早期保護穀物和穀類方面發揮著至關重要的作用。

- 在亞太地區,不斷成長的糧食需求推動了種植面積的增加。農民經常在同一塊土地上重複種植或增加每年種植的作物數量。這種強化增加了各種種子傳播疾病和昆蟲爆發的風險,導致種子處理的使用增加。預測期內(2023-2029 年),亞太地區的種子處理市場預計將大幅成長,複合年成長率為 4.0%。

亞太地區種子處理市場趨勢

種子和幼苗保護意識的增強推動了種子處理農藥的消費

- 2022 年亞太地區種子處理劑的平均消費量將達到每公頃 261.08 克。近年來,種子處理劑因其在保護和提高作物生產力方面的有效性和效率而變得越來越受歡迎。

- 隨著亞太國家農業實踐的強化和對更高生產率的需求不斷成長,該地區的農民越來越意識到作物保護作為保護作物免受疾病、害蟲和其他壓力的有效手段的重要性,從而降低產量損失的風險。

- 種子處理可保護作物免受多種真菌疾病的侵害,包括種子腐爛、幼苗猝倒病、猝倒病、根腐病以及葉面疾病,如白粉病、霜霉病和早疫病。活性成分的使用是有幫助的,因為它是基於目標疾病和種子處理要求。Metalaxyl、Carbendazim和Captan是亞太市場種子處理產品中使用最廣泛的活性成分。

- 種子處理也用於防治害蟲和線蟲。例如,根結線蟲是影響水果和蔬菜作物的最危險的線蟲種類,已知可造成產量損失34%,馬鈴薯產量損失26%,番茄產量損失23%,檳榔產量損失22%,茄子產量損失21%,但可以透過種子處理有效減輕。

- 亞太國家的種子處理產業正在經歷技術進步,以實現更精確、更有效率的種子處理應用。這些進步包括改進的種子處理配方和先進的種子處理設備,導致該地區農民更多地使用種子處理。

亞太地區各政府機構加大促銷活動,推動需求及物價上漲

- 種子處理在保護種子和幼苗免受影響作物出苗和生長的種子和土壤傳播的疾病和害蟲侵害方面發揮著重要作用。Cypermethrin、Avermectin、Azoxystrobin、Malathion和Metalaxyl是亞太地區最常用的種子處理化學品。

- Cypermethrin是一種非系統性土壤作用型擬除蟲菊酯殺蟲劑。它被用作種子處理劑,以減少秋冬播種的小麥和大麥的球莖和金針蟲的損害。 2022 年的價格為每噸 21,000 美元。

- Avermectin屬於伊維菌素家族,對線蟲具有強烈的內在活性。它用於玉米、大豆和棉花生產中,以保護幼苗免受線蟲侵害根部。 2022 年的價格為每噸 8,700 美元。

- Azoxystrobin是一種廣譜預防性種子處理殺菌劑,具有系統性作用,建議用於控制導致產量減產的子實體真菌、真菌、子囊菌和擔子菌。 2022年Azoxystrobin價格為每噸4,500美元。

- 各種政府法規鼓勵使用種子處理來提高種子的適銷性。印度政府決定在全國範圍內開展宣傳活動,確保喀拉拉夫季節所有重要作物的種子處理覆蓋率達到 100%。農藥產業協會、ATMA、CIPMC、KVK、農民俱樂部、SAU、非政府組織等可以在 100% 種子處理宣傳活動中發揮重要作用。這些努力可能會在未來幾年進一步影響該地區的種子處理價格。

亞太地區種子處理產業概況

亞太種子處理市場較為分散,前五大企業佔33.38%的市佔率。市場的主要企業是:BASF公司、拜耳公司、科迪華農業科技、先正達集團和 UPL 有限公司(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 每公頃農藥消費量

- 有效成分價格分析

- 法律規範

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 緬甸

- 巴基斯坦

- 菲律賓

- 泰國

- 越南

- 價值鏈與通路分析

第5章 市場區隔

- 功能

- 殺菌劑

- 殺蟲劑

- 殺線蟲劑

- 作物類型

- 經濟作物

- 水果和蔬菜

- 糧食

- 豆類和油籽

- 草坪和觀賞植物

- 原產地

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 緬甸

- 巴基斯坦

- 菲律賓

- 泰國

- 越南

- 其他亞太地區

第6章 競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- Crystal Crop Protection Ltd

- FMC Corporation

- Nufarm Ltd

- PI Industries

- Syngenta Group

- UPL Limited

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 51830

The Asia Pacific Seed Treatment Market size is estimated at 2.8 billion USD in 2025, and is expected to reach 3.38 billion USD by 2030, growing at a CAGR of 3.83% during the forecast period (2025-2030).

Insecticides dominated the Asia-Pacific seed treatment market as seeds are more susceptible to soil-borne insects

- Seed treatment is an important practice in Asia-Pacific to protect seeds and enhance crop performance. These treatments help control seed-borne diseases, pests, and nematodes, ensuring healthy seedlings and improved crop establishment.

- The market value of seed treatment experienced a growth of 29.2% during the historical period. This upward trend can be attributed to the increasing recognition of the advantages offered by seed treatment for protecting and enhancing the growth of seedlings and their productivity.

- China and India are the leading agricultural nations that hold a significant share of seed treatments in the Asia-Pacific market. China constituted approximately 16..8% of the regional market value, while India held around 12.4% market share in 2022.

- Insecticide seed treatment dominated the market, accounting for 77.6% of the Asia-Pacific seed treatment market in 2022. Insects can severely damage seeds and seedlings, which can result in poor stand establishment, limited germination, and yield losses. Insecticide seed treatments prevent the damage posed by these pests, resulting in seedlings that are healthier and more vigorous.

- Fungicides applied to seeds form a protective barrier that aids in the prevention and control of diseases such as damping off, seedling blight, and root rot. Fungicide seed treatment held a significant share of 21.2% in the Asia-Pacific fungicide market in 2022.

- The market is expected to grow during the forecast period (2023-2029), registering a CAGR of 4.0%. This growth is primarily anticipated to be driven by the rising demand for food production to meet the needs of a growing population. In order to optimize crop yields and minimize losses due to diseases and insects, farmers are increasingly adopting seed treatments.

The need to protect seeds and seedlings from early-growth pests and diseases may increase the seed treatment adoption rate

- The seed treatment market in Asia-Pacific is experiencing significant growth, driven by farmers' increasing awareness of the need to protect seeds and seedlings from early crop diseases and insect pests. Farmers of the region's major crops, including rice, wheat, mangoes, grapes, bananas, and cotton, are adopting seed treatment applications.

- In 2022, China emerged as the leading market within Asia-Pacific, accounting for a substantial share of 16.7% of the market. This dominance can be attributed to a combination of factors that fueled the country's impressive growth. These factors include the increasing imperative for ensuring food security and the escalating adoption of seed treatment products in crops such as rice and wheat.

- The grains & cereals segment dominates the Asia-Pacific seed treatment market. In 2022, the segment accounted for 50.3% of the market's total value. This dominance can be because they are staple crops in the region, and a significant portion of agricultural land is dedicated to their cultivation. Due to their economic importance and high susceptibility to various pests and diseases, seed treatment plays a vital role in protecting grains and cereals during the early stages of growth.

- Crop intensity has been rising in Asia-Pacific as a result of increased food demand. Farmers often practice repeated cropping or intensify the number of crop cycles per year on the same land. This intensification leads to a higher risk of various seed-borne diseases and insect outbreaks, resulting in an increase in seed treatment usage. The Asia-Pacific seed treatment market is projected to witness significant growth during the forecast period (2023-2029) and register a CAGR of 4.0%.

Asia Pacific Seed Treatment Market Trends

The growing awareness to protect seeds and seedlings is driving the consumption of seed treatment pesticides

- The average consumption of seed treatment chemicals in Asia-Pacific was 261.08 grams per hectare in 2022. Seed treatment has become increasingly popular in recent years due to its effectiveness and efficiency in protecting and enhancing crop productivity.

- As agricultural practices in these countries are intensifying and the need for higher productivity is growing, Asia-Pacific farmers are becoming more aware of the importance of crop protection as an effective means of protecting crops from diseases, pests, and other stresses, thereby reducing the risk of yield loss.

- Seed treatment can prevent and offer protection to crops against several fungal diseases, including seed rot, seedling blight, damping off, root rot, and foliar diseases like powdery mildew, downy mildew, and early blight. The use of active ingredients helps as they are based on target diseases and seed treatment requirements. Metalaxyl, carbendazim, and captan are the most used active ingredients in seed treatment products in the Asia-Pacific market.

- Seed treatments are also being used against insect pests and nematodes. For instance, the root-knot nematode is the most dangerous among the nematode species that affect fruit and vegetable crops and is known to cause a yield loss of 34% in carrots, 26% in potatoes, 23% in tomatoes, 22% in bottle gourds, and 21% in brinjal, which can effectively be mitigated by seed treatment practices.

- The seed treatment industry in Asia-Pacific countries is witnessing technological advancements that enable more precise and efficient seed treatment applications. These advancements include improved seed treatment formulations and advanced seed treatment equipment, leading to higher usage of seed treatment chemicals by farmers in the region.

Increasing promotional activities by various government agencies across Asia-Pacific drives the demand and price

- Seed treatment plays an important role in protecting seeds and seedlings from seed and soil-borne diseases and insect pests affecting crop emergence and growth. Cypermethrin, abamectin, azoxystrobin, malathion, and metalaxyl are the most commonly used seed treatment chemicals in Asia-Pacific.

- Cypermethrin is a non-systemic soil-acting pyrethroid insecticide. It is used in seed treatment for the reduction of wheat bulb fly and wireworm damage to autumn/winter sown wheat and barley. It was valued at a price of USD 21.0 thousand per metric ton in 2022.

- Abamectin belongs to the ivermectin chemical class and has high intrinsic activity against nematodes. It is used to protect young plants from root-attacking nematodes in corn, soybean, and cotton production. It was priced at USD 8.7 thousand per metric ton in 2022.

- Azoxystrobin is a broad-spectrum preventative seed treatment fungicide with systemic properties recommended for the control of Deuteromycetes, Oomycetes, Ascomycetes, and Basidiomycetes fungi that cause yield losses in crops. In 2022, azoxystrobin was priced at USD 4.5 thousand per metric ton.

- Various regulations by government agencies are encouraging the use of seed treatments to increase the marketability of seeds. The Government of India has decided to launch a countrywide campaign for ensuring 100% seed treatment in all important crops during the kharif season. Pesticide industry associations, ATMAs, CIPMCs, KVKs, farmers clubs, SAUs, NGOs, etc., can play an important role in the campaign promoting 100% seed treatment. Such initiatives may further affect the price of seed treatment chemicals in the region over the coming years.

Asia Pacific Seed Treatment Industry Overview

The Asia Pacific Seed Treatment Market is fragmented, with the top five companies occupying 33.38%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Myanmar

- 4.3.7 Pakistan

- 4.3.8 Philippines

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Insecticide

- 5.1.3 Nematicide

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Myanmar

- 5.3.7 Pakistan

- 5.3.8 Philippines

- 5.3.9 Thailand

- 5.3.10 Vietnam

- 5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Crystal Crop Protection Ltd

- 6.4.6 FMC Corporation

- 6.4.7 Nufarm Ltd

- 6.4.8 PI Industries

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

北美種子處理市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)南美種子處理市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印度種子處理:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲種子處理:市場佔有率分析、行業趨勢和成長預測(2025-2030)種子處理:市場佔有率分析、產業趨勢與成長預測(2025-2030)稻米種子處理:市場佔有率分析、產業趨勢與成長預測(2025-2030)美國種子處理:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

北美種子處理市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)南美種子處理市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印度種子處理:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲種子處理:市場佔有率分析、行業趨勢和成長預測(2025-2030)種子處理:市場佔有率分析、產業趨勢與成長預測(2025-2030)稻米種子處理:市場佔有率分析、產業趨勢與成長預測(2025-2030)美國種子處理:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 2025 年全球種子處理市場報告

2025 年全球種子處理市場報告 2025 年至 2033 年種子處理市場規模、佔有率、趨勢及預測(按類型、應用技術、作物類型、功能和地區分類)

2025 年至 2033 年種子處理市場規模、佔有率、趨勢及預測(按類型、應用技術、作物類型、功能和地區分類) 種子處理市場:2033 年市場分析與預測 - 按類型、產品、技術、應用、形式、原材料類型、最終用戶、階段、功能

種子處理市場:2033 年市場分析與預測 - 按類型、產品、技術、應用、形式、原材料類型、最終用戶、階段、功能

▼