|

市場調查報告書

商品編碼

1685936

越南生物農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Vietnam Biopesticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

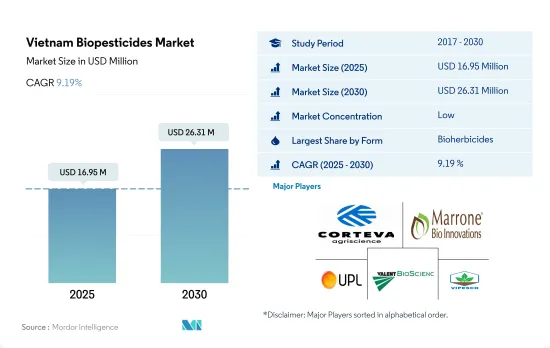

越南生物農藥市場規模預計在 2025 年為 1,695 萬美元,預計在 2030 年將達到 2,631 萬美元,在市場估計和預測期(2025-2030 年)內以 9.19% 的複合年成長率成長。

- 生物農藥是基於微生物、植物抽取物和其他天然化合物的安全農作物保護產品。它對於綜合蟲害管理(IPM)來說具有許多有吸引力的特性。生物防治促進有益微生物的生長,同時消滅有害害蟲。根據糧農組織統計,農業病蟲害造成的作物損失每年達40.0%。

- 生物農藥在越南生物農藥市場佔據主導地位,2022 年佔 31.5% 的佔有率。在越南,用作生物除草劑的菌屬包括炭疽菌、鐮刀菌、鍊格孢菌、尾孢菌、柄銹菌、根腐菌、殼鬥菌和核盤菌。越南制定了農業生態政策來促進特定的農業生態,如農林業、綜合病蟲害管理(IPM)、綜合作物管理(ICM)、農業實踐標準化、有機生產、食品安全病蟲害防治以及保護和景觀農業政策。

- IPM 和 ICM 旨在幫助農民了解他們的田間生態系統,使用適當的農業技術,有效地管理他們的生產系統,種植健康的作物,並減少田間農藥和化肥的使用。這些政策預計將促進該國生物農藥市場的發展。

- 農藥行動網路(PAN)亞太區(PANAP)是一個致力於消除農藥使用對人類和環境造成的危害並促進基於生物多樣性的生態農業的全球性組織。該計畫也提高了人們對農藥不良影響的認知,預計將推動2023年至2029年間生物農藥國內市場價值成長68.0%。

越南生物農藥市場趨勢

該國計劃擴大有機農業,由於需求不斷成長,水果和蔬菜將成為首要任務。

- 2022年,越南有機作物種植面積將達38,000公頃,約佔亞太地區有機農地總面積的1%。越南目前擁有約17,000家有機生產商、555家加工商和60家出口商。

- 隨著消費者的健康意識增強,全球有機農產品需求預計將激增,越南正尋求擴大有機農產品的出口。有機水果蔬菜種植是該國有機農業的主導,2022 年佔 58.8%,其次是經濟作物(35.7%)和連續作物(5.5%)。

- 隨著2017年以來國家政策的訂定以及《促進越南有機農業發展的國家有機標準》、《有機農業法令》、《2020-2030年國家有機農業計劃》等政府計劃的訂定,越來越多的省市正在積極制定地方計劃和計劃,發展有機農業。

- 有機農業在越南蓬勃發展,許多計劃由政府、國際合作夥伴和私營部門資助。參與式保障體系(PGS)越來越受歡迎,並正在許多社區實施。越南有機農業協會(VOAA)目前在13個省份擁有17個PGS小組,其中5個已投入營運,其餘處於規劃階段。這些PGS集團產品包括蔬菜、米、柳橙、柚子等。

- 越南有機產品銷往180個國家。越南已設定目標,2030年將有機農業面積擴大到總農地面積的2.5-3%。

約 88% 的河內消費者願意購買有機農產品,導致人均消費量增加。

- 越南民眾逐漸重視產品的品質和健康。健康和健身是越南消費者最關心的五大議題之一。越南的人均收入不斷增加,鼓勵人們在營養食品上花費更多。

- 蔬菜中高濃度的農藥和化肥一直對越南人民來說是危險的。河內約30%的蔬菜產區由政府管理,並認證為安全。根據對河內四家大型超級市場185名受訪者進行的調查的說明統計和分析結果顯示,約有15%的消費者已經有過購買有機蔬菜的經驗。然而,如果市場上有有機產品,88% 的人願意購買。

- 有機食品消費有限的主要原因是缺乏有關有機市場的資訊以及購買有機產品的不便。有機蔬菜的平均價格比常規蔬菜高出約70%。此外,高所得的顧客更關心蔬菜的安全性,以前消費過有機產品的顧客更有可能為有機蔬菜支付更高的價格。這些結果表明應該向消費者廣泛傳播有關有機蔬菜的訊息。

- 越南有機食品消費量的增加將導致國內需求的增加。因此,需要鼓勵將土地轉變為有機農業,以生產所需的產品。因此,需要增加對有機保護和營養產品的需求以確保產品質量,從而決定該國生物農藥市場的潛在成長。

越南生物農藥產業概況

越南生物農藥市場較為分散,前五大企業市佔率合計為3.46%。市場的主要企業有:Corteva Agriscience、Marrone Bio Innovations Inc.、UPL、Valent BioSciences LLC 和 Vipesco。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 有機種植區

- 有機產品人均支出

- 法律規範

- 越南

- 價值鍊和通路分析

第5章市場區隔

- 形式

- 生物真菌劑

- 生物除草劑

- 生物殺蟲劑

- 其他生物防治劑

- 作物類型

- 經濟作物

- 園藝作物

- 耕地作物

第6章 競爭格局

- 重大策略舉措

- 市場佔有率分析

- 商業狀況

- 公司簡介.

- Biotech Bio-Agriculture

- Corteva Agriscience

- Marrone Bio Innovations Inc.

- UPL

- Valent BioSciences LLC

- Vipesco

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 49580

The Vietnam Biopesticides Market size is estimated at 16.95 million USD in 2025, and is expected to reach 26.31 million USD by 2030, growing at a CAGR of 9.19% during the forecast period (2025-2030).

- Biopesticides are crop protection products that are safe to use and are based on microorganisms, plant extracts, and other natural compounds. They have a variety of appealing properties for Integrated Pest Management (IPM). Biopesticides encourage the growth of beneficial microorganisms while controlling harmful pests. According to FAO, agricultural pests cause up to 40.0% of crop loss annually.

- Bioherbicides dominate the biopesticides market in the country, and they accounted for a share of 31.5% in 2022. In Vietnam, some genera used as bioherbicides are Colletotrichum, Fusarium, Alternaria, Cercospora, Puccinia, Entyloma, Ascochyta, and Sclerotinia, Agroecology policies are developed in Vietnam in order to promote particular agroecological practices like agroforestry, Integrated Pest Management (IPM), Integrated Crop Management (ICM), standardization of agricultural practices organic production, food safety control, and conservation and landscape agriculture policies.

- IPM and ICM are intended to assist farmers in understanding the field ecology, using suitable farming techniques, managing the production system effectively, growing healthy crops, and using fewer pesticides and fertilizers in fields. These policies are expected to propel the biopesticides market in the country.

- Pesticide Action Network (PAN) Asia Pacific (PANAP) is a global organization working to eliminate the harm that pesticide usage causes to people and the environment and advance ecological agriculture based on biodiversity. This program also raises awareness about the negative consequences of pesticides, which is expected to increase the domestic market value of biopesticides between 2023 and 2029 by 68.0%.

Vietnam Biopesticides Market Trends

The country plans to expand organic farming, with fruits and vegetables as the top priority due to increasing demand

- The area under organic crop cultivation in Vietnam was recorded at 38.0 thousand hectares in 2022, around 1% of the overall Asia-Pacific organic agricultural land. In Vietnam, there are currently approximately 17,000 organic agriculture producers, 555 processors, and 60 exporters.

- Vietnam has been trying to increase the export of organic farm produce as global demand is expected to rise rapidly as consumers become more health conscious. Organic cultivation in the fruit and vegetable crops is dominating the country's organic farming, and it accounted for 58.8% in 2022, followed by cash crops and row crops, accounting for 35.7% and 5.5% in the same year, respectively.

- With national policies issued since 2017 and government programs such as the National Organic Standard, the Decree on Organic Agriculture, and the National Organic Agriculture Project 2020-2030 to promote organic agriculture in Vietnam, more provinces and cities have actively developed local programs and projects to develop organic agriculture.

- Organic agriculture is thriving in Vietnam, with numerous projects funded by the government, international partners, and the private sector. Participatory Guarantee Systems (PGS) are becoming more popular and are being replicated in an increasing number of communities. The Vietnam Organic Agriculture Association (VOAA) currently has 17 PGS groups in 13 provinces, five of which are operational and the rest in the planning stages. These PGS groups' products include vegetables, rice, oranges, and grapefruits.

- Organic products from Vietnam are available in 180 countries. Vietnam has set a target of increasing the total organic land area to 2.5-3% of the total agricultural land area by 2030.

Approximately 88% of the Hanoi consumers are willing to by organic produce, leads to increase in per capita spending.

- People in Vietnam have gradually begun to pay more attention to product quality and health than they had previously. Health and fitness are still among Vietnamese consumers' top five concerns. Vietnam's per capita income has continuously increased, encouraging people to spend more on nutritious food.

- High levels of pesticides and chemical fertilizers inside vegetables are always risky for Vietnamese people. Around 30% of the area for vegetable production in Hanoi is controlled and safely certified by the government. Descriptive statistics and the results analyzed a sample of 185 respondents surveyed at four big supermarkets in Hanoi concluded that about 15% of the consumers already had the experience of using organic vegetables. However, 88% wanted to try and buy organic products if they were available in the market.

- Major reasons for the limitation in the consumption of organic foods were the lack of information about the organic market and the inconvenience of buying organic products. The average price for organic vegetables was about 70% higher than that of conventional ones. High-income customers were also concerned about the safety of vegetables, and those who previously consumed organic products were likely to pay more for organic vegetables. These findings suggest that information about organic vegetables should be widely publicized to consumers.

- The rising organic food consumption in Vietnam leads to increasing domestic demand. This requires a higher land conversion to organic farming to produce the desired product. A subsequent increase in the demand for organic protection and nutrition products is needed to ensure the quality of the product, thus determining potential growth in the biofertilizers market in the country.

Vietnam Biopesticides Industry Overview

The Vietnam Biopesticides Market is fragmented, with the top five companies occupying 3.46%. The major players in this market are Corteva Agriscience, Marrone Bio Innovations Inc., UPL, Valent BioSciences LLC and Vipesco (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Biofungicides

- 5.1.2 Bioherbicides

- 5.1.3 Bioinsecticides

- 5.1.4 Other Biopesticides

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Biotech Bio-Agriculture

- 6.4.2 Corteva Agriscience

- 6.4.3 Marrone Bio Innovations Inc.

- 6.4.4 UPL

- 6.4.5 Valent BioSciences LLC

- 6.4.6 Vipesco

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

生物農藥市場:全球產業分析、市場規模、佔有率、成長、趨勢與未來預測(2025-2032)

生物農藥市場:全球產業分析、市場規模、佔有率、成長、趨勢與未來預測(2025-2032) 生物農藥市場規模、佔有率及成長分析(按類型、來源、劑型、應用類型、作物類型和地區)-2025-2032 年產業預測

生物農藥市場規模、佔有率及成長分析(按類型、來源、劑型、應用類型、作物類型和地區)-2025-2032 年產業預測 歐洲生物防治化學品:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)生物農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國生物防治劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

歐洲生物防治化學品:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)生物農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國生物防治劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 全球生物農藥市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 至 2033 年預測

全球生物農藥市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 至 2033 年預測 2025 年生物防治全球市場報告生物殺線蟲劑市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、形式、作物類型、治療方式、感染、地區和競爭進行細分,2020 年至 2030 年預測生物農藥市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按作物類型、按應用、按配方、按地區和競爭進行細分,2020-2030 年

2025 年生物防治全球市場報告生物殺線蟲劑市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、形式、作物類型、治療方式、感染、地區和競爭進行細分,2020 年至 2030 年預測生物農藥市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按作物類型、按應用、按配方、按地區和競爭進行細分,2020-2030 年 全球生物農藥市場按類型、作物類型、配方、原料、使用方法和地區分類 - 預測至 2029 年

全球生物農藥市場按類型、作物類型、配方、原料、使用方法和地區分類 - 預測至 2029 年

▼