|

市場調查報告書

商品編碼

1687824

氣體感測器、檢測器和分析儀器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Gas Sensor, Detector And Analyzer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

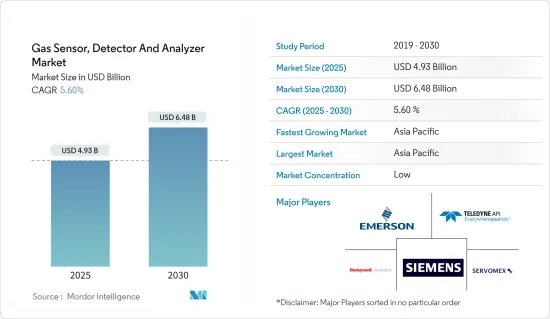

氣體感測器、檢測器和分析儀的市場規模預計在 2025 年為 49.3 億美元,預計到 2030 年將達到 64.8 億美元,預測期內(2025-2030 年)的複合年成長率為 5.6%。

氣體感測器是一種化學感測器,可以測量附近成分氣體的濃度。這些感測器採用多種技術來量化介質中的氣體的精確量。氣體檢測儀利用其他技術來測量並顯示空氣中特定氣體的濃度。氣體探測器的特點在於它們可以在環境中探測到的氣體類型。氣體分析儀應用於多個終端用戶產業所使用的安全設備中,以確保足夠的職場安全。

主要亮點

- 頁岩氣和緻密油的發現不斷增加,推動了全球對氣體分析儀的需求。政府立法和職業安全與健康法規的執行也要求在某些工業環境中使用氣體分析儀。社會對氣體洩漏和廢氣危害的認知不斷提高,也促進了氣體分析儀的普及。製造商正在將氣體分析儀與行動電話和其他無線設備整合,以提供即時監控、遠端控制和資料備份。

- 氣體洩漏和其他意外污染可能造成爆炸後果、人身傷害和火災危險。在密閉空間內,多種危險氣體會取代氧氣,甚至使附近的工人窒息。這些後果危害員工、設備和財產的安全。

- 手持式氣體偵測工具透過監測固定和移動使用者的呼吸區域來確保工人的安全。在許多可能存在氣體危險的情況下,這些設備極為重要。空氣中氧氣、可燃物和有毒氣體的監測對於確保每個人的安全至關重要。手持式氣體偵測儀內建警報器,可提醒人員密閉空間和其他應用的潛在危險情況。當警報響起時,大型易讀的 LCD 顯示器會辨識危險氣體或氣體濃度。

- 近年來,由於技術進步,氣體感測器和探測器的製造成本一直在穩步上升。雖然市場現有企業能夠適應這些變化,但新參與企業和中階製造商面臨相當大的挑戰。

- 由於COVID-19疫情爆發,受訪市場中的多個終端用戶產業受到了營運減少、工廠暫時關閉等影響。例如,在可再生能源產業,全球供應鏈是一個主要問題,生產大幅放緩,導致對新測量系統和感測器的支出減少。在天然氣加工中,硫化氫 (H2S) 和二氧化碳 (CO2) 的檢測和監測至關重要,因此對氣體分析儀的需求很大。

氣體感測器、檢測器和分析儀的市場趨勢

石油和天然氣產業預計將佔據主要市場佔有率

- 在石油和天然氣工業中,保護壓力管道免受腐蝕和洩漏以最大限度地減少停機時間是一項關鍵責任。根據NACE(美國腐蝕工程師協會)的研究,石油和天然氣生產行業每年的腐蝕總成本約為13.72億美元。

- 氣體樣本中是否存在氧氣決定了加壓管道系統中是否有洩漏。持續的、未被發現的洩漏會使情況變得更糟,影響管道的運作流動效率。此外,當管道系統內存在硫化氫 (H2S) 和二氧化碳 (CO2) 等氣體時,它們會與氧氣反應並結合,形成腐蝕性、破壞性混合物,從內到外劣化管道壁。

- 降低這些高成本是工業界採用氣體分析儀作為預防措施的驅動力之一。氣體分析儀透過有效檢測此類氣體的存在,有助於監測洩漏,從而延長管道系統的使用壽命。石油和天然氣產業正在朝向可調諧二極體雷射 (TDL) 技術發展,因為 TDL 技術的高解析度可以實現可靠、準確的檢測,同時避免傳統分析儀的常見干擾。

- 根據國際能源總署 (IEA) 2022 年 6 月發布的公告,預計 2022 年全球淨精製能力將增加 100 萬桶/日,2023 年將再增加 160 萬桶/日。這一趨勢預計將進一步增加市場需求,因為煉油廠氣分析儀通常用於表徵原油精製過程中產生的氣體。

- 國際能源總署表示,預計 2021 年全球天然氣供應量將成長 4.1%,部分原因是新冠疫情後的市場復甦。在天然氣加工中,硫化氫 (H2S) 和二氧化碳 (CO2) 的檢測和監測至關重要,因此對氣體分析儀的需求很大。

- 該行業有許多正在進行和即將進行的計劃,涉及巨額投資以擴大生產。例如,西通道輸送2023計劃將在現有的25,000公里NGTL系統中增加約40公里的新天然氣管道,並將天然氣運往加拿大各地和美國市場。預計此類計劃將在預測期內繼續進行,從而推動對氣體分析儀的需求。

亞太地區預計將佔據主要市場佔有率

- 預計石油和天然氣、鋼鐵、電力、化學和石化行業新工廠的投資增加以及國際安全標準和實踐的採用將影響市場的成長。亞太地區是近年來唯一一個石油和天然氣產能成長的地區。該地區已開設約四家新煉油廠,為全球原油產量增加近 75 萬桶/日。

- 該地區的工業發展正在推動氣體分析儀的成長,因為它可用於製程監控、提高石油和天然氣工業的安全性、效率和品質等應用。因此,該地區的煉油廠正在其工廠安裝氣體分析儀。

- 預計預測期內亞太地區將成為全球氣體感測器市場成長最快的地區之一。這是由於政府法規越來越嚴格以及環保意識提升宣傳活動持續進行。此外,根據印度基礎設施基金會 (IBEF) 的數據,根據 2019-25 年國家基礎設施規劃,在預計總資本支出 111 億印度盧比(1.4 兆美元)中,能源產業計劃佔最高(24%)。

- 由於政府的嚴格監管,該地區近年來也出現了強勁成長。此外,政府對智慧城市計劃的投資激增可能為智慧感測器設備創造巨大的潛力,並推動該地區氣體感測器市場的成長。

- 亞太地區各國快速工業化是推動氣體檢測市場成長的主要因素之一。火力發電廠、煤礦、海綿鐵、鋼鐵、鐵合金、石油和化學品等高污染產業會產生煙霧、煙氣和有毒氣體排放。氣體檢測儀通常用於檢測可燃性氣體、易燃和有毒氣體,以確保工業操作安全。

氣體感測器、檢測器和分析儀器產業概況

氣體感測器、檢測器和分析儀市場分散,全球有許多參與者。目前,一些知名公司正在開發以檢測器為中心的應用產品。分析儀部門有廣泛的應用,包括臨床測試、環境排放控制、爆炸物檢測、農產品儲存和運輸以及職場危害監測。市場參與者正在採用夥伴關係、合併、擴張、創新、投資和收購等策略來增強其產品供應並獲得永續的競爭優勢。

- 2022 年 12 月 - 仕富梅Group Limited (Spectris PLC) 在韓國開設新的服務中心,將服務擴展到亞洲市場。該服務中心在龍仁正式揭牌,為半導體、石油和天然氣、發電和鋼鐵行業的工業過程和排放客戶提供寶貴的建議和幫助。

- 2022 年 8 月 - 艾默生宣布將在蘇格蘭開設一個氣體分析解決方案中心,以幫助工廠實現永續性目標。該中心擁有10多種不同的感測技術,能夠測量60多種不同的氣體成分。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業價值鏈分析

- 評估新冠肺炎對產業的影響

第5章 市場動態

- 市場促進因素

- 提高對工作場所事故的安全意識

- 手持設備的興起

- 市場限制

- 高成本,產品缺乏差異化

第6章 市場細分

- 氣體分析儀

- 科技

- 電化學公式

- 順磁性

- 鋯石

- 無損紅外線

- 最終用戶產業

- 石油和天然氣

- 化工和石化

- 用水和污水

- 藥品

- 其他最終用戶產業

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 科技

- 氣體感測器

- 類型

- 毒性

- 電化學

- 半導體

- 光電離

- 易燃

- 催化劑

- 紅外線的

- 最終用戶產業

- 石油和天然氣

- 化工和石化

- 用水和污水

- 金屬與礦業

- 公共產業

- 其他最終用戶產業

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 類型

- 氣體探測器

- 通訊類型

- 有線

- 無線的

- 探測器類型

- 固定的

- 可攜式的

- 最終用戶產業

- 石油和天然氣

- 化工和石化

- 用水和污水

- 金屬與礦業

- 公共產業

- 其他最終用戶產業

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 通訊類型

第7章 競爭格局

- 公司簡介

- Emerson Electric Company

- Teledyne API

- Siemens AG

- Servomex Group Limited(Spectris PLC)

- Honeywell Analytics Inc.

- Draegerwerk AG & Co KGaA

- Industrial Scientific Corporation

- MSA Safety Incorporated

- Crowncon Detection Instruments Limited

- Yokogawa Electric Corporation

- Control Instruments Corporation

- Membrapor AG

- Senseir AB

- Eaton Corporation PLC

- GfG Gas Detection UK Ltd

- Figaro Engineering Inc.

- Robert Bosch GmbH

- Thermofisher Scientific Inc.

- Detector Electronics Corporation

- Alphasense Limited

- California Analytical Instruments

- Testo SE & Co. KGaA

- Trolex Ltd

- Bacharach Inc.

- MKS Instruments Inc.

- RKI Instruments Inc.

- Horiba Ltd

- SGX Sensortech Limited(Amphenol Limited)

- Afriso-Euro-Index GmbH

- General Electric Company

- NGK Spark Plugs USA Inc.

- Delphi Technologies(BorgWarner Inc.)

- Denso Corporation

- 供應商市場佔有率分析

第8章投資分析

第9章市場機會與未來成長

The Gas Sensor, Detector And Analyzer Market size is estimated at USD 4.93 billion in 2025, and is expected to reach USD 6.48 billion by 2030, at a CAGR of 5.6% during the forecast period (2025-2030).

Gas sensors are chemical sensors that can measure the concentration of a constituent gas in its vicinity. These sensors embrace different techniques for quantifying a medium's exact amount of gas. A gas detector measures and indicates the concentration of certain gases in the air via other technologies. These are characterized by the type of gases they can detect in the environment. Gas analyzers find applications across safety instruments used in multiple end-user industries to maintain adequate safety in the workplace.

Key Highlights

- The global demand for gas analyzers has been boosted by an increase in shale gas and tight oil discoveries since these resources are utilized to stop corrosion in the infrastructure of natural gas pipelines. The use of gas analyzers has also been enforced in several industrial settings by government law and the enforcement of occupational health and safety rules. The growing public consciousness of the dangers of gas leaks and emissions contributed to the increased adoption of gas analyzers. Manufacturers are integrating gas analyzers with mobile phones and other wireless devices to offer real-time monitoring, remote control, and data backup.

- Gas leaks and other unintentional contamination can result in explosive consequences, physical harm, and fire risk. In confined spaces, numerous hazardous gases can even asphyxiate workers in the vicinity by displacing oxygen, which results in death. These outcomes jeopardize employee safety and the safety of equipment and property.

- Handheld gas detection tools keep personnel safe by monitoring a user's breathing zone while stationary and moving. These devices are critical in many situations where gas risks may exist. It is essential to monitor the air for oxygen, combustibles, and poisonous gases to ensure the safety of all people. Handheld gas detectors include built-in sirens that alert workers to potentially hazardous situations within an application, such as a confined space. When an alert is triggered, a large, easy-to-read LCD verifies the concentration of dangerous gas or gases.

- The production costs for gas sensors and detectors have steadily risen due to recent technological changes. While the market incumbents have been able to adapt to these changes, new entrants and mid-range manufacturers face considerable challenges.

- With the onset of COVID-19, multiple end-user industries in the market studied have been affected by reduced operations, temporary factory closures, etc. For instance, in the renewable energy industry, significant concerns revolve around global supply chains, which are considerably slowing down production, thus, aiming at reduced spending for new measurement systems and sensors. The detection and monitoring of hydrogen sulfide (H2S) and carbon dioxide (CO2) is pertinent in natural gas processing, creating significant demand for gas analyzers.

Gas Sensor, Detector, and Analyzer Market Trends

Oil and Gas Industry Segment is Expected to Hold Significant Market Share

- In the oil and gas industry, protecting a pressurized pipeline from corrosion and leaks and minimizing downtime are a few of the crucial responsibilities of the industry. As per a NACE (National Association of Corrosion Engineers) study, the total annual cost of corrosion in the oil and gas production industry is around USD 1.372 billion.

- The presence of oxygen in the gas sample determines a leak in the pressurized pipeline system. The continuous and undetected leak may worsen the situation while impacting on operational flow efficiency of the pipeline. Moreover, the presence of gases, such as hydrogen sulfide (H2S) and carbon dioxide (CO2), in the pipeline system reacting with oxygen can combine and form a corrosive and destructive mixture that can deteriorate the pipeline wall inside out.

- Mitigating such expensive costs is one of the drivers for adopting gas analyzers for preventive actions in the industry. Gas analyzer helps monitor leaks to extend the life of pipeline systems by effectively detecting the presence of such gases. The oil and gas industry is moving toward the TDL technique (tunable diode laser), which enables the reliability of detecting with precision because of its high-resolution TDL technique and avoids common interferences with traditional analyzers.

- As per the International Energy Agency's (IEA) June 2022, net global refining capacity is expected to expand by 1.0 million b/d in 2022 and by an additional 1.6 million b/d in 2023. With refinery gas analyzers commonly used to characterize gases produced during crude oil refining, such trends are expected to increase the market demand further.

- According to IEA, global natural gas supply increased by an estimated 4.1% globally in 2021, partly supported by the market recovery post the COVID-19 pandemic. The detection and monitoring of hydrogen sulfide (H2S) and carbon dioxide (CO2) is pertinent in natural gas processing, creating significant demand for gas analyzers.

- There are many ongoing and upcoming projects in the industry, with massive investments toward expanding production. For instance, the West Path Delivery 2023 project is expected to add about 40 km of new natural gas pipeline to the existing 25,000-km NGTL system, which ships gas across Canada and to the U.S. markets. Such projects are expected to continue during the forecast period, which will fuel the demand for gas analyzers.

Asia Pacific is Expected to Hold Significant Market Share

- Increased investments in new plants in oil and gas, steel, power, chemical, and petrochemicals and the rising adoption of international safety standards and practices are expected to influence market growth. Asia Pacific is the only region to register an oil and gas capacity growth in recent years. About four new refineries were added in the area, which has added nearly 750,000 barrels per day to global crude oil production.

- The development of industries in the region is driving the growth of gas analyzers, owing to their use in the oil and gas industry, such as monitoring processes, increased safety, enhanced efficiency, and quality. Hence, the refineries in the region are deploying gas analyzers in the plants.

- During the forecast period, Asia Pacific is anticipated to be one of the fastest-growing global gas sensors market regions. This is due to a rise in strict governmental regulations and ongoing environmental awareness campaigns. Further, according to IBEF, as per the National Infrastructure Pipeline 2019-25, energy sector projects accounted for the highest share (24%) out of the total expected capital expenditure of INR 111 lakh crore (USD 1.4 trillion).

- Also, the strict government regulations have recently shown significant growth in this region. Moreover, the surge in the government's investments in smart city projects creates a significant potential for smart sensor devices, likely to impel regional Gas Sensors Market growth.

- Rapid industrialization across the different countries in the Asia Pacific region is one of the primary factors driving the growth of the gas detectors market. Smoke, fumes, and toxic gas emissions occur due to highly polluting industries such as thermal power plants, coal mines, sponge iron, steel and ferroalloys, petroleum, and chemicals. Gas detectors are commonly used to detect combustible, flammable, and toxic gases and ensure safe industrial operations.

Gas Sensor, Detector, and Analyzer Industry Overview

The gas analyzer, sensor, and detector market is fragmented due to the presence of many players worldwide. Currently, some prominent companies are developing products with applications centering on the detector. The analyzer segment has applications across clinical assaying, environmental emission control, explosive detection, agricultural storage, shipping, and workplace hazard monitoring. Players in the market are adopting strategies such as partnerships, mergers, expansion, innovation, investment, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2022 - Servomex Group Limited (Spectris PLC) extended its offerings to the Asian market by opening a new service center in Korea. As the service center is officially unveiled at Yongin, customers from the semiconductor industry, as well as the industrial process and emissions for oil and gas, power generation, and steel industry, can access invaluable advice and assistance.

- August 2022 - Emerson has announced opening a gas analysis solutions center in Scotland to help plants meet sustainability goals. The center has access to more than ten different sensing technologies that can measure more than 60 other gas components.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 An Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Safety Awareness Regarding Occupational Hazards

- 5.1.2 Proliferation of Handheld Devices

- 5.2 Market Restraints

- 5.2.1 High Costs and Lack of Product Differentiation

6 MARKET SEGMENTATION

- 6.1 Gas Analyzers

- 6.1.1 Technology

- 6.1.1.1 Electrochemical

- 6.1.1.2 Paramagnetic

- 6.1.1.3 Zirconia

- 6.1.1.4 Non-disruptive IR

- 6.1.2 End-user Industry

- 6.1.2.1 Oil and Gas

- 6.1.2.2 Chemicals and Petrochemicals

- 6.1.2.3 Water and Wastewater

- 6.1.2.4 Pharmaceuticals

- 6.1.2.5 Other End-user Industries

- 6.1.3 Geography

- 6.1.3.1 North America

- 6.1.3.2 Europe

- 6.1.3.3 Asia-Pacific

- 6.1.3.4 Latin America

- 6.1.3.5 Middle-East and Africa

- 6.1.1 Technology

- 6.2 Gas Sensor

- 6.2.1 Type

- 6.2.1.1 Toxic

- 6.2.1.1.1 Electrochemical

- 6.2.1.1.2 Semiconductor

- 6.2.1.1.3 Photoionization

- 6.2.1.2 Combustible

- 6.2.1.2.1 Catalytic

- 6.2.1.2.2 Infrared

- 6.2.2 End-user Industry

- 6.2.2.1 Oil and Gas

- 6.2.2.2 Chemicals and Petrochemicals

- 6.2.2.3 Water and Wastewater

- 6.2.2.4 Metal and Mining

- 6.2.2.5 Utilities

- 6.2.2.6 Other End-user Industries

- 6.2.3 Geography

- 6.2.3.1 North America

- 6.2.3.2 Europe

- 6.2.3.3 Asia-Pacific

- 6.2.3.4 Latin America

- 6.2.3.5 Middle-East and Africa

- 6.2.1 Type

- 6.3 Gas Detectors

- 6.3.1 Communication Type

- 6.3.1.1 Wired

- 6.3.1.2 Wireless

- 6.3.2 Type of Detector

- 6.3.2.1 Fixed

- 6.3.2.2 Portable

- 6.3.3 End-user Industry

- 6.3.3.1 Oil and Gas

- 6.3.3.2 Chemicals and Petrochemicals

- 6.3.3.3 Water and Wastewater

- 6.3.3.4 Metal and Mining

- 6.3.3.5 Utilities

- 6.3.3.6 Other End-user Industries

- 6.3.4 Geography

- 6.3.4.1 North America

- 6.3.4.2 Europe

- 6.3.4.3 Asia-Pacific

- 6.3.4.4 Latin America

- 6.3.4.5 Middle-East and Africa

- 6.3.1 Communication Type

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Emerson Electric Company

- 7.1.2 Teledyne API

- 7.1.3 Siemens AG

- 7.1.4 Servomex Group Limited (Spectris PLC)

- 7.1.5 Honeywell Analytics Inc.

- 7.1.6 Draegerwerk AG & Co KGaA

- 7.1.7 Industrial Scientific Corporation

- 7.1.8 MSA Safety Incorporated

- 7.1.9 Crowncon Detection Instruments Limited

- 7.1.10 Yokogawa Electric Corporation

- 7.1.11 Control Instruments Corporation

- 7.1.12 Membrapor AG

- 7.1.13 Senseir AB

- 7.1.14 Eaton Corporation PLC

- 7.1.15 GfG Gas Detection UK Ltd

- 7.1.16 Figaro Engineering Inc.

- 7.1.17 Robert Bosch GmbH

- 7.1.18 Thermofisher Scientific Inc.

- 7.1.19 Detector Electronics Corporation

- 7.1.20 Alphasense Limited

- 7.1.21 California Analytical Instruments

- 7.1.22 Testo SE & Co. KGaA

- 7.1.23 Trolex Ltd

- 7.1.24 Bacharach Inc.

- 7.1.25 MKS Instruments Inc.

- 7.1.26 RKI Instruments Inc.

- 7.1.27 Horiba Ltd

- 7.1.28 SGX Sensortech Limited (Amphenol Limited)

- 7.1.29 Afriso-Euro-Index GmbH

- 7.1.30 General Electric Company

- 7.1.31 NGK Spark Plugs USA Inc.

- 7.1.32 Delphi Technologies (BorgWarner Inc.)

- 7.1.33 Denso Corporation

- 7.2 Vendor Market Share Analysis

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE GROWTH

氣體感測器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

氣體感測器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 氣體感測器市場:全球2025-2029

氣體感測器市場:全球2025-2029 2025-2029年全球油質感測器市場

2025-2029年全球油質感測器市場 2025 年石油和天然氣感測器全球市場報告2025 年氣體感測器全球市場報告氣體感測器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、技術、應用、地區和競爭細分,2020-2030 年

2025 年石油和天然氣感測器全球市場報告2025 年氣體感測器全球市場報告氣體感測器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、技術、應用、地區和競爭細分,2020-2030 年 全球氣體感測器市場:按產品、按輸出類型、按連接、按技術、按類型、按最終用途、按地區 - 預測到 2032 年CO 氣體感測器 -市場佔有率分析、行業趨勢/統計、成長預測 (2025-2030)拉丁美洲氣體感測器:市場佔有率分析、產業趨勢、成長預測(2025-2030)歐洲氣體感測器:市場佔有率分析、產業趨勢、統計、成長預測(2025-2030)

全球氣體感測器市場:按產品、按輸出類型、按連接、按技術、按類型、按最終用途、按地區 - 預測到 2032 年CO 氣體感測器 -市場佔有率分析、行業趨勢/統計、成長預測 (2025-2030)拉丁美洲氣體感測器:市場佔有率分析、產業趨勢、成長預測(2025-2030)歐洲氣體感測器:市場佔有率分析、產業趨勢、統計、成長預測(2025-2030)