|

市場調查報告書

商品編碼

1685806

稻米種子處理:市場佔有率分析、產業趨勢與成長預測(2025-2030)Rice Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

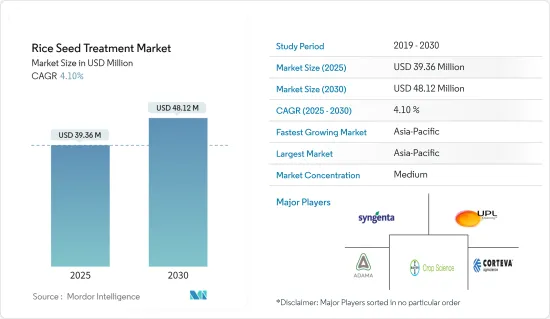

預計 2025 年水稻種子處理市場規模為 3,936 萬美元,到 2030 年將達到 4,812 萬美元,預測期內(2025-2030 年)的複合年成長率為 4.10%。

種子處理可以保護種子和幼苗免受影響作物出苗和生長的種子和土壤傳播的疾病和害蟲的侵害。為了使稻農能夠在全球範圍內採用這種處理方法,需要有效的推廣策略,包括獲得適當的化學/生物農藥和設備,以及了解種子處理方法和後處理程序。在稻米種植中,化學種子處理主要用於種子改良和保護。

全球範圍內都在進行種子處理,以生產無蟲害種子,使用能夠在整個作物週期內防止害蟲發芽的產品。根據美國農業部的資料,2023-2024會計年度米總產量預計將達到5.227億噸。中國佔產量的28%,其次是印度(26%)、孟加拉(7%)、印尼(6%)和越南(5%)。

根據美國農業部報告,預計2024-2025會計年度全球稻米產量將達到創紀錄的5.337億噸(碾米基數),增加1,100萬噸。阿根廷、巴西和台灣的產量數據被上調,而澳洲、哥斯大黎加、古巴、歐盟、宏都拉斯、尼泊爾、巴拿馬、菲律賓和韓國的產量預測則被下調。預計2024-2025年全球稻米消費量及剩餘使用量將達5.303億噸,比上年度增加620萬噸。稻米種子處理市場的成長得益於稻米作為主食的消費量不斷增加、優質種子採用率不斷提高、政府對種子產業的支持以及種子處理技術的進步,以減少水稻病蟲害的侵染。

稻米種子處理市場趨勢

優質種子的需求和採用不斷增加

農民越來越接受種子處理作為保護其在優質種子上的昂貴投資的一種方式。由於對具有理想農藝性狀的優質種子的需求不斷增加,種子成本也在上升。公司和農民都願意在種子處理解決方案上花費額外的錢來保存昂貴的高品質種子。

基因改造種子的引入使得種子的附加價值很高,種子的成本也很高,有時甚至是非基因改造種子的兩倍。此前,農民預計產量只能增加 85%,因為有些種子會腐爛或受到昆蟲的侵襲。隨著趨勢的變化,種子處理變得至關重要,種植者希望即使在惡劣的條件下也能 100% 的種子出苗。新興市場的關鍵參與者不斷專注於透過現代育種技術開發優質種子,從而提高種子的成本。

市場的主要企業正專注於透過現代育種技術開發優質種子,從而提高種子成本。未能發芽或被昆蟲損壞的種子必須重新種植,這可能會很昂貴。此外,所需的高昂勞動成本也增加了總成本。根據糧食及農業組織的數據,2022 年穀物產量為每公頃 4,182.4 公斤,高於前一年的每公頃 4,152.2 公斤。因此,農民需要經過精心加工的高品質種子來提高有限作物面積的產量,並滿足日益成長的需求。

非洲國家米產量不足,依賴進口。塞拉利昂就是這樣一個國家。因此,為了實現自給自足,政府採取了多種策略。一個有希望的解決方案是廣泛使用新非洲稻(NERICA)等產量品種。 NERICA 被非洲稻農譽為奇蹟作物,因為它結合了亞洲水稻(產量)和非洲水稻(抗旱、抗病)的基因特性。然而,目前的估計表明,只有 2% 的非洲農民使用 NERICA。這是因為改良品種的價格比傳統品種高出40%至100%,這對貧困農民採用NERICA造成了重大障礙。因此,由於這些雜交品種的成本較高,稻農有機會以可負擔的成本使用經過處理的種子。預計這將在未來幾年推動水稻種子處理市場實現積極成長。

亞太地區佔市場主導地位

2023 年,亞太地區佔據水稻種子處理領域最大的市場佔有率,這得益於水稻作為主要主食和種植作物最大的作物。中國已成為該地區最大、成長最快的市場,其次是印度和日本。中國是僅次於美國的世界第二大種子市場,2021年種子年產量達1,200萬噸,市場價值達190億美元。根據美國農業部的資料,2022年全球雜交稻種子產量將達16.8萬噸,平均產量為每公頃2160公斤。

根據中國農業部報道,水稻種子產業正在優先發展差別化商業品種,以解決當前水稻品種產量、低抗性(特別是抗稻瘟病)的限制。中國注重提高種子價值,從而促進了雜交品種的開發。稻米仍然是中國的主要作物,根據糧農組織的資料,預計到 2022 年,稻米產量將達到 2.1 億噸,種植面積為 2,970 萬公頃。國家稻米產量的擴大和糧食需求的增加繼續推動稻米種子處理市場的成長。

印度是世界第二大稻米生產國和主要稻米出口國。該國多樣的海拔和氣候條件適合廣泛種植水稻。根據ITC Trade Map的資料,2023年印度米出口量將達到1,050萬噸,佔全球出口量的32.5%,成為全球最大的米出口國。該國良好的氣候和農業實踐提高了水稻產量,增強了對水稻種子處理劑的需求。受食品需求不斷成長和持續研發創新產品的推動,區域稻米種子處理市場預計將保持穩定成長。

稻米種子處理產業概況

稻米種子處理市場正在整合,預計到 2023 年,少數幾家大公司將佔據市場佔有率的主導地位。拜耳股份公司、先正達國際股份公司、UPL 有限公司、安道麥農業解決方案有限公司和科迪華農業科技是該市場的主要企業。這些公司主要專注於新產品的發布、合作和收購。投資研發和開發創新產品系列仍是市場成長的重要策略。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概覽

- 市場促進因素

- 優質種子的需求和採用不斷增加

- 作物保護產業的技術發展

- 政府加大對種子處理的支持

- 市場限制

- 日益嚴重的環境問題

- 農場級種子處理的局限性

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場區隔

- 應用

- 化學

- 非化學/生物

- 功能

- 種子保護

- 種子增強

- 其他功能

- 應用科技

- 種子披衣

- 種子丸粒化

- 拌種

- 其他應用技術

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 西班牙

- 英國

- 法國

- 德國

- 俄羅斯

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 非洲

- 南非

- 世界其他地區和非洲

- 北美洲

第6章 競爭格局

- 最受歡迎的策略

- 市場佔有率分析

- 公司簡介

- Adama Agricultural Solutions Ltd

- Yara International ASA

- Bayer AG

- Indofill Industries Limited

- Dhanuka Agritech Limited

- Corteva Agriscience

- Croda International(INCOTEC)

- Crystal Crop Protection Limited

- UPL Limited

- Nufarm Limited

- Syngenta AG

第7章 市場機會與未來趨勢

The Rice Seed Treatment Market size is estimated at USD 39.36 million in 2025, and is expected to reach USD 48.12 million by 2030, at a CAGR of 4.10% during the forecast period (2025-2030).

Seed treatment protects seeds and seedlings from seed and soil-borne diseases and insect pests that affect crop emergence and growth. The global adoption of this practice among rice farmers requires effective extension strategies, including access to appropriate chemical pesticides/bio-pesticides and equipment, along with knowledge of seed treatment methods and post-treatment handling procedures. In rice cultivation, chemical seed treatment is primarily used for seed enhancement and protection.

Seed treatment is implemented globally to produce pest and disease-free seeds using products that protect against pests and diseases throughout germination and the crop cycle. According to USDA data, total rice production reached 522.7 million metric tons during MY 2023-2024. China contributed 28% of this production, followed by India at 26%, Bangladesh at 7%, Indonesia at 6%, and Vietnam at 5%.

USDA reports indicate that global rice production for MY 2024-2025 is projected to reach a record 533.7 million metric tons (milled basis), an increase of 11 million metric tons. While Argentina, Brazil, and Taiwan received upward production revisions, forecasts were reduced for Australia, Costa Rica, Cuba, the European Union, Honduras, Nepal, Panama, the Philippines, and South Korea. Global rice consumption and residual use in MY 2024-2025 is anticipated to reach 530.3 million metric tons, increasing by 6.2 million metric tons from the previous year. The rice seed treatment market growth is driven by increasing rice consumption as a staple food, higher adoption of high-quality seeds, government support in the seed industry, and technological advancements in seed treatment for reducing rice diseases and pest infestation.

Rice Seed Treatment Market Trends

Increasing Demand and Adoption of High-Quality Seeds

Farmers are increasingly acknowledging seed treatment as a mode to protect high investments made in good quality seeds. Owing to the increasing demand for high-quality seeds with desirable agronomic traits, the cost of seeds is increasing. Both companies and farmers are ready to spend extra on seed treatment solutions to save costly high-quality seeds.

The introduction of GM seeds added high value to seeds, with the cost of seeds being high and sometimes being twice as much as that of non-GM seeds. Earlier, a growth of 85% was anticipated by farmers as some seeds would rot or be destroyed by insects. With changing trends and 100% seed emergence expectations by growers even in unfavorable conditions, seed treatment has become a necessity. The key players in the market are constantly focusing on developing superior-quality seeds through modern breeding techniques, thereby increasing the cost of the seeds.

Top players in the market are focusing on the development of superior quality seeds through modern breeding techniques, thereby increasing the seed cost. Replanting seeds due to poor germination and insect attack is expensive. Moreover, the high cost of labor requirements is associated with overall cost. According to the Food and Agriculture Organization, the total crop yield of cereals accounted for 4,182.4 kg/ha in 2022, which is higher than the previous year at 4,152.2 kg/ha. Hence to meet the growing demand, farmers need quality seeds that are well-treated to enhance the yield in limited harvested areas.

African countries do not produce enough rice and are reliant on imports. One such country is Sierra Leone. Hence, to become self-sufficient, the country's government is adopting a few strategies. A promising solution is the dissemination of high-yielding rice varieties, such as the New Rice of Africa (NERICA), which have become known as the miracle crop for African rice farmers because they combine the genetic qualities of Asian rice (high yielding) and African rice (high resistance to drought and disease). However, current estimates suggest only 2% of farmers in the country use NERICAs. This is due to the cost of improved varieties that cost 40-100% more than traditional ones, representing a significant barrier to adoption among poor farmers. Hence, due to the high cost of these hybrid varieties, there is an opportunity for paddy farmers to use treated seeds at an affordable cost. This, in turn, is anticipated to lead to the positive growth of the rice seed treatment market in the coming years.

Asia-Pacific Dominates the Market

The Asia-Pacific region held the largest market share in the rice seed treatment sector in 2023, driven by rice being the primary staple food and most cultivated crop. China emerged as the region's largest and fastest-growing market, followed by India and Japan. China represents the world's second-largest seed market after the United States, with an annual seed planting volume of 12 million metric tons and a market value of USD 19 billion in 2021. According to USDA data, global hybrid rice seed production reached 168,000 metric tons in 2022, with an average yield of 2,160 kg/ha.

The Chinese Ministry of Agriculture reports that the rice seed industry is prioritizing differentiated commercial varieties to address the limitations of current high-yield, low-resistance varieties, particularly regarding rice blast resistance. China's emphasis on seed value enhancement has resulted in increased hybrid rice variety development. Rice remains China's primary crop, with FAO data showing production of 210 million metric tons in 2022 across 29.7 million hectares. The country's expanding rice production and growing food demand continue to drive the rice seed treatment market growth.

India maintains its position as the world's second-largest producer and primary rice exporter. The country's diverse altitude and climatic conditions support widespread rice cultivation. ITC Trade Map data indicates that India exported 10.5 million metric tons of rice in 2023, accounting for 32.5% of global export volume and ranking as the world's leading rice exporter. The country's favorable climate and agricultural practices have increased rice production, strengthening the demand for rice seed treatment chemicals. The regional rice seed treatment market is projected to maintain steady growth, supported by increasing food demand and ongoing research and development efforts to develop innovative products.

Rice Seed Treatment Industry Overview

The rice seed treatment market is consolidated, with a few major players dominating the market share in 2023. Bayer AG, Syngenta International AG, UPL Limited, Adama Agricultural Solutions Ltd, and Corteva Agriscience are the key companies operating in the market. These companies primarily focus on new product launches, partnerships, and acquisitions. Investment in research and development and the development of innovative product portfolios remain essential strategies for market growth.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand And Adoption Of High-Quality Seeds

- 4.2.2 Technological Developments In The Crop Protection Industry

- 4.2.3 Rising Government Support For Seed Treatment

- 4.3 Market Restraints

- 4.3.1 Rising Environmental Concerns

- 4.3.2 Limitations Across Farm-Level Seed Treatment

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Chemical

- 5.1.2 Non-chemical/Biological

- 5.2 Function

- 5.2.1 Seed Protection

- 5.2.2 Seed Enhancement

- 5.2.3 Other Functions

- 5.3 Application Techniques

- 5.3.1 Seed Coating

- 5.3.2 Seed Pelleting

- 5.3.3 Seed Dressing

- 5.3.4 Other Application Techniques

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Spain

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Germany

- 5.4.2.5 Russia

- 5.4.2.6 Italy

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Rest of and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Adama Agricultural Solutions Ltd

- 6.3.2 Yara International ASA

- 6.3.3 Bayer AG

- 6.3.4 Indofill Industries Limited

- 6.3.5 Dhanuka Agritech Limited

- 6.3.6 Corteva Agriscience

- 6.3.7 Croda International (INCOTEC)

- 6.3.8 Crystal Crop Protection Limited

- 6.3.9 UPL Limited

- 6.3.10 Nufarm Limited

- 6.3.11 Syngenta AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

亞太種子處理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太種子處理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 北美種子處理市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

北美種子處理市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 南美種子處理市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

南美種子處理市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 印度種子處理:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

印度種子處理:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 歐洲種子處理:市場佔有率分析、行業趨勢和成長預測(2025-2030)

歐洲種子處理:市場佔有率分析、行業趨勢和成長預測(2025-2030) 種子處理:市場佔有率分析、產業趨勢與成長預測(2025-2030)

種子處理:市場佔有率分析、產業趨勢與成長預測(2025-2030) 美國種子處理:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

美國種子處理:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 2025 年全球種子處理市場報告

2025 年全球種子處理市場報告 2025 年至 2033 年種子處理市場規模、佔有率、趨勢及預測(按類型、應用技術、作物類型、功能和地區分類)

2025 年至 2033 年種子處理市場規模、佔有率、趨勢及預測(按類型、應用技術、作物類型、功能和地區分類) 種子處理市場:2033 年市場分析與預測 - 按類型、產品、技術、應用、形式、原材料類型、最終用戶、階段、功能

種子處理市場:2033 年市場分析與預測 - 按類型、產品、技術、應用、形式、原材料類型、最終用戶、階段、功能