|

市場調查報告書

商品編碼

1683199

自動駕駛卡車:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Autonomous Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

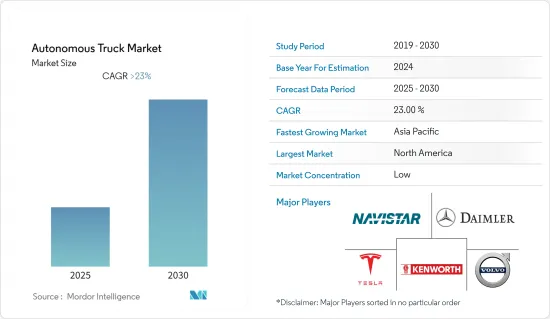

預測期內,自動駕駛卡車市場預計將以超過 23% 的複合年成長率成長。

與整個產業相比,COVID-19 疫情對汽車產業這一領域的影響相對較小。疫情封鎖和全球交通停頓在一定程度上阻礙了自動駕駛卡車的需求。不過,隨著市場和貿易的逐步開放,以及對自動化的需求不斷增加,自動駕駛卡車市場有望實現經濟復甦。

主要亮點

- 推動市場成長的關鍵因素包括新興市場工業部門的擴張、物流行業的需求增加以及建築業的需求增加(由於建設活動增加)。由於新興經濟體和已開發經濟體的經濟成長,預計未來幾年市場將會成長。

- 自動駕駛卡車在便利性方面具有取代傳統卡車的巨大潛力,但生產成本、缺乏適當的基礎設施、政府法規和政策不足以及通勤者和行人的安全問題阻礙因素了它們的發展。已報告 36 起涉及自動駕駛汽車的事故。

- 對車輛安全的需求不斷成長以及嚴格的政府法規正在推動 ADAS 市場的成長。美國公路交通安全管理局 (NHTSA) 要求到 2022 年 9 月 1 日,所有重量在 8,501 至 10,000 磅之間的卡車都必須配備自動緊急煞車系統。英國還建立了網聯和自動駕駛汽車中心(CAV),並致力於制定允許在高速公路和道路上進行車輛測試的法律法規。

自動駕駛卡車市場趨勢

ADAS 需求不斷上升

消費者意識的不斷增強推動了對具有自動駕駛功能和先進安全功能的車輛的需求。 90% 為車輛選擇 ADAS 系統的客戶會成為回頭客。政府的規範和政策也在推動 ADAS 市場的銷售。美國和歐洲當局計劃在 2022 年強制實施汽車緊急煞車 (AEB),並在 2020 年正面防撞/警告系統。

只有昂貴的豪華車才配備完整的 ADAS 系統。許多卡車OEM正在與 ADAS 製造商合作生產低成本的 ADAS 系統。然而,雖然汽車(商用車和乘用車)的價格以每年 1% 的微不足道的平均速度成長,但 ADAS 系統的製造成本很高。由於OEM不願意提高中小型汽車領域的價格,ADAS 公司可能無法獲得預期的回報。這一因素可能會阻礙 ADAS 市場的成長。

各大OEM供應商均採取與科技公司合作開發ADAS的策略。 Nvidia 等科技公司已進入該領域,為Volvo和 Paccar 等公司提供服務。亞馬遜使用 Embark 自動駕駛卡車運送貨物。

過去幾十年來,被動安全領域經歷了許多創新,但新興市場仍然沒有太多改進空間。開發商目前專注於在新興市場提供最佳的被動安全性。主動式安全(預測和避免碰撞)尚處於起步階段,還有很多需要改進的地方。 ADAS技術已獲得多數參與者的早期核准,很可能在未來全自動駕駛汽車的發展中發揮關鍵作用。

北美引領自動駕駛卡車市場

雖然自動駕駛卡車在歐洲和亞太等地區處於應用的早期階段,但由於基礎設施的完善和大量科技公司進入自動駕駛領域,北美目前是最大的市場。

新興市場的汽車電氣化,以及特斯拉等公司開拓基礎建設,也推動了北美市場的發展。電動車中線控技術的引進有助於改善自動駕駛。

2021 年 9 月,PACCAR 與主要企業的自動駕駛技術公司 Aurora 合作,開始在華盛頓對用於運輸業務的自動駕駛卡車進行商業測試。該技術預計將被聯邦快遞採用。

2019 年,戴姆勒北美卡車公司與 Torc Robotics 合作,開始在維吉尼亞81 號州際公路上測試自動駕駛卡車。在 2020 年國際消費電子展 (CES) 上,肯沃斯卡車發布了基於其 T680 卡車的自動駕駛卡車技術。自動駕駛卡車將在行駛過程中使用感測器和LiDAR每小時收集多達Terabyte的資料。

自動駕駛卡車行業概況

自動駕駛卡車市場主要由以下參與者主導:戴姆勒、沃爾沃、特斯拉等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場促進因素

- 市場限制

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 購買者/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章 市場區隔

- 按類型

- 小型貨車

- 中型卡車

- 大型卡車

- 按自動化程度

- 半自動駕駛

- 完全自主

- 透過ADAS功能

- 主動式車距維持定速系統

- 車道偏離警示

- 智慧停車輔助

- 高速公路導航

- 自動緊急制動

- 盲點偵測

- 交通壅塞輔助

- 車道維持輔助系統

- 依組件類型

- 騎士

- 雷達

- 相機

- 感應器

- 按驅動類型

- 內燃機

- 電動式的

- 混合

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 世界其他地區

- 南美洲

- 中東和非洲

- 北美洲

第6章 競爭格局

- 供應商市場佔有率

- 公司簡介

- AB Volvo

- Mercedes Benz Group

- Traton SE

- TuSimple

- Fabu Technology

- Tesla Inc.

- Paccar Inc

- BYD Co. Ltd.

- Einride

- Embark

第7章 市場機會與未來趨勢

The Autonomous Truck Market is expected to register a CAGR of greater than 23% during the forecast period.

The COVID-19 pandemic had a relatively more minor impact on this automotive industry segment compared to the whole. The demand for autonomous trucks was slightly hindered due to the lockdown and global transportation halt due to the pandemic. However, with market and trade gradually opening up and the increased need for automation, the autonomous truck market is hoping for an economic revival.

Key Highlights

- Some major factors driving the growth of the market are the expansion of industrial sectors in the emerging market, growing demand from the logistics industry, and rising demand from the construction sector (owing to growing construction activities). The market is expected to witness growth in the coming years due to growing economies across developing and developed counties.

- Although autonomous/driverless trucks have a great potential to replace conventional trucks in terms of convenience-high, cost of manufacturing, lack of proper infrastructures, inadequate regulations and policies of governments, and safety of commuters and pedestrians are some of the reasons are acting as a hindrance in the growth. There have been 36 reported accidents involving autonomous vehicles.

- The rising demand for vehicle safety and stringent government rules drive the ADAS market growth. National Highway Traffic Safety Administration (NHTSA) makes it mandatory for all trucks with weights ht range from 8501 lb. to 10000 lb. to be equipped with Automatic Emergency Braking by September 1, 2022. United Kingdom has also set up a Centre for Connected and Autonomous Vehicles (CAV) that is working towards establishing laws and regulations to allow vehicle testing on highways and roads.

Autonomous Truck Market Trends

ADAS demand is on the rise

Rising awareness among customers is leading to growth in demand for vehicles with autonomous and advanced safety features. 90% of the customers who opt for any ADAS system in their vehicle become repeat purchasers. Government norms and policies are also boosting the sales of the ADAS market. US and European authorities will make the installation of Automotive Emergency Braking (AEB) mandatory by 2022 and the Forward Collision Avoidance/Warning System by 2020.

The complete ADAS systems are featured in expensive luxury segment vehicles only. Many truck OEMs collaborate with ADAS manufacturing companies to produce low-cost ADAS systems. However, vehicles (commercial and passenger) register a minute average annual growth of 1% in their prices, while ADAS systems are expensive due to their high manufacturing cost. OEMs may show reluctance in increasing the prices of small and mid-sized vehicle segments, and ADAS companies might not get the expected return. This factor might hinder the growth of the ADAS market.

Top OEM suppliers have adopted the strategy of partnering with technology companies to develop ADAS. Tech companies like Nvidia have entered this space to provide services to companies such as Volvo and Paccar. Amazon is using Embark's self-driving trucks to deliver its cargo.

Passive safety (safety measures to prevent drivers from injuries during or after the crash) has seen a lot of innovations in the past decades, andminimale scope for improvement is left to make in the markets of developed geographies. Companies are now focusing on providing the best passive safety in developing markets. Active Safety (to predict and avoid crashes) is in its initial stage and has a lot to offer. Any ADAS technology that gets early approval from a majority of players will play a crucial role in the development of fully autonomous vehicles in the future.

North America is leading the autonomous truck market

Although Autonomous trucks are in the early stage of adoption across the globe in geographies such as Europe and the Asia Pacific, North America is currently the largest market due to the availability of infrastructure and significant technology companies that are entering autonomous driving segment.

The rising electrification of vehicles due to infrastructure development by companies such as Tesla is also propelling the market in North America. The induction of x-by-wire technology in electric vehicles is helping in the improvement of autonomous driving.

In Sep 2021, PACCAR teamed up with Aurora, a leading autonomous driving technology company, to launch a commercial pilot of autonomous trucks in hauling operations in Washington. The technology is expected to be used by FedEx.

In 2019, Daimler Trucks North America partnered with Torc Robotics and started testing autonomous trucks at Interstate 81 in Virginia. At CES 2020, Kenworth Truck Co. unveiled its autonomous truck technology based on the T680 truck. The autonomous truck uses sensors and LiDAR and collects up to 1 terabyte of data per hour during driving.

Autonomous Truck Industry Overview

The autonomous truck market is firmly consolidated by players such as Daimler, Volvo, Tesla, etc. The primary strategy players adopt collaborating with technology companies to integrate services such as artificial intelligence (AI), robotics, advanced analytics, Internet of Things, Cloud technology, etc., in the production and operation of autonomous trucks.

- In Sep 2021, Volvo Autonomous Solutions revealed a prototype long-haul autonomous truck for the North America application.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Light-duty Trucks

- 5.1.2 Medium-duty Trucks

- 5.1.3 Heavy-duty Trucks

- 5.2 Level of Autonomy

- 5.2.1 Semi-Autonomonus

- 5.2.2 Fully Autonomoys

- 5.3 ADAS Features

- 5.3.1 Adaptive Cruise Control

- 5.3.2 Lane Departure Warning

- 5.3.3 Intelligent Park Assist

- 5.3.4 Highway Pilot

- 5.3.5 Automatic Emergency Braking

- 5.3.6 Blind Spot Detection

- 5.3.7 Traffic Jam Assist

- 5.3.8 Lane Keeping Assist System

- 5.4 Component Types

- 5.4.1 LIDAR

- 5.4.2 RADAR

- 5.4.3 Camera

- 5.4.4 Sensors

- 5.5 Drive Type

- 5.5.1 IC Engine

- 5.5.2 Electric

- 5.5.3 Hybrid

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Rest of the World

- 5.6.4.1 South America

- 5.6.4.2 Middle-East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 AB Volvo

- 6.2.2 Mercedes Benz Group

- 6.2.3 Traton SE

- 6.2.4 TuSimple

- 6.2.5 Fabu Technology

- 6.2.6 Tesla Inc.

- 6.2.7 Paccar Inc

- 6.2.8 BYD Co. Ltd.

- 6.2.9 Einride

- 6.2.10 Embark

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2030 年自動駕駛卡車市場預測:按卡車類型、推進類型、組件、自動化程度、應用和地區進行的全球分析

2030 年自動駕駛卡車市場預測:按卡車類型、推進類型、組件、自動化程度、應用和地區進行的全球分析 自動駕駛卡車的全球市場:市場規模·佔有率·趨勢,產業分析 (各自動駕駛等級·感測器類別·各最終用途·各地區),未來預測 (2025年~2034年)

自動駕駛卡車的全球市場:市場規模·佔有率·趨勢,產業分析 (各自動駕駛等級·感測器類別·各最終用途·各地區),未來預測 (2025年~2034年) 自動駕駛卡車市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測自動卡車市場規模、佔有率和成長分析:按 ADAS 功能、自動化程度、推進類型、感測器類型、卡車類別、應用和地區 - 2025-2032 年行業預測

自動駕駛卡車市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測自動卡車市場規模、佔有率和成長分析:按 ADAS 功能、自動化程度、推進類型、感測器類型、卡車類別、應用和地區 - 2025-2032 年行業預測 自動駕駛卡車市場評估:自動駕駛層級·推動因素·各地區的機會及預測 (2018-2032年)

自動駕駛卡車市場評估:自動駕駛層級·推動因素·各地區的機會及預測 (2018-2032年) 全球自動駕駛卡車市場,2024-2028

全球自動駕駛卡車市場,2024-2028 自動卡車市場:按類型、感測器技術、連接水準、ADAS - 2025-2030 年全球預測

自動卡車市場:按類型、感測器技術、連接水準、ADAS - 2025-2030 年全球預測 全球自動駕駛卡車市場:現況分析與預測(2024-2032)

全球自動駕駛卡車市場:現況分析與預測(2024-2032) 自動駕駛卡車的全球市場全球 B2B 互聯車隊服務市場預測(截至 2030 年)

自動駕駛卡車的全球市場全球 B2B 互聯車隊服務市場預測(截至 2030 年)