|

市場調查報告書

商品編碼

1685844

氣體感測器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Gas Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

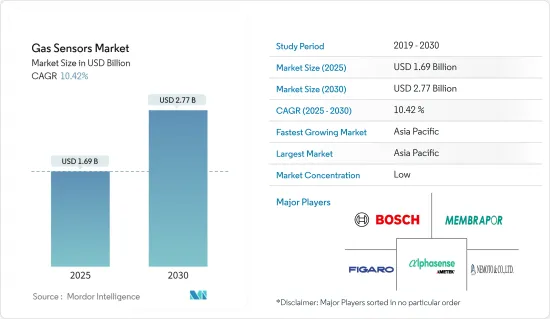

預計 2025 年氣體感測器市場規模為 16.9 億美元,到 2030 年將達到 27.7 億美元,預測期內(2025-2030 年)的複合年成長率為 10.42%。

主要亮點

- 在智慧城市中,氣體感測器正在應用於環境監測,例如氣象站、公共區域和大樓自動化系統中的空氣品質檢查。預計這種廣泛的採用將在整個預測期內推動市場成長。

- 此外,暖氣、通風和空調 (HVAC) 系統對於建築物、監測環境和調節氣體濃度至關重要。這兩個特點正在刺激巨大的需求並進一步支持市場成長。

- 氣體檢測在全球石油和天然氣領域至關重要。該行業的海上鑽井和探勘活動會產生危險、可燃性氣體和有毒的氣體。雖然某些氣體在少量時是無害的,但在高濃度時它們會帶走氧氣並造成嚴重風險,包括窒息。隨著石油產量預計增加,對氣體感測器的需求也將增加。這些感測器對於快速識別設施、管道和儲存槽的氣體洩漏至關重要。

- 人們對與有毒有害氣體相關的職場危害的認知不斷提高,推動了氣體感測器的採用,特別是在石油和天然氣、化學、石化、金屬和採礦等領域。鑑於潛在的風險,化學工業通常依靠氣體感測器在氣體濃度超過安全限值時啟動緊急系統。

- 氣體感測器的製造成本正在上升,這主要是由於技術進步。現在,許多感測器都採用了電子機械系統 (MEMS) 和奈米技術等最尖端科技,這些技術在提高性能的同時,也增加了製造過程的複雜性和成本。開發這種先進的感測器技術需要大量的研發投入,進一步加劇成本結構。雖然現有製造商正在適應這些變化,但新進業者和中型製造商面臨巨大的障礙。

- 由於俄羅斯-烏克蘭衝突和隨之而來的經濟放緩,氣體感測器市場面臨明顯的混亂。通貨膨脹和利率上升抑制了消費者支出,從而抑制了對氣體感測器的需求。美國和中國的貿易緊張局勢加劇了全球供應鏈的中斷。尤其是美國半導體製造設備出口的嚴格管制,對中國電力、汽車等產業的生產造成了阻礙。

氣體感測器市場趨勢

一氧化碳(CO)領域佔據很大市場佔有率

- 一氧化碳 (CO) 構成重大威脅,因為它會引起中毒,並且是不可預測的發病率和死亡率的主要原因。因此,找到檢測這種危險氣體的最佳材料和技術至關重要。金屬氧化物半導體(MOS)感測器的應用越來越受到關注,尤其是在微米或奈米薄膜格式中。

- 一氧化碳本質上具有毒性,但在工業和冶金作業中卻是重要的可燃且環保的能源來源。一氧化碳在氧化還原反應中起著至關重要的作用,並有助於金屬的精製。一氧化碳尤其易燃、易爆。鑑於潛在的危險,一氧化碳感測器的採用越來越多。日益嚴格的政府法規,特別是針對工人安全的法規進一步推動了這一趨勢。

- 一氧化碳偵測儀因其能夠檢測這種無色、無味、無臭的氣體而成為各行各業的必需品。這種感測器對於避免一氧化碳中毒至關重要。如果不及時治療,一氧化碳中毒可能會導致嚴重後果,包括失去意識、癲癇發作甚至死亡。光是在美國,這種無聲殺手每年就會導致超過 20,000 人次急診就診,是許多國家最常見的致命中毒原因。

- 一氧化碳 (CO) 會減少身體器官和組織的氧氣供應,從而危害您的健康。即使在較低的 CO 濃度下,患有心臟病的人也會面臨更大的風險,並且可能會出現胸痛和運動能力下降等症狀,反覆接觸可能會導致心血管併發症。道路上車輛數量的增加會產生大量的二氧化碳,對用於分析和檢測環境中氣體的氣體感測器的需求龐大。 CO(一氧化碳)氣體感測器是氣體檢測儀器的關鍵組成部分,旨在識別各種環境中(從家庭、汽車到工業環境)的一氧化碳。

- 根據美國環保署估計,不包括野火排放,美國2023年將排放約4,230萬噸一氧化碳(CO)。二氧化碳排放的增加將為該領域的成長創造新的市場機會。

亞太地區可望大幅成長

- 甲烷是繼二氧化碳之後對全球暖化影響最大的溫室氣體。中國是石化燃料活動甲烷排放量最大的國家之一,面臨控制排放的壓力。

- 中國生態環境部最近發布的《甲烷控制規劃》概述了這些努力,但仍面臨控制甲烷排放的壓力。控制甲烷排放面臨資料收集不足、稅收和監管標準以及持續的技術和管理障礙。

- 由於地緣政治衝突導致能源價格上漲,人們對氫等替代能源的興趣日益濃厚。氫氣有潛力成為工業和住宅用途的初級能源能源。由於二氧化碳測量儀和呼吸分析儀等設備中加入了氣體感測器,醫療產業預計將保持強勁成長。

- 氣體感測器對於檢測氫氣洩漏以及確保氫氣的安全生產、儲存和使用至關重要。日本正大力投資氫能作為清潔能源來源,並致力於開發用於汽車和發電的氫燃料電池。氣體感測器對於檢測氫氣洩漏以及確保氫氣的安全生產、儲存和使用至關重要。

- 例如,日本最著名的發電公司JERA打算在2035年到氨和氫燃料供應方面投資超過60億美元,該公司的主要重點是藍氫氫和綠氫。藍氫由天然氣產生並排放二氧化碳,但可以捕獲和儲存以最大限度地減少對溫室氣體的影響。另一方面,綠色氫是利用水力發電解從太陽能和風力發電可再生能源產生的。

氣體感測器產業概況

氣體感測器市場分散,參與者多。提供各種類型氣體感測器的公司根據技術優勢來區分其產品。因此,他們與競爭對手採取價格戰策略來搶佔市場佔有率。主要參與者包括 Membrapor AG、AlphaSense Inc.、Nemoto Industries、Figaro Engineering Inc. 和 Robert Bosch GmbH。

2023 年 10 月-Figaro Engineering 宣佈在德國諾伊斯開設 Figaro 歐洲辦事處。這項策略性舉措旨在透過向客戶和當地經銷商提供專門的技術支援來加強費加羅在歐洲的影響力。預計該辦公室將帶頭進行有針對性的行銷工作,並凸顯費加洛擴大其在歐洲市場立足點的決心。

2023 年 10 月-MEMBRAPOR AG 增強了其 NO2/CA-2 感測器,靈敏度幾乎提高了一倍。這項改進使得檢測 ppb 範圍內的低濃度成為可能。該感測器具有完善的催化 O3 過濾器,可有效減輕電化學 NO2 感測器中常見的 O3 交叉敏感性。推出了 NO2/CA-20 感測器,將測量能力擴展到 20 ppm 範圍。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業價值鏈分析

第5章 市場動態

- 市場促進因素

- 為滿足政府法規,汽車對氣體感測器的需求增加

- 提高對主要行業職業事故的認知

- 市場挑戰

- 成本上升和產品缺乏差異化

第6章 市場細分

- 按類型

- 氧

- 一氧化碳(CO)

- 二氧化碳 (CO2)

- 氮氧化物

- 碳氫化合物

- 其他類型

- 依技術分類

- 電化學公式

- 光電離檢測器(PID)

- 固體/金屬氧化物半導體

- 催化

- 紅外線的

- 半導體

- 按應用

- 醫療

- 建築自動化

- 產業

- 飲食

- 車

- 運輸和物流

- 其他用途

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 亞洲

- 中國

- 日本

- 印度

- 澳洲和紐西蘭

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 北美洲

第7章 競爭格局

- 公司簡介

- Figaro Engineering Inc.

- Membrapor AG

- AlphaSense Inc.

- Nemoto & Co. Ltd

- Robert Bosch GmbH

- Delphi Technologies

- SGX Sensortech Ltd(Amphenol Corporation)

- Zhengzhou Winsen Electronics Technology Co., Ltd.

- Niterra Co. Ltd.(NGK-NTK)

- Senseair(Asahi Kesai)

- Drgerwerk AG & Co. KGaA

第8章投資分析

第9章市場機會與未來成長

The Gas Sensors Market size is estimated at USD 1.69 billion in 2025, and is expected to reach USD 2.77 billion by 2030, at a CAGR of 10.42% during the forecast period (2025-2030).

Key Highlights

- In smart cities, gas sensors find applications in environmental monitoring, including air quality checks at weather stations, public areas, and within building automation systems. This widespread adoption is expected to drive the market's growth through the forecast period.

- Additionally, heating, ventilation, and air conditioning (HVAC) systems are integral to buildings, monitoring environments and regulating gas concentrations. This dual functionality has spurred significant demand, further fueling market growth.

- Gas detection is paramount in the global oil and gas sector. This industry's offshore drilling and exploration activities produce a spectrum of hazardous, flammable, and toxic gases. While some gases are benign in small quantities, they can deplete oxygen in high concentrations, leading to severe risks like suffocation. As oil production is projected to rise, so is the demand for gas sensors. These sensors are crucial for swiftly identifying gas leaks from equipment, pipelines, and storage tanks.

- Increasing awareness of workplace hazards related to toxic and hazardous gases is propelling the adoption of gas sensors, especially in sectors like oil and gas, chemicals, petrochemicals, metals, and mining. Given the potential risks, chemical industries often rely on gas sensors to trigger emergency systems when gas concentrations exceed safe limits.

- Production costs for gas sensors have increased, primarily due to technological advancements. Many sensors now incorporate cutting-edge technologies like microelectromechanical systems (MEMS) or nanotech, which, while enhancing performance, also complicate the fabrication process, thereby increasing costs. Developing these advanced sensor technologies necessitates substantial investments in research and development, further adding to the cost structure. While established players have adapted to these changes, newcomers and mid-tier manufacturers face significant hurdles.

- The gas sensors market faced notable disruptions due to the Russia-Ukraine conflict and subsequent economic slowdown. Rising inflation and interest rates curtailed consumer spending, dampening the demand for gas sensors. The trade tensions between the United States and China exacerbated global supply chain disruptions. Notably, the United States' stringent controls on semiconductor manufacturing equipment exports to China have hampered production in China's consumer electronics and automotive sectors.

Gas Sensors Market Trends

Carbon Monoxide (CO) Segment to Hold Significant Market Share

- Carbon monoxide (CO) poses a significant threat as it can cause intoxication, a leading factor in unpredictable morbidity and mortality, which is often linked to inhalation injuries from combustion. This underscores the critical need to identify optimal materials and technologies for detecting this hazardous gas. Metal oxide semiconductor (MOS) sensors have garnered attention, especially for their application in micro- or nano-thin film formats.

- While carbon monoxide is inherently toxic, it serves as a crucial, combustible, and eco-friendly energy source in industrial and metallurgical operations. It plays a pivotal role in redox reactions, aiding in metal purification. Notably, carbon monoxide is both highly flammable and prone to explosions. Given the potential dangers, the adoption of carbon monoxide sensors is on the rise. This trend is further propelled by increasingly stringent government regulations, particularly those emphasizing worker safety.

- Carbon monoxide detectors are indispensable in various industries, primarily for their ability to detect this colorless, odorless, and tasteless gas, which is otherwise imperceptible to human senses. Such sensors are pivotal in averting carbon monoxide poisoning, a condition that, when left unchecked, can lead to severe consequences, including loss of consciousness, seizures, or even death. In the United States alone, this silent killer prompts over 20,000 emergency room visits annually and stands as the most common fatal poisoning in many nations.

- Carbon monoxide (CO) can harm health by impeding oxygen delivery to the body's organs and tissues. Individuals with heart disease face heightened risks even at lower CO levels, experiencing symptoms like chest pain, reduced exercise capacity, and potentially additional cardiovascular complications with repeated exposure. The growing number of vehicles on the road generates a huge amount of CO, which creates a significant demand for gas sensors to analyze and detect gases in the environment. CO (Carbon Monoxide) gas sensors are crucial components in gas detection equipment, designed to identify carbon monoxide in various settings, from homes and automotive to industrial environments.

- According to the Environmental Protection Agency, the United States saw emissions of around 42.3 million tons of carbon monoxide (CO) in 2023, excluding those from wildfires. Such increased CO emissions create new market opportunities for segment growth.

Asia-Pacific Expected to Witness Major Growth

- After CO2, methane is the second most impactful greenhouse gas, significantly contributing to global warming. China is one of the top methane emitters from fossil fuel activities, and the nation is under pressure to rein in its methane output.

- Despite efforts outlined in China's recent methane plan issued by the Ministry of Ecology and Environment. These include inadequate data collection, tax regulatory standards, and ongoing technical and managerial hurdles in controlling methane emissions.

- The increase in energy prices due to geopolitical conflicts has caused a growing interest in alternative energy sources like Hydrogen. Hydrogen can potentially be a primary energy source for industrial and residential uses. The medical industry is projected to stay steady, with gas sensors in devices like capnography and breath analyzers.

- Gas sensors are crucial for detecting hydrogen leaks and ensuring Hydrogen's safe production, storage, and utilization. Japan invests heavily in Hydrogen as a clean energy source, with initiatives to develop hydrogen fuel cells for vehicles and power generation. Gas sensors are crucial for detecting hydrogen leaks, ensuring the safe production, storage, and utilization

- For instance, Japan's most prominent power generation company, JERA, intends to invest over USD 6 billion in ammonia and hydrogen fuel supplies by 2035. The company's primary focus will be on blue and green Hydrogen. Blue Hydrogen is generated from natural gas, which produces carbon emissions that are then captured and stored to minimize its greenhouse gas impact. In contrast, green Hydrogen is produced through water electrolysis-powered solar and wind energy renewable resources.

Gas Sensors Industry Overview

The gas sensors market is fragmented because of the presence of many players. The companies offering various types of gas sensors have technological product differentiation. Hence, they are adopting competitive pricing strategies to gain market share. Some of the key players include Membrapor AG, AlphaSense Inc., Nemoto & Co. Ltd, Figaro Engineering Inc., and Robert Bosch GmbH

October 2023-Figaro Engineering announced the opening of the Figaro Europe Office in Neuss, Germany. This strategic move aimed to bolster Figaro's presence in Europe by offering dedicated technical support to customers and local distributors. The office was expected to spearhead targeted marketing initiatives, underscoring Figaro's commitment to expanding its foothold in the European market.

October 2023 - MEMBRAPOR AG enhanced its NO2/CA-2 sensor, boosting its sensitivity to nearly double its capability. This advancement enabled the sensor to detect lower concentrations in the ppb range. The sensor features its established catalytic O3 filter, effectively mitigating the common O3 cross-sensitivity in electrochemical NO2 sensors. It introduced the NO2/CA-20 sensor, extending its measurement capabilities to ranges of up to 20 ppm.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Gas Sensors in Automobiles for Compliance with Governmental Regulations

- 5.1.2 Growing Awareness on Occupational Hazards across Major Industries

- 5.2 Market Challenges

- 5.2.1 Rising Costs and Lack of Product Differentiation

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Oxygen

- 6.1.2 Carbon Monoxide (CO)

- 6.1.3 Carbon Dioxide (CO2)

- 6.1.4 Nitrogen Oxide

- 6.1.5 Hydrocarbon

- 6.1.6 Other Types

- 6.2 By Technology

- 6.2.1 Electrochemical

- 6.2.2 Photoionization Detectors (PID)

- 6.2.3 Solid State/Metal Oxide Semiconductor

- 6.2.4 Catalytic

- 6.2.5 Infrared

- 6.2.6 Semiconductor

- 6.3 By Application

- 6.3.1 Medical

- 6.3.2 Building Automation

- 6.3.3 Industrial

- 6.3.4 Food and Beverages

- 6.3.5 Automotive

- 6.3.6 Transportation and Logistics

- 6.3.7 Other Applications

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.5.1 Brazil

- 6.4.5.2 Argentina

- 6.4.5.3 Mexico

- 6.4.6 Middle East and Africa

- 6.4.6.1 United Arab Emirates

- 6.4.6.2 Saudi Arabia

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Figaro Engineering Inc.

- 7.1.2 Membrapor AG

- 7.1.3 AlphaSense Inc.

- 7.1.4 Nemoto & Co. Ltd

- 7.1.5 Robert Bosch GmbH

- 7.1.6 Delphi Technologies

- 7.1.7 SGX Sensortech Ltd (Amphenol Corporation)

- 7.1.8 Zhengzhou Winsen Electronics Technology Co., Ltd.

- 7.1.9 Niterra Co. Ltd. (NGK-NTK)

- 7.1.10 Senseair (Asahi Kesai)

- 7.1.11 Drgerwerk AG & Co. KGaA

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE GROWTH

氣體感測器、檢測器和分析儀器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

氣體感測器、檢測器和分析儀器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 氣體感測器市場:全球2025-2029

氣體感測器市場:全球2025-2029 2025-2029年全球油質感測器市場

2025-2029年全球油質感測器市場 2025 年石油和天然氣感測器全球市場報告2025 年氣體感測器全球市場報告氣體感測器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、技術、應用、地區和競爭細分,2020-2030 年

2025 年石油和天然氣感測器全球市場報告2025 年氣體感測器全球市場報告氣體感測器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、技術、應用、地區和競爭細分,2020-2030 年 全球氣體感測器市場:按產品、按輸出類型、按連接、按技術、按類型、按最終用途、按地區 - 預測到 2032 年CO 氣體感測器 -市場佔有率分析、行業趨勢/統計、成長預測 (2025-2030)拉丁美洲氣體感測器:市場佔有率分析、產業趨勢、成長預測(2025-2030)歐洲氣體感測器:市場佔有率分析、產業趨勢、統計、成長預測(2025-2030)

全球氣體感測器市場:按產品、按輸出類型、按連接、按技術、按類型、按最終用途、按地區 - 預測到 2032 年CO 氣體感測器 -市場佔有率分析、行業趨勢/統計、成長預測 (2025-2030)拉丁美洲氣體感測器:市場佔有率分析、產業趨勢、成長預測(2025-2030)歐洲氣體感測器:市場佔有率分析、產業趨勢、統計、成長預測(2025-2030)