|

市場調查報告書

商品編碼

1665222

直視 LED 顯示器市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Direct View LED Display Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

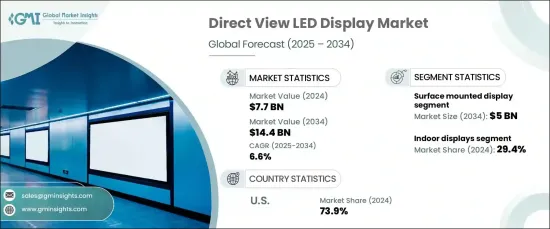

2024 年全球直視 LED 顯示器市場規模達到 77 億美元,預計 2025 年至 2034 年期間將以 6.6% 的強勁複合年成長率成長。 DVLED 顯示器以其提供生動的視覺效果、無縫的性能和卓越的耐用性而聞名,正在成為各種室內和室外應用的首選解決方案。

2024 年,室內顯示器將成為市場領導者,佔 29.4% 的佔有率。其清晰的解析度、精確的色彩準確度和美觀性使其在企業環境、零售空間和娛樂場所的應用中備受追捧。室內 DVLED 系統採用更精細的像素間距和最佳化的亮度等級設計,範圍從 500 到 1,500 個單位,提供無與倫比的視覺清晰度,滿足這些高階產業的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 77億美元 |

| 預測值 | 144億美元 |

| 複合年成長率 | 6.6% |

在技術方面,由於其緊湊的設計和卓越的耐用性,表面貼裝顯示器預計到 2034 年將產生 50 億美元的市場價值。這些顯示器利用表面貼裝設備 (SMD) 技術,將 LED 晶片直接整合到電路板中,從而提高了亮度、色彩一致性和整體性能。這項先進技術非常適合室內和室外安裝,包括動態數位看板和大尺寸顯示器。

2024 年,美國市場引領全球 DVLED 市場,佔有高達 73.9% 的市佔率。這種主導地位很大程度上歸因於 DVLED 顯示器在零售、娛樂和商業領域的日益普及。零售商擴大利用這些顯示器來實現動態店內標牌,創造引人入勝的客戶體驗,同時增強視覺吸引力。在城市地區,戶外廣告正在經歷數位轉型,靜態廣告看板讓位給引人注目的數位替代品。娛樂產業也採用 DVLED 技術在體育場館、音樂會場館和活動場所創造身臨其境的體驗。

隨著對視覺衝擊力大、節能的顯示解決方案的需求不斷成長,DVLED 市場必將蓬勃發展。像素密度和智慧功能整合的技術進步正在推動創新並擴大應用。由於應用範圍涵蓋各個領域,直覺 LED 顯示器市場在預測期內將實現顯著成長並帶來變革性影響。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 對高品質視覺體驗的需求日益增加

- 成本下降和技術進步

- 戶外廣告和數位看板的採用日益廣泛

- 互動式顯示器日益流行

- 產業陷阱與挑戰

- 初期投資及維護成本高

- 技術挑戰和複雜整合

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按顯示類型,2021 年至 2034 年

- 主要趨勢

- 室內顯示幕

- 戶外顯示器

- 體育場螢幕

- 數位看板

第 6 章:市場估計與預測:按技術,2021 年至 2034 年

- 主要趨勢

- 表面貼裝顯示器

- 板載晶片顯示

- MicroLED 顯示器

- 量子點顯示器

第 7 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 廣告

- 運動的

- 運輸

- 零售

- 廣播

第 8 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 政府

- 商業的

- 教育

- 住宅

第 9 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Absen

- AOTO Electronics

- Barco NV

- Christie Digital Systems

- Daktronics

- Delta Electronics

- INFiLED

- Ledman Optoelectronic

- Leyard Optoelectronic

- LG Electronics

- Lighthouse Technologies

- NEC Display Solutions

- Planar Systems

- ROE Visual

- Samsung Electronics

- Shenzhen Absen Optoelectronic

- Shenzhen Liantronics

- SiliconCore Technology

- Unilumin Group

- Yaham Optoelectronics

The Global Direct View LED Display Market reached USD 7.7 billion in 2024 and is anticipated to grow at a robust CAGR of 6.6% from 2025 to 2034. The increasing demand for high-resolution, energy-efficient displays is fueling this growth across commercial, entertainment, and retail sectors. Renowned for their ability to deliver vibrant visuals, seamless performance, and exceptional durability, DVLED displays are becoming the go-to solution for a wide range of indoor and outdoor applications.

In 2024, indoor displays emerged as the market leader, capturing a 29.4% share. Their sharp resolution, precise color accuracy, and aesthetic appeal make them highly sought after for applications in corporate environments, retail spaces, and entertainment venues. Designed with finer pixel pitches and optimized brightness levels ranging from 500 to 1,500 units, indoor DVLED systems offer unmatched visual clarity, meeting the demands of these high-profile sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.7 Billion |

| Forecast Value | $14.4 Billion |

| CAGR | 6.6% |

On the technology front, surface-mounted displays are projected to generate USD 5 billion by 2034, driven by their compact design and superior durability. Leveraging Surface Mounted Device (SMD) technology, these displays feature LED chips directly integrated into circuit boards, enhancing brightness, color consistency, and overall performance. This advanced technology is ideal for both indoor and outdoor installations, including dynamic digital signage and large-format displays.

The U.S. market led the global DVLED landscape in 2024, holding an impressive 73.9% share. This dominance is largely attributed to the growing adoption of DVLED displays across retail, entertainment, and commercial sectors. Retailers are increasingly leveraging these displays for dynamic in-store signage, creating engaging customer experiences while enhancing visual appeal. In urban areas, outdoor advertising is undergoing a digital transformation as static billboards give way to eye-catching digital alternatives. The entertainment industry is also embracing DVLED technology to create immersive experiences in sports arenas, concert venues, and event spaces.

As the demand for visually striking, energy-efficient display solutions continues to rise, the DVLED market is set to flourish. Technological advancements in pixel density and the integration of smart features are driving innovation and expanding adoption. With applications spanning diverse sectors, the direct view LED display market is poised for significant growth and transformative impact over the forecast period.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for high-quality visual experiences

- 3.6.1.2 Declining costs and technological advancements

- 3.6.1.3 Growing adoption in outdoor advertising and digital signage

- 3.6.1.4 Rising popularity of interactive displays

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial investment and maintenance costs

- 3.6.2.2 Technical challenges and complex integration

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Display Type, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Indoor displays

- 5.3 Outdoor displays

- 5.4 Stadium screens

- 5.5 Digital signage

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Surface mounted display

- 6.3 Chip on board display

- 6.4 MicroLED display

- 6.5 Quantum dot display

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 Advertising

- 7.3 Sports

- 7.4 Transportation

- 7.5 Retail

- 7.6 Broadcasting

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Government

- 8.3 Commercial

- 8.4 Educational

- 8.5 Residential

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Absen

- 10.2 AOTO Electronics

- 10.3 Barco NV

- 10.4 Christie Digital Systems

- 10.5 Daktronics

- 10.6 Delta Electronics

- 10.7 INFiLED

- 10.8 Ledman Optoelectronic

- 10.9 Leyard Optoelectronic

- 10.10 LG Electronics

- 10.11 Lighthouse Technologies

- 10.12 NEC Display Solutions

- 10.13 Planar Systems

- 10.14 ROE Visual

- 10.15 Samsung Electronics

- 10.16 Shenzhen Absen Optoelectronic

- 10.17 Shenzhen Liantronics

- 10.18 SiliconCore Technology

- 10.19 Unilumin Group

- 10.20 Yaham Optoelectronics

2025-2029年全球發光二極體(LED)市場

2025-2029年全球發光二極體(LED)市場 封裝 GaN LED 全球市場報告:趨勢、預測和競爭分析(至 2031 年)

封裝 GaN LED 全球市場報告:趨勢、預測和競爭分析(至 2031 年) LED 智慧燈帶市場:類型、類別、顏色、長度、連接性、分銷管道、應用、最終用途 - 2025 年至 2030 年全球預測

LED 智慧燈帶市場:類型、類別、顏色、長度、連接性、分銷管道、應用、最終用途 - 2025 年至 2030 年全球預測 2025年高亮度LED全球市場報告

2025年高亮度LED全球市場報告 PLED 市場規模、佔有率及成長分析(按產品類型、應用和地區)- 2025 年至 2032 年產業預測

PLED 市場規模、佔有率及成長分析(按產品類型、應用和地區)- 2025 年至 2032 年產業預測 GaN LED 晶片市場機會、成長動力、產業趨勢分析及 2025-2034 年預測

GaN LED 晶片市場機會、成長動力、產業趨勢分析及 2025-2034 年預測 全球二極體:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)小訊號二極體:全球市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)2024-2032 年日本高亮度 LED 市場報告(按應用(汽車照明、普通照明、背光、移動設備、訊號和標誌等)和地區)LED模組市場機會、成長動力、產業趨勢分析及2024 - 2032年預測

全球二極體:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)小訊號二極體:全球市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)2024-2032 年日本高亮度 LED 市場報告(按應用(汽車照明、普通照明、背光、移動設備、訊號和標誌等)和地區)LED模組市場機會、成長動力、產業趨勢分析及2024 - 2032年預測