|

市場調查報告書

商品編碼

1683507

膠原蛋白:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Collagen - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

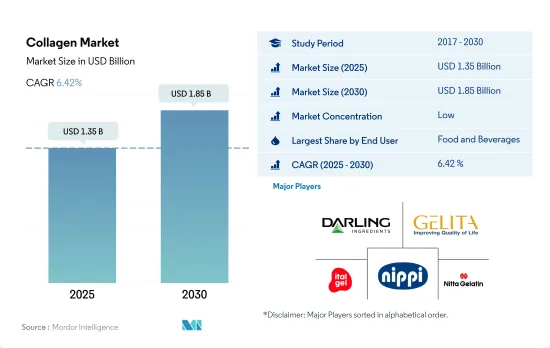

膠原蛋白市場規模預計在 2025 年為 13.5 億美元,預計到 2030 年將達到 18.5 億美元,預測期內(2025-2030 年)的複合年成長率為 6.42%。

由於消費者對基於膠原蛋白的美容產品(即具有皮膚益處的產品)的偏好日益成長,預計預測期內個人護理和化妝品領域的銷售額將增加。

- 根據最終用戶,飲料、烘焙和零嘴零食子區隔佔據了大部分應用,其中食品和飲料仍然是最大的細分市場。預計該領域也將引領市場,預測期內銷售複合年成長率為 5.99%。這種需求是由其多功能性和營養價值所驅動。

- 然而,膠原蛋白在個人護理和化妝品領域的應用預計將優於其他領域,在預測期內,其產量複合年成長率最快,為 7.02%。在該領域,人們使用水解形式的膠原膠原蛋白,因為它們對皮膚的刺激、致敏性和光毒性最小。隨著健康意識的增強,蛋白質強化已成為全球消費者關注的焦點。例如,到2021年,全球75%的消費者將為強化蛋白質的食品和飲料支付更高的價格,其中超過一半的消費者願意支付10%的溢價,15%的消費者願意支付25%的溢價。

- 飲料子區隔是膠原蛋白市場中最大的終端用戶細分市場,佔 2023 年總消費量的 44.2% 以上。膠原蛋白飲料市場正處於發展初期。隨著消費者越來越意識到飲料的健康益處,預計整體膠原蛋白飲料市場將會擴大。膠原蛋白飲料含有大量的羥脯氨酸和氨基酸甘氨酸、精氨酸和脯氨酸,這些與能量供應、細胞再生和新陳代謝有關。膠原蛋白可用於多種熱飲,為具有健康益處的創新產品鋪平了道路。因此,富含膠原蛋白的熱飲(如咖啡和熱巧克力)的消費量正在快速成長。

由於膠原蛋白蛋白產品越來越受歡迎,且各類製造單位實力雄厚,亞太地區將在 2022 年佔據大部分佔有率。

- 亞太地區的膠原蛋白市場最大,主要得益於中國和印度的原料產量不斷增加。在中國,膠原蛋白不僅有助於美容,還有助於增強免疫力、關節健康和運動表現,因此被用於補充劑。該地區膠原蛋白的銷售受到人口老化和企業逐漸在其產品線中添加基於膠原蛋白的成分的推動。在東南亞,60歲及以上人口比例預計將從2017年的9.8%上升到2030年的13.7%。

- 歐洲是該市場的第二大區域,預計在預測期內以 6.48% 的最快以金額為準成長。這是由於區域參與者的增加,他們採用獨特的策略來滿足不斷成長的需求,例如針對個人護理和化妝品等高潛力終端用戶群體不斷進行產品創新。在德國,以膠原蛋白為基礎的膠原蛋白飲料和以膠原蛋白胜肽為基礎的飲料(如Sanotact和BeautyHacker的美容膠原蛋白飲料)的日益普及促進了這一成長。

- 中東和非洲是另一個潛力市場。由於許多消費者遵循伊斯蘭教義,該地區的市場參與者看到了供應膠原蛋白和海洋膠原膠原蛋白的機會。隨著信仰政策的推出和實施,需求預計會增加,主要是為了為膠原蛋白蛋白產品的使用提供靈活性。預測期內,中東和非洲的海洋膠原蛋白市場預計將分別以 7.47% 和 8.21% 的複合年成長率成長。

全球膠原蛋白市場趨勢

健康零食偏好和線上平台的成長將推動市場成長

- 全球消費者的健康意識日益增強,越來越喜歡吃零食的生活方式。這種轉變明顯表現為人們更傾向於選擇比傳統零嘴零食更有營養的替代品。例如,2021 年 6 月在英國,25% 的 Z 世代(16-24 歲)更喜歡標有「低卡路里」的零食,而 18% 的千禧世代(25-34 歲)想要蛋白質含量更高的零食。此外,36% 的 55 歲以上的人正在積極尋找「低碳水化合物」或「零碳水化合物」零食。因此,產業領導者紛紛推出各種低脂、低熱量的產品。

- 此外,消費者擴大透過社群媒體來了解食品趨勢和靈感,Instagram 和 YouTube 等平台已成為發現新零食的重要工具。 2022 年,超過 70% 的全球消費者,尤其是 Z 世代和千禧世代,在發現新零食時會向社群媒體尋求靈感。線上平台的興起進一步簡化了這個流程,讓消費者可以在舒適的家中探索和購買各種零食。

- 優質化也推動了零嘴零食產業的創新,強調零嘴零食的新鮮、健康和功能性。濃郁的辛辣口味和異國風的配料越來越受歡迎,滿足了全球多樣化的口味,並有助於推動區域市場的成長。零食不再只是一種營養來源;它已經深深植根於現代文化之中。在家工作或娛樂時吃零食正變得越來越普遍。例如,Godrej Yummiez 在 2022 年 11 月發布的一份報告強調,45% 的印度消費者更喜歡在聚會和節慶期間吃零食。這些文化轉變凸顯了零食如何從個人選擇演變為社會期望。

肉類主要用作生產膠原蛋白的原料

- 肉類是世界各地人們重要的營養來源。過去50年來,全球對肉類的需求不斷擴大,肉類產量增加了兩倍。目前,全球每年肉類產量超過3.5億噸。從區域來看,亞太地區是最大的肉類生產地區,佔全球肉類產量的很大一部分。這標誌著與過去幾十年相比的重大轉變。近年來,歐洲的肉類產量也增加了一倍。預計中國將佔肉類產量成長的大部分,其次是美國、巴西和印度。

- 美國是牛肉和水牛肉的最大生產國,其次是巴西和中國。阿根廷、澳洲和印度的貢獻也值得關注。在雞肉領域,美國引領市場,中國和巴西也扮演重要角色。整體來看,歐洲的雞肉產量與美國相當。然而,在人均肉品消費量已經很高的高所得國家,需求預計會停滯甚至下降。這些變化是由人口老化和優先考慮更多種類蛋白質的飲食偏好的改變所驅動。

- 牛和畜群數量的擴大,尤其是在中國,正在支撐全球肉類產量的上升趨勢。這一趨勢,加上畜牧業生產和技術的進步(特別是在中低收入國家),將提高生產力。雞肉尤其推動了全球肉類產量的激增。

膠原蛋白產業概況

膠原蛋白市場較為分散,前五大公司的市佔率為11.59%。市場的主要企業有:Darling Ingredients Inc.、GELITA AG、Italgelatine SpA、Nippi。 Inc. 和 Nitta Gelatin Inc.(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第 2 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第3章 產業主要趨勢

- 最終用戶市場規模

- 嬰兒食品和嬰兒奶粉

- 麵包店

- 飲料

- 早餐用麥片穀類

- 調味品/醬料

- 糖果零食

- 乳製品和乳製品替代品

- 老年營養與醫學營養

- 肉類、家禽、魚貝類和肉類替代品

- RTE/RTC 食品

- 小吃

- 運動/運動營養

- 動物飼料

- 個人護理和化妝品

- 蛋白質消費趨勢

- 動物

- 生產趨勢

- 動物

- 法律規範

- 中國

- 法國

- 德國

- 印度

- 義大利

- 日本

- 英國

- 美國

- 價值鏈與通路分析

第 4 章 市場細分

- 形式

- 動物性

- 海洋類

- 最終用戶

- 動物飼料

- 飲食

- 按次級最終用戶

- 麵包店

- 飲料

- 早餐用麥片穀類

- 小吃

- 個人護理和化妝品

- 補充

- 按次級最終用戶

- 老年營養與醫學營養

- 運動/運動營養

- 按地區

- 非洲

- 按類型

- 按最終用戶

- 按國家

- 奈及利亞

- 南非

- 非洲其他地區

- 亞太地區

- 按類型

- 按最終用戶

- 按國家

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 馬來西亞

- 紐西蘭

- 韓國

- 泰國

- 越南

- 其他亞太地區

- 歐洲

- 按類型

- 按最終用戶

- 按國家

- 比利時

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 土耳其

- 英國

- 其他歐洲國家

- 中東

- 按類型

- 按最終用戶

- 按國家

- 伊朗

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 北美洲

- 按類型

- 按最終用戶

- 按國家

- 加拿大

- 墨西哥

- 美國

- 北美其他地區

- 南美洲

- 按類型

- 按最終用戶

- 按國家

- 阿根廷

- 巴西

- 其他南美洲地區

- 非洲

第5章 競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介(包括全球概況、市場層級概況、主要業務部門、財務狀況、員工人數、關鍵資訊、市場排名、市場佔有率、產品和服務以及最新發展分析)

- ASAHI GELATINE INDUSTRIAL Co.,Ltd.

- Darling Ingredients Inc.

- Ewald-Gelatine GmbH

- Foodchem International Corporation

- GELITA AG

- Italgelatine SpA

- Jellice Pioneer Private Limited

- Nippi. Inc.

- Nitta Gelatin Inc.

第6章 執行長的關鍵策略問題

第7章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 90227

The Collagen Market size is estimated at 1.35 billion USD in 2025, and is expected to reach 1.85 billion USD by 2030, growing at a CAGR of 6.42% during the forecast period (2025-2030).

Personal care and cosmetic segment is expected to gain higher sales in forecast period due to growing consumer preferences for collagen-based beauty products i.e. beneficial for skin

- By end user, F&B remained the largest segment, with the majority of applications in the beverage, bakery, and snacks sub-segments. The segment is also anticipated to drive the market with a CAGR of 5.99%, by volume, in the forecast period. This demand can be attributed to its multi-functionality and nutritional benefits.

- However, in the forecast period, collagen application in the personal care and cosmetics segment is projected to outpace other segments with the fastest CAGR of 7.02% by volume. The segment uses collagen in the hydrolyzed form, owing to its negligible skin irritation, sensitization, or indication of phototoxicity. Protein fortification has become a major interest among global consumers, with a rise in their health concerns. For example, in 2021, 75% of global consumers paid a higher price for protein-fortified food and beverages, while more than half paid a 10% premium, and 15% of consumers would be willing to pay a 25% premium.

- The beverages sub-segment is the largest end-user segment in the collagen market and represents over 44.2% of the total consumption volume in 2023. The collagen drinks market is in its early stages of development. As consumers become increasingly aware of the health benefits of the beverages they consume, it is expected to increase the overall market for collagen drinks. Collagen-based drinks are high in hydroxyproline, amino acids glycine, arginine, and proline, which are associated with energy supply, cell regeneration, and metabolism. Collagen can be used in many hot beverages, which paves the way for innovative products with health benefits. Hence, the consumption of collagen-enhanced hot beverages such as coffee and hot chocolate is increasing at a high pace.

Asia-pacific accounted majority of share in 2022 due to growing popularity of collagen based products coupled with strong presence of various manufacturing units

- The Asia-Pacific collagen market is the largest, owing to the higher production of raw materials in the region, mainly in China and India. In China, collagen application in supplements is not only used for skin beauty but also beneficial for immune, joint health, and sports performance. Collagen sales in the region are being driven by the aging population and companies that are progressively adding collagen-based ingredients to their product lines. In Southeast Asia, the proportion of individuals aged 60 years and older was 9.8% in 2017, which is projected to rise to 13.7% by 2030.

- Europe is the second-largest regional segment for the market and is also projected to record the fastest CAGR of 6.48%, by value, during the forecast period, attributed to a rise in regional players catering to the surging demand by adopting distinct strategies like constant product innovation for highly potential end-user segments, like personal care and cosmetics. The growing popularity of collagen-based beauty drinks and collagen peptide-based beverages like Sanotact and BeautyHacker beauty collagen drinks in Germany contributes to this growth.

- Middle East & Africa is another promising market, as most consumers follow Islamic principles, thus creating opportunities for market players in the region to supply collagen sourced from halal sources or marine-based collagen/ With the introduction and implementation of religion-based policies, the demand is anticipated to increase, primarily to render flexibility for using collagen-based products. The marine-sourced collagen market in the Middle East and African regions is projected to record a CAGR of 7.47% and 8.21%, respectively, during the forecast period.

Global Collagen Market Trends

Healthy snacking preferences with growth in online platforms are supporting market growth

- Consumers worldwide increasingly embrace a snacking lifestyle with a heightened focus on health. This shift is evident in their preference for nutritious alternatives over traditional snacks. For instance, in June 2021, 25% of Gen Zs (16 to 24 years old) in the United Kingdom favored snacks labeled "low in calories," while 18% of millennials (25 to 34 years old) sought out high-protein options. Additionally, 36% of those over 55 actively sought snacks with "low" or "no sugar" content. Consequently, leading industry players have responded by introducing a variety of low-fat and low-calorie offerings.

- Furthermore, with users increasingly relying on social media for food trends and inspiration, platforms like Instagram and YouTube have emerged as crucial tools for discovering new snacks. Over 70% of global consumers, particularly Gen Zs and millennials, attributed their discovery of new snacks in 2022 to social media. The rise of online platforms has further streamlined the process, allowing consumers to explore and purchase a diverse range of snacks from the comfort of their homes.

- Also, premiumization is driving innovation innovation in the snacks segment, emphasizing fresh, better-for-you, and functional snacks. Bold, spicy flavors and exotic ingredients are gaining traction, appealing to a diverse global palate and fueling growth in regional markets. Snacking has transcended mere sustenance, becoming deeply ingrained in modern culture. It has become common to snack while working or enjoying entertainment at home. For example, a November 2022 report from Godrej Yummiez highlighted that 45% of Indian consumers favored snacking during parties and celebrations. This cultural shift highlights the transformation of snacking from a personal choice to a societal expectation.

Meat is majorly used as a raw material by collagen manufacturers

- Meat is an important source of nutrition for people around the world. Global demand for meat has grown over the past 50 years, with meat production tripling. Global produce presently stands at more than 350 million tonnes each year. Regionally, Asia-Pacific holds the position of being the largest meat producer, contributing a substantial portion of the total global meat production. This represents a significant shift from previous decades. Europe's meat output has also doubled in recent years. China is projected to account for most of the total increase in meat production, followed by the United States, Brazil, and India.

- The United States takes the crown as the top producer of beef and buffalo meat, with Brazil and China following suit. Noteworthy contributions also come from Argentina, Australia, and India. In the poultry realm, the United States leads the pack, with China and Brazil playing pivotal roles. As a collective, Europe matches the United States in its substantial poultry output. However, in high-income nations, where per capita meat consumption is already high, a plateau or even a decline in demand is foreseen. This shift is attributed to aging populations and evolving dietary preferences, emphasizing a broader protein palette.

- Expanding herds and flocks, especially in China, are underpinning global meat production's upward trajectory. This trend is set to bolster productivity, coupled with advancements in animal breeding and technology, particularly in low and middle-income nations. Poultry meat, in particular, is driving this surge in global meat production.

Collagen Industry Overview

The Collagen Market is fragmented, with the top five companies occupying 11.59%. The major players in this market are Darling Ingredients Inc., GELITA AG, Italgelatine SpA, Nippi. Inc. and Nitta Gelatin Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 China

- 3.4.2 France

- 3.4.3 Germany

- 3.4.4 India

- 3.4.5 Italy

- 3.4.6 Japan

- 3.4.7 United Kingdom

- 3.4.8 United States

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Animal Based

- 4.1.2 Marine Based

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.2 Sport/Performance Nutrition

- 4.3 Region

- 4.3.1 Africa

- 4.3.1.1 By Form

- 4.3.1.2 By End User

- 4.3.1.3 By Country

- 4.3.1.3.1 Nigeria

- 4.3.1.3.2 South Africa

- 4.3.1.3.3 Rest of Africa

- 4.3.2 Asia-Pacific

- 4.3.2.1 By Form

- 4.3.2.2 By End User

- 4.3.2.3 By Country

- 4.3.2.3.1 Australia

- 4.3.2.3.2 China

- 4.3.2.3.3 India

- 4.3.2.3.4 Indonesia

- 4.3.2.3.5 Japan

- 4.3.2.3.6 Malaysia

- 4.3.2.3.7 New Zealand

- 4.3.2.3.8 South Korea

- 4.3.2.3.9 Thailand

- 4.3.2.3.10 Vietnam

- 4.3.2.3.11 Rest of Asia-Pacific

- 4.3.3 Europe

- 4.3.3.1 By Form

- 4.3.3.2 By End User

- 4.3.3.3 By Country

- 4.3.3.3.1 Belgium

- 4.3.3.3.2 France

- 4.3.3.3.3 Germany

- 4.3.3.3.4 Italy

- 4.3.3.3.5 Netherlands

- 4.3.3.3.6 Russia

- 4.3.3.3.7 Spain

- 4.3.3.3.8 Turkey

- 4.3.3.3.9 United Kingdom

- 4.3.3.3.10 Rest of Europe

- 4.3.4 Middle East

- 4.3.4.1 By Form

- 4.3.4.2 By End User

- 4.3.4.3 By Country

- 4.3.4.3.1 Iran

- 4.3.4.3.2 Saudi Arabia

- 4.3.4.3.3 United Arab Emirates

- 4.3.4.3.4 Rest of Middle East

- 4.3.5 North America

- 4.3.5.1 By Form

- 4.3.5.2 By End User

- 4.3.5.3 By Country

- 4.3.5.3.1 Canada

- 4.3.5.3.2 Mexico

- 4.3.5.3.3 United States

- 4.3.5.3.4 Rest of North America

- 4.3.6 South America

- 4.3.6.1 By Form

- 4.3.6.2 By End User

- 4.3.6.3 By Country

- 4.3.6.3.1 Argentina

- 4.3.6.3.2 Brazil

- 4.3.6.3.3 Rest of South America

- 4.3.1 Africa

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 ASAHI GELATINE INDUSTRIAL Co.,Ltd.

- 5.4.2 Darling Ingredients Inc.

- 5.4.3 Ewald-Gelatine GmbH

- 5.4.4 Foodchem International Corporation

- 5.4.5 GELITA AG

- 5.4.6 Italgelatine SpA

- 5.4.7 Jellice Pioneer Private Limited

- 5.4.8 Nippi. Inc.

- 5.4.9 Nitta Gelatin Inc.

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

膠原蛋白市場-全球產業規模、佔有率、趨勢、機會和預測,按產品、來源、應用、地區和競爭細分,2020-2030 年

膠原蛋白市場-全球產業規模、佔有率、趨勢、機會和預測,按產品、來源、應用、地區和競爭細分,2020-2030 年 美國膠原蛋白:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

美國膠原蛋白:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 膠原蛋白市場規模、佔有率、成長分析、按產品類型、按類型、按形式、按來源、按產品類型、按功能、按應用、按地區 - 行業預測 2025-2032

膠原蛋白市場規模、佔有率、成長分析、按產品類型、按類型、按形式、按來源、按產品類型、按功能、按應用、按地區 - 行業預測 2025-2032 全球膠原蛋白市場:市場規模、佔有率、趨勢分析(按產品、原料、應用和地區)、細分市場預測(2025-2030 年)

全球膠原蛋白市場:市場規模、佔有率、趨勢分析(按產品、原料、應用和地區)、細分市場預測(2025-2030 年) 膠原蛋白市場機會、成長動力、產業趨勢分析及 2025-2034 年預測

膠原蛋白市場機會、成長動力、產業趨勢分析及 2025-2034 年預測 2025 年膠原蛋白全球市場報告

2025 年膠原蛋白全球市場報告 膠原蛋白市場:按產品、形式、來源、萃取製程、類型、應用 - 2025-2030 年全球預測

膠原蛋白市場:按產品、形式、來源、萃取製程、類型、應用 - 2025-2030 年全球預測 2024 年至 2031 年膠原蛋白市場(按地區)

2024 年至 2031 年膠原蛋白市場(按地區) 全球 II 型膠原蛋白市場 - 2024-2031

全球 II 型膠原蛋白市場 - 2024-2031 美國膠原蛋白市場規模、佔有率、趨勢分析報告:按產品、來源、應用、細分市場預測,2025-2030 年

美國膠原蛋白市場規模、佔有率、趨勢分析報告:按產品、來源、應用、細分市場預測,2025-2030 年

▼