|

市場調查報告書

商品編碼

1687151

鋰:市場佔有率分析、產業趨勢和統計數據、成長預測(2025-2030 年)Lithium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

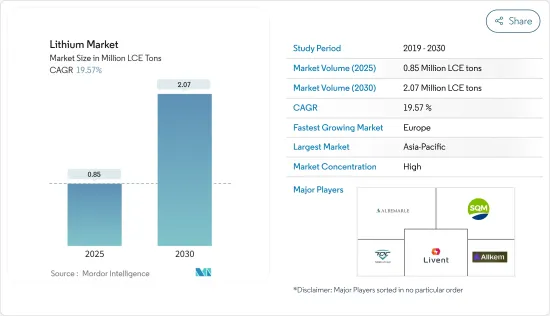

預計 2025 年鋰市場規模為 85 萬噸,2030 年將達到 207 萬噸,預測期間(2025-2030 年)的複合年成長率為 19.57%。

2020 年,汽車市場受到新冠疫情的嚴重打擊,上半年受到封鎖影響,自 2 月以來月度汽車銷量出現前所未有的下降。目前市場已恢復至疫情前的水準。

關鍵亮點

- 短期內,電動車需求加速成長以及可攜式家用電子電器的使用和需求增加是推動市場發展的關鍵因素。

- 然而,對鋰市場供需缺口的日益擔憂可能會阻礙市場成長。

- 在預測期內,智慧電網電力的日益普及可能會為全球鋰市場帶來重大機會。

- 亞太地區在全球市場佔據主導地位,其中消費量最高的國家是中國、韓國和日本。

鋰市場趨勢

電池應用領域佔據市場主導地位

- 鋰主要用於生產鋰電池。電池應用領域佔全球鋰市場的最大佔有率。

- 鋰電池可分為一次性電池和可充電電池兩類。一次性鋰電池使用金屬鋰作為負極。與其他標準電池相比,這些電池的壽命更長、充電密度更高。這些電池用於心臟心律調節器和其他需要長期使用的電子醫療設備等關鍵設備。

- 可充電鋰電池有兩種類型:鋰離子電池和鋰離子聚合物電池。鋰離子電池裝在硬殼中,而鋰聚合物電池裝在軟性聚合物殼中。此外,鋰聚合物電池的比能量比鋰離子電池略高。鋰聚合物電池使用聚合物作為電解質,而不是鋰離子電池中使用的標準液體電解質。

- 在鋰離子電池中,金屬鋰構成正極,鋰與電解接觸時發生的化學反應表徵了電池的特性。然而,鋰單獨用於電池裝置時非常不穩定。因此,鋰和氧的組合(稱為氧化鋰)已作為正極投入實用化。這使得氧化鋰成為比元素鋰更穩定的化合物。

- 鋰離子電池用途廣泛,包括通訊設備和家用電子電器產品。鋰離子電池重量輕、能量密度高、可充電,是攜帶式電子設備的理想選擇。鋰離子和鋰聚合物充電電池由於能量密度高且無“記憶效應”,是行動電話、筆記型電腦和其他攜帶式電子設備最有效的電源。

- 這些電池在電動車 (EV)、行動電話、筆記型電腦、電源備份/UPS、平板電腦、電動工具、視訊遊戲、玩具和電動自行車等產品中需求量很大。除此之外,鋰電池也在能源儲存系統中得到應用,考慮到風能等各種可再生能源領域的成長,使用鋰離子電池的能源儲存系統的需求正在以相當快的速度成長。

- 鋰離子電池之所以受到歡迎,主要是因為與其他類型的電池相比,其容量重量比更佳。推動鋰離子電池普及的其他因素包括效能的提高(壽命更長、維護成本更低)和價格的下降。

- 全球主要鋰離子電池製造商包括LG化學、寧德時代、松下、三星SDI、比亞迪等。

- 由於上述因素,電池應用領域對鋰的需求預計會增加。

亞太地區佔市場主導地位

- 由於中國、韓國和日本等國家的鋰消費量不斷增加,亞太地區已成為鋰消費的主要市場。

- 隨著消費者越來越傾向於電池驅動的汽車,該國的汽車產業正在經歷趨勢的轉變。電動車,包括Scooter、汽車和巴士等輕型商用車,在該國越來越受歡迎。根據中國乘用車市場資訊聯席會(CPCA)預測,2021年中國汽車銷量將超過330萬輛,較2020年成長約169%。

- 中國政府預測未來五年電動車普及率將達20%。因此,汽車電池的生產和消費預計將會增加。中國電池製造商 CATL 控制著全球 30% 以上的電動車電池市場。鈷專業供應商 Darton Commodities 估計,中國煉油廠供應了全球 85% 的電池鈷,有助於提高鋰離子電池的穩定性。

- 根據國家鋰電池藍圖,預計到 2025 年中國鋰電池產量將達到 1,811 吉瓦。中國是全球最大的電動車市場,並主導鋰離子電池製造供應鏈,其中包括礦物和原料加工。

- 韓國最大的產業是電子、汽車、通訊、造船、化工和鋼鐵。韓國是最大的電子產品和半導體製造國之一,擁有三星電子、海力士半導體等全球知名品牌。

- 根據韓國汽車技術研究院(KAII)的資料,2021 年前 9 個月,韓國電動車銷量成長 96%,達到 71,006 輛。

- 隨著消費者對替代燃料技術的需求不斷成長,日本的電動車銷售未來可能會增加。不過,2021年日本內燃機汽車銷量下降了3%以上,至4,448,340輛。日本汽車經銷商協會稱,660cc以上新車銷量下降2.9%至2,795,818輛。根據輕型汽車協會統計,同年輕型汽車銷量下降3.8%至1,652,522輛。

- 預計所有這些因素都將在預測期內推動鋰市場的成長。

鋰行業概況

全球鋰市場呈現整合態勢,前五大公司佔全球產量的80%以上。市場的主要企業包括(不分先後順序)Albemarle Corporation、SQM SA、天齊鋰業、Livent 和 Allkem Limited。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 電動車需求不斷成長

- 可攜式家用電子電器的使用和需求不斷增加

- 其他促進因素

- 限制因素

- 鋰市場供需缺口

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 定價分析

- 技術簡介

第5章市場區隔

- 類型

- 金屬

- 化合物

- 碳酸鹽

- 氯化物

- 氫氧化物

- 合金

- 應用

- 電池

- 潤滑脂

- 空氣處理

- 製藥

- 玻璃/陶瓷(包括玻璃料)

- 聚合物

- 其他

- 最終用戶產業

- 工業的

- 消費性電子產品

- 能源儲存

- 醫療保健

- 車

- 其他

- 地區

- 生產及蘊藏量分析

- 澳洲

- 智利

- 中國

- 阿根廷

- 辛巴威

- 美國

- 其他中東和非洲地區

- 消費分析

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 生產及蘊藏量分析

第6章競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)分析

- 主要企業策略

- 公司簡介(概況、財務狀況、產品與服務、最新發展)

- Albemarle Corporation

- Allkem Limited

- Ganfeng Lithium Co. Ltd

- Lithium Australia NL

- Livent

- Mineral Resources

- Morella Corporation Limited

- Sichuan Yahua Industrial Group Co. Ltd

- SQM SA

- Tianqi Lithium

- Avalon Advanced Materials Inc.

- Pilbara Minerals

第7章 市場機會與未來趨勢

- 擴大智慧電網的使用

- 其他機會

The Lithium Market size is estimated at 0.85 million lce tons in 2025, and is expected to reach 2.07 million lce tons by 2030, at a CAGR of 19.57% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020, as the first half of the year was affected by the lockdowns, causing unprecedented declines in monthly vehicle sales from February. Presently the market has reached pre-pandemic levels.

Key Highlights

- Over the short term, the major factors driving the market studied are the accelerating demand for electric vehicles and increasing usage and demand for portable consumer electronics.

- However, rising concern over the demand-supply gap in the lithium market may hamper the market growth.

- Nevertheless, the growing adoption of smart grid electricity is likely to be a major opportunity in the global lithium market over the forecast period.

- Asia-Pacific dominates the market across the world, with the most substantial consumption from countries like China, South Korea, and Japan.

Lithium Market Trends

The Battery Application Segment to Dominate the Market

- Lithium is majorly used for the production of lithium batteries. The battery application segment accounted for the largest share of the global lithium market.

- Lithium batteries can be categorized into two segments, namely, disposable and rechargeable. Disposable lithium batteries use lithium in the metallic form as an anode. These batteries have a longer life and higher charge density when compared to other standard batteries. These batteries find applications in critical devices, such as pacemakers and other electronic medical devices intended for long-term use.

- Rechargeable lithium batteries are of two types, i.e., lithium-ion batteries and lithium-ion polymer batteries. Li-ion battery is packed in a rigid case, whereas the Li-po battery comes in a flexible polymer casing. Also, a Li-po battery has a slightly higher specific energy when compared to a Li-ion battery. The Li-po battery uses a polymer as an electrolyte instead of the standard liquid electrolyte used in a Li-ion battery.

- In the case of a Li-ion battery, the metal lithium forms the cathode, and it is the chemical reactions of lithium upon contact with the electrolyte that makes these batteries characteristic. However, elemental lithium is highly unstable when used inside a battery's apparatus. Hence, a combination of lithium and oxygen together, called lithium oxide, is used as the cathode for practical purposes. Thereby, lithium oxide is a much more stable compound as opposed to elemental lithium.

- Lithium-ion batteries are employed in several applications, including telecommunication devices and consumer electronics. The light weight of lithium-ion batteries, coupled with their high energy density and rechargeability, makes them a good fit for portable electronics. Due to their energy density and lack of 'memory effect,' lithium-ion and lithium-polymer rechargeable batteries are the most efficient power sources for cell phones, laptops, and other portable electronic devices.

- These batteries are in great demand in products such as electric vehicles (EVs), cell phones, laptops, power backups/UPS, tablets, power tools, video games, toys, and e-bikes. Apart from these, lithium-based batteries find one of their applications in energy storage systems, and the demand for lithium-ion battery-based energy storage systems is growing at a significant pace, considering the growth in various renewable energy sectors, including wind and others.

- Li-ion batteries are gaining more popularity compared to other battery types, majorly due to their favorable capacity-to-weight ratio. The other factors that contribute to its adoption include its better performance (long life and low maintenance) and decreasing price.

- Some of the key global lithium-ion battery manufacturers include LG Chem, Contemporary Amperex Technology Co., Limited (CATL), Panasonic, Samsung SDI, and BYD, among other companies.

- All the above-said factors are expected to increase the demand for lithium in the battery application segment.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific was found to be the major market for the consumption of lithium, owing to increasing consumption from countries such as China, South Korea, and Japan.

- The automobile industry in the country is witnessing switching trends as the consumer inclination toward battery-operated vehicles is on the higher side. Electric vehicles, including scooters, passenger cars, and light commercial vehicles like buses, are gaining popularity in the country. According to the China Passenger Car Association (CPCA), the country sold over 3.3 million units in 2021, indicating an increase of about 169% compared to 2020.

- The government of China estimates a 20% penetration rate of electric vehicle production over the next five years. Hence, this is anticipated to increase the production and consumption of batteries for vehicles. Chinese battery maker CATL controls over 30% of the world's EV battery market. The cobalt specialist supplier, Darton Commodities, estimated that Chinese refineries supplied 85% of the world's battery-ready cobalt, a mineral that helps in improving the stability of lithium-ion batteries.

- According to the National Blueprint for Lithium Batteries, China is projected to have 1,811 GWh of lithium cell production by 2025. China is the largest global EV market and dominates the supply chain for the manufacture of lithium-ion batteries, including the processing of minerals and raw materials.

- South Korea's largest industries are electronics, automobiles, telecommunications, shipbuilding, chemicals, and steel. The country is among the largest manufacturers of electronic goods as well as semiconductors, with globally popular brands, such as Samsung Electronics Co. Ltd and Hynix Semiconductor.

- According to the data collected by the Korea Automotive Technology Institute (KAII), the sales of electric vehicles in the country surged by 96% to 71,006 units in the first nine months of 2021.

- Electric vehicle sales in Japan are likely to ascend in the future with rising consumer demand for alternate fuel technology. However, ICE-based automobile sales in the country dropped by over 3% to 4,448,340 units in 2021. The Japan Automobile Dealers Association reported that sales of new vehicles larger than 660 CC slipped by 2.9% to 2,795,818 units. The Japan Light Motor Vehicle and Motorcycle Association reported that sales of mini-vehicles fell by 3.8% to 1,652,522 units in the same year.

- All these factors are expected to facilitate the growth of the lithium market over the forecast years.

Lithium Industry Overview

The global lithium market is consolidated in nature, with the top five players holding more than 80% share of the global production outputs. Some of the major players in the market include (not in any particular order) Albemarle Corporation, SQM SA, Tianqi Lithium, Livent, and Allkem Limited, among other companies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Accelerating Demand for Electric Vehicles

- 4.1.2 Increasing Usage and Demand by Portable Consumer Electronics

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Demand-supply Gap in the Lithium Market

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Pricing Analysis

- 4.6 Technological Snapshot

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Metal

- 5.1.2 Compound

- 5.1.2.1 Carbonate

- 5.1.2.2 Chloride

- 5.1.2.3 Hydroxide

- 5.1.3 Alloy

- 5.2 Application

- 5.2.1 Battery

- 5.2.2 Grease

- 5.2.3 Air Treatment

- 5.2.4 Pharmaceuticals

- 5.2.5 Glass/Ceramic (Including Frits)

- 5.2.6 Polymer

- 5.2.7 Other Applications

- 5.3 End-user Industry

- 5.3.1 Industrial

- 5.3.2 Consumer Electronics

- 5.3.3 Energy Storage

- 5.3.4 Medical

- 5.3.5 Automotive

- 5.3.6 Other End-user Industries

- 5.4 Geography

- 5.4.1 Production and Reserve Analysis

- 5.4.1.1 Australia

- 5.4.1.2 Chile

- 5.4.1.3 China

- 5.4.1.4 Argentina

- 5.4.1.5 Zimbabwe

- 5.4.1.6 United States

- 5.4.1.7 Other Regions

- 5.4.2 Consumption Analysis

- 5.4.2.1 Asia-Pacific

- 5.4.2.1.1 China

- 5.4.2.1.2 India

- 5.4.2.1.3 Japan

- 5.4.2.1.4 South Korea

- 5.4.2.1.5 Australia & New Zealand

- 5.4.2.1.6 Rest of Asia-Pacific

- 5.4.2.2 North America

- 5.4.2.2.1 United States

- 5.4.2.2.2 Canada

- 5.4.2.2.3 Mexico

- 5.4.2.3 Europe

- 5.4.2.3.1 Germany

- 5.4.2.3.2 United Kingdom

- 5.4.2.3.3 France

- 5.4.2.3.4 Italy

- 5.4.2.3.5 Nordic Countries

- 5.4.2.3.6 Rest of Europe

- 5.4.2.4 South America

- 5.4.2.4.1 Brazil

- 5.4.2.4.2 Argentina

- 5.4.2.4.3 Rest of South America

- 5.4.2.5 Middle East and Africa

- 5.4.2.5.1 Saudi Arabia

- 5.4.2.5.2 South Africa

- 5.4.2.5.3 Rest of Middle East and Africa

- 5.4.1 Production and Reserve Analysis

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles (Overview, Financials, Products and Services, and Recent Developments)

- 6.4.1 Albemarle Corporation

- 6.4.2 Allkem Limited

- 6.4.3 Ganfeng Lithium Co. Ltd

- 6.4.4 Lithium Australia NL

- 6.4.5 Livent

- 6.4.6 Mineral Resources

- 6.4.7 Morella Corporation Limited

- 6.4.8 Sichuan Yahua Industrial Group Co. Ltd

- 6.4.9 SQM SA

- 6.4.10 Tianqi Lithium

- 6.4.11 Avalon Advanced Materials Inc.

- 6.4.12 Pilbara Minerals

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Adoption in Smart Grid Electricity

- 7.2 Other Opportunities

2032 年氯化鋰市場預測:按類型、等級、純度等級、功能、應用、最終用戶和地區進行的全球分析

2032 年氯化鋰市場預測:按類型、等級、純度等級、功能、應用、最終用戶和地區進行的全球分析 氫氧化鋰市場:全球產業分析、規模、佔有率、成長、趨勢及預測(2025-2032)鋰市場按類型、應用和地區分類

氫氧化鋰市場:全球產業分析、規模、佔有率、成長、趨勢及預測(2025-2032)鋰市場按類型、應用和地區分類 全球氫氧化鋰市場:預測(2025-2030)

全球氫氧化鋰市場:預測(2025-2030) 直接提鋰(DLE)的全球市場(2025年~2035年)鋰市場規模、佔有率、成長分析、按類型、按來源、按應用、按最終用戶行業、按地區 - 行業預測,2024-2031 年

直接提鋰(DLE)的全球市場(2025年~2035年)鋰市場規模、佔有率、成長分析、按類型、按來源、按應用、按最終用戶行業、按地區 - 行業預測,2024-2031 年 鋰市場:按類型、應用和最終用戶分類 - 2025-2030 年全球預測2030 年氫氧化鋰市場預測:按類型、應用、最終用戶和地區分類的全球分析

鋰市場:按類型、應用和最終用戶分類 - 2025-2030 年全球預測2030 年氫氧化鋰市場預測:按類型、應用、最終用戶和地區分類的全球分析 碳酸鋰:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)全球氫氧化鋰市場:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)

碳酸鋰:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)全球氫氧化鋰市場:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)