|

市場調查報告書

商品編碼

1687431

浮體式海上風電-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Floating Offshore Wind Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

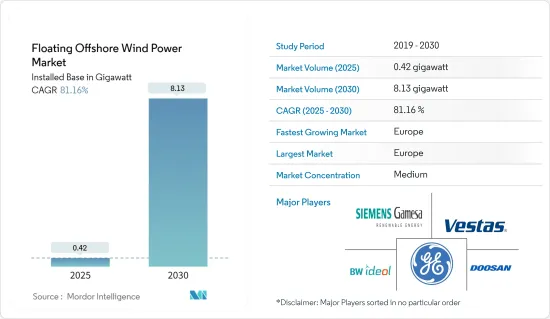

預計浮體式海上風電裝置規模將從 2025 年的 0.42 吉瓦擴大到 2030 年的 8.13 吉瓦,預測期內(2025-2030 年)的複合年成長率為 81.16%。

主要亮點

- 從中期來看,預計對海上可再生風力發電計劃的投資增加以及先進且易於獲得的海上風力發電技術將成為預測期內浮體式海上風電市場的主要驅動力。

- 然而,在預測期內,來自替代可再生能源市場的激烈競爭將抑制浮體式海上風電市場的發展。

- 然而,由於尚未開發的深水區有利於浮體式結構的發展,浮體式海上風電越來越受歡迎,為市場參與者提供了充足的機會。

- 預計預測期內歐洲將主導浮體式海上風電市場。這是因為該地區目前正在建造和規劃浮體式海上發電工程。

浮體式海上風電市場趨勢

過渡水深(30 公尺至 60 公尺深度)段預計將成長

- 由於水深較大、計劃經濟性較高,浮體式海上風電(FOWT)技術正在過渡水深(30-60公尺深度)中開發。駁船型是淺水區最具商業性可行性的浮體式風力發電機設計。此型號適用於30公尺以上的作業,是所有浮體式基礎中吃水最淺的。

- 基於駁船的浮體式風力發電機佔地面積為方形,而其他設計則採用月池來減少波浪載荷造成的壓力。據 GWEC 稱,一台典型的 6 兆瓦浮體式駁船風力發電機重量在 2,000 至 8,000 噸之間。然而,BW Ideol 憑藉其阻尼池駁船浮動子結構技術,是唯一部署兆瓦級駁船型 FOWT 的公司。

- 由於水深較淺,FOWT 技術從商業角度來看不如固定基座技術實用。預計在預測期內,駁船技術將佔據 FOWT 市場的一小部分。根據美國環保署的數據,截至 2021 年,全球運作的駁船 FOWT 容量僅為 5 兆瓦。基於駁船的FOWT容量約為1,932兆瓦,佔全球未來計劃宣布的離岸風電基礎技術總量的2.1%。

- 大多數公司正嘗試將可以在深水域中使用的FOWT設計推向市場。然而,一些半潛式技術也可以在過渡深度使用。幾種基於半潛式設計的商業性FOWT 模型允許它們在過渡水深下運作。其中一些模型最初用於實驗計劃,而其他一些模型則經過改進後用於商業項目。

- 美國能源局風力發電技術辦公室(WETO)於2024年4月24日宣布,打算發布一份意向通知,其中包含4800萬美元的資助機會,用於區域和國家浮體式海上風電技術的研究和開發,包括浮動離岸風電平台的研究和開發。這為該市場的未來成長潛力提供了良好的基礎。

- 根據國際可再生能源機構 (IEA) 的《2024 年可再生能源容量報告》,全球離岸風力發電裝置容量將在 2023-24 年成長 17.26%,即 2023 年增加 10,696 兆瓦,到 2022 年裝置容量將達到 61,967 兆瓦。這樣的發展為不久的將來的市場先驅者帶來了光明的前景。

- 大多數處於轉型期的 FOWT計劃可能位於歐洲,特別是英國、斯堪地那維亞和法國,其中大型計劃正處於規劃階段。預計預測期內該領域的大部分部署將在這些地區進行。

- 因此,預計預測期內過渡水深(30 公尺至 60 公尺深度)段將大幅成長。

預計歐洲將主導市場

- 歐洲佔據全球離岸風力發電裝置容量的最大佔有率。根據歐盟統計,歐洲佔全球離岸風力發電裝置容量的四分之一。該國(主要是北海國家)很可能成為離岸風力發電市場的推動力量。

- 全球整體約85%的離岸風力發電電場安裝在歐洲海域。北海地區的政府尤其為在其領海內建立離岸風力發電設定了雄心勃勃的目標。

- EolMed計劃是法國在地中海的首個浮體式試驗風力發電廠。 2022 年 5 月,道達爾能源宣布開始該計劃建設,目標是在 2024 年運作。該計劃由三台 10MW浮體式渦輪機組成,固定在 62 公尺深的海床上。該渦輪機將採用帶有阻尼池的駁船設計。

- 根據國際可再生能源機構的《2024年再生能源容量報告》,歐洲離岸風力發電裝置容量將在2023-24年間成長9.58%,從2023年的2830兆瓦增加到2022年的29539兆瓦。這些發展趨勢預示著市場相關人員在不久的將來將擁有光明的前景。

- 2023年8月,全球最大的浮體式風力發電廠Hywind Tampen計劃在挪威海岸約140公里處270-310公尺深的水域開始運作。 Hywind Tampen 將使用 11 台浮體式風力發電機,系統容量為 88MW。我們為海上石油和天然氣平台的電力供應做出貢獻。

- 2024 年 5 月,著名可再生能源公司 Invenergy 宣布計劃在拉科魯尼亞建設一個 552 兆瓦的浮體式海上風電發電工程。該計劃名為“O Boi”,位於離岸 45.7 至 60 公里處,該地區被國家政府認定為具有巨大風力發電潛力。一旦運作,O Boi'計劃將滿足加利西亞約 15% 的電力需求,並為超過 60住宅供電。

- 這些趨勢很可能使歐洲在預測期內成為浮體式海上風力發電廠的關鍵參與者。

浮體式海上風電產業概況

浮體式海上風電市場較為分散。市場的主要企業包括通用電氣、斗山能源、西門子歌美颯可再生能源、BW Ideaol SA 和維斯塔斯風力系統 AS。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究範圍

- 市場定義

- 調查前提

第2章執行摘要

第3章調查方法

第4章 市場概述

- 介紹

- 截至2029年浮體式海上風電累積設置容量預測

- 主要計劃資訊

- 現有主要計劃

- 未來計劃

- 近期趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 加大對海上風力發電計劃的投資

- 先進、隨時可用的海上風力發電技術

- 限制因素

- 來自替代可再生能源市場的激烈競爭

- 驅動程式

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- 投資分析

第5章市場區隔

- 依深度(僅定性分析)

- 淺水區(水深小於30公尺)

- 瞬時水深(水深30m至60m)

- 深水域(水深超過60公尺)

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 越南

- 泰國

- 印尼

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 埃及

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章競爭格局

- 合併、收購、合作及合資

- Strategies and SWOT Adopted by Leading Players

- 公司簡介

- Vestas Wind Systems AS

- General Electric Company

- Siemens Gamesa Renewable Energy SA

- BW Ideol AS

- Equinor ASA

- Marubeni Corporation

- RWE AG

- Doosan Enerbility Co. Ltd

- 市場排名分析

- List of Other Prominent Companies

第7章 市場機會與未來趨勢

- 在未開發的深海近海區域開發浮體式海上發電工程

簡介目錄

Product Code: 62712

The Floating Offshore Wind Power Market size in terms of installed base is expected to grow from 0.42 gigawatt in 2025 to 8.13 gigawatt by 2030, at a CAGR of 81.16% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, rising investments in offshore renewable wind energy projects, coupled with advanced and readily accessible offshore wind turbine technologies, are expected to be major drivers of the floating offshore wind market during the forecast period.

- On the other hand, tough competition from alternate renewable energy markets will restrain the floating offshore wind market during the forecast period.

- Nevertheless, floating offshore wind energy is becoming more popular in developing untapped deep-water prospects favorable for floating structures, providing ample opportunities for the market players.

- Europe is expected to dominate the floating offshore wind market during the forecast period. Owing to ongoing and upcoming floating offshore wind energy projects in the region.

Floating Offshore Wind Power Market Trends

The Transitional Water (30 m to 60 m depth) Segment is Expected to Grow

- Due to the greater water depth and favorable project economics, floating offshore wind turbine (FOWT) technology is more developed in transitional water depths (30-60 meters). The barge variant is the most commercially viable floating wind turbine design at shallow depths. This model is appropriate for activities higher than 30 meters (m) and has the shallowest draft of any floating foundation.

- Barge-style floating wind turbines have a square footprint, while other designs incorporate a moonpool to lessen stresses brought on by wave-induced loads. According to GWEC, a typical 6-megawatt floating barge wind turbine weighs between 2,000 and 8,000 tons. However, BW Ideol, with its Damping Pool Barge Floating Substructure Technology, is the only company that has deployed barge-type FOWT at the MW scale.

- Since the water depth is shallower, FOWT technology is less practical from a business point of view than fixed-base technology. During the forecast period, barge technology is expected to make up a small part of the FOWT market. According to the US EPA, only 5 MW of barge FOWT capacity operated globally as of 2021. Around 1,932 MW of FOWT capacity on barges, or 2.1% of all announced offshore wind substructure technologies for future projects worldwide, was announced.

- Most companies attempt to market FOWT designs that can be used in deeper waters. However, some semi-submersible technologies can also be used at transitional water depths. They can function at transitional depths due to several commercial FOWT models that are built on the semi-submersible design. A few of these models were initially used in experimental projects, while others were modified for use in ventures for profit.

- The US Department of Energy's Wind Energy Technologies Office (WETO) announced on April 24, 2024, that it intended to issue a Notice of Intent involving a USD 48 million funding opportunity for regional and national research and development of offshore wind technologies, including floating offshore wind platform research and development. This promises future growth potential for the market.

- According to the International Renewable Energy Agency RE Capacity 2024, the global installed offshore wind energy capacity increased by 17.26% in FY 2023-24, adding 10,696 MW in 2023 to the earlier installed capacity of 61,967 MW in 2022. Such developments show promising outlooks for the market players in the near future.

- Most of the FOWT projects in transitional depths are likely to be in Europe, especially in the United Kingdom, Scandinavia, and France, where large projects are in the planning stages. During the forecast period, most of the deployments in this segment are likely to happen in these regions.

- Thus, the transitional water (30 m to 60 m depth) segment is expected to grow significantly during the forecast period.

Europe is Expected to Dominate the Market

- Europe holds the largest share of offshore wind energy installations globally. According to the European Union, Europe represents a quarter of global offshore wind installations. The country (primarily North Sea countries) is likely to be at the helm of the offshore wind market.

- Around 85% of offshore wind installations are globally in European waters. Governments, particularly in the North Sea area, have set ambitious targets for installing offshore wind farms in their territorial waters.

- The EolMed project is France's first floating pilot wind farm in the Mediterranean Sea. In May 2022, TotalEnergies announced the start of the project's construction, which is expected to be operational by 2024. The project consists of three 10 MW floating turbines on the bathymetry of the 62-meter depth and anchored to the seabed. The turbines will use a barge design with a damping pool.

- According to the International Renewable Energy Agency RE Capacity 2024, the installed offshore wind energy capacity in Europe increased by 9.58% in FY 2023-24, adding 2,830 MW in 2023 to the earlier installed capacity of 29,539 MW in 2022. Such developments show promising outlooks for the market players in the near future.

- In August 2023, the world's largest floating wind farm, the Hywind Tampen Project, started operating around 140 kilometers off the coast of Norway in depths ranging from 270 to 310 meters. Hywind Tampen uses 11 floating wind turbines and has a system capacity of 88 MW. It helps power operations at offshore oil and gas platforms.

- In May 2024, Invenergy, a prominent player in the renewable energy sector, unveiled its plans for a 552 MW floating offshore wind project in A Coruna. Dubbed 'O Boi', the project will be situated 45.7 to 60 kilometers offshore, in a zone recognized by the central government for its significant wind potential. Once operational, the 'O Boi' project aims to meet approximately 15% of Galicia's electricity demand, sufficient to energize over 600,000 residences.

- During the forecast period, these trends should make Europe a significant players involved in floating offshore wind farms.

Floating Offshore Wind Power Industry Overview

The floating offshore wind power market is semi-fragmented. Some major players in the market include General Electric Company, Doosan Energy, Siemens Gamesa Renewable Energy, BW Ideaol SA, and Vestas Wind Systems AS.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Floating Offshore Wind Power Cumulative Installed Capacity Forecast, till 2029

- 4.3 Key Projects Information

- 4.3.1 Major Existing Projects

- 4.3.2 Upcoming Projects

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Rising Investments in Offshore Wind Energy Projects

- 4.6.1.2 Advanced and Readily Accessible Offshore Wind Turbine Technologies

- 4.6.2 Restraint

- 4.6.2.1 Tough Competition from Alternate Renewable Energy Markets

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Water Depth (Qualitative Analysis Only)

- 5.1.1 Shallow Water (less than 30 m depth)

- 5.1.2 Transitional Water (30 m to 60 m depth)

- 5.1.3 Deep Water (higher than 60 m depth)

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Nordic Countries

- 5.2.2.7 Russia

- 5.2.2.8 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Malaysia

- 5.2.3.6 Vietnam

- 5.2.3.7 Thailand

- 5.2.3.8 Indonesia

- 5.2.3.9 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Egypt

- 5.2.5.4 South Africa

- 5.2.5.5 Nigeria

- 5.2.5.6 Rest of the Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Collaboration and Joint Ventures

- 6.2 Strategies and SWOT Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Vestas Wind Systems AS

- 6.3.2 General Electric Company

- 6.3.3 Siemens Gamesa Renewable Energy SA

- 6.3.4 BW Ideol AS

- 6.3.5 Equinor ASA

- 6.3.6 Marubeni Corporation

- 6.3.7 RWE AG

- 6.3.8 Doosan Enerbility Co. Ltd

- 6.4 Market Ranking Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Developing Floating Offshore Wind Projects in Untapped Offshore Deep-water Prospects

02-2729-4219

+886-2-2729-4219

離岸風力發電市場規模、佔有率、成長分析,按組件、按水深、按安裝、按容量、按應用、按地區 - 行業預測,2025 年至 2032 年

離岸風力發電市場規模、佔有率、成長分析,按組件、按水深、按安裝、按容量、按應用、按地區 - 行業預測,2025 年至 2032 年 浮動離岸風能市場機會、成長動力、產業趨勢分析及2025-2034年預測海上風能市場機會、成長動力、產業趨勢分析及2025-2034年預測離岸風電電纜市場規模、佔有率和成長分析(按類型、材料、安裝類型、最終用途和地區)- 產業預測 2025-2032

浮動離岸風能市場機會、成長動力、產業趨勢分析及2025-2034年預測海上風能市場機會、成長動力、產業趨勢分析及2025-2034年預測離岸風電電纜市場規模、佔有率和成長分析(按類型、材料、安裝類型、最終用途和地區)- 產業預測 2025-2032 海上可再生能源市場報告:趨勢、預測和競爭分析(至 2031 年)

海上可再生能源市場報告:趨勢、預測和競爭分析(至 2031 年) 2025 年離岸風力發電全球市場報告離岸風力發電市場:2033 年市場分析與預測 - 按類型、產品、服務、技術、組件、應用、安裝類型、設備、最終用戶、解決方案

2025 年離岸風力發電全球市場報告離岸風力發電市場:2033 年市場分析與預測 - 按類型、產品、服務、技術、組件、應用、安裝類型、設備、最終用戶、解決方案 離岸風力發電市場:2025-2035年

離岸風力發電市場:2025-2035年 亞太地區浮體式海上風電:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美浮體式海上風電:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

亞太地區浮體式海上風電:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美浮體式海上風電:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

▼