|

市場調查報告書

商品編碼

1687216

中東和非洲的電池:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)Middle East And Africa Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

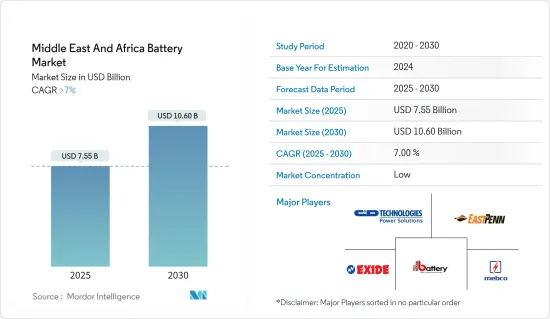

中東和非洲電池市場規模預計在 2025 年為 75.5 億美元,預計到 2030 年將達到 106 億美元,預測期內(2025-2030 年)的複合年成長率將超過 7%。

關鍵亮點

- 推動中東和非洲電池市場發展的關鍵因素包括鋰離子電池價格下降、電動車普及率提高以及可再生能源領域的成長。此外,隨著資料中心正在發展其用於雲端服務的數資料基礎設施,且下一代雲端服務可能會納入區塊鏈網路,預計資料中心的需求將推動市場發展。

- 然而,原料供需不匹配可能會阻礙市場成長。

- 太陽能能源儲存在新興國家越來越受歡迎,可能為電池市場創造重大機會。

- 阿拉伯聯合大公國預計將佔據市場主導地位,受其年輕且多元化的人口推動,他們將購買包括智慧型手機和汽車在內的家用電子電器產品。

中東和非洲的電池市場趨勢

汽車電池大幅成長

- 由於電池(尤其是鋰離子電池)用於電動車,汽車產業預計將成為主要的終端用戶領域之一。電動車的廣泛應用預計將為鋰離子電池行業的成長提供重大動力。

- 混合動力和電氣化正在興起,各種類型的汽車正在全球銷售。車輛有很多類型,包括混合動力電動車、插電式混合動力電動車和電動車。

- 在中東和非洲低度開發國家,需求成長微乎其微。中東大多數國家都依賴原油生產。然而,根據排放法規,預計預測期內對電動車的需求將會增加,這將導致電池消費量的增加。

- 南非是非洲主要汽車市場之一,日產聆風於2014年推出首款電動車型。 2015年,BMW進入南非市場,推出i3和i8車款。

- 2023年6月,BMW宣布將向位於南非比勒陀利亞的Plant Rosslyn工廠投資2.18億美元。該工廠是BMW在德國以外的第一家海外工廠,也是全球第二家生產和出口插電式混合模式的工廠。

- 2023 年 7 月,總部位於班加羅爾的電動車製造商 Pravaig 與沙烏地阿拉伯印度創業工作室簽署協議,在沙烏地阿拉伯建立製造工廠。一旦投入營運,這些工廠將滿足海灣、歐洲和美國市場的需求,總產能將達到 100 萬輛。

- 因此,電池價格下降和技術進步有望為市場帶來具有價格競爭力的電動車,從而創造對電池技術的需求。

預計阿拉伯聯合大公國的需求量大

- 由於消費性電子產品的普及和汽車銷售的成長,預計阿拉伯聯合大公國在預測期內的需求將大幅成長。

- 此外,由於人口成長,建築業仍然是成長最快的行業之一。該國的基礎設施發展計劃(如阿布達比地鐵和阿提哈德鐵路網)、蓬勃發展的工業化和建設活動正在興起,預計將推動備用、照明、電動工具等活動對電池的需求。

- 2023年7月,阿拉伯聯合大公國政府宣布計劃在2023年底將電動車充電站的數量增加一倍以上。

- 阿拉伯聯合大公國政府計畫到2050年,其汽車持有中50%為電動車,25%為插電式混合動力汽車(PHEV)。同時,70%的公車將是電動的,15%將是插混合動力汽車,其餘將是ICE、CNG和H2。阿拉伯聯合大公國卡車的目標是 10% 為 PHEV,40%混合動力汽車。

- 主要電動車製造商正在阿拉伯聯合大公國推出新的電動車車型。其中包括BMW i8、Mercedes GLC350e、雷諾 Zoe 和雪佛蘭 Bolt。特斯拉在阿拉伯聯合大公國的電動車市場處於領先地位,該美國品牌佔據了純電動持有的一半左右。預計這些因素將在預測期內推動阿拉伯聯合大公國對電動車電池的需求。

- Exide Al Dobowi Ltd 和 Energizer Middle East & Africa Ltd 是阿拉伯聯合大公國電池市場的主要企業。因此,從上述因素來看,阿拉伯聯合大公國可望主導中東和非洲電池市場。

中東和非洲電池產業概況

中東和非洲電池市場是分散的。主要參與企業包括(不分先後順序)C&D Technologies Inc.、East Penn Manufacturing Co. Ltd.、Exide Industries Ltd.、First National Battery Pty Ltd 和 Middle East Battery Company (MEBCO)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究範圍

- 市場定義

- 調查前提

第2章調查方法

第3章執行摘要

第4章 市場概述

- 介紹

- 2029 年市場規模與需求預測

- 近期趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 鋰離子電池價格下跌

- 電動車日益普及

- 限制因素

- 原料供需不匹配

- 驅動程式

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場區隔

- 類型

- 一次電池

- 二次電池

- 科技

- 鉛酸電池

- 鋰離子電池

- 鎳氫(NiMH)電池

- 其他技術(例如鎳鎘(NiCD)電池、鎳鋅(NiZn)電池)

- 應用領域

- 汽車電池

- 工業電池(動力、固定(電訊、UPS、能源儲存系統(ESS)等))

- 手提電池(家用電子電器產品等)

- 其他

- 地區

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

第6章競爭格局

- 併購、合資、合作與協議

- 主要企業策略

- 公司簡介

- Panasonic Corporation

- SAFT GROUPE SA

- Middle East Battery Company(MEBCO)

- Amara Raja Batteries Ltd

- First National Battery Pty Ltd

- EnerSys

- C&D Technologies Inc.

- East Penn Manufacturing Co. Inc.

- Exide Industries Ltd

- 市場佔有率

第7章 市場機會與未來趨勢

- 太陽能與能源儲存結合

The Middle East And Africa Battery Market size is estimated at USD 7.55 billion in 2025, and is expected to reach USD 10.60 billion by 2030, at a CAGR of greater than 7% during the forecast period (2025-2030).

Key Highlights

- The major factors driving the Middle-East and Africa battery market include declining lithium-ion battery prices, increasing adoption of electric vehicles, and growing renewable sector. Also, increasing demand from data centers is likely to drive the market as data centers are evolving digital infrastructures for cloud services, and the next generation of cloud services may be adapted to incorporate a blockchain network.

- However, the demand-supply mismatch of raw materials is likely to hinder the market growth.

- The use of energy storage with solar PV has been gaining popularity in developing countries, which is likely to create a huge opportunity for the battery market.

- The United Arab Emirates is expected to dominate the market, owing to its purchase of consumer electronics, including smartphones and automobiles, by the young and diverse population of the country.

Middle East And Africa Battery Market Trends

Automotive Batteries Segment to Witness Significant Growth

- The automotive sector is expected to be one of the major end-user segments for batteries, primarily lithium-ion batteries, as soon as they are used in EVs. The penetration of electric vehicles is anticipated to provide a massive impetus for the lithium-ion battery industry's growth.

- A range of different vehicle types are available globally, featuring increasing degrees of hybridization and electrification. There are various types of vehicles, including hybrid electric vehicles, plug-in hybrid electric vehicles, and electric vehicles.

- The demand has been growing at a negligible rate in the less developed nations of the Middle-East and Africa. In the Middle Eastern region, most of the countries are dependent on crude oil production. However, aligning with the emission norms, the demand for EVs is expected to increase over the forecast period, in turn leading to an increase in the consumption of batteries.

- South Africa is one of the major automotive markets in Africa, where Nissan Leaf launched the electric car in 2014. In 2015, BMW entered the market and launched the i3 and i8 models.

- In June 2023, BMW announced that it would inject USD 218 Million into its factory at Plant Rosslyn in Pretoria, South Africa, which was BMW's first foreign plant outside of Germany, making it the second in the world to produce and export its X3 plug-in hybrid model.

- In July 2023, Pravaig, a Bengaluru-based electric vehicle manufacturer, inked a pact with Saudi India Venture Studio to set up a manufacturing facility in Saudi Arabia. Upon commencement, it will cater to the demand in the Gulf, European, and US markets with a total capacity of up to one million units.

- Therefore, falling battery prices and improving technology are expected to bring price-competitive electric vehicles to the market, creating demand for battery technologies.

The United Arab Emirates to Witness Significant Demand

- The United Arab Emirates is likely to witness significant demand over the forecast period due to the increasing adoption of consumer electronic goods and increasing automotive sales, which in turn is expected to boost the overall battery demand, i.e., both primary and secondary, in the United Arab Emirates.

- Furthermore, the construction and building industry remains one of the fastest-growing sectors, owing to the increasing population. Infrastructure development projects (such as Abu Dhabi Metro and Etihad Rail Network), booming industrialization, and construction activities are expected to be on the higher side in the country, which, in turn, is expected to supplement the demand for batteries for activities, such as backup, lighting, and power tools.

- In July 2023, the UAE government announced plans to more than double the number of EV charging stations by the end of 2023.

- The United Arab Emirates government is planning the car fleet to be 50% electric vehicles by 2050 and 25% plug-in hybrids (PHEV). Meanwhile, buses are to be 70% electric, 15% plug-in hybrid, and the remainder to ICE, CNG, and H2; the target for trucks in the UAE is 10% PHEV and 40% hybrid.

- Major EV manufacturers are launching new EV models in the United Arab Emirates. Some of these are BMW i8, Mercedes GLC350e, Renault Zoe, and Chevrolet Bolt. Tesla has been driving the EV market in the United Arab Emirates, with the American brand being responsible for roughly half of the PEV fleet. These factors are expected to drive the demand for EV batteries in the United Arab Emirates over the forecast period.

- Exide Al Dobowi Ltd and Energizer Middle East & Africa Ltd are some of the top players in the UAE battery market. Therefore, from the above factors, it is evident that the United Arab Emirates is anticipated to dominate the battery market in the Middle-East and African region.

Middle East And Africa Battery Industry Overview

The Middle-East and Africa battery market is fragmented. Some of the key players include (in no particular order) C&D Technologies Inc., East Penn Manufacturing Co. Inc., Exide Industries Ltd, First National Battery Pty Ltd, and Middle East Battery Company (MEBCO).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Declining lithium-ion battery prices

- 4.5.1.2 Increasing adoption of electric vehicles

- 4.5.2 Restraints

- 4.5.2.1 Demand-supply mismatch of raw materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Primary Battery

- 5.1.2 Secondary Battery

- 5.2 Technology

- 5.2.1 Lead-acid Battery

- 5.2.2 Lithium-ion Battery

- 5.2.3 Nickel-metal Hydride (NiMH) Battery

- 5.2.4 Other Technologies (Nickel-cadmium (NiCD) Battery, Nickel-zinc (NiZn) Battery, etc.)

- 5.3 Application

- 5.3.1 Automotive Batteries

- 5.3.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.3.3 Portable Batteries (Consumer Electronics, etc.)

- 5.3.4 Other Applications

- 5.4 Geography

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 South Africa

- 5.4.4 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Panasonic Corporation

- 6.3.2 SAFT GROUPE SA

- 6.3.3 Middle East Battery Company (MEBCO)

- 6.3.4 Amara Raja Batteries Ltd

- 6.3.5 First National Battery Pty Ltd

- 6.3.6 EnerSys

- 6.3.7 C&D Technologies Inc.

- 6.3.8 East Penn Manufacturing Co. Inc.

- 6.3.9 Exide Industries Ltd

- 6.4 Market Share

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Use of energy storage with solar PV

2032 年電池市場預測:按類型、材料類型、電壓、應用、最終用戶和地區進行的全球分析

2032 年電池市場預測:按類型、材料類型、電壓、應用、最終用戶和地區進行的全球分析 2025 年至 2033 年電池市場報告,按類型(一次電池、二次電池)、產品(鋰離子電池、鉛酸電池、鎳氫電池、鎳鎘電池等)、應用(汽車電池、工業電池、攜帶式電池)和地區分類

2025 年至 2033 年電池市場報告,按類型(一次電池、二次電池)、產品(鋰離子電池、鉛酸電池、鎳氫電池、鎳鎘電池等)、應用(汽車電池、工業電池、攜帶式電池)和地區分類 量子電池市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分,按技術類型、按原料、按應用、按地區、按競爭,2020-2030F

量子電池市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分,按技術類型、按原料、按應用、按地區、按競爭,2020-2030F NMC 電池組:市場佔有率分析、行業趨勢和統計、成長預測(2025-2029 年)亞太地區 NMC 電池組市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)亞太電池:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美 NMC 電池組:市場佔有率分析、行業趨勢和統計、成長預測(2025-2029 年)拉丁美洲電池:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)日本電池市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)東南亞電池:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

NMC 電池組:市場佔有率分析、行業趨勢和統計、成長預測(2025-2029 年)亞太地區 NMC 電池組市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)亞太電池:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美 NMC 電池組:市場佔有率分析、行業趨勢和統計、成長預測(2025-2029 年)拉丁美洲電池:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)日本電池市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)東南亞電池:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)