|

市場調查報告書

商品編碼

1686301

包裝自動化:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Packaging Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

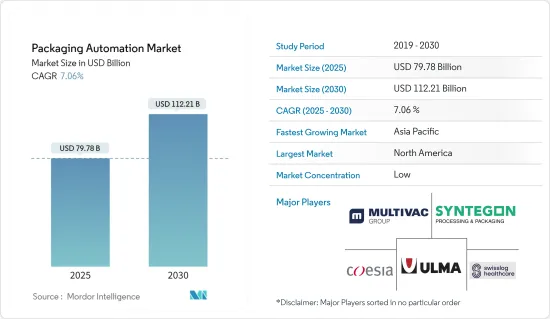

2025 年包裝自動化市場規模預計為 797.8 億美元,預計到 2030 年將達到 1,122.1 億美元,預測期內(2025-2030 年)的複合年成長率為 7.06%。

主要亮點

- 自動化提高了二次包裝的效率和生產力。自動化系統擅長完成紙箱組裝、裝箱、堆疊和貼標籤等任務,其速度和準確性超越了手工勞動。這意味著產量增加、勞動力需求減少,使公司能夠將人力資源重新分配到更具策略性的任務上。

- 越來越多的公司正在客製化包裝解決方案以滿足客戶需求。例如,2023 年 5 月,專門從事醫療/製藥和食品領域的 ULMA Packaging 推出了一條緊湊型全自動包裝線。這條生產線負責處理從產品裝載到最終碼垛的整個包裝過程,滿足公司尋求自動化和簡化包裝業務。這項技術創新有助於企業最佳化工廠佔地面積並提高整體業務效率。

- 隨著自動化在包裝領域變得越來越普遍,公司正在獲得許多好處,包括降低營運成本、提高準確性和增強擴充性。為了進一步鼓勵這一趨勢,包裝器材製造商正在推出促銷計劃,促進終端用戶產業採用這些先進技術。

- 自動化,尤其是與機器人技術的結合,對釀酒廠和其他消費包裝商品企業來說已經變得非常寶貴。雖然許多消費品公司已經採用了自動化技術,但釀酒廠仍被敦促加快採用自動化技術。其好處包括提高生產效率和產品品質、增強安全性和衛生水平,以及資料主導的洞察力。這些技術使釀酒廠能夠保持產品品質的一致性並簡化生產流程。

- 雖然包裝自動化的好處顯而易見,但龐大的初始資本支出可能會成為中小型企業的障礙。此外,中國生產成本的上升以及人民幣兌美元的走強也促使投資者尋找其他生產地點。但在這轉變過程中,製造商不應忽視品質和環保實踐。適應尖端自動化技術是一個漸進的過程,通常需要數年時間才能進步。但緩慢的行動可能會扼殺該地區的成長機會。公司必須平衡創新需求與採用的實用性,才能在不斷變化的市場環境中保持競爭力。

包裝自動化市場趨勢

食品終端用戶領域預計將佔據主要市場佔有率

- 食品包裝自動化對於提高業務效率、維持產品品質和滿足消費者需求至關重要。透過實現填充、密封、貼標和堆疊等任務的自動化,食品包裝作業變得更快、更一致。這會提高生產力並減少勞動力需求。自動化系統確保了維護食品完整性和安全性至關重要的精確度和一致性。自動化最大限度地減少了人為錯誤和污染的風險,確保了更高的衛生標準並遵守嚴格的食品安全法規。

- 自動化正在徹底改變許多行業,食品和飲料行業也不例外。從基本的拾取功能到諸如罐頭、袋子或包裝生產等複雜過程,機器人解決方案現在已覆蓋整個包裝範圍。包裝方法的這些變化提高了生產率,提高了成本效率,並改善了糖果等日常用品的包裝品質。先進的機器人和自動化技術使製造商能夠適應各種各樣的物料輸送和格式,從而提供更大的靈活性和適應性來滿足市場需求。感測器和即時監控系統的整合使得自動化包裝線更加高效和可靠。

- 2023 年 5 月,服務於食品、飲料和化妝品行業的瑞士OEM包裝器材製造商 Rotzinger 與工業無線自動化專家 CoreTigo 在 Interpack 上展開合作。 CoreTigo 的 IO-Link 無線技術將整合到 Rotzinger 的先進包裝機中,以提供增強的功能,重點是靈活性、吞吐量和永續性。此次夥伴關係凸顯了工業自動化領域採用無線通訊技術日益成長的趨勢,有助於實現無縫資料交換和遠端監控。這些技術的整合不僅提高了營運效率,而且還支援預測性維護並減少停機時間。

- 隨著食品公司加大研發投入以改善產品並利用自動化來改善衛生狀況、延長保存期限並提高成本效率,包裝自動化的前景將大幅成長。對研發的關注凸顯了該產業對創新和持續改進的承諾。透過投資先進的自動化技術,食品公司可以實現規模經濟,減少廢棄物並在市場上提高競爭力。這些先進技術有望推動整個食品包裝產業採用自動化解決方案,支持其長期成長和永續性。

預計北美將佔據較大的市場佔有率

- 美國是北美領先的包裝市場,安姆科有限公司(Amcor Ltd)和蒙迪公司(Mondi PLC)等行業巨頭在技術創新和研發活動方面投入大量資金。人們越來越關注先進的包裝技術,目的是提高生產力、降低人事費用並提供更客製化的包裝解決方案。值得注意的是,對永續性的日益關注正在鼓勵企業安裝新的機器,以最大限度地減少對環境的影響並支持環保包裝實踐。

- 此外,美國正在利用其強大的包裝器材出口來加強其市場地位。包括博世包裝服務公司在內的公司業務多元化,涉及糖果零食、烘焙、新鮮和冷凍食品以及藥品等多個領域。這種多元化策略不僅將拓寬我們的市場基礎,還將促進各種包裝應用的技術進步和業務效率。

- 智慧輸送技術 (ICT) 系統正在成為傳統機械解決方案的智慧替代方案,克服了吞吐量和物理限制。例如,羅克韋爾自動化的 MagneMove Lite 系統透過實現更快、更靈活的有效載荷移動徹底改變了操作。該系統提高了更高 SKU 操作的效率,能夠更快地響應不斷變化的生產需求並減少停機時間。

- 同時,加拿大的包裝產業擴大轉向緊湊、自動化的解決方案,例如遠端視覺感測器,以適應工業 4.0 的進步。尤其值得注意的是,人工智慧和機器學習技術正在應用於因空間限制而限制大型自動化機械投資的設施。這些創新,例如解析度更高的遠端感測器,可以在沒有人工直接參與的情況下進行更仔細的檢查,從而提高準確性並減少對人工的需求。此外,這些技術有助於即時監控和資料分析,從而做出更明智的決策並最佳化生產流程。

包裝自動化產業概況

包裝自動化市場高度分散,主要參與者包括 Multivac Group、Coesia SpA、ULMA Packaging、Syntegon Technology 和 Swisslog Healthcare。該市場中的公司正在進行策略性投資、建立合作夥伴關係和夥伴關係,以滿足日益成長的水資源管理需求。我們正在擴大我們的產品和解決方案組合,加強我們的分銷網路,並利用先進技術來提高生產效率和產品質量,以獲得永續的競爭優勢。

- 2024 年 5 月,包裝自動化先驅 LeafyPack 與軟包裝解決方案領導者 KindPack 合作,推出了業界首個租賃購買計畫。這項創新舉措將大大提高包裝自動化的可近性,進而改變大麻的經營方式。

- 2023年12月,MULTIVAC集團將在印度開設新的生產設施、展示室、培訓和應用中心,以滿足南亞地區對食品包裝器材日益成長的需求。

- 2023 年 11 月,Alma Packaging 將成為蘇格蘭充滿活力和多樣化的包裝行業的領導者。我們提供市場上最廣泛的機器和應用,包括流動包裝 (HFFS)、熱成型 (TF)、托盤密封 (TS)、垂直 (VFFS)、拉伸膜和 Alma 包裝自動化 (UPA)。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 產業影響評估

第5章 市場動態

- 市場促進因素

- 提高二次包裝的自動化程度

- 各行各業擴大採用自動化解決方案

- 市場挑戰/限制

- 高資本成本和網路安全問題

第6章 市場細分

- 依產品類型

- 填充

- 標籤

- 箱裝包裝

- 袋裝

- 碼垛

- 封蓋

- 包裝

- 其他產品類型

- 按最終用戶

- 食物

- 飲料

- 藥品

- 個人護理及盥洗用品

- 工業/化工

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 其他亞太地區

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他拉丁美洲國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 埃及

- 其他中東和非洲地區

- 北美洲

第7章 競爭格局

- 公司簡介

- Multivac Group

- Coesia Spa

- ULMA Packaging

- Syntegon Technology

- Swisslog Healthcare

- Rockwell Automation Inc.

- Sealed Air Corporation

- Mitsubishi Electric Corporation

- Automated Packaging System LLC(Sealed Air Corporation)

第8章投資分析

第9章:市場的未來

The Packaging Automation Market size is estimated at USD 79.78 billion in 2025, and is expected to reach USD 112.21 billion by 2030, at a CAGR of 7.06% during the forecast period (2025-2030).

Key Highlights

- Automation enhances efficiency and productivity in secondary packaging. Automated systems excel at tasks like carton erecting, case packing, palletizing, and labeling, outperforming manual processes in speed and accuracy. This translates to increased throughput and reduced labor demands, allowing companies to reallocate human resources to more strategic tasks.

- Companies are increasingly tailoring packaging solutions to meet customer demands. For instance, in May 2023, ULMA Packaging, specializing in medical/pharmaceutical and food sectors, unveiled compact, fully automated packaging lines. These lines handle the entire packaging process, from product loading to final palletizing, catering to businesses seeking to automate or streamline their packaging operations. This innovation helps companies optimize factory footprints and improve overall operational efficiency.

- As automation gains traction in packaging, businesses are reaping its benefits, including reduced operational costs, improved accuracy, and enhanced scalability. Packaging machinery manufacturers are rolling out promotional schemes to further this trend, making it easier for end-user industries to adopt these advanced technologies.

- Automation, especially when coupled with robotics, is proving invaluable for wineries and other consumer-packaged goods businesses. While many CPG companies have already integrated automation, wineries are urged to hasten their adoption. The benefits are vast, spanning from heightened production efficiency and product quality to enhanced safety, hygiene, and data-driven insights. These technologies enable wineries to maintain consistency in product quality and streamline their production processes.

- While the advantages of packaging automation are clear, the substantial initial capital outlay can deter smaller firms. Moreover, with production costs rising in China and the Yuan strengthening against the Dollar, investors are eyeing alternative manufacturing hubs. Yet, amidst these shifts, manufacturers must not lose sight of quality and eco-friendly practices. Adapting to cutting-edge automation technologies is a gradual process, often taking years to refine. However, a sluggish approach risks stunting regional growth opportunities. Companies must balance the need for innovation with the practicalities of implementation to stay competitive in the evolving market landscape.

Packaging Automation Market Trends

Food End-User Segment Expected to Hold Significant Market Share

- Automation in food packaging is pivotal for enhancing operational efficiency, maintaining product quality, and meeting consumer demands. By automating tasks such as filling, sealing, labeling, and palletizing, food packaging operations become faster and more consistent. This, in turn, increases production rates and reduces labor requirements. Automated systems ensure precision and uniformity, which are critical for maintaining the integrity and safety of food products. Automation minimizes human error and contamination risks, thereby ensuring higher standards of hygiene and compliance with stringent food safety regulations.

- Automation has revolutionized various industries, and the food and beverage sector is no exception. From basic pick-and-drop functions to complex processes like can, pouch, or packet manufacturing, robotics solutions now cover the entire packaging spectrum. This transformation in packaging methodologies has led to increased productivity, cost efficiencies, and improved quality, even in the packaging of everyday items like candies. Advanced robotics and automation technologies enable manufacturers to handle a wide range of packaging materials and formats, offering greater flexibility and adaptability to market demands. The integration of sensors and real-time monitoring systems further enhances the efficiency and reliability of automated packaging lines.

- In May 2023, Rotzinger, a Swiss OEM packaging machinery manufacturer serving the food, beverage, and cosmetic sectors, partnered with CoreTigo, a specialist in industrial wireless automation, at Interpack. By integrating CoreTigo's IO-Link wireless technology into Rotzinger's advanced packaging equipment, the collaboration aims to introduce enhanced capabilities, emphasizing flexibility, throughput, and sustainability. This partnership highlights the growing trend of adopting wireless communication technologies in industrial automation, which facilitates seamless data exchange and remote monitoring. The integration of such technologies not only improves operational efficiency but also supports predictive maintenance and reduces downtime.

- As food companies increase their R&D investments to refine their offerings and leverage automation for improved hygiene, extended shelf life, and cost efficiencies, the outlook for packaging automation appears promising for substantial growth. The focus on R&D underscores the industry's commitment to innovation and continuous improvement. By investing in advanced automation technologies, food companies can achieve economies of scale, reduce waste, and enhance their competitive edge in the market. These advancements are expected to drive the adoption of automation solutions across the food packaging industry, supporting long-term growth and sustainability.

North America Expected to Hold Significant Market Share

- The United States stands out as a leading packaging market in North America, with industry giants like Amcor Ltd and Mondi PLC spearheading significant investments in innovation and R&D activities. This heightened focus on advanced packaging technologies aims to enhance productivity, cut labor expenses, and offer more tailored packaging solutions. Notably, a growing emphasis on sustainability is prompting firms to adopt new machinery that minimizes environmental impact and supports eco-friendly packaging practices.

- Moreover, the United States leverages its robust packaging machinery exports, bolstering its market position. Companies, including Bosch Packaging Services, are diversifying into various sectors such as confectionery, bakery, fresh and frozen foods, and pharmaceuticals. This diversification strategy not only broadens their market reach but also drives technological advancements and operational efficiencies across different packaging applications.

- Intelligent Conveyor Technology (ICT) systems are emerging as a smart alternative to traditional mechanics, overcoming their throughput and physical limitations. Rockwell Automation's MagneMove Lite system, for instance, is revolutionizing operations by enabling faster and more flexible payload movement. This system enhances higher-SKU operations' efficiency, allowing for quicker adaptation to changing production demands and reducing downtime.

- Meanwhile, Canada's packaging sector is increasingly turning to compact, automated solutions like remote vision sensors, aligning with the advancements of Industry 4.0. Notably, AI and ML technologies are finding applications in facilities where space constraints limit investments in larger automation machinery. These innovations, such as remote sensors with enhanced resolution, allow for precise inspections without direct human involvement, improving accuracy and reducing the need for manual labor. In addition, these technologies facilitate real-time monitoring and data analysis, leading to more informed decision-making and optimized production processes.

Packaging Automation Industry Overview

The packaging automation market is highly fragmented, with major players like Multivac Group, Coesia SpA, ULMA Packaging, Syntegon Technology, and Swisslog Healthcare. Companies in the market are strategically investing, forming partnerships, and collaborating to address the increasing demand for water management. They are expanding product or solutions portfolios, enhancing distribution networks, and leveraging advanced technologies to improve production efficiency and product quality to gain sustainable competitive advantage.

- May 2024: LeafyPack, a pioneer in packaging automation, collaborated with KindPack, a leader in flexible packaging solutions, to launch the industry's first Lease-to-Own Program. This innovative initiative is set to transform cannabis operations by significantly enhancing the accessibility of packaging automation.

- December 2023: MULTIVAC Group opened a new site in India with a production facility, showroom, and training and application center to address the growing demand for food packaging machines in the South Asian region.

- November 2023: ULMA Packaging established itself as one of the leaders in the dynamic and diverse Scottish packaging industry, offering sustainable and competitive packaging machinery solutions that meet its customers' needs. The ULMA's unique proposition includes the widest range of machines and applications available on the market, comprising Flow Pack (HFFS), Thermoforming (TF), Traysealing (TS), Vertical (VFFS), Stretch Film packaging technologies, and ULMA Packaging Automation (UPA).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Number of Automation for Secondary Packaging

- 5.1.2 Increasing Adoption of Automation Solutions Across Various Industries

- 5.2 Market Challenges/Restraints

- 5.2.1 High Capital Cost and Cybersecurity Concerns

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Filling

- 6.1.2 Labelling

- 6.1.3 Case Packaging

- 6.1.4 Bagging

- 6.1.5 Palletizing

- 6.1.6 Capping

- 6.1.7 Wrapping

- 6.1.8 Other Product Types

- 6.2 By End-user

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Pharmaceuticals

- 6.2.4 Personal Care and Toiletries

- 6.2.5 Industrial and Chemicals

- 6.2.6 Other End-users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Spain

- 6.3.2.6 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 Australia

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Argentina

- 6.3.4.3 Mexico

- 6.3.4.4 Rest of Latin America

- 6.3.5 Middle East and Africa

- 6.3.5.1 Saudi Arabia

- 6.3.5.2 South Africa

- 6.3.5.3 Egypt

- 6.3.5.4 Rest of Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Multivac Group

- 7.1.2 Coesia Spa

- 7.1.3 ULMA Packaging

- 7.1.4 Syntegon Technology

- 7.1.5 Swisslog Healthcare

- 7.1.6 Rockwell Automation Inc.

- 7.1.7 Sealed Air Corporation

- 7.1.8 Mitsubishi Electric Corporation

- 7.1.9 Automated Packaging System LLC (Sealed Air Corporation)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

全球包裝自動化市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年

全球包裝自動化市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年 全球包裝自動化解決方案市場規模、佔有率、趨勢分析報告:按應用、產品類型、最終用戶和地區分類的展望和預測(2024-2031 年)

全球包裝自動化解決方案市場規模、佔有率、趨勢分析報告:按應用、產品類型、最終用戶和地區分類的展望和預測(2024-2031 年) 包裝自動化市場規模、佔有率和成長分析(按組件、產品類型、包裝技術、包裝材料、最終用途和地區)- 產業預測 2025-2032

包裝自動化市場規模、佔有率和成長分析(按組件、產品類型、包裝技術、包裝材料、最終用途和地區)- 產業預測 2025-2032 中東和非洲的包裝自動化:市場佔有率分析、行業趨勢和成長預測(2025-2030)亞太地區包裝自動化:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美包裝自動化:市場佔有率分析、行業趨勢和成長預測(2025-2030)拉丁美洲包裝自動化:市場佔有率分析、行業趨勢和成長預測(2025-2030)歐洲包裝自動化:市場佔有率分析、行業趨勢和成長預測(2025-2030)

中東和非洲的包裝自動化:市場佔有率分析、行業趨勢和成長預測(2025-2030)亞太地區包裝自動化:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美包裝自動化:市場佔有率分析、行業趨勢和成長預測(2025-2030)拉丁美洲包裝自動化:市場佔有率分析、行業趨勢和成長預測(2025-2030)歐洲包裝自動化:市場佔有率分析、行業趨勢和成長預測(2025-2030) 包裝自動化市場:按解決方案、最終用戶分類 - 2025-2030 年全球預測包裝自動化解決方案市場:按組件、按產品類型、按功能、按最終用途 - 2025-2030 年全球預測

包裝自動化市場:按解決方案、最終用戶分類 - 2025-2030 年全球預測包裝自動化解決方案市場:按組件、按產品類型、按功能、按最終用途 - 2025-2030 年全球預測