|

市場調查報告書

商品編碼

1686299

無線感測器:市場佔有率分析、行業趨勢和成長預測(2025-2030)Wireless Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

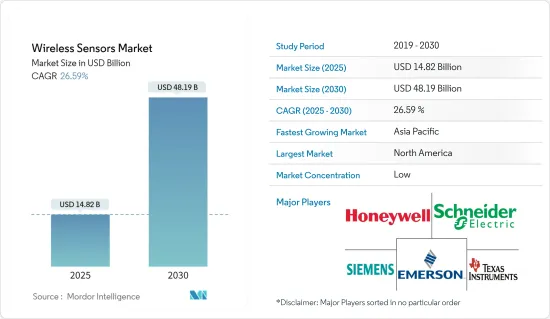

無線感測器市場規模預計在 2025 年為 148.2 億美元,預計到 2030 年將達到 481.9 億美元,在市場估計和預測期(2025-2030 年)內的複合年成長率為 26.59%。

無線感測器在RFID和藍牙等各種創新技術的幫助下,具有準確性和可靠性等多種優勢,並且可以更輕鬆地整合到電子設備中。因此,它在過去幾年裡獲得了許多支持。這些感測器主要用於工廠監控生產流資料。其他應用包括汽車、國防、建築自動化以及物料輸送、食品和飲料等其他產業。對新能源來源的不斷探索、政府法規、可再生能源開發以及快速的技術進步正在推動無線感測器市場的發展。

主要亮點

- 無線感測器被視為智慧電網中用於遠端監控電力線和變壓器的重要組成部分。無線感測器用於監測電力線上的溫度和天氣。工業自動化以及對小型消費性設備(如穿戴式裝置和物聯網連接設備)的需求是推動無線感測器市場發展的關鍵因素。

- 由於政府對使用感測器來增強安全性的監管日益嚴格,對無線感測器的需求也日益成長。例如,在石油鑽井平台、鍋爐等環境條件惡劣的區域,則有高壓、高溫等。無線感測器讓您可以輕鬆地從安全距離控制和監控您的設施。

- 工業 4.0 革命使機器變得更加智慧、更加直覺,從而推動了無線感測器工業應用的需求。新設備的設計更有效率、安全、靈活,並能夠自主監控其性能、使用情況和故障。因此,這些應用正在推動對高靈敏度感測器的需求。

- 物聯網的普及也是推動市場成長的一個主要因素。物聯網連接設備的增加預計將推動對無線感測器的需求。此外,智慧家庭、智慧建築、智慧城市和智慧工廠的發展需要無線感測器,因為它們外形規格小、精度高、功耗低,並且能夠控制周圍參數。

- 這些感測器降低了安裝成本,並最大限度地減少了對人員和室內裝飾的干擾,因為安裝無線感測器系統不需要對建築物進行佈線或結構變更。許多企業正在投資無線技術,因為它具有成本效益、安全且方便。

- 例如,Monnit 公司最近宣布推出 ALTA 土壤濕度感測器,以滿足農業科技市場的需求。這種創新的土壤濕度感測器可幫助農民、商業種植者和溫室管理者輕鬆地將他們的精準灌溉作業連接到物聯網 (IoT)。國防部門正在採用無線感測器技術。這些感測器可以監控場所、識別可疑活動並追蹤有價值的資產。

- 然而,對高性能、具成本效益和高可靠性感測器的需求不斷成長,推動市場供應商增加對研發活動的支出。預計奈米技術和微技術的進步將在預測期內推動無線感測器市場的成長。

無線感測器市場趨勢

能源和電力佔據較大的市場佔有率

- 節能對於企業減少電力消耗和相關成本以及最大限度地減少對環境的影響(包括生態足跡)變得越來越重要。為了提高節能效果,可攜式和固定式氣象站、風力發電系統、柴油卡車排放測試儀器、新建築設計空氣動力學的風動態、高空氣象研究氣球、海洋調查、水污染儀器、空氣品質調查、煙囪汞採樣等都需要精確的無線感測器測量。

- 零功率無線感測器需要能量處理低功耗管理電路來監控換能器輸出功率、儲存能量並為無線感測器的其餘部分供電。能源採集有助於為工業應用中的無線感測網路供電。低功耗、可靠的無線通訊、感測器和能源採集技術的進步使得這種通訊方式比有線基礎設施更加實用和高效。

- 隨著電動車和自動駕駛汽車等未來技術創新,汽車領域對這些無線壓力感測器的需求預計將會增加。動力傳動系統應用佔業務的 50% 以上,其次是安全應用,其中輪胎壓力管理系統 (TPMS) 是最重要的單一汽車應用。在二氧化碳排放和自動化的推動下,無線壓力感測器在未來將得到更廣泛的採用和使用。

- 基於能源採集的自主無線感測器節點是一種方便且經濟高效的解決方案。能源採集的使用消除了限制無線節點廣泛採用的關鍵限制。電源的稀缺性具有必要的特性,可以為感測器節點提供多年的能量和電力,而無需更換電池。與硬佈線解決方案相比,部署零無線感測器可實現顯著的經濟優勢。據英國石油公司稱,印度的初級能源消費量最近達到約35.4艾焦耳,推動了能源和電力產業對無線感測器的需求。

亞太地區快速成長

- 亞太地區是電氣和電子設備製造市場最大的地區之一。該地區也是無線感測器技術的重要供應商,尤其是中國和日本。中國是全球最大的汽車市場,也是全球最大的汽車生產基地,包括電動車生產基地,具有巨大的成長潛力。根據中國工業協會統計,近期中國商用車銷量約31.7萬輛。中國銷量約佔全球汽車銷量的32.56%。

- 這些行業佔據了無線感測器市場的很大一部分,因此該地區將在預測期內提供機會。聯網汽車概念和汽車安全法規的興起也有望推動該地區無線感測器的採用。

- 在汽車中,液壓煞車是保障乘客安全的重要部件。您使用煞車控制車輛的能力歸功於包括壓力感測器在內的複雜組件的組合。據 Auto Punditz 稱,二輪車是 2022 會計年度印度銷售的主要電動車類型,銷量達到約 231,000 輛,推動了汽車行業對無線壓力感測器的需求。

- 無線感測器日益普及的另一個原因是該地區積極部署無線感測器,以加強不斷成長的 IT 醫療保健市場並創新新的醫療保健設備和器械。

- 橫河電機株式會社近日宣佈在日本推出其OpreX品牌無線解決方案Sushi Sensor。該感測器是一種整合感測和通訊功能的緊湊型無線設備,用於監測工廠設備的振動和表面溫度。

無線感測器產業概況

無線壓力感測器市場競爭非常激烈。高昂的研發成本、夥伴關係、聯盟和收購是區域公司為在激烈的競爭中保持競爭力而採取的主要成長策略。市場的主要企業包括Honeywell國際、Schneider Electric、艾默生電氣、德克薩斯、西門子、ABB、羅克韋爾自動化和 Pasco Scientific。

- 2022 年 10 月 - 西門子與 Volta Trucks 合作,加速商用車電氣化進程。壓力是電動車液體冷卻系統的關鍵參數。壓力感測器對於提供反饋以調整和最佳化冷卻系統以及檢測可能表明洩漏的壓力損失至關重要。

- 2022 年 6 月 - 無線壓力感測器也用於壓裂、酸洗和固井應用中,用於類似的壓力監測和控制目的。無線壓力感測器能夠測量管道中氣體或液體的表壓。 ABB 與城市燃氣發行公司 Think Gas 合作,實現其燃氣網路的自動化運作。無線壓力感測器支援直接安裝到管道上,有助於在生產車間輕鬆安裝,並且濕潤材料具有很強的耐腐蝕性。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- COVID-19對無線感測器市場的影響

第5章市場動態

- 市場促進因素

- 無線技術的採用率不斷提高,尤其是在惡劣環境中

- 智慧工廠概念(工業自動化)的出現

- 市場挑戰

- 感測器產品具有較高的安全需求和成本

- 物聯網領域的網路安全問題與最新趨勢

第6章市場區隔

- 按類型

- 壓力感測器

- 溫度感測器

- 化學和氣體感測器

- 位置和接近感測器

- 其他感測器

- 按最終用戶產業

- 車

- 衛生保健

- 航太與國防

- 能源與電力

- 食品和飲料

- 其他最終用戶產業

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

第7章競爭格局

- 公司簡介

- Honeywell International Inc.

- Schneider Electric SE

- Emerson Electric Co.

- Texas Instruments Incorporated

- Siemens AG

- ABB Ltd.

- Rockwell Automation, Inc.

- Pasco Scientific

- Monnit Corporation

- Phoenix Sensors LLC

第8章投資分析

第9章:市場的未來

The Wireless Sensors Market size is estimated at USD 14.82 billion in 2025, and is expected to reach USD 48.19 billion by 2030, at a CAGR of 26.59% during the forecast period (2025-2030).

Wireless sensors offer several advantages, such as accuracy and reliability, with the help of various innovative technologies, such as RFID and Bluetooth, and the potential to make electronic devices easy to integrate. As a result, they gained significant traction in the past few years. These sensors are primarily used in factory settings for data monitoring production flow. These also find applications in Automotive, defense, building automation, and other industries, like materials handling and food and beverage. Due to the increasing quest for new energy sources, government regulations, renewable energy development, and rapid technological advancements, the wireless sensors market is propelling.

Key Highlights

- Wireless sensors are considered a vital component in smart grids for remote monitoring of power lines and transformers. They are present in service to monitor line temperature and weather conditions. Industrial automation and demand for miniaturized consumer devices across regions, such as wearables and IoT - connected devices, are among the significant factors driving the wireless sensors market.

- Due to the increased government regulation for the increased use of the sensor for safety, the demand for wireless sensors is growing. For instance, the areas with challenging environmental conditions, such as Oil rigs, Boilers, etc., present high pressure, high temperature, etc. Wireless sensors make it easy to control and monitor the facility from a safe distance.

- The industry 4.0 revolution, in which machines are becoming brighter and more intuitive, is increasing the need for wireless sensors' industrial applications. The new devices are designed to be more efficient, safe, and flexible, with the ability to monitor their performance, usage, and failure autonomously. These applications, therefore, spur the demand for highly- sensitive sensors.

- The rising adoption of IoT is another major factor driving the market's growth. This growth in IoT-connected devices is projected to fuel the demand for wireless sensors. Further, transforming the development of smart homes and buildings, smart cities, and intelligent factories demands wireless sensors, owing to the small form factor, high precision, low power consumption, and ability to control ambient parameters.

- These sensors have reduced installation costs and minimal disruption to the workforce and interiors; therefore, installing wireless sensor systems requires no wiring or structural building changes. Many companies are investing in wireless technologies, which are cost-effective, safe as well as convenient.

- For instance, Monnit Corporation recently announced its ALTA Soil Moisture Sensor's availability to meet the AgriTech market's demands. The innovative Soil Moisture Sensor assists farmers, commercial growers, and greenhouse managers in easily connecting their precision irrigation operations to the Internet of Things (IoT). The defense sector is embracing wireless sensor technology, as these sensors can monitor their premises, identify suspicious activity, and track valuable assets.

- However, the demand for high-performance, cost-efficient, and reliable sensors has increased, leading to higher spending in R&D activities by market vendors. These technological advancements in nanotechnology and micro-technology are expected to propel the market growth of wireless sensors over the forecast period.

Wireless Sensors Market Trends

Energy and Power to Hold Significant Market Share

- Energy conservation is increasingly essential to reduce any enterprise's power consumption and associated costs and minimize the environmental impact, including a business's ecological footprint. For improved energy conservation, accurate wireless sensor measurements are required in portable and stationary weather stations, wind energy systems, testing devices for diesel truck emissions, wind engineering concerning new building design aerodynamics, high-altitude weather research balloons, ocean research, water pollution devices, atmospheric studies, and smokestack mercury sampling.

- Zero-power wireless sensors require energy processing low power management circuitry to monitor the transducer output power, store energy, and deliver power to the rest of the wireless sensor. Energy harvesting helps in powering wireless sensor networks in industrial apps. Advancements in low-power and reliable wireless communications and sensor and energy harvesting technologies make this type of communication more practical and efficient than a wired infrastructure.

- With futuristic innovations, like electric cars and self-driving cars, the demand for these wireless pressure sensors is assumed to increase in the automotive sector. Powertrain applications represent more than 50% of the business, followed by safety, with tire pressure management systems (TPMS) being the most significant single automotive application. Driven by carbon dioxide emission reduction and automation, wireless pressure sensors will increasingly be adopted and used in the future.

- Energy harvesting-based autonomous wireless sensor nodes are a convenient and cost-effective solution. Using energy harvesting removes one of the critical factors limiting the proliferation of wireless nodes. The scarcity of power sources has the characteristics necessary to deliver the energy and power to the sensor node for years without battery replacement. Significant economic advantages are realized when zero wireless power sensors are deployed vs. hard-wired solutions. According to BP, primary energy consumption in India recently amounted to some 35.4 exajoules, thus driving the demand for wireless sensors in the energy and power industry.

Asia Pacific to Witness Significant Growth

- The Asia Pacific is one of the largest regions in the electrical and electronics manufacturing market. The region is also a significant vendor of wireless sensor technologies, especially in China and Japan. China is also the world's largest car market and the world's largest production site for cars, including electric cars, with much growth potential. According to the China Association of Automobile Manufacturers (CAAM), recently, approximately 317,000 commercial vehicles were sold in China. Sales in China accounted for about 32.56% of global motor vehicle sales.

- As these industries account for a significant portion of the wireless sensor market, the region offers an opportunity over the forecast period. The growing concept of connected cars and regulations regarding automotive safety is also expected to drive the adoption of wireless sensors in the region.

- In automobiles, hydraulic brakes are a crucial component in passenger safety. The ability to control a vehicle using brakes is down to a complex blend of components, including pressure sensors. According to Auto Punditz, In the financial year 2022, the leading type of electric vehicle sold in India was two-wheelers, reaching around 231 thousand units, thus driving the demand for wireless pressure sensors in the automotive industry.

- Another reason for increasing the adoption of wireless sensors is the region's high activity level in deploying them to enhance its growing IT healthcare market and innovate new healthcare equipment and devices.

- Recently, Yokogawa Electric Corporation announced the release of the Sushi Sensor, an OpreX brand wireless solution, in Japan. The sensor is a compact wireless device with integrated sensing and communication functions that are intended to monitor plant equipment vibration and surface temperature.

Wireless Sensors Industry Overview

The Wireless Pressure Sensors Market is highly competitive. The high expense on research and development, partnerships, collaborations, and acquisitions are the prime growth strategies adopted by the regional companies to sustain the intense competition. Key players in the market are Honeywell International Inc., Schneider Electric SE, Emerson Electric Co., Texas Instruments Incorporated, Siemens AG, ABB Ltd., Rockwell Automation Inc, Pasco Scientific, and many more.

- October 2022 - Siemens partnered with Volta Trucks to accelerate commercial fleet electrification. Pressure is a crucial parameter in an electric vehicle's liquid cooling system. Pressure sensors are vital for feedback for cooling system regulation and optimization and to detect pressure loss that could suggest a leak.

- June 2022 - Wireless pressure sensors are also used during fracturing, acidizing, and cementing applications for similar pressure monitoring and control purposes. The wireless pressure sensor has the function of measuring the gauge pressure of gases and liquids in piping. ABB Partnered with Think Gas, a city gas distribution company, to automate operations across Think Gas' gas network. The wireless pressure sensors help easy installation for a production site to support direct installation into piping, and wetted material is highly resistant to corrosion.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Wireless Sensors Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Wireless Technologies (Especially in Harsh Environments)

- 5.1.2 Emergence of Smart Factory Concepts (Industrial Automation)

- 5.2 Market Challenges

- 5.2.1 Higher Security Needs and Cost associated with the Sensor Products

- 5.2.2 Concerns pertaining to cybersecurity in the IoT space and recent developments

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Pressure Sensors

- 6.1.2 Temperature Sensors

- 6.1.3 Chemical and Gas Sensors

- 6.1.4 Position and Proximity Sensors

- 6.1.5 Other Types of Sensors

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Healthcare

- 6.2.3 Aerospace and Defense

- 6.2.4 Energy and Power

- 6.2.5 Food and Beverage

- 6.2.6 Other End-user Industries

- 6.3 ***By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Honeywell International Inc.

- 7.1.2 Schneider Electric SE

- 7.1.3 Emerson Electric Co.

- 7.1.4 Texas Instruments Incorporated

- 7.1.5 Siemens AG

- 7.1.6 ABB Ltd.

- 7.1.7 Rockwell Automation, Inc.

- 7.1.8 Pasco Scientific

- 7.1.9 Monnit Corporation

- 7.1.10 Phoenix Sensors LLC

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

中東和非洲無線感測器:市場佔有率分析、行業趨勢、統計和成長預測(2025-2030)亞太地區無線感測器:市場佔有率分析、產業趨勢和成長預測(2025-2030)北美無線感測器:市場佔有率分析、行業趨勢、統計和成長預測(2025-2030)拉丁美洲無線感測器:市場佔有率分析、行業趨勢和成長預測(2025-2030)歐洲無線感測器:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)美國無線感測器:市場佔有率分析、產業趨勢、統計、成長預測(2025-2030)

中東和非洲無線感測器:市場佔有率分析、行業趨勢、統計和成長預測(2025-2030)亞太地區無線感測器:市場佔有率分析、產業趨勢和成長預測(2025-2030)北美無線感測器:市場佔有率分析、行業趨勢、統計和成長預測(2025-2030)拉丁美洲無線感測器:市場佔有率分析、行業趨勢和成長預測(2025-2030)歐洲無線感測器:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)美國無線感測器:市場佔有率分析、產業趨勢、統計、成長預測(2025-2030) 無線感測器市場規模、佔有率、成長分析,按類型、按應用、按最終用戶、按地區 - 行業預測,2025-2032 年

無線感測器市場規模、佔有率、成長分析,按類型、按應用、按最終用戶、按地區 - 行業預測,2025-2032 年 無線感測器市場:按類型、最終用戶分類 - 2025-2030 年全球預測2024-2032 年按產品類型、技術、最終用途和地區分類的無線感測器市場報告

無線感測器市場:按類型、最終用戶分類 - 2025-2030 年全球預測2024-2032 年按產品類型、技術、最終用途和地區分類的無線感測器市場報告 無線感測器全球市場 2024-2028

無線感測器全球市場 2024-2028