|

市場調查報告書

商品編碼

1687467

瓦楞包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Corrugated Board Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

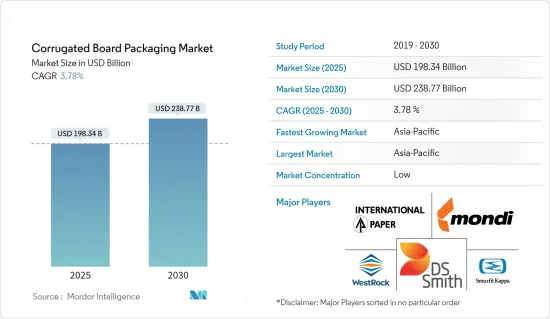

瓦楞包裝市場規模預計在 2025 年為 1,983.4 億美元,預計到 2030 年將達到 2,387.7 億美元,預測期內(2025-2030 年)的複合年成長率為 3.78%。

瓦楞紙板由於其對粗暴搬運的強大保護能力而成為首選的包裝材料。瓦楞紙板的耐用性、多功能性和穩定性使其成為零售業的主要材料,而且隨著全球電子商務銷售額的飆升,其採用率也日益成長。

主要亮點

- 越來越多的公司將注意力轉向不僅防潮而且還能承受長期運輸的紙板包裝。隨著企業採用瓦楞紙板進行二次和三次包裝,這一趨勢顯而易見。需求激增主要是因為麵包和肉品等加工食品和易腐食品需要一次性包裝。此外,隨著人們生活方式變得越來越忙碌,對簡便食品的需求也越來越大。

- 紙板由紙漿和紙製成,比塑膠更可回收。瓦楞紙板可充當減震器,保護內容物免受外部衝擊。瓦楞紙板可以承受巨大的壓力,其不同厚度的層和凹槽提供了必要的緩衝作用。電子商務行業最近已成為紙板的主要消費領域。亞馬遜和其他大公司使用紙板作為主要包裝,但使用塑膠來包裝單一物品。

- 這個市場也存在挑戰和限制。紙板不像塑膠箱或木箱那麼耐用,因此不適合承受重載或極端壓力。它們通常更適合短期使用,而不是長期可重複使用的投資。

- 瓦楞紙板用途廣泛,可以製成各種形狀,包括盒子。隨著人們對永續性的興趣日益濃厚,紙板正逐漸被軟性塑膠袋所取代。此外,它與多種印刷技術的兼容性使其成為企業的一種有吸引力的行銷工具,可以有效地充當行動廣告牌,而無需產生額外的行銷成本。

- 紙張和再生材料等原料的供應和價格波動會影響我們的生產和定價策略。紙包裝產業正在努力應對森林砍伐、供應鏈脆弱性、環境問題、監管挑戰以及永續創新的迫切動力等帶來的挑戰。

紙板包裝市場的趨勢

加工食品預計將佔據主要市場佔有率

- 瓦楞紙板是加工食品行業的流行包裝選擇。盒子有各種尺寸和形狀。顧客可以用熟悉的容器享用零食。紙板包裝的穀物、餅乾和其他零嘴零食的消費歷史可以追溯到幾個世代以前。

- 由於瓦楞包裝可以使產品遠離濕氣並能承受長時間的運輸,因此公司擴大採用它以提供更好的客戶結果,特別是在二次或三級包裝中。麵包、肉品和其他生鮮產品等加工食品的需求量很大,因為這些包裝材料只需一次性使用。

- 根據詹姆斯敦容器公司 2023 年 9 月發布的公告,紙板食品包裝越來越被視為傳統材料的環保替代品。它的多功能性延伸到各種食品,包括生鮮食品、烘焙點心、冷凍食品和罐頭食品等。瓦楞包裝的高度可自訂性使企業能夠創造出獨特且具有視覺吸引力的設計。這包括將您的品牌標識、產品詳細資訊和其他品牌元素直接印在盒子上,以提高品牌知名度並改善產品展示。

- 對許多食品來說,紙板包裝正成為塑膠包裝的可行替代品。隨著高速網路服務的普及以及電子零售和電子商務管道的興起,消費者現在可以更輕鬆地在線上訂購各種包裝食品。此外,豐厚的折扣和便利性吸引了許多消費者,推動了整個預測期內這一領域的成長。這包括起司、預製湯、罐頭魚等。瓦楞紙箱包裝可以用可回收和可堆肥的材料更簡單地製作。

- 消費者,尤其是千禧世代,越來越意識到食品包裝、生產和廢棄物對環境的影響。根據斯道拉恩索的一項調查,59% 的千禧世代認為包裝應該在整個價值鏈中實現永續。對永續包裝產品的需求是加工食品包裝的主要驅動力,對瓦楞包裝市場的成長產生了積極影響。

- 據巴西紙漿和造紙製造商 Suzanne 以及歐洲領先的工程、設計和諮詢服務公司 AFRY 稱,預計 2022 年全球紙和紙板消費量將達到 4.15 億噸。預計未來十年消費量將進一步增加,到 2032 年將達到 4.76 億噸。世界上大部分的紙和紙板產量都用於包裝。

預計亞太地區將佔很大佔有率

- 隨著都市化以及人們對環保包裝意識的不斷增強,亞太地區瓦楞包裝市場將會成長。主要的行業趨勢包括瓦楞紙生產能力的提高和技術的進步。然而,嚴格的法規和產品品質問題可能會阻礙這種成長。

- 亞洲瓦楞包裝市場加速成長的動力包括永續包裝需求激增、電子商務產業蓬勃發展、電子產品和個人保健產品需求上升以及發展中經濟體人均收入上升。

- 人均收入的提高和人口結構的變化正在改變中國瓦楞包裝行業,需要新的包裝材料和工藝。阿里巴巴等電子商務巨頭準備推動瓦楞包裝市場的發展。國際貿易部報告稱,中國在全球電子商務市場佔據主導地位,佔全球貿易總額的 50% 左右。預計到 2024 年,線上零售貿易將達到 3.56 兆美元,這項繁榮將擴大對永續包裝解決方案的需求,從而促進瓦楞包裝的銷售。

- 在印度、中國、日本等國家,食品飲料、IT電子、家電等嚴重依賴瓦楞包裝的產業正經歷消費升級趨勢。主要終端用戶產業的轉變預計將推動中高階瓦楞包裝市場的發展。

- 此外,亞太國家原料的供應、政府對一次性塑膠的限制以及這些國家終端使用產業數量的增加也刺激了瓦楞包裝市場的成長。

瓦楞包裝行業概況

瓦楞包裝市場分散,有許多參與者,包括:Mondi Group、DS Smith PLC、WestRock Company、Smurfit Kappa Group 等,提供多樣化的解決方案。這些公司正在創新並推出環保包裝產品以支持永續發展。此外,他們還推出了適合各終端用戶產業的客製化瓦楞紙箱設計,抓住新興機會。此外,隨著主要參與者加強在瓦楞紙板包裝領域的投資組合,市場正經歷一系列合作和收購。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場動態

- 市場促進因素

- 環保材料的日益普及和瓦楞紙板數位印刷的發展

- 電子商務產業需求強勁

- 市場限制

- 增加可回收和可重複使用的包裝

第6章 市場細分

- 按最終用戶產業

- 加工食品

- 生鮮食品和蔬菜

- 飲料

- 個人及居家護理

- 電子商務

- 其他終端用戶產業(電氣和電子、醫療保健、工業、紡織、玻璃和陶瓷)

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 波蘭

- 亞洲

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 泰國

- 澳洲和紐西蘭

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 北美洲

第7章 競爭格局

- 公司簡介

- International Paper Company

- Mondi Group

- DS Smith PLC

- WestRock Company

- Smurfit Kappa Group

- Stora Enso Oyj

- Sealed Air Corporation

- Asia Pulp & Paper(APP)Sinar Mas

- Napco National

- Georgia-Pacific LLC

- Nine Dragons Paper Holdings Limited

- Oji Holdings Corporation

第8章投資分析

第9章:未來市場展望

The Corrugated Board Packaging Market size is estimated at USD 198.34 billion in 2025, and is expected to reach USD 238.77 billion by 2030, at a CAGR of 3.78% during the forecast period (2025-2030).

With its robust protection against harsh handling, the corrugated board has emerged as the packaging of choice. Its durability, versatility, and stability make it a staple in the retail sector, and with the global surge in e-commerce sales, its adoption is only intensifying.

Key Highlights

- Businesses increasingly turn to corrugated board packaging, not only for its moisture protection but also for its resilience during extended transportation. This trend is significantly pronounced as companies adopt it for secondary and tertiary packaging. The surge in demand is primarily driven by processed and perishable foods, like bread and meat products, which necessitate single-use packaging. Additionally, as people's lifestyles grow busier, the appetite for convenience foods rises.

- Crafted from pulp and paper, corrugated boards boast a recyclability edge over their plastic counterparts. The fluting medium acts as a shock absorber, safeguarding contents from external impacts. These boards can endure significant pressure, and their layered and varied-thickness flutes provide essential cushioning. The e-commerce sector has recently emerged as a dominant consumer of corrugated boards. Major players, including Amazon, utilize these boards for primary packaging while reserving plastic for individual items.

- The market also has challenges and limitations. The corrugated board lacks the durability of plastic or wooden boxes, making them less suitable for heavy items or extreme pressures. Typically, it's favored for short-term use rather than as long-term, reusable investments.

- Their versatility allows corrugated boards to be molded into various shapes, including boxes. As sustainability concerns mount, they're gradually replacing flexible plastic bags. Furthermore, their compatibility with diverse printing techniques makes them an attractive marketing tool for companies, effectively serving as mobile billboards without incurring extra marketing costs.

- Variations in the availability and pricing of raw materials, such as paper and recycled content, can influence production and pricing strategies. The paper packaging industry grapples with challenges stemming from deforestation, encompassing supply chain vulnerabilities, environmental issues, regulatory challenges, and an urgent push for sustainable innovations.

Corrugated Board Packaging Market Trends

Processed Food Segment Expected to Occupy Significant Market Share

- The corrugated board is a popular packaging choice in the processed food industry. There are many different sizes and shapes of boxes. Customers are given a well-known container to enjoy their snacking in. The consumption of cereal, crackers, and other snack foods packaged in corrugated boards spans several generations.

- The corrugated board packaging keeps moisture away from products and can withstand long shipping times, companies are increasingly adopting this packaging to offer better customer outcomes, especially for secondary or tertiary packaging. Processed foods, such as bread, meat products, and other perishable items, need these packaging materials to be used just once, thus driving the demand.

- According to Jamestown Container in September 2023, corrugated food packaging is increasingly considered an eco-friendly alternative to conventional materials. Its versatility spans various food products, including fresh produce, baked goods, and frozen and canned items. The high customizability of corrugated packaging allows businesses to craft distinctive and visually appealing designs. This includes printing brand logos, product details, and other branding elements directly onto the boxes, enhancing brand recognition, and elevating product presentation.

- Corrugated board packaging is becoming a viable alternative to plastic packaging for many food products. Due to the rising accessibility of high-speed internet services and the rise of e-retail and e-commerce channels has been sparked, making it more straightforward for customers to order various kinds of processed food goods online. In addition, the generous savings and convenience it offers draw more consumers, adding to the segment's growth throughout the forecast period. These include cheese, ready-made soups, and canned fish, among others. Corrugated box packaging can be created more simply from recycled or composted materials.

- Consumers, such as millennials, are becoming more aware of the environmental impact of food packaging, production, and waste. According to a Stora Enso survey, 59% of millennials think packaging should be sustainable throughout the value chain. Demand for sustainable packaging products is a key driver in processed food packaging, positively impacting corrugated board packaging market growth.

- According to Suzanne, a Brazilian pulp and paper producer, and AFRY, a critical European engineering, design, and advisory services firm, the global consumption of paper and paperboard was expected to be 415 million tonnes in 2022. Consumption will rise further over the next decade, reaching 476 million tonnes by 2032. Packaging consumes the majority of worldwide paper and paperboard production.

Asia Pacific is Expected to Hold a Significant Share

- Asia Pacific's corrugated board packaging market is set to grow, driven by an urbanizing population and heightened awareness of eco-friendly packaging. Key industry trends include increased containerboard capacity and technological advancements. However, stringent regulations and product quality concerns could hinder this growth.

- Accelerated growth in Asia's corrugated board packaging market is fueled by a surge in demand for sustainable packaging, a booming e-commerce sector, heightened demand for electronics and personal care products, and rising per capita income amid economic development.

- Rising per capita income and shifting demographics shape China's corrugated board packaging sector, necessitating new packaging materials and processes. E-commerce giants like Alibaba are poised to drive the corrugated packaging market. The International Trade Administration reported that China dominates the global e-commerce landscape, accounting for about 50% of total transactions. With projections of online retail transactions hitting USD 3.56 trillion by 2024, this boom is set to amplify the demand for sustainable packaging solutions, bolstering sales of corrugated board packaging.

- In countries like India, China, and Japan, industries such as food and beverage, IT electronics, and home appliances, which heavily rely on corrugated boxes, are experiencing a trend of consumption upgrading. This shift in leading end-user industries is anticipated to boost the market for mid to high-end corrugated cartons.

- Additionally, the growth of the corrugated board packaging market is spurred by the availability of raw materials in Asia Pacific nations, government regulations curbing single-use plastics, and a rising number of end-use industries across these countries.

Corrugated Board Packaging Industry Overview

The corrugated board packaging market is fragmented, with numerous players such as Mondi Group, DS Smith PLC, WestRock Company, Smurfit Kappa Group, and more offering diverse solutions. These companies are innovating and rolling out eco-friendly packaging products to support sustainability. Additionally, they're unveiling tailored corrugated box designs catering to various end-user industries, seizing emerging opportunities. Furthermore, the market is seeing a flurry of partnerships and acquisitions as key players bolster their portfolios in the corrugated board packaging arena.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Eco-friendly Materials and Evolution of Digital Print for Corrugated Boards

- 5.1.2 Strong Demand from the E-commerce Sector

- 5.2 Market Restraint

- 5.2.1 Increasing Usage of Returnable and Reusable Packaging

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Processed Foods

- 6.1.2 Fresh Food and Produce

- 6.1.3 Beverages

- 6.1.4 Personal and Household Care

- 6.1.5 E-commerce

- 6.1.6 Other End-user Industries (Electrical & Electronics, Healthcare, Industrial, Textile, Glass & Ceramics)

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.2.4 Italy

- 6.2.2.5 Spain

- 6.2.2.6 Poland

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 South Korea

- 6.2.3.5 Indonesia

- 6.2.3.6 Thailand

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.5.1 Brazil

- 6.2.5.2 Argentina

- 6.2.5.3 Mexico

- 6.2.6 Middle East and Africa

- 6.2.6.1 Saudi Arabia

- 6.2.6.2 South Africa

- 6.2.6.3 United Arab Emirates

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 International Paper Company

- 7.1.2 Mondi Group

- 7.1.3 DS Smith PLC

- 7.1.4 WestRock Company

- 7.1.5 Smurfit Kappa Group

- 7.1.6 Stora Enso Oyj

- 7.1.7 Sealed Air Corporation

- 7.1.8 Asia Pulp & Paper (APP) Sinar Mas

- 7.1.9 Napco National

- 7.1.10 Georgia-Pacific LLC

- 7.1.11 Nine Dragons Paper Holdings Limited

- 7.1.12 Oji Holdings Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

北美瓦楞包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

北美瓦楞包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 2025 年全球飲料紙盒包裝機市場報告

2025 年全球飲料紙盒包裝機市場報告 瓦楞包裝市場按設計、產品類型、最終用途和地區分類瓦楞包裝市場規模、佔有率和成長分析(按壁型、箱型、瓦楞、印刷技術、最終用戶、分銷管道和地區)- 2025-2032 年行業預測2030 年大型瓦楞包裝市場預測:按產品類型、產能、分銷管道、最終用戶和地區進行的全球分析歐洲和中東/非洲的瓦楞包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)英國瓦楞包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

瓦楞包裝市場按設計、產品類型、最終用途和地區分類瓦楞包裝市場規模、佔有率和成長分析(按壁型、箱型、瓦楞、印刷技術、最終用戶、分銷管道和地區)- 2025-2032 年行業預測2030 年大型瓦楞包裝市場預測:按產品類型、產能、分銷管道、最終用戶和地區進行的全球分析歐洲和中東/非洲的瓦楞包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)英國瓦楞包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 瓦楞紙板包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測瓦楞紙箱及折疊紙箱包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測飲料紙盒包裝器材市場規模、佔有率、趨勢分析報告:按類型、應用、營運模式、地區、細分預測,2025-2030 年

瓦楞紙板包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測瓦楞紙箱及折疊紙箱包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測飲料紙盒包裝器材市場規模、佔有率、趨勢分析報告:按類型、應用、營運模式、地區、細分預測,2025-2030 年