|

市場調查報告書

商品編碼

1687117

英國熱電聯產 (CHP):市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)UK Combined Heat And Power (CHP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

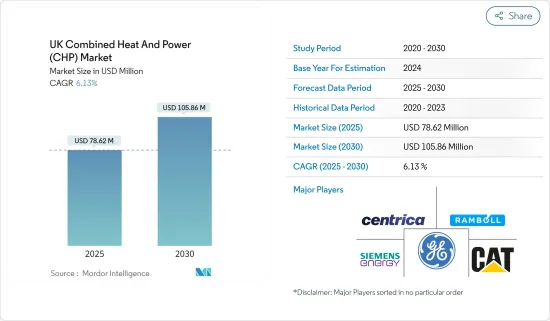

英國熱電聯產 (CHP) 市場規模預計在 2025 年為 7,862 萬美元,預計到 2030 年將達到 1.0586 億美元,預測期內(2025-2030 年)的複合年成長率為 6.13%。

2020 年,市場受到了新冠疫情的負面影響。目前市場已恢復至疫情前的水準。

主要亮點

- 從中期來看,對節能發電技術的日益重視以及對熱電發電工程的投資增加也有望推動所研究市場的成長。

- 另一方面,地緣政治緊張局勢和天然氣價格上漲預計將對英國熱電聯產市場構成挑戰,這可能會對市場成長產生不利影響,並成為市場的主要限制因素之一。

- 然而,分散式發電和空間加熱的需求不斷增加,加上技術進步,預計將推動市場參與者的發展並創造巨大的商機。

英國熱電聯產 (CHP) 市場趨勢

商業和運輸部門預計將佔據市場的大部分佔有率

- 在商業終端用戶領域,熱電聯產 (CHP) 系統通常安裝在飯店、超級市場、辦公大樓、體育中心、醫院、資料中心、購物中心等,以提供能源獨立性和安全性。由於這些系統相對較大且噪音污染不是問題,因此商務用系統主要是電氣高效的內燃機熱電聯產系統。然而,隨著成本下降和燃料電池技術效率的提高,基於燃料電池的熱電聯產系統也被商務用終端用戶所採用。

- 隨著汽車製造商加緊開發此類動力傳動系統,氫基燃料電池(CHP)技術是汽車產業的一個領域,正變得越來越重要。與電動車一樣,燃料電池電動車 (FCEV) 也以氫氣為動力,被歸類為超低排放氣體車 (ULEV),因為其排氣中排放的唯一物質是水蒸氣。

- 由於商業建築、辦公室、飯店、醫院等領域的開發和應用日益增多,預計預測期內英國商業終端用戶領域將顯著採用 CHP 系統。

- 超級市場是商用熱電聯產系統的主要終端用戶之一,超級市場總能耗的大部分來自冷凍、照明和暖通空調系統,其中冷卻佔總能耗的近三分之一。零售業的能源需求在非運作時段明顯較低,且受季節性波動的影響,因此商務用熱電聯產系統需要適當規模才能滿足需求高峰。在超級市場中,熱電聯產系統(通常基於 ICE)直接安裝在機車上,可以覆蓋電力負載和熱負荷,或至少覆蓋其中的一部分。

- 近年來,國內建設活動也有所增加。根據國家統計局的數據,2022 年私人商業領域的新建設訂單總額將達到約 179.6 億美元,比 2020 年成長約 35%。在預測期內,這可能會推動該國熱電聯產系統的成長。

- 因此,鑑於上述情況,預計商業和運輸部門將在預測期內佔據英國熱電聯產 (CHP) 市場的大部分佔有率。

天然氣價格上漲預計將抑制市場需求

- 天然氣 是 一種 重要 的能源來源, 它 在燃氣引擎上 的 使用 是 所有石化燃料中 二氧化碳排放最低 的 , 這 符合英國減少 溫室 氣體排放的 目標 .此外,英國商業、能源和工業戰略部表示,使用天然氣作為熱電聯產 (CHP) 裝置的燃料可減少氮氧化物排放,並且硫和硫氧化物排放,並且硫氧化物含量較低。

- 由於亞洲和南美對天然氣的需求突然增加,俄羅斯入侵烏克蘭導致俄羅斯對歐洲市場的天然氣供應減少,天然氣庫存減少,以及各種電氣設備一系列故障,英國消費者面臨天然氣價格大幅上漲。依賴天然氣的消費者、電力公司和使用熱電聯產裝置的企業都會受到影響。

- 天然氣價格上漲的主要原因是全球天然氣批發價格的上漲。國內供應滿足了英國約40%的需求。同時,其餘則從挪威和荷蘭等鄰國進口。此外,卡達、美國和俄羅斯供應了英國約5%的市場佔有率。

- 根據英國能源統計摘要(DUKES),2021 年英國約有 2,016 個熱電聯產站點,與 2020 年相比減少了 236 個熱電聯產 (CHP) 站點。

- 此外,2022年2月俄羅斯入侵烏克蘭,戰爭升級,導致天然氣價格進一步飆升。 2022年3月,英國天然氣現貨價格為511便士/熱量單位,與前一年同期比較去年同期上漲139%。此外,根據英國國家統計局的數據,2022 年英國天然氣平均消費者物價指數為 164.7 指數點。

- 因此,鑑於上述情況,預測期內天然氣價格上漲可能會阻礙英國熱電聯產 (CHP) 市場的發展。

英國熱電聯產 (CHP) 產業概況

英國熱電聯產(CHP)市場正走向半固體。市場上的主要企業(不分先後順序)包括通用電氣公司、西門子能源股份公司、Ramboll 集團、Centrica PLC 和Caterpillar公司等。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究範圍

- 市場定義

- 調查前提

第 2 章執行摘要

第3章調查方法

第4章 市場概況

- 介紹

- 2028 年市場規模與需求預測(美元)

- 最新趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 增加對發電工程的投資

- 政府對熱電聯產電廠開發和營運的支持政策和獎勵

- 限制因素

- 英國天然氣價格上漲

- 驅動程式

- 供應鏈分析

- PESTLE分析

- 2014 年至 2022 年熱電聯產發電廠統計資料(按數量和容量)

- 熱電聯產發電廠的燃料消耗統計(按燃料類型和部門)

第5章 市場區隔

- 最終用戶

- 產業部門

- 貿易及運輸業

- 其他最終用戶(例如農業、區域供熱、休閒)

- 類型

- 燃氣渦輪機

- 蒸氣渦輪

- 其他類型(往復式引擎、有機朗肯迴圈熱電聯產)

第6章 競爭格局

- 併購、合資、合作、協議

- 主要企業策略

- 公司簡介

- Caterpillar Inc.

- Centrica PLC

- General Electric Company

- Mitsubishi Power Ltd

- Siemens Energy AG

- Ramboll Group

- Helec Limited

- Tedom AS

第7章 市場機會與未來趨勢

- 熱電聯產 (CHP) 系統的技術進步

The UK Combined Heat And Power Market size is estimated at USD 78.62 million in 2025, and is expected to reach USD 105.86 million by 2030, at a CAGR of 6.13% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. Presently the market has now reached pre-pandemic levels.

Key Highlights

- Over the medium term, growing emphasis on energy-efficient technology that generates electricity and increasing investments in CHP-based power projects are also expected to drive the growth of the market studied.

- On the other hand, geopolitical tensions and increasing natural gas prices are expected to impose challenges on the combined heat and power market in the United Kingdom and may negatively impact the market's growth and are one of the major restraints for the market.

- Nevertheless, increasing demand for distributed power generation and space heating coupled with technological advancements are expected to drive and create significant amount of opportunities for the market players.

UK Combined Heat and Power (CHP) Market Trends

Commercial and Transportation Segment is Expected to have as Significant Share in the Market

- In the commercial end-user segment, the Combined Heat, and Power (CHP) systems are typically installed at hotels, supermarkets, office buildings, sports centers, hospitals, data centers, and shopping centers, providing energy independence and security. As these systems are relatively larger, and noise is a lesser concern, commercial systems are primarily internal combustion engine CHPs with higher electrical efficiency. However, with falling costs and the rising efficiency of fuel cell technology, fuel cell-based CHP systems are also becoming increasingly adopted by commercial end-users.

- The hydrogen-based fuel cell (CHP) technology is an area of the automotive industry that is becoming increasingly essential as manufacturers commit to developing this type of power train. Like electric cars, hydrogen-powered fuel cell electric vehicles (FCEVs) are classed as ultra-low emission vehicles (ULEVs) since water vapor is the only substance that comes from the exhaust.

- The commercial end-user segment in the United Kingdom is expected to witness a notable adoption of CHP systems due to the developments and the rising applications in commercial buildings, offices, hotels, hospitals, etc., during the forecast period.

- Supermarkets are one of the major end-users of commercial CHP systems, which most of the total energy consumption in supermarkets is from refrigeration, lighting, and HVAC systems, with refrigeration responsible for nearly 1/3rd of the total energy consumption. As the energy requirement in the retail sector is significantly lower during non-operational hours and subject to seasonal variations, commercial CHP systems need to be sized accordingly to match demand spikes. In supermarkets, CHP systems (usually based on ICEs) are installed directly in loco, which could cover both electricity and heat loads, or at least a part of them.

- The construction activity around the country has also been increasing in recent times. According to the Office of National Statistics, the total value of of new orders for construction in the private commercial sector increased to about USD 17,960 million in 2022, an increase of around 35% compared to 2020. These are likely to surge the growth of CHP systems in the country during the forecast period.

- Therefore, owing to the above-mentioned points, commercial and transportation segment is expected to have a significant share in the United Kingdom's combined heat and power (CHP) market during the forecast period.

Increasing Natural Gas Price is Expected to Restrain the Market Demand

- Natural Gas is one of the essential sources of energy, and the utilization of natural gas in gas engines is characterized by the lowest carbon dioxide emissions levels of all fossil fuels, which is in line with the United Kingdom's goal to reduce greenhouse gas emissions. In addition, according to the United Kingdom's Department for Business, Energy, and Industrial Strategy, using natural gas as a fuel for Combined Heat and Power (CHP) units reduce nitrogen oxide emissions and virtually contains no sulfur or contaminants.

- Factors such as circumstances, such as soaring demand for natural gas in Asia and South America, diminished gas supply from Russia to the European markets due to the invasion of Russia on Ukraine, low gas stocks, and a series of breakdowns at various electrical facilities, consumers in the United Kingdom faced a significant increase in gas prices. Consumers, utility companies, and businesses using CHP units dependent on natural gas are impacted.

- The primary cause of the natural gas price rise has been a surge in the wholesale price of natural gas globally. Domestic supply covers approximately 40% of the United Kingdom's needs. At the same time, the rest is imported from neighboring countries, such as Norway and the Netherlands. Further, afield in Qatar and the United States, and Russia supplies around 5% of the United Kingdom market.

- According to Digest of UK Energy Statistics (DUKES), the United Kingdom had around 2,016 CHP sites in 2021, witnessing a decrease of 236 combined heat and power (CHP) areas compared to 2020.

- Moreover, In February 2022, Russia's invasion of Ukraine in a horrific escalation of a war that started in February 2022 further spiked the natural gas prices. In March 2022, the Natural Gas spot prices in the United Kingdom were 511 pence/therm witnessing an increase of 139% as compared to the previous year. Further, according to Office for National Statistics (UK), in 2022, the average consumer price index for gas in the United Kingdom stood at 164.7 index points.

- Thus, owing to the above points, increasing natural gas prices will likely hamper the combined heat and power (CHP) market in the United Kingdom during the forecast period.

UK Combined Heat and Power (CHP) Industry Overview

The UK combined heat and power (CHP) market is semi-consolidated. The key players in the market (in no particular order) include General Electric Company, Seimens Energy AG, Ramboll Group, Centrica PLC, and Caterpillar Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Investments in the CHP-Based Power Projects

- 4.5.1.2 Supportive Government Policies And Incentives To Develop And Operate CHP Plants

- 4.5.2 Restraints

- 4.5.2.1 Increasing Natural Gas Prices in the United Kingdom

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 CHP Power Plant Statistics, 2014-2022 (by Number and Capacity)

- 4.9 CHP Power Plant Fuel Used Statistics (by Fuel Type and Sector)

5 MARKET SEGMENTATION

- 5.1 End User

- 5.1.1 Industrial Sector

- 5.1.2 Commercial and Transportation Sector

- 5.1.3 Other End Users (Agriculture, Community Heating, Leisure, etc.)

- 5.2 Type

- 5.2.1 Gas Turbine

- 5.2.2 Steam Turbine

- 5.2.3 Other Types (Reciprocating Engine and Organic Rankine Cycle CHP)

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Caterpillar Inc.

- 6.3.2 Centrica PLC

- 6.3.3 General Electric Company

- 6.3.4 Mitsubishi Power Ltd

- 6.3.5 Siemens Energy AG

- 6.3.6 Ramboll Group

- 6.3.7 Helec Limited

- 6.3.8 Tedom AS

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in Combined Heat And Power (CHP) Systems

熱電聯產市場規模、佔有率、成長分析,按燃料類型、按技術、按產能、按應用、按地區 - 產業預測,2025 年至 2032 年

熱電聯產市場規模、佔有率、成長分析,按燃料類型、按技術、按產能、按應用、按地區 - 產業預測,2025 年至 2032 年 2025 年熱電聯產 (CHP) 全球市場報告

2025 年熱電聯產 (CHP) 全球市場報告 中東和非洲的熱電聯產 -市場佔有率分析、行業趨勢、統計數據、成長預測(2025-2030)

中東和非洲的熱電聯產 -市場佔有率分析、行業趨勢、統計數據、成長預測(2025-2030) 歐洲熱電聯產 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

歐洲熱電聯產 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 熱電聯產 (CHP) 市場:未來預測(2025-2030 年)

熱電聯產 (CHP) 市場:未來預測(2025-2030 年) 熱電聯產 (CHP) 全球市場預測 (-2030):按燃料類型、成分、技術、應用和地區進行分析

熱電聯產 (CHP) 全球市場預測 (-2030):按燃料類型、成分、技術、應用和地區進行分析 熱電聯產市場:依產品、技術、燃料、範圍、應用、2025-2030 年全球預測

熱電聯產市場:依產品、技術、燃料、範圍、應用、2025-2030 年全球預測 全球熱電聯產市場:按原動機、容量、燃料、最終用戶、地區分類 - 到 2029 年的預測

全球熱電聯產市場:按原動機、容量、燃料、最終用戶、地區分類 - 到 2029 年的預測 熱電聯產市場:依燃料種類、容量、技術、應用、地區

熱電聯產市場:依燃料種類、容量、技術、應用、地區 全球熱電聯供系統 (CHP) 市場 2024-2028

全球熱電聯供系統 (CHP) 市場 2024-2028