|

市場調查報告書

商品編碼

1664893

二手車融資市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Used Car Financing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

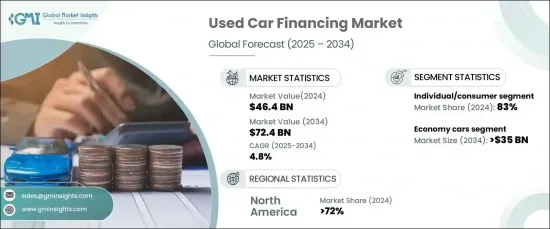

2024 年全球二手車融資市場估值達到 464 億美元,預計 2025 年至 2034 年期間將以 4.8% 的複合年成長率穩步成長。這些創新簡化了融資流程、增強了可近性並改善了整體消費者體驗。自動化系統也加快了貸款核准速度,提供了更快、更方便消費者的選擇。數位轉型正在提高市場效率和吸引力。

二手車需求的不斷成長是推動市場成長的關鍵因素。隨著新車成本不斷上漲,二手車已成為注重預算的消費者、首次購車者以及尋求經濟型交通解決方案的消費者的經濟實惠的替代品。這一趨勢反映了向價值驅動型購買的轉變,尤其是在經濟不確定性和生活費用上漲壓力日益增大的情況下。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 464億美元 |

| 預測值 | 724億美元 |

| 複合年成長率 | 4.8% |

市場分為經濟型轎車、豪華轎車和 SUV/跨界車。 2024年經濟型汽車將引領市場,佔總佔有率的52%。預計到 2034 年,這些汽車將因其經濟實惠、實用性和燃油效率而創造 350 億美元的收入。它們在注重預算的消費者中很受歡迎,凸顯了對可靠而又經濟高效的交通選擇的需求日益成長,尤其是在經濟波動期間。

就最終用途而言,市場分為個人消費者和企業/商業用戶。 2024 年,個人消費者將佔據該領域的主導地位,佔有 83% 的佔有率。對於個人買家來說,經濟承受能力仍然是主要動機,他們傾向於購買二手車,將其作為應對新車價格上漲和資金限制的可行解決方案。這些買家優先考慮具有成本效益的選擇,這些選擇既可靠又能滿足他們的日常旅行需求,而且不需要超出他們的預算。

2024 年,北美二手車融資市場佔有 72% 的佔有率。郊區和農村地區公共交通選擇有限進一步凸顯了對私家車的依賴。隨著負擔能力成為主要考慮因素,越來越多的消費者選擇二手車,從而維持了整個地區對融資解決方案的強勁需求。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 貸款人

- 經銷商和網路平台

- 保險提供者

- 支付和技術提供者

- 最終用戶

- 供應商概況

- 利潤率分析

- 技術與創新格局

- 專利分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 消費者對二手車的需求不斷成長

- 融資選擇日益增多

- 借貸平台和流程的技術創新

- 消費者偏好的改變

- 產業陷阱與挑戰

- 信用風險與貸款挑戰

- 二手車折舊率高

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按貸方,2021 - 2034 年

- 主要趨勢

- 銀行和信用合作社

- OEM/專屬融資

- 網路直接貸款人

- 經銷商內部融資

第6章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 經濟型轎車

- 豪華轎車

- SUV/跨界車

第7章:市場估計與預測:依貸款期限,2021 - 2034 年

- 主要趨勢

- 短期(12-36個月)

- 中期(37-60個月)

- 長期(61-84個月)

- 長期(超過 84 個月)

第 8 章:市場估計與預測:按最終用途,2021 - 2034 年

- 主要趨勢

- 個人/消費者

- 企業/商業

第 9 章:市場估計與預測:按車齡,2021 - 2034 年

- 主要趨勢

- 較新(最多 3 年)

- 年齡較大(4 歲以上)

第 10 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第 11 章:公司簡介

- Ally Financial

- AmeriCredit

- AutoCreditExpress

- AutoNation

- Bank of America Auto Loans

- Capital One Auto Finance

- CarMax

- CarsDirect

- Carvana

- Chase Auto

- Credit Union Direct Lending (CUDL)

- DriveTime

- LightStream (a division of SunTrust Bank)

- OpenRoad Lending

- PenFed Credit Union

- RoadLoans

- Santander Consumer USA

- TD Auto Finance

- US Bank Auto Loans

- Wells Fargo Auto

The Global Used Car Financing Market achieved a valuation of USD 46.4 billion in 2024 and is projected to expand at a steady CAGR of 4.8% from 2025 to 2034. This growth is underpinned by rapid advancements in lending technologies, including digital platforms and mobile applications, which are revolutionizing the sector. These innovations streamline the financing process, enhance accessibility, and improve the overall consumer experience. Automated systems have also expedited loan approvals, offering faster, more consumer-friendly options. This digital transformation is driving greater market efficiency and appeal.

The rising demand for used vehicles is a key factor propelling market growth. As the cost of new cars continues to rise, pre-owned vehicles have emerged as an affordable alternative for budget-conscious consumers, first-time car buyers, and those seeking economical transportation solutions. This trend reflects a shift toward value-driven purchases, especially amidst economic uncertainties and the growing pressures of rising living expenses.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $46.4 Billion |

| Forecast Value | $72.4 Billion |

| CAGR | 4.8% |

The market is segmented into economy cars, luxury cars, and SUVs/crossovers. Economy cars led the market in 2024, accounting for 52% of the total share. These vehicles are projected to generate USD 35 billion by 2034, driven by their affordability, practicality, and fuel efficiency. Their popularity among budget-conscious consumers underscores the increasing demand for reliable yet cost-effective transportation options, especially during economic fluctuations.

In terms of end use, the market is divided into individual consumers and businesses/commercial users. Individual consumers dominated the segment in 2024, capturing an 83% share. Affordability remains the primary motivator for personal buyers, who are gravitating toward pre-owned vehicles as a viable solution to rising new car prices and financial constraints. These buyers prioritize cost-effective options that deliver reliability and meet their daily mobility needs without stretching their budgets.

North America used car financing market held a commanding 72% share in 2024. The region's strong car ownership culture, coupled with a high demand for personal mobility, continues to drive market growth. Limited public transportation options in suburban and rural areas further underscore the reliance on private vehicles. With affordability emerging as a key concern, consumers are increasingly opting for pre-owned vehicles, sustaining robust demand for financing solutions across the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Lenders

- 3.1.2 Dealers and online platforms

- 3.1.3 Insurance providers

- 3.1.4 Payment and technology providers

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising consumer demand for used cars

- 3.8.1.2 Growing access to financing options

- 3.8.1.3 Technological innovations in lending platforms and processes

- 3.8.1.4 Changing consumer preferences

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Credit risk and lending challenges

- 3.8.2.2 High depreciation of used cars

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Lender, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Banks and credit unions

- 5.3 OEM/captive financing

- 5.4 Online direct lenders

- 5.5 Dealership in-house financing

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Economy cars

- 6.3 Luxury cars

- 6.4 SUVs/crossovers

Chapter 7 Market Estimates & Forecast, By Loan Duration, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Short-term (12-36 months)

- 7.3 Medium-term (37-60 months)

- 7.4 Long-term (61-84 months)

- 7.5 Extended-term (over 84 months)

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Individuals/consumers

- 8.3 Businesses/commercial

Chapter 9 Market Estimates & Forecast, By Age of Vehicle, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Newer (upto 3 years)

- 9.3 Older (4 years and above)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Ally Financial

- 11.2 AmeriCredit

- 11.3 AutoCreditExpress

- 11.4 AutoNation

- 11.5 Bank of America Auto Loans

- 11.6 Capital One Auto Finance

- 11.7 CarMax

- 11.8 CarsDirect

- 11.9 Carvana

- 11.10 Chase Auto

- 11.11 Credit Union Direct Lending (CUDL)

- 11.12 DriveTime

- 11.13 LightStream (a division of SunTrust Bank)

- 11.14 OpenRoad Lending

- 11.15 PenFed Credit Union

- 11.16 RoadLoans

- 11.17 Santander Consumer USA

- 11.18 TD Auto Finance

- 11.19 U.S. Bank Auto Loans

- 11.20 Wells Fargo Auto

菲律賓二手車:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

菲律賓二手車:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 二手卡車市場規模、佔有率及成長分析(按車型、最終用戶、通路和地區)-2025-2032 年產業預測

二手卡車市場規模、佔有率及成長分析(按車型、最終用戶、通路和地區)-2025-2032 年產業預測 2025年全球二手卡車市場報告二手半拖車市場 - 全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、推進類型、銷售管道、地區和競爭細分,2020-2030 年預測2025 年全球二手車市場報告2030 年二手車市場預測:按車型、價格分佈、車齡、最終用戶和地區進行全球分析

2025年全球二手卡車市場報告二手半拖車市場 - 全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、推進類型、銷售管道、地區和競爭細分,2020-2030 年預測2025 年全球二手車市場報告2030 年二手車市場預測:按車型、價格分佈、車齡、最終用戶和地區進行全球分析 二手卡車市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測二手車市場規模、佔有率、成長分析、按車輛類型、按供應商類型、按燃料類型、按銷售管道、按地區 - 行業預測,2024-2031 年

二手卡車市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測二手車市場規模、佔有率、成長分析、按車輛類型、按供應商類型、按燃料類型、按銷售管道、按地區 - 行業預測,2024-2031 年 二手車市場:按車輛類型、燃料類型、分銷管道分類 - 2025-2030 年全球預測二手車市場規模、佔有率、趨勢分析報告:按車型、供應商、燃料類型、規模、銷售管道、地區、細分趨勢,2025-2030

二手車市場:按車輛類型、燃料類型、分銷管道分類 - 2025-2030 年全球預測二手車市場規模、佔有率、趨勢分析報告:按車型、供應商、燃料類型、規模、銷售管道、地區、細分趨勢,2025-2030