|

市場調查報告書

商品編碼

1686658

水電-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Hydropower - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

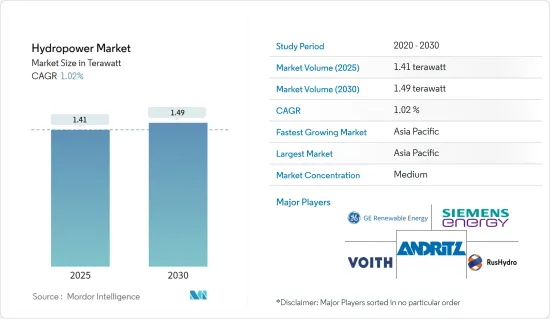

預計 2025 年水電市場規模為 1.41兆瓦,預計到 2030 年將達到 1.49兆瓦,預測期內(2025-2030 年)的複合年成長率為 1.02%。

主要亮點

- 從中期來看,預計預測期內,政府支持下的新水力發電發電工程增加以及對可靠電力的需求不斷成長等因素將推動市場發展。

- 另一方面,發電工程對環境的不利影響可能會在預測期內阻礙市場成長。

- 然而,旨在增加水力發電的新技術趨勢預計將在未來幾年為水力發電市場創造重大機會。

- 由於亞太地區各國對發電工程的投資不斷增加,預計該地區將佔據市場主導地位。

水力發電市場趨勢

大型水力發電(100MW以上)領域佔據市場主導地位

- 大型水力發電是一種利用流水獲取的可再生能源發電形式,用於驅動大型水輪機。為城市生產大量水力發電需要湖泊、水庫和水壩來儲存和調節水量,以便日後用於發電、灌溉、家庭或工業用途。由於大型水力發電設施可以輕鬆開啟和關閉,因此水力發電比大多數其他能源來源更可靠,可以滿足全天的尖峰時段電力需求。

- 傳統水力發電廠、抽水蓄能電站和徑流式水力發電廠是世界各地大型水力發電廠的不同類型。

- 根據國際可再生能源機構的數據,2022年全球水力發電投資約為75.5億美元,而2021年約為78.3億美元。對新水力發電裝置容量的持續投資正在推動全球大型水力發電領域的成長。此外,大型水力發電的平均安裝成本相對較低。

- 中國、巴西、美國、加拿大、印度、日本是世界上開發大型水力發電發電工程的主要國家。預計在預測期內,向更清潔能源來源的轉變以及增加世界主要已開發經濟體和新興經濟體可再生能源在總發電量中的比重的計劃等因素將推動大型水力發電行業的發展。

- 除了主要水力發電生產國外,東南亞地區較小的國家也迅速進行大規模水力發電開發。湄公河經濟對能源的需求不斷成長,引起了流域國家對水力發電開發的濃厚興趣。近幾十年來,全部區域發電工程的投資巨大。

- 例如,寮國政府宣布計畫完成12個水力發電廠計劃,總裝置容量為195萬千瓦。寮國政府計劃在2030年向鄰國出口約20,000兆瓦電力,水電開發是該計畫的核心重點。

- 2022 年 5 月,Drax Group PLC 向克魯坎發電廠投資 6.16 億美元。該公司計劃為其克魯坎發電廠增加 600MW 地下抽水蓄能容量。該公司計劃在 2030 年將克魯坎發電站的容量加倍,現場工程將於 2024 年開始。該公司計劃挖空本克魯坎洞穴並挖掘約 200 萬噸岩石,以容納發電站和相關基礎設施。

- 因此,由於上述因素,預計大型水力發電(100兆瓦以上)部分將在預測期內主導全球水力發電市場。

亞太地區佔市場主導地位

- 近年來,亞太地區一直佔據水力發電市場的主導地位,預計在預測期內將繼續佔據主導地位。根據國際可再生能源機構的數據,截至 2022 年,中國是全球水力發電市場的領導者,裝置容量為 413.5 吉瓦。

- 中國已宣布計畫在2060年實現碳中和,到2025年煤炭消費達到高峰。這將帶動可再生能源領域的投資增加,到2022年將新增水力發電裝置容量約2,250萬千瓦。

- 2023年5月,中國國家發展與改革委員會宣布,將核准在西藏自治區建造一座新的水力發電廠,資金支持約84.3億美元。年平均發電量超過112.8億度。

- 此外,2023年2月,印度核准投資39億美元,用於國家水電公司(NHPC)在阿魯納恰爾邦的迪邦水力發電發電工程(2,880兆瓦(MW)),預計計劃工期為9年。

- 因此,由於上述因素,預計亞太地區將在預測期內主導全球水力發電市場。

水力發電產業概況

水電市場正在變得半固體。主要公司包括通用電氣再生能源公司、西門子能源股份公司、安德里茨股份公司、福伊特有限公司和 PJSC RusHydro。

2022年3月,安德里茨與泰國電力局(EGAT)簽署合作備忘錄,共同探索並拓展泰國及鄰近東南亞國家發電工程的商機。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究範圍

- 市場定義

- 調查前提

第2章執行摘要

第3章調查方法

第4章 市場概述

- 介紹

- 裝置容量及2029年預測

- 近期趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 可靠電力的需求不斷增加

- 政府加強對水力發電的支持

- 限制因素

- 發電工程對環境的不利影響

- 驅動程式

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場區隔

- 規模

- 大型水力發電(100MW以上)

- 小型水力(小於10MW)

- 其他規模(10-100MW)

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 法國

- 英國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 北美洲

第6章競爭格局

- 併購、合資、合作與協議

- 主要企業策略

- 公司簡介

- GE Renewable Energy

- Siemens Energy AG

- Andritz AG

- Voith GmbH & Co. KGaA

- China Yangtze Power Co. Ltd

- PJSC RusHydro

- Electricite de France SA(EDF)

- Iberdrola SA

- Market Ranking/Share Analysis

第7章 市場機會與未來趨勢

- 旨在提高水力發電量的新技術趨勢

The Hydropower Market size is estimated at 1.41 terawatt in 2025, and is expected to reach 1.49 terawatt by 2030, at a CAGR of 1.02% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, gactors such as the increasing number of new hydropower projects backed by government support and the rising demand for reliable electricity are expected to drive the market during the forecast period.

- On the other hand, negative environmental consequences of hydropower projects are likely to hinder the market growth during the forecast period.

- Nevertheless, emerging technological trends aimed at increasing hydropower generation are expected to provide significant opportunities for the hydropower market in the coming years.

- Asia-Pacifc is estimated to dominate the market due to increasing investment in hydropower projects across the various countries in the region.

Hydropower Market Trends

The Large Hydropower (Greater Than 100 MW) Segment to Dominate the Market

- Large-scale hydropower is a form of renewable energy generation derived from flowing water, which is used to drive large water turbines. In order to generate large amounts of hydroelectricity for cities, lakes, reservoirs, and dams are needed to store and regulate water for later release for power generation, irrigation, and domestic or industrial use. Since large-scale hydropower facilities can easily be turned on and off, hydropower has become more reliable than most other energy sources for meeting peak electricity demands throughout the day.

- Conventional hydroelectric dams, pumped storage, and run-of-the-river are the different types of large-scale hydropower plants worldwide.

- As per International Renewable Energy Agency, around USD 7.55 billion was invested in hydropower globally in 2022, whereas around USD 7.83 billion was invested in 2021. The constant investment in new hydropower capacity globally drives growth in large hydropower segments. Also, the average cost of large hydropower installation is comparatively low.

- China, Brazil, the United States, Canada, India, and Japan are the major countries in the deployment of large-scale hydropower projects across the world. Factors such as a shift towards cleaner energy sources and plans to increase the share of renewable energy in the total power generation mix across all the major developed and emerging economies across the world are expected to drive the large hydropower segment during the forecast period.

- In addition to the major hydropower countries, smaller countries from the Southeast Asia region are also moving forward rapidly in the large hydropower development. Increasing demand for energy to boost the Mekong economy has attracted riparian countries' keen interest in hydropower development. Over the last few decades, this has been evidenced by extensive investment in hydropower projects across the region.

- For instance, the Lao government announced that it plans to complete 12 hydropower dam projects with a total capacity of 1,950 MW. Hydropower development is a central priority of the Lao government's plan to export around 20,000 MW of electricity to its neighboring countries by 2030.

- In May 2022, Drax Group PLC invested USD 616 million in the Cruachan power station. The company planned to add 600 MW of underground pumped storage hydropower capacity to the Cruachan power station. The company plans to double the Cruachan facility's capacity by 2030, and work on-site begins in 2024. The company plans to hollow out a cavern in Ben Cruachan and excavate around two million tons of rock to house the power station and related infrastructure.

- Therefore, based on the factors mentioned above, the large hydropower (greater than 100 MW) segment is expected to dominate the global hydropower market during the forecast period.

Asia-Pacific to Dominate the Market

- The Asian-Pacific region has dominated the hydropower market in recent years, and it is likely to maintain its dominance during the forecast period. According to International Renewable Energy Agency, as of 2022, China is the global leader in the hydropower market, with an installed capacity of 413.5 GW.

- China announced its plan to become carbon neutral by 2060 and peak coal consumption by 2025. This led to increased investment in the renewable sector, and in 2022, around 22.5 GW of new hydropower was installed.

- In May 2023, the National Development and Reform Commission (NDRC) of China announced to approval construction of a new hydropower plant in the Xizang Autonomous region which will have capital backing of around USD 8.43 billion. The annual average electricity volume produced by the plant will surpass 11.28 billion kilowatt-hours.

- Further, in February 2023, India approved a USD 3.9 billion investment for the 2,880 megawatts (MW) Dibang hydropower project in Arunachal Pradesh, National Hydroelectric Power Corporation (NHPC), and it is estimated that this project will take nine years to build.

- Therefore, based on the factors mentioned above, Asia-Pacific is expected to dominate the global hydropower market during the forecast period.

Hydropower Industry Overview

The hydropower market is semi-consolidated. Some of the major players include (not in particular order) GE Renewable Energy, Siemens Energy AG, Andritz AG, Voith GmbH & Co. KGaA, and PJSC RusHydro, among others.

In March 2022, ANDRITZ and the Electricity Generating Authority of Thailand (EGAT) signed a Memorandum of Understanding (MoU) to jointly explore and expand business opportunities for hydropower projects in Thailand and surrounding Southeast Asian countries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Installed Capacity and Forecast in GW, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Demand for Reliable Electricity

- 4.5.1.2 Increasing Government Support for Hydropower Gneeration

- 4.5.2 Restraints

- 4.5.2.1 Negative Environmental Consequences of Hydropower Projects

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Size

- 5.1.1 Large Hydropower (Greater Than 100 MW)

- 5.1.2 Small Hydropower (Smaller Than 10 MW)

- 5.1.3 Other Sizes (10-100 MW)

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 United Kingdom

- 5.2.2.4 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 GE Renewable Energy

- 6.3.2 Siemens Energy AG

- 6.3.3 Andritz AG

- 6.3.4 Voith GmbH & Co. KGaA

- 6.3.5 China Yangtze Power Co. Ltd

- 6.3.6 PJSC RusHydro

- 6.3.7 Electricite de France SA (EDF)

- 6.3.8 Iberdrola SA

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Technological Trends Aimed at Increasing Hydropower Generation

水力發電市場報告,按規模(大型水力發電(大於 100 兆瓦)、小型水力發電(小於 10 兆瓦)及其他)、應用(工業、住宅、商業)和地區分類,2025 年至 2033 年

水力發電市場報告,按規模(大型水力發電(大於 100 兆瓦)、小型水力發電(小於 10 兆瓦)及其他)、應用(工業、住宅、商業)和地區分類,2025 年至 2033 年 東南亞水電市場 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

東南亞水電市場 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 2025年全球水力發電市場報告2025年全球水力發電市場報告

2025年全球水力發電市場報告2025年全球水力發電市場報告 水電市場:按類型、應用和地區分類歐洲水電 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)美國水力發電:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

水電市場:按類型、應用和地區分類歐洲水電 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)美國水力發電:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 水電市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測2024-2032 年日本水力發電市場報告(按規模(大型水力發電(大於 100 兆瓦)、小型水力發電(小於 10 兆瓦)等)、應用(工業、住宅、商業)和地區)到 2030 年智慧微水力發電系統市場預測:按技術、安裝類型、容量、組件、應用、最終用戶和地區進行的全球分析

水電市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測2024-2032 年日本水力發電市場報告(按規模(大型水力發電(大於 100 兆瓦)、小型水力發電(小於 10 兆瓦)等)、應用(工業、住宅、商業)和地區)到 2030 年智慧微水力發電系統市場預測:按技術、安裝類型、容量、組件、應用、最終用戶和地區進行的全球分析