|

市場調查報告書

商品編碼

1590947

脫離電池將創造milliWh-GWh大規模新市場:40條生產線的預測與技術(2025-2045)Escape from Batteries Creates Large New Markets milliWh-GWh: Forecasts in 40 lines, Technology 2025-2045 |

||||||

無電池儲存預計在 20 年內成長五倍,成為價值 2,500 億美元的業務。

脈衝與高功率儲存

儘管超級電容器、飛輪發電機和抽水蓄能等傳統儲存領域有所成長,但大部分成長來自許多新的儲存格式。鋰離子電容器目前用於電磁武器、熱核反應器和採礦車輛。鉭混合電容器在脈衝雷達等軍用飛機應用中越來越受歡迎。此外,利用吊運、地下抽水蓄能發電、壓縮空氣、液化氣、熱泵蓄熱等技術的大型輸電網路正在興建中。大多數電池每 GWh 的成本更高,但替代品具有巨大的規模經濟,不易燃,並且降解或洩漏的可能性很小。還能滿足每月只能使用一次的風力發電、太陽能發電的新需求。如何在很少或沒有儲存的情況下進行管理

該報告還解決了儲存排除問題,例如太陽能海水淡化、無人機和計劃中的 6G 通訊設備中出現的儲存排除情況。還有中間選項:無電池感測器、樓宇控制和由 Dracula、EnOcean 和 8Power 等公司的能量收集供電的物聯網節點。

本報告調查了由於電池轉型而產生的新市場趨勢,包括電池的局限性和課題、電池轉型的趨勢、無電池系統的類型和概述、關鍵技術的研究管道、我們的技術編製了路線圖、SWOT分析、主要公司簡介等。

目錄

第 1 章執行摘要/概述

第 2 章簡介

- 摘要

- 電池的局限性

- 鋰離子電池火災為何不斷發生

- 電氣化、電池採用和廢除的大趨勢

- 2025 年至 2045 年對儲存的影響

- 2025 年推出的電池和無電池固定儲存技術的比較和未來趨勢

- 2025 年至 2045 年的電池佔有率

第 3 章無電池系統:反向散射(EAS、RFID、6G SWIPT)、無電池電路、自供電超低功耗電路和感測器、供需管理

- 摘要

- 反向散射 SWOT

- 電路設計可最大限度地減少電池消耗

- 使用 V2G、V2H 和 V2V 消除電池並透過太陽能板直接為車輛充電

- 需求管理:2024年無蓄能太陽能海水淡化設備

- 原始碼控制:2024 年的進展

- 電池排除和規格

- 無電池能量收集

第四章靜電儲存:超級電容器、贗電容器、鋰離子電容器等BSH

- 電容器位置及其變化

- 選擇範圍:從電容器到超級電容器和電池

- 研究管線:純超級電容器

- 研究通路:混合方法

- 研究管線:贗電容器

- 超級電容器及其衍生物的實際與潛在應用

- 對103家超級電容器企業的評價:10項

- 鋰離子電容器和其他電池超級電容器混合BSH存儲

第 5 章 LGES(液化氣體儲能):LAES 或 CO2

- 摘要

- LAES(液化空氣儲能)LDES(長期儲能系統)

- 液化二氧化碳 LDES

第 6 章 CAES(壓縮空氣儲能)

- 摘要

- 供應不足吸引克隆

- CAES 市場定位

- CAES和LAES的參數評估

- CAES 技術選項

- CAES 製造商、專案、研究

- 系統設計者和供應商的 CAES 簡介/評估

- ALCAES(瑞士)

- APEX CAES(美國)

- Augwind Energy(以色列)

- Cheesecake Energy(英國)

- Corre Energy(荷蘭)

- Gaelectric(愛爾蘭)

- Huaneng Group (中國)

- Hydrostor(加拿大)

- LiGE Pty(南非)

- Storelectric(英國)

- Terrastor Energy Corporation(美國)

- SWOT評估

第七章機械儲能:APHES(先進抽水蓄能儲能)、SGES(固態重力儲能)、電轉電飛輪

- APHES(先進抽水蓄能)

- SGES(固態重力儲能)

- 電轉電飛輪

第8章氫和其他化學中間體LDES

- 摘要

- 化學中間體LDES的最佳點

- 2025 年(預發表)和 2024 年報告了 53 項研究進展

- LDES 中甲烷、氨與氫氣的比較

- 氫 LDES 領導者:美國卡利斯託加彈性中心

- 計算顯示氫在長期 LDES 中獲勝

- 礦業巨頭正在謹慎地尋求多種選擇

- 建築物及其他小地點

- 儲氫技術

- LDES儲氫參數評估

- LDES 中的氫氣、甲烷和氨:SWOT 評估

第 9 章 ETES(熱能儲存)用於延遲供電

- 摘要

- 2024年研究進展

- 熱機方法取得了成功:Echogen USA

- 利用極端溫度和光電轉換

- 一家工廠延遲銷售熱力和電力

- LDES 的 ETES:SWOT 評估

- ETES參數評估

Summary

Battery-free storage will quintuple to become a $250 billion business in 20 years. A new 493-page Zhar Research report has the detail. It is, "Escape from Batteries Creates Large New Markets milliWh-GWh: Forecasts in 40 lines, Technologies 2025-2045".

Pulse and high-power storage

There is growth in the traditional forms - supercapacitors, flywheel generators and pumped hydro. However, most of the growth comes from a host of new forms. Lithium-ion capacitors are now seen in electromagnetic weapons, thermonuclear reactors and mining vehicles. Tantalum hybrid capacitors further penetrate military aircraft applications such as pulsed radar. Massive grid storage is being built based on lifting blocks, underground pumped hydro, compressed air and liquid gas, heat pump thermal storage. With most batteries, to get GWh you just buy more, whereas all alternatives have great economy of scale, they are all non-flammable and they have little or no fade and self-leakage. They better meet the new need of wind and solar power being feeble for a month at a time.

How to manage with little or no storage

The report also covers the elimination of storage as seen in next solar desalination, some drones and some planned 6G Communications devices. Add the in-between option of battery-free sensors, building controls and IOT nodes with energy harvesting sold by Dracula, EnOcean, 8Power and others.

Do not make batteries your first choice

Electronics and electrical designers now first consider if they need batteries - from chip to power station - because the new battery-free options are often far better. This report is their essential reference, assessing hundreds of companies that can now supply and the remarkable new research advances through 2024. It answers questions such as:

- Gaps in the market?

- Emerging competition?

- Full list of technology options?

- 2024 research pipeline analysis?

- Technology sweet spots by parameter?

- Zhar Research appraisals by technology?

- Market forecasts by value and GWh 2025-2045?

- Technology readiness and potential improvement?

- Technology parameters compared against each other?

- Market drivers and forecasts of background parameters?

- Potential winners and losers by company and technology?

- Technologies compared by numbers GW, GWh, delay, duration, etc.?

- Appraisal of proponents, your prospective partners and acquisitions?

- Evolving market needs and technology milestones in roadmaps by year 2025-2045?

Report findings

The Executive Summary and Conclusions (39 pages) is the quick read, with many new infograms and 40 forecast lines with explanation. One image is "Lithium-ion capacitor LIC market positioning by energy density spectrum" showing images of applications over a range of energy density and cycle life. Another shows latest grid and off-grid storage projects - duration vs power - for six battery-free forms compared with battery versions.

Chapter 2. Introduction (7 pages) explains battery limitations, how lithium-ion battery fires are ongoing with many 2024 examples, electrification megatrends, battery adoption, battery elimination. See implications for storage 2025 - 2045: batteries will lose share yet remain the largest value market.

The rest of the report is extremely detailed, starting with a chapter on how to minimise or eliminate storage. Other chapters deep-dive into battery-free storage, - electrostatic, mechanical, thermal, chemical - spanning microWh to GWh, electronics to heavy engineering, pulse to one year of storage. See this formidable virtuosity increasing to replace many batteries and do what batteries can never achieve but realise there is inability impact some other battery applications.

The 63 pages of Chapter 3 concern "Systems that eliminate batteries: backscatter (EAS, RFID, 6G SWIPT), battery elimination circuits, self-powering ultra-low-power circuits and sensors, demand and supply management". Navigate the jargon such as Electronic Article Surveillance EAS , passive RFID, SWIPT, AmBC, CD-ZED for 6G Communications, V2G, V2H, V2V and vehicle charging directly from solar panels. 13 primary energy harvesting technologies are compared. See examples of battery-free desalinators, cameras, drones, IOT nodes and the significance of 25 research advances through 2024.

Chapter 4. "Electrostatic storage: Supercapacitors, pseudocapacitors, lithium-ion capacitors, other BSH" (119 pages) spans activities of 103 companies compared in ten columns, a flood of important research advances in 2024, and a very wide variety of applications emerging. That spans aerospace, electric vehicles: AGV, material handling, car, truck, bus, tram, train, grid, microgrid, peak shaving, renewable energy, uninterrupted power supplies, medical and wearables, data centers, welding, laser cannon, railgun, pulsed linear accelerator weapon, capacitor-supercapacitor hybrids in radar. All have growth ahead but battery-supercapacitor hybrids have the greatest potential 2025-2045.

In electricity generation, your solar house will continue to have a battery. At the other extreme, national and continental grids will suffer massive earthworks and massive delays to get the very lowest levelised cost of storage LCOS up to months. However, there is a very large intermediate requirement emerging from the strong trend to factories, towns and islands being off-grid or capable of being off grid using wind and solar power for around 100MW. They prefer no long delays or major earthworks. Capital cost and long life, low maintenance, small footprint matter here. New redox flow batteries serve well potentially up to one month storage but they have competition from the subject of Chapter 5. "Liquefied gas energy storage LGES: Liquid air LAES or CO2" (22 pages, 5 companies). See SWOT appraisals, parameter comparisons and a niche opportunity in grids as well.

Chapter 6. Compressed air CAES (59 pages) covers the main competitor for pumped hydro grid storage as batteries fail to keep up with ever more wind and solar power demanding ever longer storage duration. Appraise 13 participants, strong research advances and major orders in 2024. Agree with the US Department of Energy that CAES will have one of the lowest LCOS and a splendid lack of expensive or toxic materials?

Chapter 7. "Mechanical storage: Advanced pumped hydro APHES, solid gravity energy storage SGES, flywheels for electricity-to-electricity" (90 pages) delves into a flood of 2024 research, 12 companies, many options. It sees greatest potential in APHES, a large system pumping water into mines being significant in 2024, then SGES for mainstream grid requirements. Flywheels tend to lose out to supercapacitors and their variants for high power density and pulse applications.

Chapter 8. "Hydrogen and other chemical intermediary LDES" (55 pages) reports potentially a very large market extending up to seasonal storage because it could store 10GWh levels underground. However, with only one small minigrid being prepared with tank hydrogen, the scope for extreme arguments for and against is considerable. Of possible chemical intermediaries, only hydrogen has a chance, mostly in salt caverns, but leakage is considerable, causing global warming, and efficiency very poor. Some will be built. Then we shall know the parameters.

Chapter 9. "Thermal energy storage for delayed electricity ETES" reports heating rocks then making steam for turbine generation of electricity has been a failure but 2024 research and the activity of several companies has led to one major installation using heat pumps in thermal storage and there is a wild card of white heat reconverted using photovoltaics. Thermal may be a niche grid/ minigrid storage opportunity.

For those wishing to enjoy this $250 billion opportunity, the essential handbook is Zhar Research report, "Escape from Batteries Creates Large New Markets milliWh-GWh: Forecasts in 40 lines, Technologies 2025-2045".

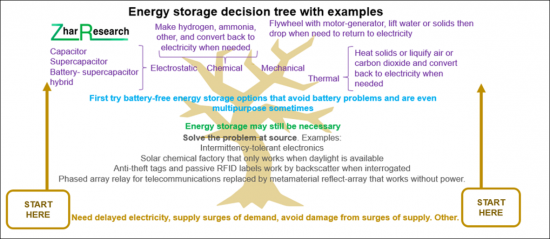

CAPTION: The energy storage decision tree with examples. Source, Zhar Research report, "Escape from Batteries Creates Large New Markets milliWh-GWh: Forecasts in 40 lines, Technologies 2025-2045".

Table of Contents

1. Executive summary and conclusions

- 1.1. Purpose and scope of this report

- 1.2. Methodology of this analysis

- 1.3. Battery current challenges and why alternatives are being adopted

- 1.3.1. General situation in electronics and electrical engineering

- 1.3.2. Battery challenges for 6G Communications and IoT and action arising 2025-2045

- 1.4. Battery-free options: eliminating storage or using alternative storage 2025-2045

- 1.5. Battery elimination options beyond drop-in replacement by battery-less storage devices

- 1.5.1. Electronics, telecommunication, electrical engineering

- 1.5.2. To the rescue: WPT, WIET, SWIPT evolution to 2045

- 1.5.3. Evolution of wireless electronic devices needing no on-board energy storage 1980-2045

- 1.5.4. SWOT appraisal of circuits and infrastructure that eliminate storage

- 1.6. Why batteries may only dominate the middle ground in 2045

- 1.7. Batteryless storage device toolkit 2025-2045

- 1.7.1. Options by size

- 1.7.2. Example: Lithium-ion capacitor LIC market positioning by energy density spectrum

- 1.7.3. Possible scenario: stationary storage batteries vs alternatives TWh cumulative 2025-2045

- 1.7.4. Example: Installed and committed stationary storage projects 2025 showing many battery and battery-less options competing

- 1.7.5. Long duration energy storage LDES toolkit for grids, microgrids, 6G base stations, data centers 2025-2045

- 1.7.6. SWOT appraisal of battery-less storage devices

- 1.8. System strategies to achieve less or no storage: combine and compromise

- 1.9. Market forecasts 2025-2045 in 40 lines

- 1.9.1. Energy storage device market battery vs batteryless $ billion 2025-2045

- 1.9.2. Possible scenario for leading storage technologies TWh cumulative 2025-2045

- 1.9.3. Supercapacitor EDLC, pseudocapacitor and battery-supercapacitor hybrid BSH $ billion 2025-2045

- 1.9.4. Total LDES value market percent in three size categories 2025-2045 table, graphs

- 1.9.5. Total LDES value market $billion X100 in three size categories 2025-2045

- 1.9.6. Total LDES value market $billionX100 by four regions 2025-2045

- 1.9.7. Regional share of LDES value market percent in four regions 2025-2045.

- 1.9.8. LDES market in 9 technology categories $ billion 2025-2045 table, graphs, explanation

- 1.9.9. LDES total value market showing beyond-grid gaining share 2025-2045

- 1.9.10. Total pumped hydro storage market including LDES $ billion 2023-2045

2. Introduction

- 2.1. Overview

- 2.2. Battery limitations

- 2.3. How lithium-ion battery fires are ongoing

- 2.4. Megatrends of electrification, battery adoption and battery elimination

- 2.5. Implications for storage 2025 - 2045

- 2.6. Duration vs power of many battery and batteryless stationary storage technologies deployed and deploying in 2025 showing future trends

- 2.7. How batteries will lose share 2025-2045

3. Systems that eliminate batteries: backscatter (EAS, RFID, 6G SWIPT), battery elimination circuits, self-powering ultra-low-power circuits and sensors, demand and supply management

- 3.1. Overview

- 3.1.1. Battery elimination options beyond drop-in replacement by battery-less storage devices

- 3.1.2. Strategies to achieve less or no storage

- 3.1.3. Enablers of self-powered, battery-free devices that can be combined

- 3.2. Backscatter with SWOT

- 3.2.1. Electronic Article Surveillance EAS , passive RFID and beyond

- 3.2.2. SWIPT AmBC and CD-ZED for 6G Communications and IOT

- 3.2.3. SWOT and 34 other advances in 2024, 2023

- 3.3. Circuit design to minimise batteries

- 3.3.1. Battery elimination circuits BEC in drones and electric cars

- 3.3.2. Intermittency tolerant electronics: BFree

- 3.4. Battery elimination by V2G, V2H, V2V and vehicle charging directly from solar panels

- 3.5. Demand management: storage-free solar desalinators in 2024

- 3.6. Source management: advances in 2024

- 3.7. Specification compromise eliminates batteries

- 3.7.1. Battery-free drones as sensors and IOT

- 3.7.2. Battery-free cameras

- 3.8. Energy harvesting eliminating batteries

- 3.8.1. Overview and 13 primary energy harvesting technologies compared

- 3.8.2. Elements of a harvesting system

- 3.8.3. Mechanical harvesting including acoustic in detail

- 3.8.4. Harvesting of electromagnetic energy in detail

- 3.8.5. Importance of flexible laminar energy harvesting 2025-2045

- 3.8.6. Advances in 2024

4. Electrostatic storage: Supercapacitors, pseudocapacitors, lithium-ion capacitors, other BSH

- 4.1. The place of capacitors and their variants

- 4.2. Spectrum of choice - capacitor to supercapacitor to battery

- 4.3. Research pipeline: pure supercapacitors

- 4.4. Research pipeline: hybrid approaches

- 4.5. Research pipeline: pseudocapacitors

- 4.6. Actual and potential major applications of supercapacitors and their derivatives

- 4.6.1. Overview

- 4.6.2. Aircraft and aerospace

- 4.6.3. Electric vehicles: AGV, material handling, car, truck, bus, tram, train

- 4.6.4. Grid, microgrid, peak shaving, renewable energy and uninterrupted power supplies

- 4.6.5. Medical and wearables

- 4.6.6. Military: Laser cannon, railgun, pulsed linear accelerator weapon, radar, trucks, other

- 4.6.7. Power and signal electronics, data centers

- 4.6.8. Welding

- 4.7 103 supercapacitor companies assessed in 10 columns

- 4.8. Lithium-ion capacitors and other battery-supercapacitor hybrid BSH storage

- 4.8.1. Definitions and choices

- 4.8.2. BSH market positioning and choices and LIC market positioning by energy density spectrum

- 4.8.3. Infograms: the most impactful market needs, comparative solutions, 13 conclusions

- 4.8.4. Research analysis and recommendations 2025-2045

- 4.8.5. Two SWOT appraisals and roadmap 2025-2045

5. Liquefied gas energy storage LGES: Liquid air LAES or CO2

- 5.1. Overview

- 5.2. Liquid air LAES LDES

- 5.2.1. Technology

- 5.2.2. Research advances in 2024

- 5.2.3. CGDG China

- 5.2.4. Highview Energy UK

- 5.2.5. Sumitomo SHI FW Japan and China

- 5.2.6. Phelas Germany

- 5.2.7. SWOT appraisal of LAES for LDES

- 5.2.8. Parameter comparison of LAES for LDES

- 5.3. Liquid carbon dioxide LDES

- 5.3.1. Research advances in 2024

- 5.3.2. Energy Dome Italy

- 5.3.3. SWOT appraisal of Liquid CO2 for LDES

6. Compressed air CAES

- 6.1. Overview

- 6.1.1. Basics

- 6.1.2. System design

- 6.1.3. Research advances in 2024

- 6.2. Undersupply attracts clones

- 6.3. Market positioning of CAES

- 6.4. Parameter appraisal of CAES vs LAES

- 6.5. CAES technology options

- 6.5.1. Thermodynamic

- 6.4.2. Isochoric or isobaric storage

- 6.4.3. Adiabatic choice of cooling

- 6.6. CAES manufacturers, projects, research

- 6.6.1. Overview

- 6.6.2. Siemens Energy Germany

- 6.6.3. MAN Energy Solutions Germany

- 6.6.4. Increasing the CAES storage time and discharge duration

- 6.6.5. Research in UK and European Union

- 6.7. CAES profiles and appraisal of system designers and suppliers

- 6.7.1. ALCAES Switzerland

- 6.7.2. APEX CAES USA

- 6.7.3. Augwind Energy Israel

- 6.7.4. Cheesecake Energy UK

- 6.7.5. Corre Energy Netherlands

- 6.7.6. Gaelectric failure Ireland - lessons

- 6.7.7. Huaneng Group China

- 6.7.8. Hydrostor Canada

- 6.7.9. LiGE Pty South Africa

- 6.7.10. Storelectric UK

- 6.7.11. Terrastor Energy Corporation USA

- 6.8. SWOT appraisal of CAES for LDES

7. Mechanical storage: Advanced pumped hydro APHES, solid gravity energy storage SGES, flywheels for electricity-to-electricity

- 7.1. Advanced pumped hydro APHES

- 7.1.1. Overview and SWOT appraisal

- 7.1.2. Research advances in 2024

- 7.1.3. Pressurised underground: Quidnet Energy USA

- 7.1.4. Mine storage in USA (EDF) and Sweden (Mine Storage Co.)

- 7.1.5. Heavy liquid up mere hills RheEnergise UK

- 7.1.6. S-PHES from the sea to land and using sea dams:

- 7.1.7. Research advances in 2024

- 7.1.8. Sea floor StEnSea Germany, Ocean Grazer Netherlands compared with other underwater LDES

- 7.1.9. SWOT appraisal of underwater energy storage for LDES

- 7.1.10. Brine in salt caverns Cavern Energy USA

- 7.1.11. Conventional pumped hydro: Research advances in 2024, parameter appraisal, SWOT

- 7.2. Solid gravity energy storage SGES

- 7.2.1. Overview

- 7.2.2. Parameter appraisal of SGES for LDES

- 7.2.3. Energy Vault Switzerland

- 7.2.4. SWOT appraisal of SGES for LDES

- 7.3. Flywheels for electricity-to-electricity

- 7.3.1. Overview

- 7.3.2. Amber Kinetics USA

- 7.3.3. Beacon Power USA

- 7.3.4. Torus USA

8. Hydrogen and other chemical intermediary LDES

- 8.1. Overview

- 8.1.1. Hydrogen past and present: successes and failures

- 8.1.2. The proposal of a hydrogen economy: 2024 research advances

- 8.1.3. The UK as an example of contention

- 8.1.4. Wide spread of parameters means interpretation should be cautious

- 8.1.5. How hydrogen is both partner and alternative to electrification

- 8.2. Sweet spot for chemical intermediary LDES

- 8.3 53 research advances reported in 2025 (pre-publication) and 2024

- 8.3.1. Introduction

- 8.3.2. New research on salt caverns, subsea and other options for large scale hydrogen storage

- 8.3.3. New research on complex mechanisms for hydrogen loss

- 8.3.4. New research on hydrogen leakage causing global warming

- 8.3.5. New research on combining grid hydrogen storage with other storage: hybrid systems

- 8.4. Hydrogen compared to methane and ammonia for LDES

- 8.5. Hydrogen LDES leader: Calistoga Resiliency Centre USA 48-hour hydrogen LDES

- 8.6. Calculations finding that hydrogen will win for longest term LDES

- 8.7. Mining giants prudently progress many options

- 8.8. Buildings and other small locations

- 8.9. Technologies for hydrogen storage

- 8.9.1. Overview

- 8.9.2. Choices of underground storage for LDES hydrogen

- 8.9.3. Hydrogen interconnectors for electrical energy transmission and storage

- 8.10. Parameter appraisal of hydrogen storage for LDES

- 8.11. SWOT appraisal of hydrogen, methane, ammonia for LDES

9. Thermal energy storage for delayed electricity ETES

- 9.1. Overview

- 9.2. Research advances in 2024

- 9.3. The heat engine approach succeeds: Echogen USA

- 9.4. Use of extreme temperatures and photovoltaic conversion

- 9.4.1. Antora USA

- 9.4.2. Fourth Power USA

- 9.5. Marketing delayed heat and electricity from one plant

- 9.5.1. Overview

- 9.5.2. MGA Thermal Australia

- 9.5.3. Malta Inc Germany

- 9.6. SWOT appraisal of ETES for LDES

- 9.7. Parameter appraisal of electric thermal energy storage ETES

大容量電池市場 - 全球行業規模、佔有率、趨勢、機會和預測,細分,按類型、按應用、按最終用戶、按地區和競爭,2020-2030F2025年可再生能源儲存全球市場報告2025 年能源儲存系統系統全球市場報告

大容量電池市場 - 全球行業規模、佔有率、趨勢、機會和預測,細分,按類型、按應用、按最終用戶、按地區和競爭,2020-2030F2025年可再生能源儲存全球市場報告2025 年能源儲存系統系統全球市場報告 2024年下半年美國公用事業規模儲能展望

2024年下半年美國公用事業規模儲能展望 2025 年中東和非洲儲能展望

2025 年中東和非洲儲能展望 全球大容量電池市場:按類型、應用程式、最終用戶和地區分類能源領域無人機市場規模、佔有率、成長分析(按類型、組件、應用、能源來源、最終用戶和地區)- 產業預測,2025 年至 2032 年

全球大容量電池市場:按類型、應用程式、最終用戶和地區分類能源領域無人機市場規模、佔有率、成長分析(按類型、組件、應用、能源來源、最終用戶和地區)- 產業預測,2025 年至 2032 年 亞太地區能源儲存系統-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲能源儲存:市場佔有率分析、產業趨勢與成長預測(2025-2030)美國能源儲存:市場佔有率分析、產業趨勢與成長預測(2025-2030)

亞太地區能源儲存系統-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲能源儲存:市場佔有率分析、產業趨勢與成長預測(2025-2030)美國能源儲存:市場佔有率分析、產業趨勢與成長預測(2025-2030)