|

市場調查報告書

商品編碼

1685939

北美飼料酸味劑:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)North America Feed Acidifiers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

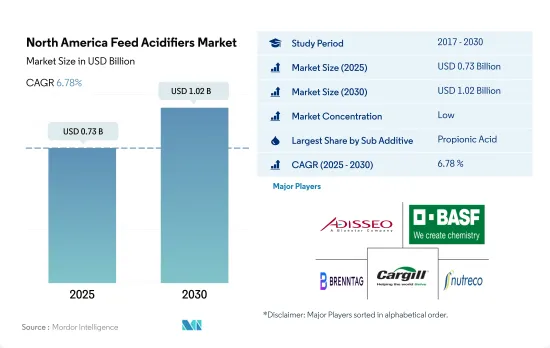

北美飼料酸味劑市場規模預計在 2025 年為 7.3 億美元,預計到 2030 年將達到 10.2 億美元,預測期內(2025-2030 年)的複合年成長率為 6.78%。

- 飼料酸味劑對於促進動物生長、增強新陳代謝、抵抗有害病原體並減少對抗生素的依賴具有重要意義。預計到 2022 年,北美飼料酸味劑市場將佔飼料添加劑總市場的 7.1%,2019 年將較 2018 年成長 18.8%。這一高佔有率歸因於飼料產量增加導致益生菌類型的市場價值增加。

- 美國將主導北美飼料酸味劑市場,到 2022 年將佔 70%,這主要歸因於該國飼料產量的增加以及肉類和乳製品市場不斷成長的需求。在所有飼料酸味劑中,丙酸是使用最多的,2022 年的價值接近 2 億美元,其次是富馬酸和乳酸,分別佔市場的 25% 和 22.8%。

- 由於對反芻動物產品的需求量很大,反芻動物將在飼料丙酸領域佔據最大佔有率,到 2022 年將達到 38.8%。美國是飼料酸味劑市場成長最快的國家,預計在預測期內的複合年成長率為 7%。預計未來幾年,肉類(尤其是雞肉和豬肉)需求的增加、乳製品需求的增加以及水產養殖業的擴張將推動該國飼料酸味劑市場的發展。

- 對肉類和水產品的需求不斷成長以及對飼料添加劑對動物生產力益處的認知不斷提高是北美飼料酸味劑市場(尤其是在美國)發展的主要驅動力。

- 北美飼料酸味劑市場近年來穩定成長,預計2022年將佔全球市場的7.1%,市場規模達6.5億美元。由於對肉類和肉類的需求不斷增加,酸味劑在動物飼料中的使用範圍不斷擴大,導致2019年的市場規模較2018年成長了18.7%。

- 在所有動物種類中,反芻動物是飼料酸味劑的最大使用者,2022 年該部分的市值為 2.3 億美元。這一趨勢主要是由於乳製品產業的高需求。家禽業緊隨其後,2022 年的市場佔有率為 35.4%。然而,由於益生菌對動物健康的正面影響,豬業正在成為成長最快的行業,預計在預測期內的複合年成長率將達到 6.7%。

- 美國是北美最大的飼料酸味劑市場,佔2022年總市場佔有率的70%。它也是北美飼料酸味劑市場成長最快的國家,預計在預測期內複合年成長率為7%。

- 在酸化劑類型中,丙酸、富馬酸和乳酸是北美最常用的,分別佔該地區市場以金額為準的 37.1%、25.1% 和 22.7%。這些酸味劑的流行與它們在多種動物中的益處和應用密切相關,即提高飼料的偏好和增加飼料攝入量。

- 據估計,肉類和肉類產品需求的不斷增加、人均肉品消費量和牲畜數量的增加將推動北美飼料酸味劑市場在預測期內以 6.7% 的複合年成長率成長。

北美飼料酸味劑市場趨勢

禽肉消費量高於紅肉,而且美國是世界上最大的雞蛋和禽肉生產國,這推動了禽肉生產的需求。

- 北美家禽業在過去幾年經歷了強勁成長,2017 年至 2022 年家禽數量將增加 5.0%。這種成長很大程度上是由於對雞肉和其他雞肉產品的需求不斷增加。美國是世界上最大的雞肉生產國和第二大出口國,並且作為最大的雞蛋生產國,主導北美雞肉產業。到2022年,美國將佔該地區雞肉總產量的62.0%。該行業的高利潤率正在吸引新的雞肉生產商,從而導致該地區生產商數量的增加。例如,加拿大的雞蛋生產商數量將從2016年的1,062家增加到2021年的1,205家。

- 家禽,尤其是肉雞,產量很大,因為它比其他牲畜更快成熟並達到市場重量。家禽(包括肉雞)可以在狹小的空間內飼養,這使得生產者可以在包括小塊土地在內的各種環境中飼養家禽。這些優點使得家禽養殖更加可行。 2022年墨西哥雞肉產量與前一年同期比較去年同期成長12%。

- 家禽消費量遠消費量牛肉和豬肉。由於食用紅肉的健康風險越來越大,越來越多的人選擇雞肉作為更精簡、更健康的蛋白質來源。預計這一趨勢將持續下去並推動該地區家禽業的成長。預計預測期內國內外市場對雞肉產品的需求不斷增加以及雞肉產量不斷上升將進一步推動市場成長。

零售貿易的擴大和對高品質水產品的需求正在增加對富含大量和微量營養素的水產養殖飼料的需求。

- 北美水產養殖飼料產量佔全球產量的比例很小,到2022年僅3.8%。然而,對多樣化水產品的需求正在推動當地水產養殖生產。 2017年至2022年飼料產量將成長9.2%。為滿足日益成長的營養均衡飼料需求,該地區的飼料製造商計劃將產量從2022年的220萬噸增加到2029年的260萬噸。為水產養殖物種提供的配方飼料含有集約化養殖條件下健康生長所需的大量和微量營養素,從而促進了該地區對水產飼料的需求成長。

- 魚類是飼料產量最突出的物種,佔2022年飼料產量的73.2%。人們對魚類在人類飲食中的健康益處的認知不斷提高、食品消費模式的改變、零售業的擴張以及國際市場的高需求,都促進了該地區魚類產量的成長。由於生產商專注於營養管理以確保動物健康和性能,魚飼料產量預計將從 2022 年的 160 萬噸增加到 2029 年的 190 萬噸。

- 2020 年,加拿大水產養殖生產商在飼料上的支出為 3.938 億美元,比 2016 年增加 6.6%,顯示對高品質海鮮的需求增加。總體而言,對多樣化水產品日益成長的需求以及對養殖物種營養均衡飼料的需求預計將在未來幾年推動北美水產養殖飼料產量的成長。

北美飼料酸味劑產業概況

北美飼料酸味劑市場分散,前五大公司佔25.96%的市佔率。該市場的主要企業有:安迪蘇、BASFSE、Brenntag SE、嘉吉公司和 SHV(Nutreco NV)(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 動物數量

- 家禽

- 反芻動物

- 豬

- 飼料生產

- 水產養殖

- 家禽

- 反芻動物

- 養豬業

- 法律規範

- 加拿大

- 墨西哥

- 美國

- 價值鍊和通路分析

第5章市場區隔

- 副添加劑

- 富馬酸

- 乳酸

- 丙酸

- 其他酸味劑

- 動物

- 水產養殖

- 按亞動物

- 魚

- 蝦

- 魚

- 其他養殖物種

- 家禽

- 按亞動物

- 肉雞

- 圖層

- 其他鳥類

- 反芻動物

- 小動物

- 肉牛

- 乳牛

- 其他反芻動物

- 豬

- 其他動物

- 水產養殖

- 國家

- 加拿大

- 墨西哥

- 美國

- 北美其他地區

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介.

- Adisseo

- Alltech, Inc.

- BASF SE

- Bio Agri Mix

- Brenntag SE

- Cargill Inc.

- EW Nutrition

- Kemin Industries

- SHV(Nutreco NV)

- Yara International ASA

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 全球市場規模和DRO

- 資訊來源及延伸閱讀

- 圖表清單

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 49634

The North America Feed Acidifiers Market size is estimated at 0.73 billion USD in 2025, and is expected to reach 1.02 billion USD by 2030, growing at a CAGR of 6.78% during the forecast period (2025-2030).

- Feed acidifiers are important in promoting animal growth, increasing metabolism, and providing resistance to harmful pathogens while reducing dependence on antibiotics. The North American feed acidifiers market accounted for 7.1% of the total feed additives market in 2022, an 18.8% increase in 2019 compared to 2018. This high share was attributed to the increased market value of probiotic types due to increased feed production.

- The United States dominated the North American feed acidifiers market, accounting for 70% in 2022, mainly due to higher feed production and demand from the country's growing meat and dairy product markets. Among all feed acidifiers, propionic acid was most significantly used, valued at almost USD 0.2 billion in 2022, followed by fumaric acid and lactic acid, accounting for 25% and 22.8% of the market, respectively.

- Ruminants held the largest share of the feed propionic acid segment, accounting for 38.8% in 2022 due to the high demand for ruminant products. The United States is the fastest-growing country in the feed acidifiers market, with a projected CAGR of 7% during the forecast period. The increasing demand for meat, especially poultry and pork, the rising demand for dairy products, and the growing aquaculture cultivation are expected to drive the country's feed acidifiers market in the coming years.

- The rising demand for meat and seafood and increasing awareness about the benefits of feed additives in animal productivity are the major drivers of the North American feed acidifiers market, especially in the United States.

- The North American feed acidifiers market has grown steadily in recent years, and in 2022, it accounted for 7.1% of the global market, with a value of USD 0.65 billion. The use of acidifiers in animal feed has expanded due to the rising demand for meat and meat products, which resulted in an 18.7% increase in the market's value in 2019 compared to 2018.

- Among all animal types, ruminants are the biggest users of feed acidifiers, and the segment accounted for a market value of USD 0.23 billion in 2022. This trend was mainly due to the high demand from dairy industries. The poultry segment followed closely behind, with a market share of 35.4% in 2022. However, swine is emerging as the fastest-growing segment, expected to record a CAGR of 6.7% during the forecast period due to the positive impact of probiotics on animal health.

- The United States is the largest feed acidifiers market in North America, accounting for 70% of the total market share in 2022. It is also the fastest-growing country in the North American feed acidifiers market, expected to witness a CAGR of 7% during the forecast period.

- Among acidifier types, propionic acid, fumaric acid, and lactic acid are the most commonly used in North America, accounting for 37.1%, 25.1%, and 22.7%, respectively, of the total regional market by value. The popularity of these acidifiers is closely linked to their benefits and application in different animals for enhancing feed intake by increasing the palatability of feed.

- The increase in demand for meat and meat products and the rising per capita meat consumption and livestock population are estimated to drive the North American feed acidifiers market with a CAGR of 6.7% during the forecast period.

North America Feed Acidifiers Market Trends

Higher consumption of poultry meat than red meat and the United States is globally largest producer of eggs and poultry meat is driving the demand for poultry production

- The North American poultry industry has experienced significant growth over the past few years, with the poultry headcount increasing by 5.0% from 2017 to 2022. This growth is largely due to the increasing demand for poultry meat and other poultry products. The United States dominates the North American poultry industry as the world's largest producer and second-largest exporter of poultry meat and a major egg producer. The United States accounted for 62.0% of the region's total poultry production in 2022. The high-profit margin in the industry is attracting new poultry producers, leading to an increase in the number of producers in the region. For example, Canada's number of egg producers increased from 1,062 in 2016 to 1,205 in 2021.

- Poultry birds, especially broiler meat, are produced in large quantities due to their quick maturity and market weight, which is faster than other livestock. Poultry birds, including broilers, can be raised in small spaces, making it possible for producers to raise poultry in a variety of environments, including small plots of land. These advantages make poultry production more feasible. Mexican poultry production increased by 12% in 2022 from the previous year.

- Poultry meat consumption is significantly higher than that of beef or pork. More people are choosing poultry as a leaner, healthier source of protein due to the rising health risks linked to eating red meat. This trend is expected to continue, driving the growth of the region's poultry industry. The increasing demand for poultry products from both domestic and international markets and rising poultry production are expected to further drive the growth of the market during the forecast period.

Expansion of retail industry, and demand for high-quality seafood is increasing the demand for macro-nutrients and micro-nutrients rich aquaculture feed

- Aquaculture feed production in North America accounted for a small fraction of global production, representing only 3.8% in 2022. However, the demand for diverse seafood products is driving local aquaculture production. Feed production grew by 9.2% between 2017 and 2022. In response to the increasing demand for nutritionally balanced feed, feed millers in the region plan to increase production from 2.2 million metric tons in 2022 to 2.6 million metric tons in 2029. The compound feed offered to aquaculture species contains the macro and micronutrients needed for healthy growth under intensive rearing conditions, thus contributing to the increased demand for aquaculture feed in the region.

- Fish, which accounted for 73.2% of feed production in 2022, is the most prominent species in terms of feed production. The rising awareness of the health benefits of fish in the human diet, changing food consumption patterns, the expanding retail sector, and high demand in the international market are contributing to the growth of fish production in the region. Fish feed production is expected to increase from 1.6 million metric tons in 2022 to 1.9 million metric tons in 2029 as producers focus on nutritional management to ensure the health and performance of their animals.

- Canada's aquaculture producers spent USD 393.8 million on feed in 2020, a 6.6% increase from 2016, demonstrating the increasing demand for high-quality aquatic food. Overall, the increasing demand for diverse seafood products and the need for nutritionally balanced feed for aquaculture species are expected to drive the growth of aquaculture feed production in North America in the coming years.

North America Feed Acidifiers Industry Overview

The North America Feed Acidifiers Market is fragmented, with the top five companies occupying 25.96%. The major players in this market are Adisseo, BASF SE, Brenntag SE, Cargill Inc. and SHV (Nutreco NV) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Additive

- 5.1.1 Fumaric Acid

- 5.1.2 Lactic Acid

- 5.1.3 Propionic Acid

- 5.1.4 Other Acidifiers

- 5.2 Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 fish

- 5.2.1.1.4 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Adisseo

- 6.4.2 Alltech, Inc.

- 6.4.3 BASF SE

- 6.4.4 Bio Agri Mix

- 6.4.5 Brenntag SE

- 6.4.6 Cargill Inc.

- 6.4.7 EW Nutrition

- 6.4.8 Kemin Industries

- 6.4.9 SHV (Nutreco NV)

- 6.4.10 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

亞太地區酸味劑市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太地區酸味劑市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 歐洲飼料酸味劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)

歐洲飼料酸味劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年) 飼料酸味劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

飼料酸味劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 飼料酸味劑市場:未來預測(2025-2030)

飼料酸味劑市場:未來預測(2025-2030) 2025 年全球飼料酸味劑市場報告

2025 年全球飼料酸味劑市場報告 飼料酸味劑市場規模、佔有率、成長分析,按類型、形式、化合物、牲畜、地區 - 產業預測,2024-2031 年

飼料酸味劑市場規模、佔有率、成長分析,按類型、形式、化合物、牲畜、地區 - 產業預測,2024-2031 年 飼料酸化劑市場:按化合物、形式、牲畜、類型分類 - 2025-2030 年全球預測

飼料酸化劑市場:按化合物、形式、牲畜、類型分類 - 2025-2030 年全球預測 全球飼料酸化劑市場 - 2024-2031

全球飼料酸化劑市場 - 2024-2031 飼料酸化劑市場-2018-2028年全球產業規模、佔有率、趨勢、機會和預測,按副添加劑(富馬酸、乳酸、丙酸)、動物(水產養殖、家禽、反芻動物、豬)和地區細分, 競賽

飼料酸化劑市場-2018-2028年全球產業規模、佔有率、趨勢、機會和預測,按副添加劑(富馬酸、乳酸、丙酸)、動物(水產養殖、家禽、反芻動物、豬)和地區細分, 競賽